Download PDF

Download PDFMarket Overview

The India food acidulants market was valued at USD ~ million in 2024 and is projected to expand at a CAGR of ~% during the 2026–2035 forecast period. According to data published by the Food Safety and Standards Authority of India (FSSAI) and the Ministry of Food Processing Industries (MoFPI), India’s food and beverage processing sector is among the largest in the world by output volume and is expanding rapidly as rising household incomes, urbanisation, and changing dietary preferences drive increasing demand for packaged, processed, and convenience food products across the country’s diverse regional markets. Food acidulants, encompassing organic and inorganic acids used to regulate pH, impart tartness, enhance flavour, extend shelf life, support preservation, facilitate specific food processing reactions such as paneer coagulation and dairy fermentation, and perform a range of other functional roles in food and beverage formulations, are among the most widely used food additive ingredient categories in India’s food manufacturing industry. Data from the Ministry of Food Processing Industries and industry associations indicates that demand for food acidulants has grown steadily alongside India’s expanding organised food manufacturing sector, driven by the rapid growth of the carbonated beverage, fruit juice, dairy processing, bakery, savoury snack, condiment, and convenience food segments. Growth is further supported by India’s large and growing domestic sugarcane molasses fermentation industry providing a cost-competitive raw material base for domestically produced citric and lactic acid, the FSSAI’s progressive tightening of food additive quality and labelling standards driving a structural shift from unorganised to organised acidulant supply, and rising interest in the commercial standardisation and valorisation of India’s distinctive range of traditional natural acidulant ingredients including tamarind, kokum, amchur, and lime.

