Download PDF

Download PDFMarket Overview

The India Insecticide Market is valued at approximately USD ~ billion, supported by India’s position as one of the world’s largest agricultural economies. The Indian agrochemical industry was valued at approximately USD ~ billion, while insecticides accounted for the largest product segment due to widespread usage in cotton, rice, vegetables, and horticulture crops. India cultivates more than 125 million hectares of foodgrain crops annually and remains one of the largest producers of rice, cotton, sugarcane, fruits, and vegetables. Increasing incidences of bollworms, stem borers, whiteflies, and sucking pests, combined with rising adoption of high-yield crop varieties and export-oriented farming practices, continue to drive insecticide demand across the country.

Market Segmentation

By Product Category

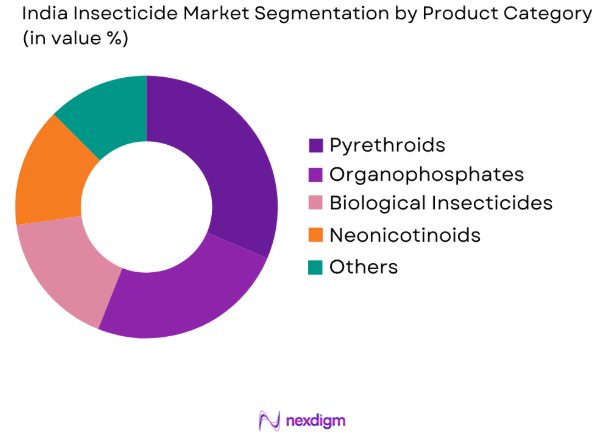

India Insecticide Market is segmented by product category into pyrethroids, organophosphates, biological insecticides, neonicotinoids, and others. Recently, pyrethroids have held the dominant market share in India because of their broad-spectrum activity against major agricultural pests such as bollworms, stem borers, whiteflies, aphids, and leafhoppers. These products are extensively used across cotton, rice, vegetables, pulses, and plantation crops due to their effectiveness, affordability, and widespread availability through India’s extensive agrochemical dealer network. Pyrethroids are also favored because they provide rapid knockdown action and are compatible with integrated pest management programs. Their strong adoption among small and medium-sized farmers, combined with a long history of use in Indian agriculture, continues to support their dominant position. Although biological insecticides are gaining momentum due to sustainability concerns, pyrethroids remain the preferred category for large-scale pest control applications.

By Crop Type

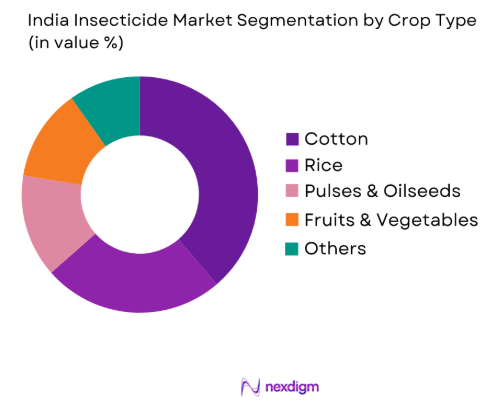

India Insecticide Market is segmented by crop type into cotton, rice, pulses and oilseeds, fruits and vegetables, and others. Recently, cotton has held the dominant market share under crop type because cotton remains one of the most insecticide-intensive crops cultivated in India. The crop is highly susceptible to bollworms, pink bollworms, whiteflies, aphids, jassids, and sucking pests, requiring multiple insecticide applications throughout the growing season. Major cotton-producing states such as Maharashtra, Gujarat, Telangana, Andhra Pradesh, and Punjab account for substantial insecticide consumption. Farmers invest heavily in pest management programs to protect yields and fiber quality, particularly in export-oriented cotton production. The recurring threat of pest resistance and the need to maintain productivity further reinforce cotton’s leadership position in India’s insecticide market, making it the largest consumer segment across all crop categories.

