Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India insect repellent market is valued at USD ~ million, based on industry revenue analysis from established research databases. Growth in 2023 and 2024 has been driven by increasing incidence of vector-borne diseases such as dengue, malaria, chikungunya, and rising public awareness about preventive health measures. Rising disposable incomes and growing urbanization have expanded household expenditure on personal protection products across rural and urban segments in the country.

India’s insect repellent demand is concentrated in major metropolitan and tropical regions due to climatic conditions that favor year-round mosquito activity. Cities such as Delhi, Mumbai, Chennai, Bengaluru, and Kolkata record high consumption levels owing to dense populations, monsoon-associated mosquito outbreaks, and well-developed distribution channels. These urban markets are further reinforced by strong retail penetration and higher awareness of health risks linked to mosquito-borne diseases in these population centers.

Market Segmentation

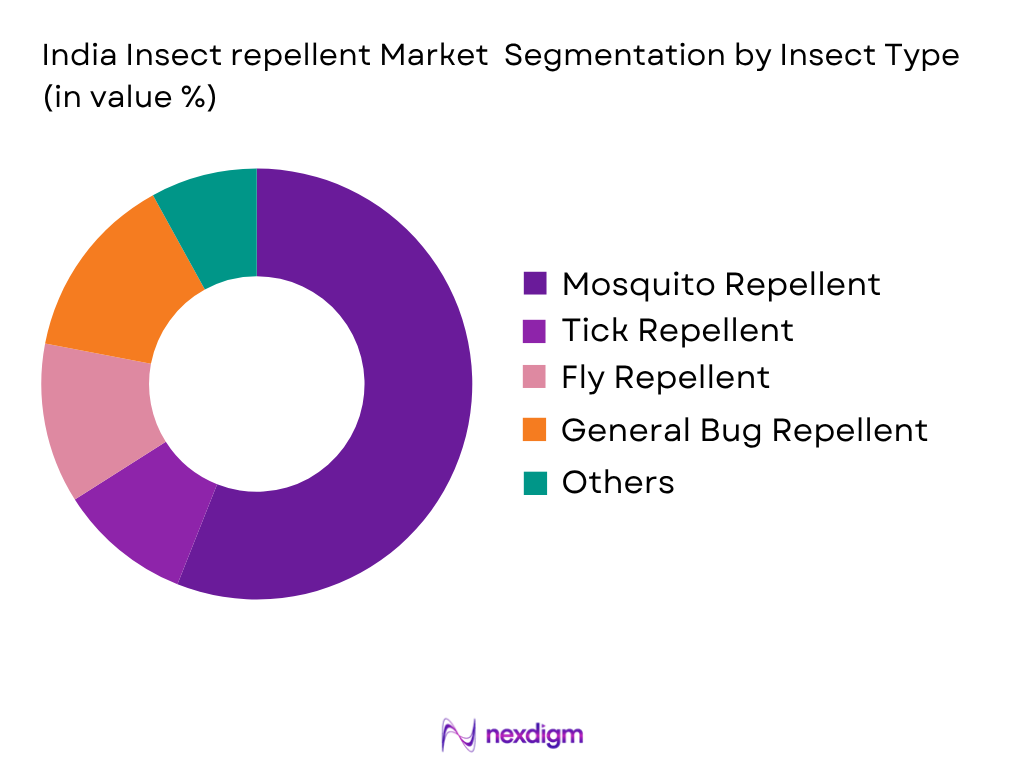

By Insect Type

The India insect repellent market is segmented by target insect into mosquito, bug/general, fly, tick, and other insect types. Mosquito repellents dominate the market because mosquitoes pose the most widespread health threat in India, driving continuous demand for protective products across households, travel use and institutional deployments. Frequent seasonal outbreaks of dengue, chikungunya and malaria, particularly following monsoon rains, elevate consumer urgency to adopt repellents that reduce bite exposure risk. The mosquito segment’s prominence is reinforced by its broad applicability across urban and rural households and its relevance to both health‑driven and comfort‑driven purchase behavior. Bug and general insect repellents are used mainly in residential settings for comfort and nuisance control, while fly repellents and tick repellents have more localized demand based on specific entomological patterns. Other insect types cover niche products targeting smaller pests such as midges and ants but contribute smaller market value. Product accessibility through modern retail and digital commerce channels supports the mosquito segment’s continued leadership.