Market Segmentation

By Acidulant Type

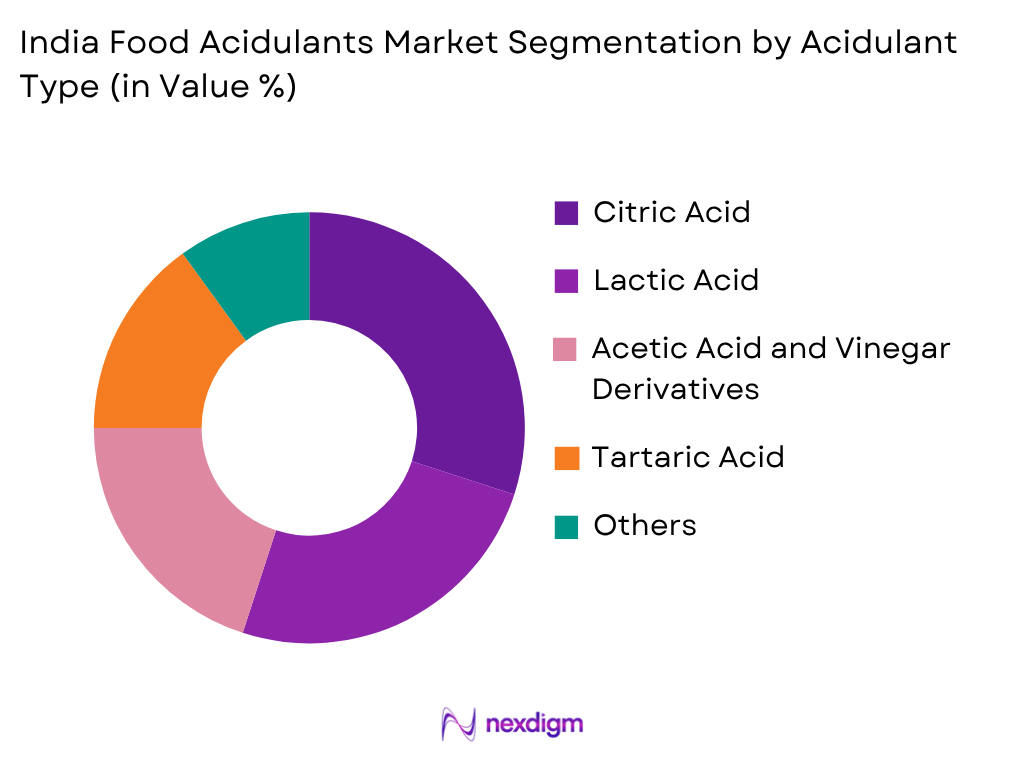

Citric acid dominates the India food acidulants market by volume and value, reflecting its extraordinary functional versatility, established FSSAI regulatory acceptance, and cost-competitive availability from both domestic fermentation manufacturers and Chinese import sources that collectively ensure continuous and affordable supply to India’s diverse food manufacturing customer base. India has a meaningful domestic citric acid fermentation industry, with producers utilising sugarcane molasses, a widely available agricultural by-product of India’s large sugar manufacturing sector, as the primary fermentation feedstock, providing a domestically sourced raw material base that partially insulates the market from the import cost volatility affecting countries entirely dependent on Chinese supply. Citric acid’s applications in India span the carbonated soft drink industry led by Coca-Cola India, PepsiCo India, and a large number of regional beverage producers, where it provides characteristic tartness and pH stabilisation in cola, lemon, and fruit-flavoured drinks; the fruit juice and nectar segment where it prevents colour browning and extends shelf life; the confectionery and mithai sector where it contributes tartness to hard candy and citrus-flavoured sweets; the packaged paneer and cheese industry where it functions as a coagulating acid to precipitate milk protein; and the ketchup, chutney, and pickle industry where it provides pH preservation support. Lactic acid and glucono delta-lactone are extensively used in dairy applications, particularly in the production of paneer, dahi, flavoured yoghurt, and processed cheese, where they perform critical coagulation, acidification, and texture development functions central to Indian dairy product manufacturing. Acetic acid and its derivatives, including vinegar and sodium diacetate, are fundamental ingredients in India’s large and culturally embedded pickle, achar, and condiment manufacturing sector, representing a distinct and high-volume application category unique to the Indian market context.

By Application

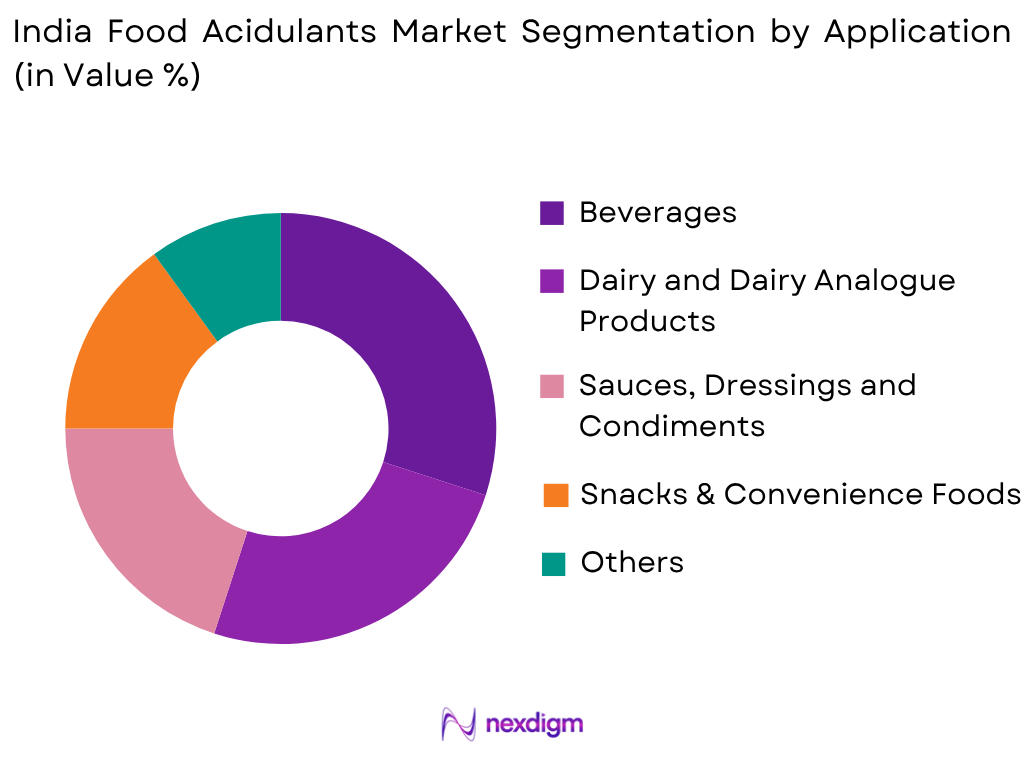

Beverages represent the largest application segment for food acidulants in India by value, driven by the country’s rapidly expanding packaged beverage market encompassing carbonated soft drinks, fruit juices and nectars, flavoured milk drinks, energy and sports drinks, packaged coconut water, and a growing range of functional and wellness beverages that collectively require acidulants for pH regulation, flavour development, microbial stability, vitamin preservation, and extended shelf life across the demanding ambient distribution conditions of India’s vast and diverse geography. The Confederation of Indian Industry and the Indian Beverage Association report that India’s packaged beverage market has grown at consistently high rates over the past decade, supported by rising household incomes, expanding modern retail and general trade distribution, and rapid adoption of packaged beverages in Tier 2 and Tier 3 cities as improved cold chain infrastructure and digital distribution extend product reach beyond metropolitan markets. The dairy and dairy products segment represents a particularly distinctive and India-specific application category for food acidulants, given the country’s position as the world’s largest milk producer and the central cultural importance of fermented and acid-set dairy products including paneer, dahi, lassi, buttermilk, and khoa-based sweets across all Indian dietary traditions. Paneer production, which relies on citric acid, lactic acid, or glucono delta-lactone as coagulating acidulants to precipitate milk protein curd, represents one of the most technically specific and volume-significant acidulant applications in the Indian food industry, with the National Dairy Development Board estimating domestic paneer production at hundreds of thousands of tonnes annually. The sauces, pickles, and condiment segment constitutes a third major high-volume acidulant application category in India, where acetic acid remains the foundational preservation and flavour ingredient across the country’s enormous and culturally diverse pickle, achar, chutney, and vinegar-based sauce manufacturing industry spanning both large organised manufacturers including Kissan, Tops, and Priya and a vast ecosystem of regional and small-scale artisanal producers.