Competitive Landscape

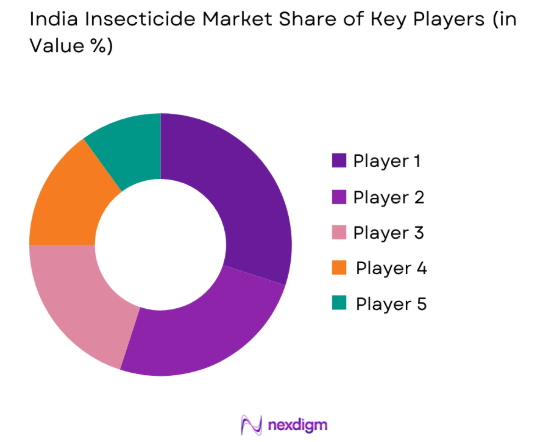

The India Insecticide Market is moderately consolidated, with a combination of multinational agrochemical companies and large domestic manufacturers competing through product innovation, dealer networks, formulation capabilities, and crop-specific solutions. Companies are increasingly investing in biological insecticides, resistance-management technologies, and digital agriculture platforms to strengthen their market presence. Competition is influenced by product registrations, manufacturing scale, farmer outreach programs, and regional distribution strength.

| Company | Establishment Year | Headquarters | Insecticide Portfolio | Manufacturing Capacity | Distribution Network | Biological Portfolio | Key Crop Focus | Competitive Position |

| UPL Limited | 1969 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Bayer Crop Science India | 1958 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Syngenta India | 2000 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| PI Industries | 1946 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Insecticides India Ltd. | 1996 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

India Insecticide Market

Growth Drivers

Expansion of Cotton and Foodgrain Cultivation

India’s insecticide demand is strongly supported by its vast agricultural base and the need to protect high-value crops from pest infestations. According to the Ministry of Agriculture & Farmers Welfare, India cultivated approximately 127 million hectares of foodgrains and over 12 million hectares of cotton during the latest agricultural cycle. Cotton remains one of the most insecticide-intensive crops because of persistent threats from pink bollworm, whitefly, aphids, and jassids. India also produced approximately 137 million tonnes of rice and over 113 million tonnes of wheat, making crop protection critical to maintaining national food security. The World Bank reported India’s GDP at approximately USD 3.9 trillion, while agriculture continues to support the livelihoods of more than 100 million farming households. Rising pressure from pest outbreaks and the need to improve productivity per hectare have encouraged greater adoption of modern insecticides, integrated pest management practices, and crop protection technologies across major agricultural states such as Maharashtra, Gujarat, Punjab, Telangana, Andhra Pradesh, and Madhya Pradesh.

Rising Pest Resistance and Increasing Agricultural Productivity Requirements

The increasing incidence of pest resistance is a major growth driver for the India Insecticide Market. Agricultural pests such as pink bollworm, stem borer, fall armyworm, whitefly, and brown planthopper have become increasingly difficult to control through traditional methods, compelling farmers to adopt advanced insecticide formulations. India possesses approximately 156 million hectares of arable land, one of the largest agricultural areas globally. According to the Food Corporation of India, annual foodgrain procurement exceeded 70 million tonnes, highlighting the strategic importance of maintaining crop productivity. India’s population exceeded 1.43 billion people, increasing pressure on agricultural systems to deliver stable food supplies. In addition, horticulture production surpassed 350 million tonnes, creating significant demand for pest management solutions across fruits and vegetables. The requirement to maximize yield while reducing crop losses has encouraged greater usage of insecticides, biological alternatives, and resistance-management programs, making pest pressure a critical long-term growth catalyst for the market.

Market Challenges

Counterfeit Agrochemicals and Regulatory Compliance Complexity

One of the major challenges facing the India Insecticide Market is the presence of counterfeit and substandard agrochemical products. The Central Insecticides Board & Registration Committee (CIB&RC) regulates more than 300 registered technical-grade pesticides and thousands of formulations available across India. However, the country’s highly fragmented agrochemical retail network, comprising over 300,000 agricultural input retailers, increases the risk of counterfeit products entering the market. Such products often reduce pest-control effectiveness and contribute to resistance development. India’s agricultural exports exceeded USD 48 billion, making compliance with residue limits and international crop protection standards increasingly important. Manufacturers are required to invest heavily in product registration, environmental testing, toxicology studies, and stewardship programs before commercialization. The regulatory approval process for new active ingredients remains lengthy and resource intensive. Consequently, both domestic and multinational companies face operational challenges related to compliance, enforcement, and maintaining product quality standards across India’s diverse agricultural regions.