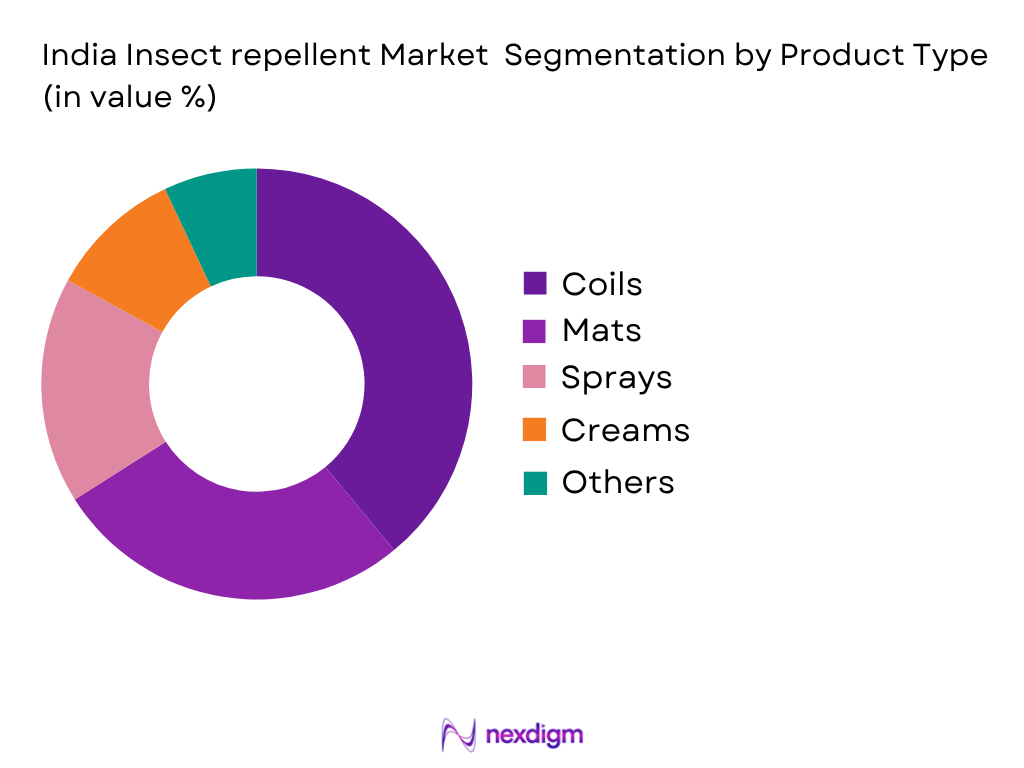

By Product Format

Within the India insect repellent market, coil‑based products are the leading format, owing to their affordability, ease of use, and widespread availability through both organized and unorganized retail across urban and rural regions. Coils typically do not require electricity and deliver prolonged protection in household settings, appealing particularly to price‑sensitive consumers. Liquid vaporizers and mats hold the next largest share, driven by cleaner, smoke‑free operation and rising adoption among urban households with reliable power. Sprays and aerosols are preferred for travel, outdoor use and individual protection, particularly among younger and mobile consumers. Creams and roll‑ons serve niche needs such as skin‑friendly applications for children and sensitive users. Wearable repellents, including patches, capture early interest among lifestyle‑oriented buyers seeking portable protection. Conventional products such as coils benefit from entrenched consumption patterns, but the segment mix is gradually diversifying toward modern and premium formats as distribution expands and consumer awareness increases.