Competitive Landscape

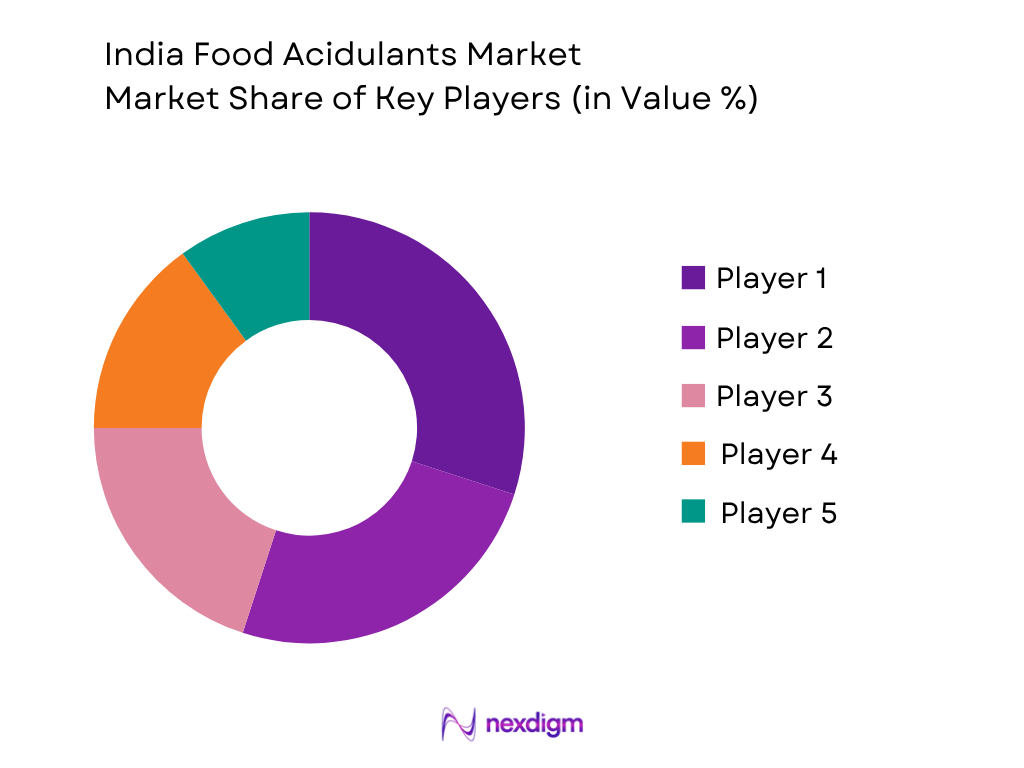

The India food acidulants market is fragmented across acidulant types, with a combination of domestic Indian manufacturers, multinational ingredient companies, large-scale Chinese acidulant importers and their distribution agents, and specialty food ingredient distributors competing across different product categories and customer segments. Domestic Indian producers with fermentation capacity including Godavari Biorefineries and Gujarat Narmada Valley Fertilizers and Chemicals supply lactic acid and acetic acid from domestic feedstocks, while multinational ingredient companies including Jungbunzlauer, Corbion, and IMCD India serve technically demanding large manufacturer customers with premium and specialty acidulant grades. Chinese citric acid manufacturers and their Indian distribution partners dominate the commodity citric acid segment through aggressive pricing leveraging large-scale Chinese fermentation capacity. Regional ingredient distributors serve the large and geographically dispersed base of small and medium food manufacturers across Tier 2 and Tier 3 markets. The FSSAI’s progressive regulatory strengthening is gradually creating a quality floor that disadvantages substandard imported products and supports organised domestic supply chains.

| Company | Establishment Year | Headquarters | Primary Acidulant Portfolio | Key Application Industries

|

Manufacturing Presence | R&D Capability | Distribution Network | Clean Label Solutions |

| Jungbunzlauer India | 2008 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Godavari Biorefineries | 1956 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Corbion India | 2010 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Brenntag India | 2006 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| IMCD India | 2012 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

