Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the India Intelligence Surveillance Reconnaissance market was valued at USD ~ billion, supported by officially disclosed defense capital acquisition allocations and parliamentary budget documents. The market size is driven by sustained investments in battlefield awareness, border monitoring, space-based surveillance, and network-centric warfare programs. Government-backed modernization initiatives, indigenous electronics manufacturing, and long-term ISR platform procurement have strengthened demand. Rising emphasis on persistent surveillance, data fusion, and real-time intelligence dissemination continues to reinforce spending across air, land, naval, and space domains.

Based on a recent historical assessment, New Delhi, Bengaluru, Hyderabad, and Pune dominate the India Intelligence Surveillance Reconnaissance market due to institutional concentration, industrial ecosystems, and operational command presence. New Delhi drives demand through policy formulation, procurement oversight, and intelligence agency headquarters. Bengaluru leads through aerospace engineering, avionics design, and ISR software development clusters. Hyderabad supports electronics manufacturing and missile-related surveillance integration. Pune contributes through military command infrastructure and testing facilities. National dominance is reinforced by border security priorities, maritime monitoring requirements, and expanding satellite intelligence programs.

Market Segmentation

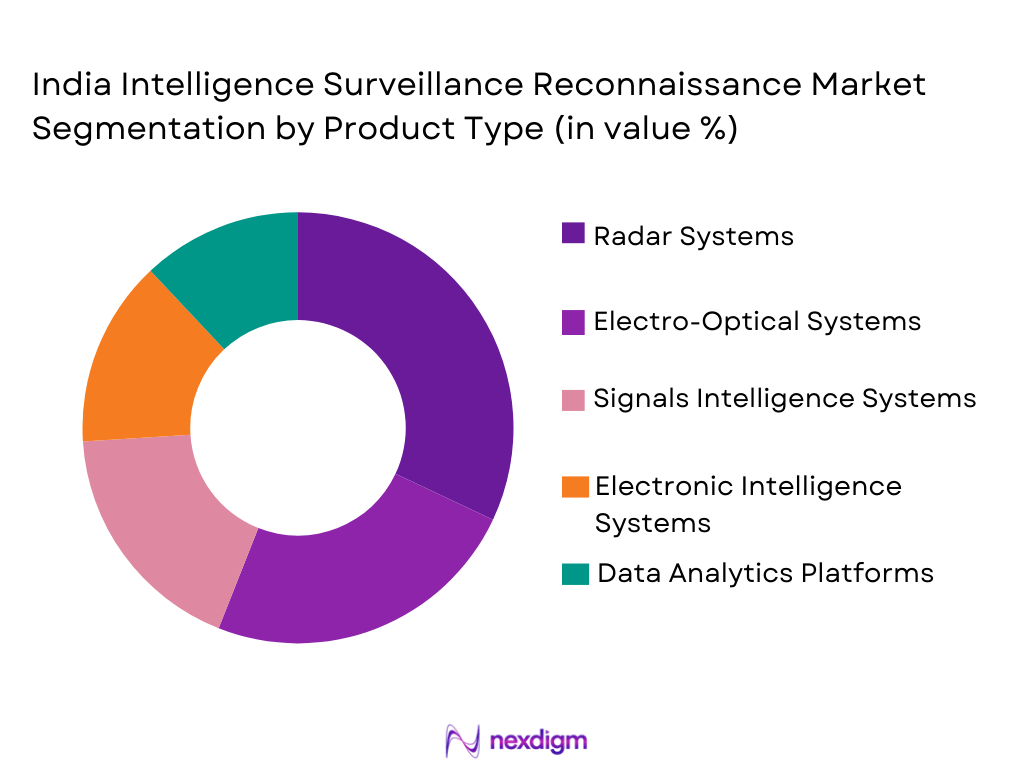

By Product Type

India Intelligence Surveillance Reconnaissance market is segmented by product type into electro-optical systems, radar systems, signals intelligence systems, electronic intelligence systems, and data analytics platforms. Recently, radar systems have a dominant market share due to demand patterns linked to border surveillance, maritime domain awareness, and all-weather operational requirements. Persistent monitoring needs across diverse terrains, combined with the ability to detect, track, and classify targets over long ranges, have strengthened radar adoption. Indigenous radar development programs, integration with airborne and ground platforms, and compatibility with networked command systems have further reinforced dominance. Continuous upgrades and lifecycle extensions have sustained procurement momentum.