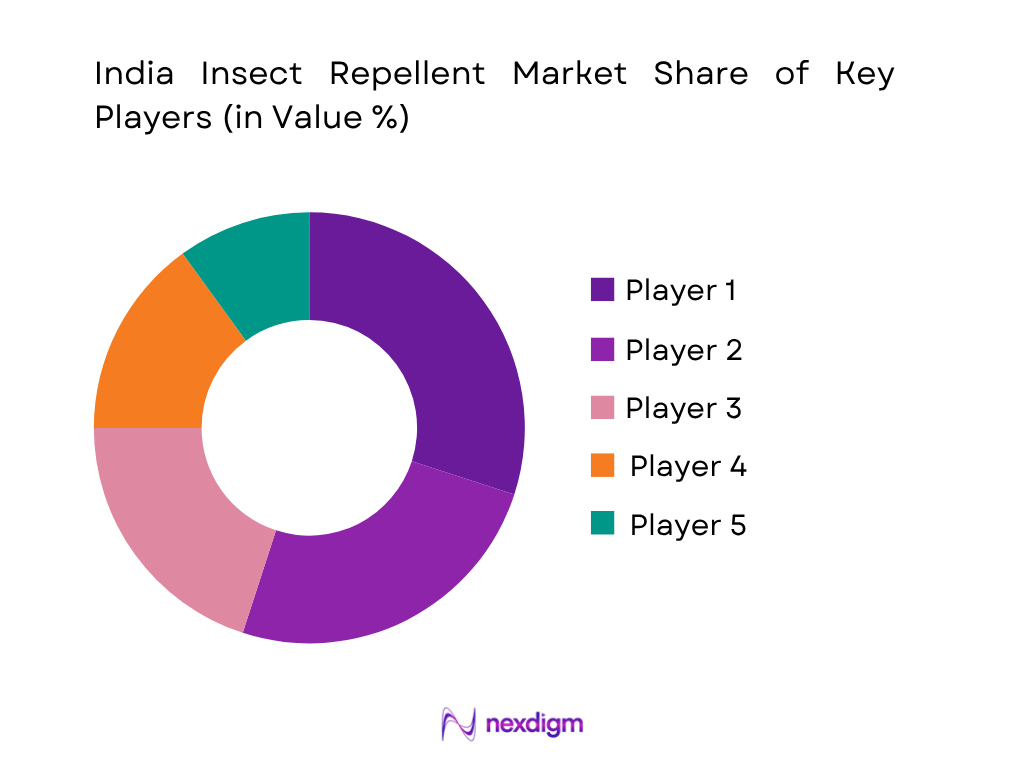

Competitive Landscape

The India insect repellent market presents a moderately consolidated competitive environment characterized by both large multinational consumer goods firms and strong Indian FMCG players. Key competition centers on product portfolio diversity, distribution reach, innovation in active formulations, and price tier management across urban and rural segments.

| Company | Est. Year | Headquarters | Active Ingredient Strategy | Product Format Coverage | Distribution Channel Reach | Regulatory Compliance | Brand Equity Index |

| Godrej Consumer Products | 1897 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Reckitt Benckiser | 1823 | UK | ~ | ~ | ~ | ~ | ~ |

| Dabur India | 1884 | Ghaziabad, India | ~ | ~ | ~ | ~ | ~ |

| SC Johnson | 1886 | USA | ~ | ~ | ~ | ~ | ~ |

| Jyothy Laboratories | 1983 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

Market Overview

Growth Drivers

Vector‑borne Disease Prevalence Driving Repellent Demand

India’s insect repellent market growth in 2025 is underpinned by persistent and rising incidence of vector‑borne diseases, which directly influences consumer behaviour toward protective products such as mosquito repellents, coils, sprays, and topical solutions. In 2023, according to data compiled from India’s National Centre for Vector Borne Disease Control reporting to government bodies, over 32,000 dengue cases were recorded nationwide, compared with 18,391 reported during the same reporting period in 2023, evidencing a significant increase in public health burden and concern. This sustained disease incidence compels households and institutions to invest in daily use of insect repellents as preventative health solutions. Concurrently, malaria trends show that India reported approximately 2.56 lakh malaria cases in 2024, with states such as Odisha recording approximately 68,700 cases, Jharkhand 42,400 cases, and Chhattisgarh 31,400 cases, indicating high endemicity in several regions. Such disease prevalence creates consistent demand for insect repellents across both rural and urban markets, as consumers attempt to mitigate health risk exposure associated with mosquito vectors through personal protection measures.

Macroeconomic and Demographic Context Supporting Product Adoption

India’s demographic and socioeconomic environment in 2025 provides a structural backdrop for the insect repellent market’s continued relevance. With a total population of ~ billion people, India remains one of the world’s most populous countries, with an annual population growth rate of 0.9%, contributing to dense urbanisation and extensive human‑mosquito contact opportunities. Urban and peri‑urban agglomerations such as Delhi, Mumbai, Bengaluru, and Chennai not only have large resident populations but also report higher vector‑borne disease prevalence due to environmental factors like stagnant water and monsoon cycles conducive to mosquito breeding. Public health infrastructure statistics indicate that only 63% of the population has access to safely managed sanitation services, a metric closely linked with mosquito breeding habitat control, thus amplifying reliance on insect repellents as an accessible protective measure for consumers. At the same time, India’s overall economy reported a GDP of USD ~ trillion in 2025 and GDP per capita of approximately USD 2,694.7, indicative of growing disposable incomes that enable consumer expenditure on household protection products including repellents. The combination of demographic scale, environmental health factors, and macroeconomic conditions underpins robust household and commercial adoption of insect repellent solutions across India in 2025.