India Food Acidulants Market Analysis

Growth Drivers

Rapidly Expanding Packaged Food and Beverage Manufacturing Sector

India’s rapidly expanding packaged food and beverage manufacturing sector, driven by urbanisation, rising household incomes, changing dietary preferences, and the progressive formalisation of food supply chains, represents the most significant and structurally durable growth driver for food acidulant demand across the forecast period. The Ministry of Food Processing Industries reports that India’s food processing sector is one of the largest in the world by output, with total industry turnover estimated at more than USD 300 billion and the sector growing at consistently high rates supported by government incentives under the Production Linked Incentive scheme for food processing, Pradhan Mantri Kisan SAMPADA Yojana infrastructure investments, and the National Mission on Food Processing. The International Monetary Fund projects India’s nominal GDP to continue growing above 6 percent annually, supporting rising household expenditure on packaged and processed food products as consumption upgrades from home-cooked and unpackaged formats to commercially manufactured branded and private label offerings across urban, semi-urban, and increasingly rural markets. The General Statistics Office of India reports that urban population is growing rapidly, with the World Bank estimating that more than 500 million Indians are now urban residents and the United Nations projecting that India’s urban population will approach 700 million by 2035, providing an expanding and concentrated addressable market for packaged food manufacturers whose production processes require food additives including acidulants for product quality, stability, and safety. India’s carbonated beverage industry, led by Coca-Cola India and PepsiCo India alongside a large number of regional producers, consumes substantial citric acid volumes annually and continues to expand as per-capita soft drink consumption, while still well below global averages, grows steadily with rising incomes and expanding modern trade distribution. The rapid growth of the fruit juice, nectar, and flavoured drink segment, supported by expanding cold chain infrastructure and Tetra Pak-format ambient packaging adoption, is creating additional acidulant demand beyond carbonated beverages. The snack food and namkeen segment, one of India’s largest and most innovation-active food categories, consumes significant volumes of citric acid and malic acid as flavour acidulants in tangy, masala, and chaat masala-flavoured products, with the snack industry growing rapidly as brands including Haldiram’s, Bikaji, Balaji, and PepsiCo’s Lay’s and Kurkure ranges expand distribution and product variety.

Domestic Sugarcane Molasses Fermentation Base and Make in India Manufacturing Expansion

India’s large and well-established sugarcane production and sugar manufacturing industry, which positions the country as one of the world’s largest sugar producers with annual sugarcane crushing exceeding 350 million tonnes, provides a strategically important domestic raw material base for the fermentation-derived production of citric acid, lactic acid, acetic acid, and other organic acids that underpin the food acidulants market. Sugarcane molasses, a thick syrup by-product generated during the crystallisation of sucrose from sugarcane juice, is produced in India in quantities of approximately 12 to 14 million tonnes annually, providing an abundant, cost-competitive, and domestically available fermentation feedstock from which food-grade organic acids can be produced through aerobic or anaerobic fermentation processes without dependence on imported raw materials. Domestic fermentation-based acidulant production using molasses as feedstock offers Indian manufacturers a meaningful cost advantage relative to import-dependent competitors in countries without domestic fermentation raw material bases, reducing foreign exchange exposure and providing greater pricing stability to food manufacturer customers who procure in Indian Rupees. The government’s Make in India initiative, which identifies food processing as a priority sector for domestic manufacturing investment, and the Production Linked Incentive scheme for food processing provide financial incentives that are encouraging investment in domestic food ingredient manufacturing capacity including organic acid fermentation facilities. Godavari Biorefineries, one of India’s largest integrated sugarcane biorefineries, produces lactic acid and other fermentation-derived biochemicals from domestic molasses feedstock, representing a model for domestic acidulant production that leverages India’s agricultural raw material abundance. The government’s Aatmanirbhar Bharat self-reliance framework creates a broader policy environment supportive of domestic acidulant manufacturing investment, reducing dependency on Chinese citric acid imports that represent a supply concentration vulnerability for the Indian food industry, and creating long-term opportunities for domestic producers to expand fermentation capacity and develop a competitive domestic supply base for multiple food acidulant categories.

Market Challenges

High Price Sensitivity and Competition from Low-Cost Chinese Citric Acid Imports

The India food acidulants market faces a persistent and structurally significant challenge arising from the extreme price sensitivity of the majority of Indian food manufacturing customers, combined with the availability of competitively priced Chinese citric acid imports that consistently undercut domestically produced and premium imported alternatives on a price-per-kilogram basis, constraining both domestic manufacturer growth and the adoption of higher-quality specialty acidulant grades across price-sensitive customer segments. China’s dominant position in global citric acid production, accounting for more than 70 percent of global output according to industry estimates, enables Chinese manufacturers including RZBC Group, Weifang Ensign, and Shandong Juxian Hongde to offer citric acid at commodity prices that reflect the scale economies, low labour costs, and government industrial support of large-scale Chinese fermentation facilities. Indian food manufacturers, a significant proportion of whom are small and medium enterprises operating on tight margins in competitive consumer categories, consistently prioritise ingredient procurement cost minimisation over quality differentiation or supply chain provenance considerations, making price the primary purchasing criterion for commodity acidulant categories including citric acid, acetic acid, and malic acid. This price-driven procurement culture creates substantial commercial pressure on domestic Indian acidulant manufacturers, who must compete with Chinese import prices while operating at smaller production scales with higher domestic energy, labour, and financing costs that constrain their ability to match Chinese commodity pricing without government support mechanisms. The FSSAI’s regulatory framework for food additives, while progressively strengthening food safety and quality standards, does not yet consistently enforce the documentation and testing requirements that would create a meaningful quality floor distinguishing compliant domestic and premium imported acidulants from lower-quality imports, allowing substandard or mislabelled acidulant products to circulate in the unorganised market segment at prices that distort fair competition and undermine investment in quality domestic production.