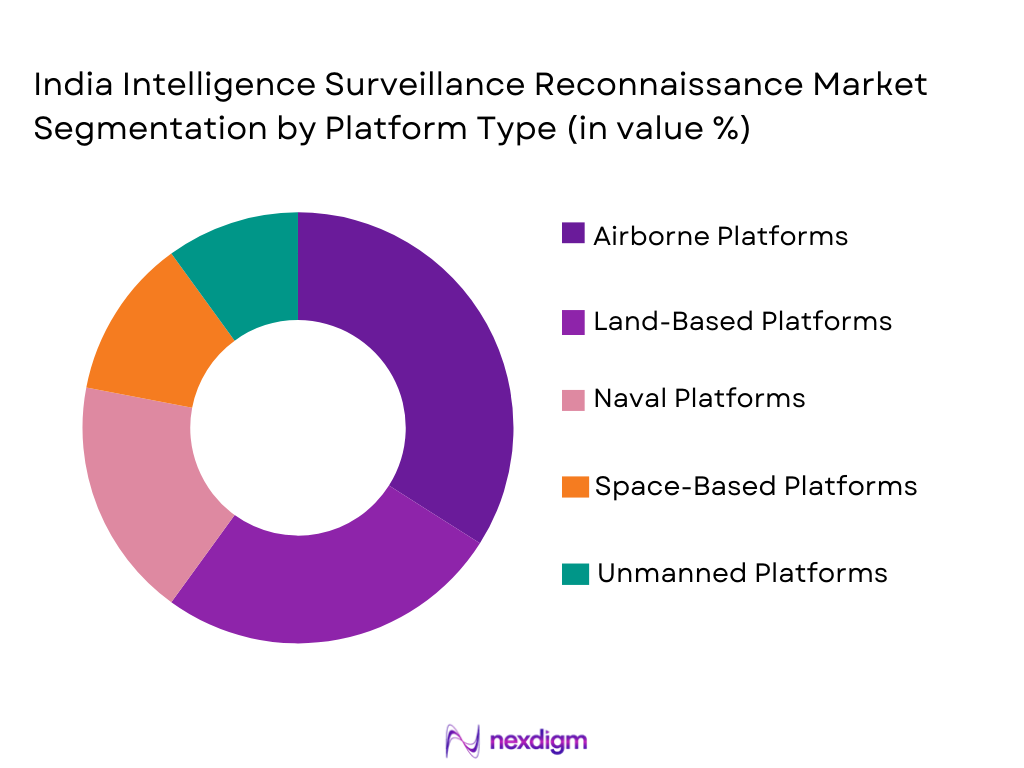

By Platform Type

India Intelligence Surveillance Reconnaissance market is segmented by platform type into airborne, land-based, naval, space-based, and unmanned platforms. Recently, airborne platforms have a dominant market share due to demand patterns emphasizing flexibility, rapid deployment, and wide-area coverage. Airborne ISR assets support both strategic and tactical missions, offering persistent intelligence collection and real-time data relay. Integration with fighter aircraft, special mission aircraft, and helicopters has expanded operational utility. Strong domestic aerospace capabilities, combined with ongoing fleet upgrades and sensor integration programs, have sustained airborne platform dominance across multiple defense services.

