Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market reached approximately USD ~ billion based on a recent historical assessment derived from agricultural machinery population, replacement cycles, and spare parts consumption benchmarks reported by the Ministry of Agriculture and industry associations such as FICCI and CII. Demand is driven by a large installed base of tractors and harvesters requiring periodic maintenance, rising mechanization intensity, and increasing use of genuine OEM components to maintain equipment performance and resale value.

Major activity centers are concentrated in Punjab, Haryana, Uttar Pradesh, Maharashtra, and Tamil Nadu due to dense tractor ownership, intensive cropping cycles, and extensive dealer and distributor networks. Cities such as Ludhiana, Karnal, Kanpur, Pune, and Coimbatore function as manufacturing and distribution hubs for spare parts and MRO services. These regions host strong agro-machinery ecosystems, component suppliers, and logistics connectivity, enabling efficient aftermarket supply chains and rapid parts availability for mechanized farming clusters.

Market Segmentation

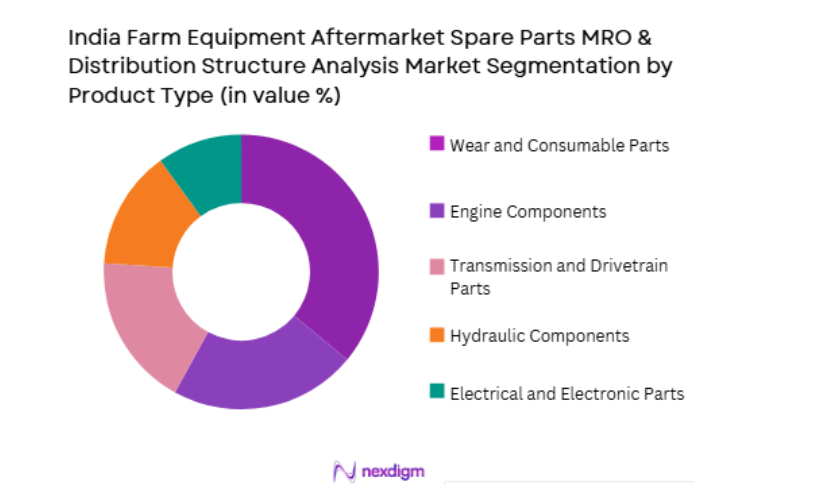

By Product Type

India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market is segmented by product type into engine components, transmission and drivetrain parts, hydraulic components, wear and consumable parts, and electrical and electronic parts. Recently, wear and consumable parts has a dominant market share due to factors such as high replacement frequency, exposure to soil abrasion and crop residue, and routine servicing requirements across all farm equipment categories. Filters, belts, blades, bearings, and lubrication components require periodic replacement regardless of tractor age, ensuring sustained demand across both organized and unorganized aftermarket channels.

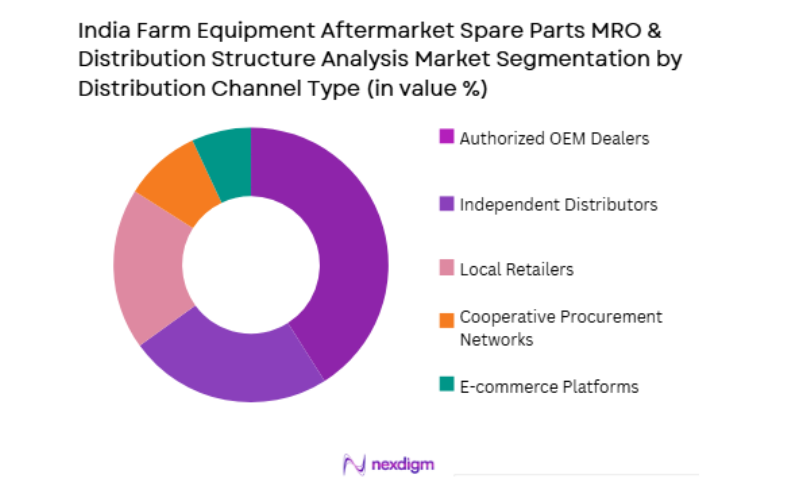

By Distribution Channel

India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market is segmented by distribution channel into authorized OEM dealers, independent distributors, local retailers, e-commerce platforms, and cooperative procurement networks. Recently, authorized OEM dealers has a dominant market share due to factors such as trust in genuine parts quality, warranty compliance requirements, and integration with scheduled maintenance services. Farmers prefer dealer-supplied components to ensure compatibility with specific tractor models and maintain resale value, particularly for high-value machinery and newer equipment fleets.