FSSAI Regulatory Complexity and Enforcement Inconsistency Across States

The regulatory environment governing food additives including acidulants in India is administered by the Food Safety and Standards Authority of India under the Food Safety and Standards Act 2006 and the associated Food Safety and Standards (Food Products Standards and Food Additives) Regulations 2011, a framework that has been progressively updated and strengthened since its introduction but continues to present compliance challenges for both ingredient suppliers and food manufacturers due to regulatory complexity, inconsistent enforcement across India’s 28 states and 8 union territories, and the practical difficulty of monitoring compliance across India’s vast and largely fragmented food manufacturing ecosystem. The FSSAI’s permitted food additive list, maximum usage levels, and labelling requirements for acidulants are updated periodically through food safety orders and notifications, but the pace of regulatory change and the requirement to monitor multiple regulatory instruments creates compliance uncertainty for food manufacturers formulating products with newer acidulant ingredients or seeking clarification on usage levels for specific food categories. State-level enforcement of FSSAI food additive regulations is highly variable, with larger and more technically capable state food safety departments in Maharashtra, Karnataka, and Tamil Nadu maintaining more rigorous inspection and testing programs, while enforcement in many other states is more limited, creating an uneven compliance environment where manufacturers operating to full regulatory standards may face price competition from non-compliant producers who avoid the costs of quality documentation, testing, and regulatory adherence. The FSSAI’s food business operator licensing system covers a large proportion of organised food manufacturers, but a significant segment of India’s food manufacturing ecosystem consists of very small and informal producers operating outside the organised licensing framework, particularly in the pickle, achar, mithai, and small snack food segments that collectively consume meaningful volumes of food acidulants. Import regulations for food ingredient acidulants require compliance with FSSAI import standards, BIS quality certifications for specific categories, and custom clearance documentation, creating administrative complexity that can slow ingredient procurement and increase landed costs for importers of specialty acidulants not readily available from domestic sources.

Market Opportunities

Natural and Traditional Indian Acidulant Standardisation and Commercial Development

India possesses a uniquely rich and culturally embedded tradition of utilising naturally derived acidulant ingredients including tamarind, kokum, amchur (dried raw mango powder), raw mango pulp, lime and lemon juice, kokum butter extracts, bilimbi, and a range of regional souring agents that collectively represent both a distinctive cultural asset and a significant commercial opportunity for the development of standardised, food-grade natural acidulant ingredients meeting the growing demand for clean label and naturally derived alternatives to synthetic acidulant systems among India’s expanding urban middle-class consumer base and export-oriented food manufacturers. Tamarind, cultivated extensively across South India, Maharashtra, and Gujarat, contains tartaric acid as its primary organic acid component and has been used for millennia as a souring agent in Indian culinary traditions, but the commercial standardisation of tamarind-derived tartaric acid as a food-grade ingredient meeting consistent purity, acidity, and microbiological standards has remained underdeveloped relative to the ingredient’s commercial potential. The global market for natural tartaric acid, currently dominated by wine industry by-product sourcing from European winemaking regions, represents a multi-million dollar opportunity that India’s abundant tamarind agricultural base could potentially serve if investment in industrial extraction, purification, and standardisation technology is directed toward developing a commercial tamarind-derived tartaric acid production capability. Kokum, cultivated primarily in the Western Ghats of Maharashtra, Goa, Karnataka, and Kerala, contains hydroxycitric acid and other organic acids with demonstrated functional properties as acidulants and flavour agents in regional Indian cuisine, and has attracted growing interest from nutraceutical and functional food manufacturers seeking Indian-origin natural acidulant ingredients with distinctive flavour profiles and potential health benefit positioning. FSSAI’s growing emphasis on clean label food production and natural ingredient use, combined with rising urban consumer preference for recognisably natural ingredient declarations, creates a market pull environment that supports investment in the commercial development and standardisation of India’s traditional natural acidulant raw materials into food-grade ingredient products suitable for modern food manufacturing applications.

Dairy Processing Expansion and India-Specific Paneer and Fermented Dairy Acidulant Demand