Climate Variability and Resistance Development

Climate variability has become a significant challenge for the India Insecticide Market because changing weather conditions alter pest life cycles and increase the unpredictability of infestations. India experienced average temperatures exceeding historical norms across several agricultural regions, while irregular rainfall patterns affected cropping cycles in key producing states. The India Meteorological Department reported multiple episodes of extreme weather impacting agricultural production. At the same time, repeated use of similar insecticide chemistries has accelerated resistance development among pests such as pink bollworm, fall armyworm, whitefly, and stem borers. India produces more than 40 million bales of cotton and over 137 million tonnes of rice, making effective pest control essential. Resistance reduces product efficacy and forces farmers to adopt more complex pest-management programs involving multiple modes of action, biological solutions, and precision applications. These factors increase operational complexity and create ongoing challenges for both growers and agrochemical manufacturers.

Market Opportunities

Expansion of Biological Insecticides and Sustainable Agriculture

The transition toward sustainable agriculture presents a significant opportunity for the India Insecticide Market. India has more than 4.4 million hectares under certified organic and organic-conversion farming systems, making it one of the largest organic agriculture markets globally. Increasing focus on export-oriented agriculture, residue management, and environmentally responsible farming practices is encouraging the adoption of biological insecticides. India exported agricultural and processed food products worth more than USD 24 billion through APEDA-supported channels, creating strong incentives for growers to comply with international residue standards. Horticulture production exceeded 350 million tonnes, offering substantial potential for biological crop protection products in fruits, vegetables, spices, and plantation crops. Government initiatives supporting integrated pest management and sustainable agriculture further reinforce this trend. As farmers seek effective alternatives to conventional chemistries, manufacturers with strong biological portfolios are positioned to benefit from expanding demand across both domestic and export-focused agricultural segments

Adoption of Drone Spraying and Precision Agriculture Technologies

Precision agriculture technologies are creating substantial opportunities for the India Insecticide Market. India’s cultivated area exceeds 190 million hectares, while labor shortages and rising operational costs are encouraging the adoption of technology-driven farming solutions. The Government of India has actively promoted agricultural drones through various subsidy and demonstration programs, enabling more efficient pesticide and insecticide applications. India’s digital economy exceeded USD 400 billion, supporting wider adoption of farm-management software, GPS-guided equipment, remote sensing systems, and AI-based pest monitoring tools. Drone-assisted spraying helps improve application accuracy, reduce chemical wastage, and increase coverage in difficult terrains such as cotton, sugarcane, horticulture, and plantation crops. As growers increasingly focus on improving productivity and sustainability, precision spraying technologies are becoming integral components of modern pest-management strategies. This shift is creating new growth avenues for insecticide manufacturers, agri-tech companies, and specialized application service providers.

Future Outlook

The India Insecticide Market is expected to witness robust growth through the forecast period, supported by increasing food security requirements, rising pest pressure, expansion of high-value horticulture, and adoption of modern crop protection technologies. India’s growing population and limited arable land availability will continue to emphasize the importance of maximizing agricultural productivity. Biological insecticides are expected to gain significant traction as sustainability concerns and residue management requirements become increasingly important. Government support for integrated pest management programs and environmentally friendly agricultural practices is likely to encourage adoption of biological crop protection solutions. The increasing use of drones, precision agriculture technologies, digital farm advisory services, and AI-based pest monitoring systems is expected to transform insecticide application practices. Export-oriented crop production and quality management requirements will also create opportunities for advanced insecticide formulations and integrated crop protection solutions.

Major Players

- UPL Limited

- Bayer Crop Science India

- PI Industries

- Syngenta India

- BASF India Agricultural Solutions

- FMC India

- Corteva Agriscience India

- Sumitomo Chemical India

- Insecticides India Limited

- Rallis India

- Dhanuka Agritech

- Best Agrolife

- Crystal Crop Protection

- India Pesticides Limited

- Godrej Agrovet Crop Protection

Key Target Audience

- Agrochemical Manufacturers

- Biological Crop Protection Companies

- Agricultural Cooperatives

- Commercial Farming Enterprises

- Agrochemical Distributors and Retail Networks

- Plantation and Horticulture Producers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India Insecticide Market. This includes agrochemical manufacturers, biological crop protection companies, distributors, retailers, growers, agricultural cooperatives, agronomists, and regulatory agencies. Extensive secondary research is conducted to identify variables influencing insecticide demand, pest pressure, crop protection expenditure, and technology adoption.