Competitive Landscape

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market is moderately fragmented with strong influence from OEM-affiliated dealer networks and large component manufacturers supplying both genuine and replacement parts. Major tractor manufacturers control organized aftermarket channels through authorized dealerships, while independent distributors and regional suppliers dominate price-sensitive rural markets. Consolidation is gradually increasing as OEMs expand branded spare parts programs and digital distribution platforms, strengthening control over parts quality, availability, and service ecosystems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Size |

| Mahindra & Mahindra Farm Equipment | 1945 | India | ~ | ~ | ~ | ~ | ~ |

| TAFE | 1960 | India | ~ | ~ | ~ | ~ | ~ |

| Escorts Kubota | 1944 | India | ~ | ~ | ~ | ~ | ~ |

| TVS Motor Components Division | 1978 | India | ~ | ~ | ~ | ~ | ~ |

| Bosch Mobility India | 1951 | India | ~ | ~ | ~ | ~ | ~ |

India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure Analysis Market Analysis

Growth Drivers

Expanding Installed Base of Tractors and Mechanized Farm Equipment

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market is strongly driven by the large and continuously growing population of tractors, harvesters, and mechanized implements operating across diverse agricultural regions. India maintains one of the world’s largest tractor fleets, and each unit generates recurring demand for maintenance, repair, and overhaul components throughout its operational life cycle. Aging machinery increases frequency of part replacement, particularly for engine, transmission, and hydraulic systems subject to wear under heavy field conditions. Intensive cropping patterns and multi-season usage accelerate component fatigue, raising aftermarket consumption per machine annually. Farmers prioritize maintaining operational reliability during critical planting and harvesting windows, which sustains consistent demand for spare parts availability and service infrastructure. Expansion of mechanization into previously low-equipment regions increases the installed base and creates new aftermarket demand clusters. Government mechanization subsidies and rural credit access support equipment ownership, indirectly expanding long-term spare parts consumption potential. Rising use of high-horsepower tractors and advanced implements also increases complexity and value of replacement components required during maintenance cycles.

Shift Toward Genuine OEM Parts and Organized Aftermarket Channels

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market is increasingly influenced by farmer preference for genuine OEM components and structured service networks rather than unbranded local replacements. Modern tractors incorporate tighter engineering tolerances and integrated hydraulic and electronic systems that require precise component compatibility, encouraging use of manufacturer-approved spare parts. Warranty conditions and resale value considerations motivate farmers to procure parts through authorized dealers rather than informal suppliers. OEMs actively promote branded spare parts programs and service packages to retain aftermarket revenue and ensure quality control across their installed equipment fleets. Organized dealer networks provide technical expertise, diagnostics, and maintenance scheduling that improve machine longevity and operational efficiency, strengthening farmer loyalty. Rising awareness of lifecycle cost benefits associated with genuine parts reduces price sensitivity in higher-value equipment segments. Digital inventory management and logistics integration enable dealers to maintain part availability across rural regions, enhancing service reliability. OEM-led training for mechanics and service technicians supports standardized repair practices aligned with genuine component usage.