India’s position as the world’s largest milk producer, with the National Dairy Development Board reporting total milk production exceeding 230 million tonnes annually, combined with the rapid expansion of organised dairy processing and the growing consumer preference for packaged and branded dairy products, creates a large and structurally growing demand opportunity for food acidulants specifically optimised for Indian dairy applications including paneer coagulation, dahi fermentation, flavoured yoghurt pH adjustment, processed cheese manufacture, and khoa-based traditional sweet production. Paneer, the fresh acid-set cheese that is one of the most widely consumed dairy protein sources in Indian vegetarian cuisine, is produced by acidifying heated milk to precipitate curd using citric acid, lactic acid, glucono delta-lactone, or combinations thereof, with the choice of acidulant influencing the final product’s texture, moisture content, yield, and cooking properties. The organised paneer manufacturing segment, served by dairy companies including Amul, Mother Dairy, Nestle India, Heritage Foods, and a growing number of regional dairy cooperatives and private manufacturers, consumes significant volumes of food-grade citric acid and glucono delta-lactone annually, with demand growing in line with the strong expansion of packaged and branded paneer availability across modern trade, general trade, and quick commerce platforms. Dahi and flavoured yoghurt production across India’s dairy industry similarly creates acidulant demand for lactic acid starter cultures, pH adjustment agents, and acidity regulators that maintain product quality and stability throughout the chilled distribution chain. The rapid growth of the UHT and extended shelf life dairy drink segment, including flavoured milk, lassi, and chaas products in Tetra Pak and aseptic packaging, creates additional acidulant demand for citric acid and lactic acid used to maintain product stability, prevent protein precipitation, and achieve target flavour profiles in ambient-distributed dairy beverages. Ingredient suppliers that develop technical expertise in Indian dairy acidulant applications, provide application-specific guidance for paneer yield optimisation and dahi texture development, and offer consistent food-grade acidulant products meeting FSSAI dairy product standards are well positioned to capture the growing acidulant demand from India’s rapidly formalising dairy processing sector.

Future Outlook

The India food acidulants market is expected to witness sustained and broad-based growth throughout the forecast period, supported by the country’s rapidly expanding packaged food and beverage manufacturing sector, urbanisation-driven dietary shifts toward processed and convenience food formats, growth of the organised dairy and snack food industries, FSSAI regulatory strengthening driving quality compliance investment, and increasing commercial interest in India’s traditional natural acidulant raw materials. Ingredient suppliers are increasingly investing in FSSAI regulatory compliance documentation, Rupee-denominated pricing stability mechanisms, distribution network expansion into Tier 2 and Tier 3 markets, and technical application support for India-specific food manufacturing requirements. Growing demand across the beverage, dairy, bakery, snack food, and condiment segments is expected to create additional market opportunities throughout the forecast period. Continued investments in domestic fermentation-based organic acid production capacity, natural acidulant standardisation and commercialisation, and export-oriented food manufacturing quality upgrading will further strengthen the long-term growth trajectory of the India food acidulants market.

Major Players

- Jungbunzlauer India

- Bartek Ingredients India Distribution

- Corbion India

- Brenntag India

- RZBC Group India Distribution

- Weifang Ensign Industry India Distribution

- IMCD India

- Univar Solutions India

- Shandong Juxian Hongde Citric Acid India Distribution

- S.V. Agro Food

- Mahindra Agri Solutions

- Merck Life Science India

- Thermo Fisher Scientific India

- Gujarat Narmada Valley Fertilizers and Chemicals

- Godavari Biorefineries

Key Target Audience

- Food and Beverage Manufacturers

- Food Ingredient and Chemical Distributors and Brokers

- Dairy Cooperatives and Organised Dairy Processors

- Nutraceutical and Pharmaceutical Grade Acidulant Consumers

- Food Technologists and Regulatory Affairs Teams

- Export-Oriented Food Manufacturers Requiring APEDA and FSSAI Compliant Ingredients

- Investments and Private Equity Firms

- Government and Regulatory Bodies (Food Safety and Standards Authority of India (FSSAI), Bureau of Indian Standards (BIS), Ministry of Food Processing Industries (MoFPI), Agricultural and Processed Food Products Export Development Authority (APEDA))

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the major stakeholders across the India food acidulants value chain, including domestic fermentation-based acidulant manufacturers, multinational ingredient companies and their India distribution partners, Chinese acidulant importers and distribution agents, food and beverage manufacturers across all relevant application segments, dairy cooperatives, FSSAI regulatory authorities, industry associations including the Confederation of Indian Food Trade and Industry (CIFTI) and the Food Industry Capacity and Skill Initiative (FICSI), and academic food technology researchers. Extensive secondary research is conducted using FSSAI regulatory publications, Ministry of Food Processing Industries data, General Statistics Office food manufacturing output surveys, APEDA export statistics, Directorate General of Commercial Intelligence and Statistics trade data, and proprietary ingredient market databases to establish the key variables influencing market performance.

Step 2: Market Analysis and Construction

Historical market information is compiled and evaluated to estimate the overall market size, ingredient volume consumption by acidulant type and application, domestic production volumes, import volumes by source country, average selling prices in Rupee and US Dollar terms, distributor margins, and revenue generation across major acidulant categories and food manufacturing end-use segments. Both demand-side and supply-side indicators are analyzed using bottom-up and top-down market sizing approaches to ensure comprehensive market coverage across all acidulant types, application categories, and regional food manufacturing clusters from Gujarat and Maharashtra in the West to West Bengal in the East and Tamil Nadu in the South.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates and analytical assumptions are validated through Computer Assisted Telephone Interviews (CATIs) and structured discussions with food technologists and product development managers at Indian food and beverage manufacturers, acidulant and ingredient sales managers at multinational and domestic suppliers, regional food ingredient distributor executives, dairy cooperative technical managers, FSSAI regulatory consultants, export-oriented food manufacturer quality managers, and academic food chemistry researchers at Indian universities and research institutions. These interviews provide critical on-ground formulation, commercial, and regulatory insights that strengthen the reliability of market estimates across both large organised and small unorganised manufacturer segments.