Competitive Landscape

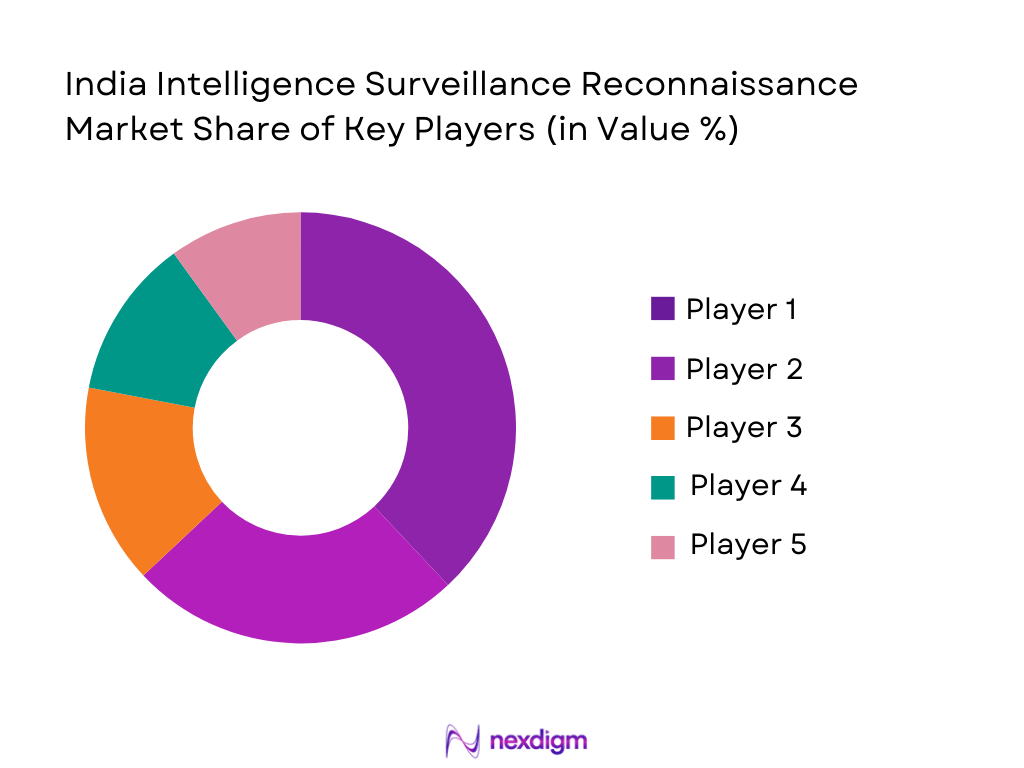

The India Intelligence Surveillance Reconnaissance market exhibits moderate consolidation, with a mix of large public sector enterprises and private defense manufacturers shaping competition. Long-term government contracts, technology partnerships, and indigenization mandates influence competitive positioning, while established players benefit from integration experience and lifecycle support capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Indigenous Content Level |

| Bharat Electronics Limited | 1954 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| Hindustan Aeronautics Limited | 1940 | Bengaluru | ~

|

~

|

~

|

~

|

~

|

| Tata Advanced Systems | 2010 | Hyderabad | ~

|

~

|

~

|

~

|

~

|

| Larsen and Toubro Defence | 2011 | Mumbai | ~

|

~

|

~

|

~

|

~

|

| Mahindra Defence Systems | 2015 | Mumbai | ~

|

~

|

~

|

~

|

~

|

India Intelligence Surveillance Reconnaissance Market Analysis

Growth Drivers

Border and Maritime Surveillance Modernization:

Border and Maritime Surveillance Modernization is a central growth driver for the India Intelligence Surveillance Reconnaissance market because national security priorities increasingly emphasize persistent monitoring of land borders, coastlines, and maritime approaches to address evolving threat environments. Complex terrain conditions, extended coastlines, island territories, and dense maritime traffic have created sustained demand for continuous situational awareness supported by integrated surveillance architectures. Government-backed investments in coastal surveillance networks, border monitoring grids, long-range radars, and sensor fusion centers have translated into consistent procurement activity across multiple defense and security agencies. Airborne surveillance aircraft, maritime patrol platforms, and ground-based sensor systems are being deployed to close intelligence gaps and improve response coordination. Indigenous radar development programs and domestic electronics manufacturing have strengthened supply reliability while reducing external dependency risks. Lifecycle upgrades of existing ISR assets further contribute to spending continuity by extending operational relevance and enhancing performance. Inter-agency intelligence sharing frameworks are reinforcing the need for interoperable systems capable of real-time data exchange. Maritime domain awareness initiatives, including port surveillance and shipping lane monitoring, add an additional layer of demand. Collectively, these factors embed border and maritime surveillance modernization as a structurally sustained driver of market expansion.

Network-Centric Warfare and Real-Time Intelligence Integration:

Network-Centric Warfare and Real-Time Intelligence Integration drives the India Intelligence Surveillance Reconnaissance market by reshaping operational doctrines around information dominance and synchronized decision making. Defense forces increasingly depend on ISR systems to provide timely, accurate, and fused intelligence across air, land, sea, and space domains. Integrated sensor networks enable commanders to access unified operational pictures rather than fragmented data streams. Data fusion platforms transform large volumes of sensor data into actionable intelligence under compressed timelines. Secure communication networks enhance interoperability between services and command hierarchies. Artificial intelligence applications improve target recognition, anomaly detection, and predictive threat assessment. Cloud-enabled intelligence architectures support scalable processing, storage, and dissemination requirements. Training reforms and doctrinal alignment reinforce adoption of network-centric operational concepts. Sustained modernization roadmaps ensure long-term investment continuity in integrated ISR capabilities.

