Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India’s last-mile delivery market is valued at approximately USD ~ billion based on a recent historical assessment, supported by data referenced from logistics industry analyses by RedSeer Strategy Consultants and the India Brand Equity Foundation. Growth is driven by the rapid expansion of e-commerce platforms, hyperlocal delivery services, and quick-commerce grocery models that require efficient urban logistics networks. Increasing smartphone penetration, rising digital payments adoption, and expanding online retail ecosystems are significantly increasing parcel volumes across metropolitan and emerging urban consumption zones.

Major urban centers such as Delhi NCR, Mumbai, Bengaluru, Hyderabad, and Chennai dominate the India last-mile delivery ecosystem due to dense consumer populations, strong e-commerce infrastructure, and high digital commerce adoption. These cities host extensive warehouse networks, fulfillment centers, and transportation hubs that enable rapid parcel movement. Large technology-driven logistics startups and integrated courier networks operate heavily within these regions because strong road connectivity, high internet penetration, and concentrated retail demand create ideal environments for efficient last-mile logistics operations.

Market Segmentation

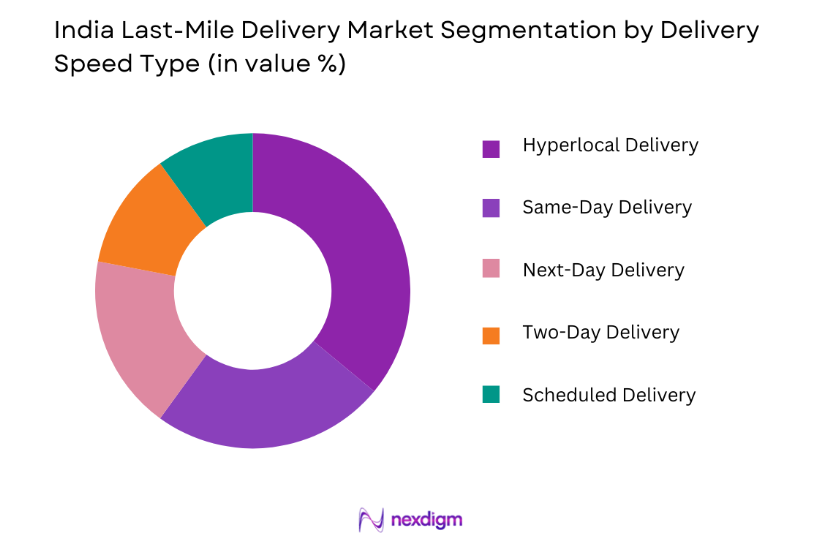

By Delivery Speed Type

India Last-Mile Delivery Market is segmented by Delivery Speed type into Same-Day Delivery, Next-Day Delivery, Two-Day Delivery, Hyperlocal Delivery, and Scheduled Delivery. Recently, Hyperlocal Delivery has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. The rise of quick-commerce grocery platforms, pharmacy deliveries, restaurant aggregators, and instant retail services has significantly increased the demand for hyperlocal logistics networks. Companies have invested heavily in micro-fulfillment centers and dark stores within dense urban neighborhoods to support rapid order fulfillment. Short-distance delivery models reduce logistics costs and enable companies to handle high-frequency orders efficiently. Retailers, e-commerce platforms, and direct-to-consumer brands increasingly rely on hyperlocal networks to provide faster delivery experiences that improve customer satisfaction and strengthen consumer loyalty.