Step 4: Research Synthesis and Final Output

The final stage integrates primary research findings with secondary information to develop a comprehensive assessment of market size, segmentation, competitive landscape, customer procurement behaviour, and future opportunities. Multiple validation techniques, including data triangulation across Directorate General of Commercial Intelligence and Statistics import trade data, General Statistics Office food manufacturing production statistics, FSSAI food business operator licensing data, and ingredient supplier commercial disclosures, are employed to ensure the consistency, accuracy, and credibility of the final market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Large and Rapidly Expanding Food and Beverage Processing Industry, Rising Packaged Food Consumption Driven by Urbanisation, Growing Beverage Sector Including Carbonated Drinks and Fruit Juices, Expanding Dairy Processing Industry, Snack Food and Namkeen Industry Growth, Rising Export-Oriented Food Manufacturing Demand, Domestic Citric Acid and Lactic Acid Production Capability, Growing Quick Service Restaurant and Organised Foodservice Sector)

- Market Challenges (High Price Sensitivity Across the Majority of Food Manufacturing Customer Base, Competition from Imported Chinese Citric Acid at Low Price Points, Regulatory Complexity Under FSSAI Food Additives Regulations, Limited Consumer Awareness of Acidulant Functionality in Food Labelling Context, Raw Material Supply Volatility for Fermentation-Derived Acids, Fragmented Small and Medium Food Manufacturer Customer Base, Counterfeit and Substandard Acidulant Product Risk, Monsoon Season Supply Chain Disruptions Affecting Distribution)

- Market Opportunities (Natural and Traditional Indian Acidulant Standardisation and Commercialisation, FSSAI Clean Label Alignment Driving Natural Acid Adoption, Export-Oriented Food Manufacturing Quality Upgrade, Domestic Fermentation-Derived Lactic and Citric Acid Capacity Expansion, Functional Beverage and Energy Drink Sector Growth, Paneer and Indian Dairy Product Acidulant Demand, Tamarind and Kokum-Derived Natural Acidulant Development, Growing Pharmaceutical Grade Acidulant Demand)

- Market Trends (Clean Label and Natural Ingredient Demand Among Urban Consumers, FSSAI Regulatory Tightening Driving Quality Compliance Investment, Growing Organised Food Manufacturing Sector Displacing Unorganised Players, Fermentation-Derived Acid Adoption in Dairy and Bakery Applications, Functional Beverage Innovation Driving Diverse Acidulant Demand, Traditional Indian Acidulant Ingredients Gaining Commercial Attention, Digital B2B Ingredient Procurement Platforms Expanding Reach to Tier 2 and Tier 3 Markets, Make in India Policy Supporting Domestic Acidulant Fermentation Capacity)

- Government Regulations (Food Safety and Standards Act 2006, Food Safety and Standards Authority of India (FSSAI) Food Additives Regulations under FSS (Food Products Standards and Food Additives) Regulations 2011, FSSAI Licensing and Registration Requirements, Bureau of Indian Standards (BIS) Food Additive Quality Standards, Food Safety and Standards (Labelling and Display) Regulations 2020, Import Policy for Food Ingredients under DGFT, APEDA Standards for Export-Oriented Food Manufacturing, FSSAI Clean and Sustainable Label Initiative, Food Fortification Resource Centre Standards)

- Raw Material and Supply Chain Analysis (Sugarcane Molasses Availability for Citric and Lactic Acid Fermentation, Domestic Citric Acid Production Capacity at Major Indian Manufacturers, Tamarind and Kokum Domestic Agricultural Supply, Lime and Lemon Juice Concentrate Availability, Acetic Acid and Glacial Acetic Acid Import and Domestic Supply, Phosphoric Acid Supply from Domestic Chemical Producers, Import Dependency for Specialty Acidulants Including Malic, Fumaric and Tartaric Acid, Raw Material Cost Trends and Seasonal Price Variability)

- Food Manufacturing Industry Demand Analysis (Carbonated Beverage Industry Citric Acid Consumption, Dairy Industry Lactic Acid and GDL Demand, Bakery Industry Acidulant Usage, Snack Food and Namkeen Industry Flavour Acid Demand, Sauce and Ketchup Industry Acetic Acid Consumption, Paneer Manufacturing GDL and Citric Acid Requirements, Pickle and Achar Industry Acetic Acid Demand)

- Seasonal Demand Analysis (Summer Beverage and Cold Drink Production Peak, Diwali and Festive Season Confectionery and Mithai Surge, Ramadan and Eid Food Production, Holi Season Beverage and Snack Production, Mango Season Amchur and Natural Acidulant Production, Post-Monsoon Pickle and Achar Production Cycle, Wedding Season Catering and Packaged Food Demand)