Market Challenges

Seasonal Demand Fluctuation

Seasonality presents a major challenge for India’s insect repellent market, affecting supply chain planning and revenue consistency. National vector surveillance shows that dengue cases surge from 4,245 in March to over 24,567 in August 2025, demonstrating strong monsoon-linked peaks in disease incidence. This seasonality causes temporary spikes in consumer purchases, followed by low off-season demand. Manufacturers face high inventory holding costs outside peak months, while distributors must manage logistics for concentrated demand periods. Smaller retail operators experience cash flow volatility, as most repellent purchases occur during the rainy season. Seasonal spikes also challenge marketing efforts, requiring firms to time promotional campaigns precisely to align with disease incidence. Without mechanisms to stabilize sales or incentivize year-round usage, companies risk underutilized capacity and fluctuating profitability, particularly in rural or semi-urban regions with lower retail sophistication.

Rural Penetration and Distribution Gaps

Despite a rural population of over 65% of India’s ~ billion residents, branded insect repellent products face limited availability outside urban centers. Government rural development statistics reveal that less than 40% of rural retail outlets consistently stock modern repellents, creating reliance on informal or unregistered alternatives. Poor road infrastructure and intermittent electricity access further hinder storage and display of powered devices such as vaporizers. Additionally, awareness campaigns reach rural consumers less effectively, limiting education about product benefits and safe usage. Consequently, rural demand remains underdeveloped relative to urban markets, restricting full market potential. Addressing these distribution and awareness gaps is critical for companies targeting pan-India expansion.

Opportunities

Public Health Initiatives Encouraging Preventive Product Adoption

India’s focus on vector-borne disease prevention offers growth potential for insect repellents. The National Vector Borne Disease Control Programme monitors dengue, malaria, chikungunya, and Japanese Encephalitis, issuing weekly district-level reports and promoting household protective measures. These programs reinforce the perception of repellents as essential for personal safety, driving consistent demand. High-incidence regions see government distribution of protective kits and educational campaigns, increasing awareness and trial of branded repellents. Manufacturers can leverage official health data to design regionally targeted marketing strategies, aligning product availability with epidemiological trends. By integrating public health collaboration into market penetration, companies can capture new users and strengthen brand trust, particularly in high-risk zones.

E-commerce Expansion Enhancing Market Accessibility

Digital retail channels provide a key opportunity to reach consumers beyond urban retail limitations. Reports from the Ministry of Commerce & Industry indicate ~ million online retail transactions by mid-2025, with personal care and household categories seeing strong growth. Mobile internet penetration in rural India has reached 75% of households, expanding potential e-commerce reach into previously underserved regions. Online platforms offer diverse SKUs, including premium and natural repellents, and faster delivery to rural areas. Data analytics from digital channels enable geographic targeting and consumer preference insights, supporting strategic product placement and promotional campaigns. Expanding online presence complements traditional retail, improving overall penetration and sustaining demand across India’s heterogeneous consumer base.

Future Outlook

Over the forecast period, the India insect repellent market is expected to maintain solid growth momentum propelled by continuous health awareness campaigns, rising disposable income, increasing incidence of vector‑borne diseases, and expanding retail penetration into tier‑2 and tier‑3 cities. The integration of natural and eco‑friendly formulations, including botanical extracts and biopesticide blends, is anticipated to expand market reach among health‑sensitive and premium consumer segments. Technological advancements in smart repellent devices and wearable formats will attract younger, tech‑savvy populations, facilitating year‑round use rather than seasonal demand. Manufacturers focusing on multi‑format product portfolios, strong rural distribution networks, and digital engagement strategies will be well‑positioned to capture evolving consumer preferences. Collaborations with government health programs targeting malaria and dengue prevention could further broaden institutional demand and product adoption across public health initiatives, cementing repellent use as a daily preventive health measure.

Major Players

- Godrej Consumer Products

- Reckitt Benckiser

- Dabur India

- SC Johnson

- Jyothy Laboratories

- Johnson & Johnson

- Henkel AG & Co KGaA

- Spectrum Brands

- Sawyer Products

- Coghlan’s Ltd

- Avon Products

- Himalayan Herbals

- Herbal Strategi Homecare

- Healthbest Private Limited

- All Out / Goodknight (Reckitt brands)

Key Target Audience

- Consumer Goods & FMCG Brand Managers

- Retail Buying & Merchandising Heads

- Product Development & R&D Strategy Teams

- Outdoor & Travel Goods Manufacturers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Occupational Safety Procurement Teams

- Public Health Program Teams

Research Methodology

Step 1: Identification of Key Variables

The initial phase identifies all stakeholders and product variants in the India insect repellent market, including formats (coils, vaporizers, sprays), insect categories (mosquito, bug, tick), and distribution channels (retail, online, institutional), based on extensive secondary research from published market databases and disease prevalence reports.