Market Challenges

Integration Complexity Across Legacy and Modern ISR Platforms:

Integration Complexity Across Legacy and Modern ISR Platforms presents a persistent challenge for the India Intelligence Surveillance Reconnaissance market due to the coexistence of heterogeneous systems procured across different time periods and technological standards. Many legacy ISR assets were designed with proprietary architectures that limit seamless integration with modern digital platforms. Retrofitting advanced sensors, analytics software, and secure communication links onto older platforms requires extensive customization and validation. These integration efforts often extend project timelines and elevate program execution risks. Interoperability testing across services demands specialized expertise and infrastructure. Cybersecurity vulnerabilities may emerge when bridging legacy and modern systems, necessitating additional safeguards. Skilled systems engineering and integration talent remains limited relative to increasing technological complexity. Budgetary constraints can restrict the scope of modernization programs. As a result, integration complexity increases lifecycle costs and slows operational deployment.

Dependence on Imported Critical ISR Technologies and Components:

Dependence on Imported Critical ISR Technologies and Components constrains market resilience and strategic autonomy by exposing supply chains to external risks. Advanced sensors, specialized electronics, and select software modules often rely on foreign suppliers. Export control regulations and geopolitical considerations can disrupt procurement schedules and technology access. Limited technology transfer restricts customization for specific operational requirements. Import-related cost volatility complicates long-term budget planning. Maintenance dependencies affect system availability throughout service life. Indigenous substitutes require extended development, testing, and certification cycles. Qualification processes for domestically developed components can delay induction. Strategic autonomy objectives remain partially unmet under such dependencies. Addressing this challenge requires sustained domestic capability development.

Opportunities

Expansion of Indigenous ISR System Design and Manufacturing Capabilities:

Expansion of Indigenous ISR System Design and Manufacturing Capabilities represents a major opportunity for the India Intelligence Surveillance Reconnaissance market as national security policy increasingly prioritizes self-reliance, localized value chains, and long-term capability ownership. Government-backed defense manufacturing frameworks encourage domestic firms to move beyond component supply toward complete system design, integration, and lifecycle support. Indigenous development reduces exposure to external supply disruptions while improving program execution predictability. Locally designed ISR solutions can be optimized for specific terrain, climate, and mission profiles unique to national operational environments. Cost efficiencies emerge through reduced import dependence, localized maintenance, and shorter logistics chains. Growing confidence in domestic engineering capability strengthens procurement preference for locally developed systems. Export potential expands as partner nations seek affordable and customizable ISR platforms. Skill development initiatives enhance systems engineering depth across public and private sectors. Collectively, these dynamics position indigenous ISR manufacturing as a structurally sustainable growth opportunity.

Growth of Space-Based Surveillance and Advanced Intelligence Analytics Ecosystems:

Growth of Space-Based Surveillance and Advanced Intelligence Analytics Ecosystems offers a high-impact opportunity for the India Intelligence Surveillance Reconnaissance market as space assets become central to modern intelligence architectures. Expanding satellite constellations enable persistent earth observation, signals collection, and strategic monitoring across wide geographic areas. Space-based ISR supports early warning, force posture assessment, and long-term threat analysis. Downstream analytics platforms convert satellite data into actionable intelligence for multiple defense users. Integration of artificial intelligence accelerates image interpretation and anomaly detection. Public private collaboration enhances capacity expansion and technology infusion. Dual-use commercial participation improves economic viability of space surveillance investments. Secure data processing frameworks strengthen trust across agencies. Long-term mission requirements ensure sustained demand for space-enabled intelligence solutions.

Future Outlook

The India Intelligence Surveillance Reconnaissance market is expected to maintain steady growth over the next five years, supported by sustained defense modernization and indigenization policies. Technological advancements in sensors, analytics, and secure communications will shape procurement priorities. Regulatory support for domestic manufacturing will enhance supply resilience. Demand-side factors such as border security, maritime awareness, and space surveillance will continue to drive long-term investment momentum.