Market Challenges

Prevalence of Unorganized Local Spare Parts Markets and Price Competition

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market faces significant challenges from widespread unorganized spare parts manufacturing and distribution networks that compete aggressively on price. Numerous small-scale component producers supply low-cost replacement parts without standardized quality assurance, attracting price-sensitive farmers operating under tight income constraints. Informal rural retailers and repair workshops often prioritize affordability and immediate availability over durability or OEM compatibility, diverting demand from authorized distribution channels. Counterfeit and imitation components further erode trust in organized aftermarket ecosystems and create safety and performance risks for farm equipment. OEM dealers struggle to compete in rural markets where purchasing decisions are driven primarily by upfront cost rather than lifecycle value or warranty compliance. Limited enforcement of intellectual property protection and quality standards enables continued circulation of non-genuine components. Farmers using older tractors often perceive limited benefit in investing in higher-cost OEM parts, sustaining demand for low-cost substitutes. Fragmented rural supply chains and local manufacturing clusters make monitoring and regulation difficult for authorities and OEMs. This pervasive unorganized competition suppresses pricing power and margins for structured aftermarket distributors.

Logistics Complexity and Parts Availability Across Dispersed Rural Markets

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market is challenged by the logistical difficulty of ensuring timely spare parts availability across geographically dispersed and infrastructure-constrained agricultural regions. Farm machinery breakdowns often occur in remote villages far from major distribution centers, requiring efficient last-mile delivery systems that remain underdeveloped in many states. Seasonal demand spikes during sowing and harvesting periods create inventory planning challenges for distributors and dealers attempting to maintain adequate stock levels. High product variety across multiple tractor brands and model generations increases inventory complexity and storage requirements for aftermarket suppliers. Rural transport limitations, poor road connectivity, and fragmented logistics networks delay part delivery and machine repair turnaround times. Dealers must balance inventory costs against service responsiveness, often resulting in stockouts or delayed procurement from central warehouses. Reverse logistics for defective or returned parts is also inefficient in rural environments, increasing operational cost for distributors. Cold storage or controlled environments required for certain electronic or hydraulic components are rarely available in rural distribution points. Limited digital supply chain integration across independent distributors further reduces visibility into demand patterns and inventory movement.

Opportunities

Digital Aftermarket Platforms and E-Commerce Distribution Integration

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market presents strong opportunity through digitalization of spare parts discovery, ordering, and distribution using e-commerce and platform-based supply chains. Online marketplaces dedicated to agricultural components can connect farmers, mechanics, and retailers directly with OEM and certified suppliers, improving part authenticity and availability. Digital catalogs with tractor model compatibility mapping reduce identification errors and enable faster procurement decisions for replacement components. Integrated logistics networks can deliver spare parts directly to villages, overcoming physical dealer access limitations and improving service responsiveness. Mobile applications in regional languages enhance usability for farmers and rural mechanics, expanding digital adoption in aftermarket purchasing. OEMs can leverage digital platforms to extend branded spare parts programs into underserved rural markets without establishing physical dealerships. Data analytics from online transactions provides demand forecasting insights and inventory optimization for distributors and manufacturers. Digital warranty validation and service history tracking strengthen trust in genuine parts ecosystems. E-commerce also enables small retailers to access broader product portfolios from centralized warehouses, enhancing competitiveness against informal suppliers.

Expansion of Mechanization Service Networks and Preventive Maintenance Programs

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market can expand through structured mechanization service networks and preventive maintenance programs that institutionalize spare parts consumption. Custom hiring centers, mechanization cooperatives, and fleet service providers operate multiple farm machines and require standardized maintenance schedules, creating predictable aftermarket demand streams. Preventive service contracts bundled with equipment financing encourage periodic replacement of wear components, increasing spare parts utilization and equipment uptime. OEM-led annual maintenance packages and extended warranty programs drive recurring genuine parts consumption through authorized channels. Service networks also provide professional diagnostics and repair capabilities, increasing reliance on quality components rather than local substitutes. Training of rural mechanics under OEM certification programs promotes standardized service practices aligned with genuine spare parts usage. Fleet-based agricultural operations such as contract farming and commercial plantations prioritize maintenance reliability, expanding demand for organized aftermarket supply chains. Integration of telematics and usage monitoring enables predictive maintenance scheduling and proactive parts replacement.