Step 2: Market Analysis and Construction

In this phase, historical data related to crop acreage, pest incidence, insecticide consumption, active ingredient demand, crop protection expenditure, and agricultural output are compiled and analyzed. Market sizing is performed through top-down and bottom-up methodologies to validate revenue estimates and segment-level performance.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted telephone interviews with agrochemical companies, distributors, agronomists, growers, agricultural cooperatives, and crop consultants. These consultations provide operational insights into product preferences, resistance-management practices, purchasing behavior, and adoption of biological alternatives.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing primary and secondary research findings to validate market estimates, competitive positioning, growth drivers, challenges, and future opportunities. Direct engagement with industry participants ensures a comprehensive and accurate assessment of the India Insecticide Market.

- Executive Summary

- Research Methodology (Market definitions and assumptions, abbreviations, India insecticide taxonomy, active ingredient classification, agricultural and public health insecticide scope, CIB&RC registration framework, Insecticides Act compliance structure, market sizing approach, top-down and bottom-up triangulation, manufacturer interviews, distributor validation, dealer network assessment, agronomist consultations, treated acreage analysis, pest incidence mapping, crop protection expenditure analysis, limitations and future conclusions)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (Cotton acreage protection, rice pest management demand, increasing pest resistance, food security requirements, biological insecticide adoption, precision agriculture penetration, export-oriented horticulture production, government support for crop protection)

- Market Challenges (Counterfeit agrochemicals, resistance development, regulatory approval complexity, climatic variability, fragmented distribution networks, farmer awareness gaps, rising input costs, environmental compliance requirements)

- Opportunities (Biological crop protection expansion, drone spraying services, integrated pest management programs, precision agriculture technologies, specialty crop protection solutions, digital agriculture platforms, sustainable farming initiatives, export crop quality management)

- Market Trends (Biological insecticide adoption, drone-assisted spraying, digital pest monitoring, integrated pest management implementation, precision application technologies, reduced-residue crop protection, AI-enabled farm advisory services, sustainable agriculture practices)

- Government Regulation (CIB&RC registrations, Insecticides Act compliance, Maximum Residue Limit regulations, state pesticide control programs, quality monitoring initiatives, environmental safety assessments, import-export compliance standards, sustainable agriculture policies)

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Active Ingredient Consumption (2020-2025)

- By Product Category (In Value %)

Pyrethroids

Organophosphates

Biological Insecticides

Neonicotinoids

Others - By Crop Type (In Value %)

Cotton

Rice

Pulses and Oilseeds

Fruits and Vegetables

Others - By Application Method (In Value %)

Foliar Spray

Seed Treatment

Soil Treatment

Drone-Based Application

Others - By Pest Type (In Value %)

Bollworms

Stem Borers

Whiteflies

Aphids and Jassids

Others - By Distribution Channel (In Value %)

Agrochemical Dealers and Retailers

Direct Company Sales

Agricultural Cooperatives

Institutional and Government Procurement

Digital Agri-Input Platforms - By Region (In Value %)

North India

West India

South India

East India

Central India

- Market Share of Major Players (Market value, volume sales, active ingredient portfolio, treated acreage coverage, crop penetration, biological product portfolio, dealer network reach, regional footprint)

- Cross Comparison Parameters (Registered active ingredients, biological insecticide portfolio, cotton and rice crop penetration, dealer and distributor network strength, manufacturing and formulation capacity, R&D investment in crop protection, resistance management solutions portfolio, digital agriculture integration capability)

- SWOT Analysis of Major Players

- Pricing Analysis Basis SKUs (Cypermethrin formulations, Chlorpyrifos formulations, Imidacloprid formulations, Lambda-cyhalothrin formulations, Emamectin Benzoate products, Biological insecticides, Whitefly control products, Bollworm control products, Stem borer control products, Seed treatment insecticides)

- Detailed Profiles of Major Companies

Bayer Crop Science India

UPL Limited

PI Industries

Sumitomo Chemical India

Syngenta India

BASF India Agricultural Solutions

FMC India

Corteva Agriscience India

Insecticides India Limited

Rallis India

Dhanuka Agritech

Best Agrolife

Crystal Crop Protection

India Pesticides Limited

Godrej Agrovet Crop Protection

- Cotton Farmer Analysis

- Rice Grower Analysis

- Horticulture Producer Analysis

- Plantation Crop Grower Analysis

- Agricultural Cooperative Analysis

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Active Ingredient Consumption (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now