Major Players

- Bharat Electronics Limited

- Hindustan Aeronautics Limited

- Larsen and Toubro Defence

- Tata Advanced Systems

- Mahindra Defence Systems

- Alpha Design Technologies

- Data Patterns India

- Astra Microwave Products

- Paras Defence and Space Technologies

- Centum Electronics

- MTAR Technologies

- ideaForge Technology

- NewSpace India Limited

- Ananth Technologies

Key Target Audience

- Defense ministries and armed forces

- Intelligence and security agencies

- Aerospace and defense manufacturers

- System integrators and OEMs

- Investments and venture capitalist firms

- Government and regulatory bodies

- Satellite and space service providers

- Homeland security organizations

Research Methodology

Step 1: Identification of Key Variables

Key variables related to platforms, technologies, procurement channels, and end users were identified through defense publications and budget documents. Operational requirements and policy drivers were mapped. Technology maturity levels were assessed. Market boundaries were defined.

Step 2: Market Analysis and Construction

Data from official defense sources and company disclosures were analyzed. Segment-level demand patterns were structured. Competitive positioning was evaluated. Market size consistency checks were applied.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through expert interviews and technical reviews. Assumptions were stress-tested. Policy implications were assessed. Revisions were incorporated.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into structured sections. Quantitative and qualitative findings were aligned. Consistency and compliance checks were completed. Final documentation was prepared.

- Executive Summary

- India Intelligence Surveillance Reconnaissance Market Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising defense modernization and network-centric warfare adoption

Expansion of border surveillance and maritime domain awareness initiatives

Increased reliance on unmanned and space-based reconnaissance platforms

Integration of artificial intelligence for real-time intelligence processing

Growing inter-agency intelligence sharing and joint operational frameworks - Market Challenges

High system integration complexity across legacy platforms

Dependence on imported critical subsystems and technologies

Data security and cyber vulnerability risks in ISR networks

Budget allocation constraints and long procurement cycles

Skilled workforce shortages for advanced ISR operations - Market Opportunities

Indigenous development under national defense manufacturing programs

Expansion of satellite-based and high-altitude ISR capabilities

Private sector participation in analytics and software-driven ISR solutions - Trends

Shift toward multi-domain integrated ISR architectures

Growing use of autonomous and remotely operated surveillance assets

Increased emphasis on real-time data fusion and decision support

Adoption of cloud-enabled intelligence processing environments

Enhanced focus on persistent surveillance and wide-area monitoring - Government Regulations & Defense Policy

Strengthening of indigenization and import substitution mandates

Policy support for private sector and startup participation in defense

Emphasis on secure data governance and classified information handling - SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Signals Intelligence Systems

Imagery Intelligence Systems

Electronic Intelligence Systems

Measurement and Signature Intelligence Systems

Cyber Intelligence and Network Surveillance Systems - By Platform Type (In Value%)

Airborne ISR Platforms

Land-Based ISR Platforms

Naval ISR Platforms

Space-Based ISR Platforms

Unmanned ISR Platforms - By Fitment Type (In Value%)

New Platform Integration

Retrofit and Upgrade Installations

Portable and Deployable Systems

Fixed Infrastructure Installations

Mobile Tactical Installations - By EndUser Segment (In Value%)

Army and Ground Forces

Air Force and Aerospace Commands

Naval Forces and Coast Guard

Intelligence Agencies and Strategic Commands

Homeland Security and Border Forces - By Procurement Channel (In Value%)

Direct Government Contracts

Defense Public Sector Undertakings

Strategic Partnership Programs

Offset and Technology Transfer Agreements

Emergency and Fast-Track Procurements - By Material / Technology (in Value %)

Electro Optical and Infrared Sensors

Radar and Synthetic Aperture Radar Technologies

Signals and Electronic Intelligence Technologies

Data Fusion and Analytics Software

Artificial Intelligence Enabled Surveillance Systems

- Market structure and competitive positioning

- Market share snapshot of major players

CrossComparison Parameters [System Integration Capability, Sensor Portfolio Breadth, Indigenous Content Level, Software and Analytics Strength, Platform Compatibility, Lifecycle Support Capability, Cybersecurity Robustness, Program Management Experience, Strategic Partnerships] - SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Bharat Electronics Limited

Hindustan Aeronautics Limited

Larsen and Toubro Defence

Tata Advanced Systems

Mahindra Defence Systems

Alpha Design Technologies

Data Patterns India

Astra Microwave Products

Paras Defence and Space Technologies

Centum Electronics

MTAR Technologies

ideaForge Technology

NewSpace India Limited

Ananth Technologies

Solar Industries Defence Systems

- Defense forces prioritizing integrated battlefield awareness

- Intelligence agencies focusing on multi-source data fusion

- Naval and air commands emphasizing persistent domain monitoring

- Homeland security users adopting rapid deployment surveillance solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now