Step 2: Market Analysis and Construction

Historical data on product revenues, consumption patterns, and pricing were compiled and analyzed to construct baseline size and growth models, cross‑referenced with verified public health data on vector‑borne disease incidence.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market insights were validated through industry expert consultations, including supply chain partners, retail category managers, and health sector advisors, to refine demand drivers and segmentation logic.

Step 4: Research Synthesis and Final Output

This phase consolidates verified secondary and primary insights into a rigorously structured report, ensuring alignment with market reality, regulatory conditions, and consumer behavior patterns in India insect repellent consumption.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Scope of India Insect Repellent Market, Market Sizing Approach [Retail + Import + Organized + Unorganized Channels], Consolidated Data Sources, Primary Research Framework, Limitations and Quality Assurance)

- Definition and Scope

- Overview Genesis

- Disease Burden & Seasonal Patterns

- Value Chain and Distribution Landscape

- Supply Chain and Raw Material Inputs

- Regulatory Framework

- Growth Drivers (High prevalence of mosquito‑borne diseases (dengue, malaria) ,Rising urbanization & disposable income, Heightened health awareness and hygiene focus, Innovation in product formats (smart devices + herbal solutions)

- Market Challenges (Health concerns linked to chemical repellents, Seasonality of demand and inventory challenges, Counterfeit/substandard product proliferation, Price sensitivity in rural segments

- Opportunities (Shift to natural/herbal formulations, Smart IoT‑enabled repellents, Rural penetration through sachets and small pack formats, Premium & functional variants (long‑lasting protection)

- Trends (Natural & Ayurvedic ingredient demand, Connected devices and automated vaporizer systems, Bundling with home‑care & personal care categories)

- Government Regulation (Insecticides Act & Registration Requirements, Quality & Safety Standards)

- SWOT Analysis

- Stake Ecosystem

- Porter’s Five Forces

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- Product Pricing Dynamics (2020-2025)

- Traditional vs Modern Distribution Contribution (2020-2025)

- Regional Demand Intensity (2020-2025)

- By Insect Type (In Value Share %)

Mosquito Repellent

Bugs/General Insect Repellent

Fly Repellent

Tick Repellent

Others (e.g., Midges, Ants) - By Product Format (In Value Share %)

Coils

Liquid Vaporizers & Mats

Sprays & Aerosols

Creams & Roll‑Ons

Wearables & Patches

Others (UV Traps/Plug‑in Devices) - By Active Ingredient Class (In Value Share %)

Synthetic

Botanical & Natural Extracts

Biopesticide Blends

Proprietary Molecules - By Distribution Channel (In Value Share %)

Modern Retail

Pharmacies/Drug Stores

E‑Commerce & Online Marketplaces

General Trade/Convenience Stores

Institutional/Government Procurement - By End‑Use Application (In Value Share %)

Residential Household

Outdoor & Recreation

Travel & Tourism Health

Commercial/Institutional Use

Occupational Health & Safety

- Market Share of Major Players (Value/Volume Basis)

- Cross Comparison Parameters (Product Portfolio Breadth, Regional Presence and Distribution Coverage, Pricing Strategy and SKUs, Revenue by Product Segment

R&D Investment and Innovation Pipeline, Marketing and Promotional Expenditure, Partnerships, Alliances, and Acquisitions) - Manufacturing Capacity and Supply Chain Efficiency

- SWOT Analysis of Major Players

- Pricing Analysis by SKU and Channel

- Detailed Profiles of Major Companies

Godrej Consumer Products

Reckitt Benckiser

Dabur India

Jyothy Laboratories

SC Johnson

Mortein (Bayer Consumer Care)

HIT/Japanese Formula (GCP)

Odomos (Avon/Dabur)

Himalayan Herbals

Jungle Formula

Kwik Knock

Goodknight (Reckitt)

All Out (Reckitt)

SC Johnson Off!

Local/Regional Herbal Brands

- Market Demand and Utilization (Residential Consumption, Institutional Use)

- Purchasing Power and Budget Allocations (Urban vs Rural Demand Economics)

- Regulatory and Compliance Requirements (Safety Labeling & Ingredient Limits)

- Consumer Needs, Desires, and Pain Point Analysis

- Decision‑Making Process (Brand Trust, Channel Influence, Product Efficacy)

- By Value (2026-2035)

- By Volume (2026-2035)

- By Price Bands (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now