Future Outlook

The India Farm Equipment Aftermarket Spare Parts MRO & Distribution Structure market is expected to grow steadily as mechanization intensity and tractor population continue expanding. Digital spare parts platforms and OEM-branded distribution networks will improve availability and authenticity. Preventive maintenance programs and service-based mechanization models will stabilize recurring demand. Logistics modernization and rural connectivity improvements will enhance distribution efficiency. Formalization of aftermarket channels will gradually shift share toward organized suppliers.

Major Players

- Mahindra & Mahindra Farm Equipment

- TAFE

- Escorts Kubota

- TVS Motor Components Division

- Bosch Mobility India

- CNH Industrial India

- John Deere India

- Kubota Agricultural Machinery India

- Yanmar Agricultural Equipment India

- Sona Comstar

- Gabriel India

- Uno Minda

- SKF India

- Timken India

- Mahle India

Key Target Audience

- Agricultural equipment manufacturers

- Spare parts distributors and wholesalers

- Rural mechanization service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural cooperatives

- Farm equipment dealerships

- Component manufacturing companies

Research Methodology

Step 1: Identification of Key Variables

Key variables including tractor population, replacement cycles, spare parts consumption rates, and distribution channel structure were identified through agricultural mechanization datasets and industry association reports. Product lifecycle parameters and service frequency benchmarks were defined to frame aftermarket demand drivers.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed by mapping installed farm equipment base with average annual spare parts expenditure per machine across categories. Distribution channel shares and regional demand clusters were derived from dealer network data and mechanization intensity patterns.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding spare parts demand frequency, channel dominance, and logistics constraints were validated through consultation with farm equipment dealers, distributors, and agricultural service professionals. Findings were cross-checked against industry studies and OEM aftermarket programs.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, distribution structure, and growth dynamics. Consistency checks ensured alignment with tractor population trends and mechanization expansion, producing the final market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expanding installed base of tractors and farm machinery

Rising equipment utilization and maintenance cycles

Growth of rural distribution and service networks - Market Challenges

High prevalence of counterfeit and low-quality parts

Fragmented distribution and supply chain inefficiencies

Price sensitivity among smallholder farmers - Market Opportunities

Expansion of organized aftermarket distribution chains

Growth of digital spare parts procurement platforms

Development of remanufacturing and refurbishment services - Trends

Shift toward branded aftermarket parts adoption

Increasing dealer-led service and maintenance contracts

Integration of digital inventory and logistics systems - Government regulations

Quality and certification norms for farm machinery components

GST standardization across spare parts supply chains

Right to repair and rural service infrastructure policies - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Engine and Powertrain Spare Parts

Hydraulic and Transmission Components

Electrical and Electronic Parts

Wear and Consumable Parts

Implement and Attachment Parts - By Platform Type (In Value%)

Tractor Aftermarket Parts

Harvester Aftermarket Parts

Tillage Equipment Parts

Planting and Seeding Equipment Parts

Crop Protection Equipment Parts - By Fitment Type (In Value%)

OEM Genuine Parts Replacement

Aftermarket Branded Parts

Unbranded Local Parts

Remanufactured Components

Refurbished Assemblies - By End User Segment (In Value%)

Smallholder Farmers

Large Commercial Farms

Custom Hiring Centers

- Market Share Analysis

- Cross Comparison Parameters (Part Quality Tier, Distribution Reach, Price Positioning, OEM Affiliation, Product Range Breadth, Authorized dealer network, Dealer & distributor hybrid, Authorized dealers, Multi-brand distributors,)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Mahindra & Mahindra Farm Equipment Parts Division

TAFE Genuine Parts

Escorts Kubota Agri Parts

Sonalika Spare Parts Division

John Deere India Parts

CNH Industrial Parts and Service India

AGCO Parts India

Swaraj Genuine Parts

VST Tillers Tractors Parts

Shakti Farm Equipment Parts

Fieldking Implement Parts

Captain Tractors Spare Parts

Uniparts India

TVS Motor Company Agri Components

Bosch Automotive Aftermarket India

- Smallholder farmers relying on local low-cost spare parts channels

- Large farms preferring OEM and branded components for reliability

- Custom hiring centers requiring frequent maintenance cycles

- Dealers and workshops acting as primary distribution interface

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now