- Export Market Analysis (Indian Processed Food Export to Middle East and GCC, Export to ASEAN and Southeast Asia, Diaspora Food Export to USA and UK, APEDA Certified Food Export Quality Requirements, Organic and Natural Acidulant Export Opportunity, Indian Traditional Food Product Export Acidulant Compliance)

- Innovation Landscape (Tamarind-Derived Tartaric Acid Commercial Scale Development, Kokum and Garcinia-Based Acidulant Standardisation, Sugarcane Molasses Fermentation Optimisation for Citric Acid Yield, Encapsulated Acidulant Systems for Indian Snack and Namkeen Applications, Dual-Function Acidulant and Antioxidant Systems, Natural Acidulant Blends for Indian Dairy and Paneer Applications, Precision Fermentation Organic Acid Development)

- Sustainability Analysis (Domestic Agricultural Raw Material Utilisation for Bio-Based Acidulants, Sugarcane Molasses By-Product Valorisation, Tamarind and Kokum Agricultural By-Product Utilisation, Reduced Carbon Footprint Through Domestic Production vs Import, Sustainable Sourcing Certification for Export-Oriented Manufacturers, Water Usage Efficiency in Fermentation-Based Acidulant Production, Packaging Sustainability for Ingredient Delivery)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Acidulant Type (In Value %)

Citric Acid

Acetic Acid and Vinegar Derivatives

Lactic Acid

Malic Acid

Tartaric Acid

Phosphoric Acid

Fumaric Acid

Ascorbic Acid (Vitamin C as Acidulant)

Glucono Delta-Lactone (GDL)

Adipic Acid

Succinic Acid

Propionic Acid - By Application (In Value %)

Beverages

Bakery and Confectionery

Dairy and Dairy Analogue Products

Processed Meat and Seafood Products

Sauces, Dressings and Condiments

Snack Foods and Extruded Products

Jams, Preserves and Fruit Preparations

Frozen and Ready-to-Eat Meals and Convenience Foods

Infant and Clinical Nutrition Products

Dietary Supplements and Nutraceuticals - By End-Use Industry (In Value %)

Food and Beverage Manufacturers

Foodservice, Quick Service Restaurants and Dhabas

Retail and Institutional Packaged Food Producers

Pharmaceutical and Nutraceutical Producers

Animal Feed and Pet Food Manufacturers - By Distribution Channel (In Value %)

Direct Sales to Food and Beverage Manufacturers (B2B)

Ingredient Distributors and Chemical Distributors

Specialty Food Ingredient Importers and Brokers

E-Commerce and Digital B2B Ingredient Platforms - By Region (In Value %)

North India

West India

South India

East India

Central India

Northeast India

- Market Share Analysis (By Value, Volume, Acidulant Type, Application Segment, Distribution Channel)

- Cross Comparison Parameters (Acidulant Portfolio Breadth, Domestic Manufacturing vs Import Model, FSSAI and BIS Regulatory Compliance Track Record, Distribution Network Coverage Across India, Annual New Product and Grade Launches, Natural and Traditional Indian Acidulant Portfolio, Fermentation Capacity Scale, Rupee-Denominated Pricing Stability, Export Market Supply Capability)

- SWOT Analysis of Major Players

- Pricing Analysis (By Acidulant Type, Purity Grade, Source, Application, Pack Size, Contract Volume)

- Detailed Profiles of Major Companies

Jungbunzlauer India

Bartek Ingredients India Distribution

Corbion India

Brenntag India

RZBC Group India Distribution

Weifang Ensign Industry India Distribution

IMCD India

Univar Solutions India

Shandong Juxian Hongde Citric Acid India Distribution

S.V. Agro Food

Mahindra Agri Solutions

Merck Life Science India

Thermo Fisher Scientific India

Gujarat Narmada Valley Fertilizers and Chemicals

Godavari Biorefineries

- Procurement Pattern Analysis (Ingredient Sourcing Frequency, Acidulant Type and Grade Preference, Application-Specific Usage Behaviour, Seasonal Procurement Cycles, Annual Ingredient Budget Allocation)

- Demographic and Industry Buyer Analysis (Large Food and Beverage Manufacturers, SME Food Processors, Dairy Cooperatives, Snack and Namkeen Manufacturers, Pickle and Condiment Producers, Foodservice and QSR Operators, Nutraceutical and Pharmaceutical Producers)

- Formulation Cost and Functionality Trade-Off Analysis

- Natural and Traditional Indian Acidulant vs Synthetic Acidulant Preference Analysis

- Supplier and Brand Loyalty Analysis

- FSSAI Regulatory Compliance-Driven Ingredient Selection Behaviour

- Ingredient Attribute Preference Analysis (FSSAI Approval Status, Purity Grade, Functional Performance, Price Competitiveness in Rupee Terms, Availability Across Tier 2 and Tier 3 Markets, Technical Support, BIS Certification, Minimum Order Quantity)

- Large Organised Manufacturer vs Unorganised SME Processor Procurement Behaviour Differences

- Digital vs Traditional B2B Ingredient Procurement Behaviour

- Customer Pain Point Analysis

- Procurement Decision-Making Process

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now