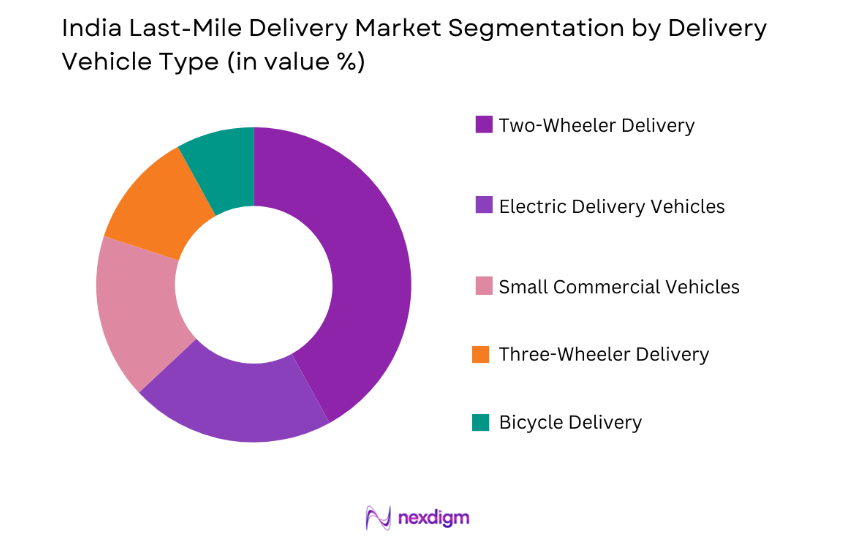

By Delivery Vehicle Type

India Last-Mile Delivery Market is segmented by Delivery Vehicle type into Two-Wheeler Delivery, Three-Wheeler Delivery, Small Commercial Vehicles, Electric Delivery Vehicles, and Bicycle Delivery. Recently, Two-Wheeler Delivery has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. Two-wheelers are highly suitable for navigating congested urban roads and narrow streets in large Indian cities, allowing faster deliveries compared with larger vehicles. Logistics companies widely deploy motorcycle fleets because they are cost-effective, fuel-efficient, and flexible for high-volume order fulfillment. The growth of quick-commerce platforms, food delivery services, and hyperlocal retail deliveries further strengthens the reliance on two-wheelers. Many delivery startups have also expanded gig-based rider networks, which significantly increases delivery capacity while keeping operational costs relatively low.

Competitive Landscape

The India last-mile delivery market is highly competitive and moderately consolidated, with both technology-driven startups and large logistics corporations operating extensive delivery networks. Major players focus on technology integration, route optimization software, warehouse automation, and AI-driven logistics platforms to improve operational efficiency. Strategic partnerships with e-commerce companies, retail chains, and digital marketplaces enable logistics providers to expand their delivery networks. Rapid growth in quick-commerce and hyperlocal delivery services has encouraged aggressive expansion strategies, including investments in micro-warehousing infrastructure and electric delivery fleets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Network Size |

| Delhivery | 2011 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Ecom Express | 2012 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Shadowfax | 2015 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| XpressBees | 2015 | Pune, India | ~ | ~ | ~ | ~ | ~ |

| Blue Dart Express | 1983 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

India Last-Mile Delivery Market Analysis

Growth Drivers

Expansion of E Commerce and Digital Retail Platforms

India’s last-mile delivery ecosystem is strongly supported by the rapid expansion of digital retail platforms that generate large parcel volumes across metropolitan and emerging urban markets. E-commerce marketplaces and direct-to-consumer brands increasingly rely on advanced logistics networks to fulfill rising consumer expectations for faster deliveries. Mobile commerce adoption has significantly expanded the base of online shoppers across urban and semi-urban regions, increasing order frequency across categories such as electronics, groceries, fashion, and pharmaceuticals. Retailers now prioritize delivery speed as a key competitive factor, encouraging investment in micro-fulfillment centers and distributed warehousing networks. Logistics firms are integrating automated sorting centers and advanced route planning systems to manage growing parcel flows efficiently. The expansion of quick-commerce grocery services further accelerates the demand for hyperlocal delivery networks capable of fulfilling orders within short time windows. Large logistics companies are also investing heavily in artificial intelligence powered delivery management systems that optimize routing, reduce operational costs, and improve delivery timelines. These developments collectively strengthen the growth trajectory of the India last-mile delivery market as online commerce continues expanding across the country.

Growth of Hyperlocal Logistics and Quick Commerce Ecosystems

The emergence of hyperlocal logistics models and quick-commerce platforms has significantly accelerated the expansion of the India last-mile delivery market. Consumers increasingly demand rapid order fulfillment for groceries, medicines, and daily essentials, which encourages retailers and digital marketplaces to establish hyperlocal delivery infrastructure. Quick-commerce companies are building dark stores and neighborhood fulfillment hubs that enable extremely short delivery distances and faster order processing. Logistics providers have adapted their operations to support these rapid fulfillment systems by expanding two-wheeler delivery fleets and gig-based rider networks. Technology platforms now utilize artificial intelligence for demand forecasting, route optimization, and delivery scheduling, which improves operational efficiency. Food delivery aggregators, pharmacy platforms, and hyperlocal retail networks collectively generate extremely high delivery frequency in urban areas. Logistics startups and established courier companies increasingly collaborate with quick-commerce platforms to scale operations across multiple cities. These partnerships accelerate network expansion while enabling companies to maintain delivery speed and service reliability. As hyperlocal commerce continues expanding in large Indian cities, demand for advanced last-mile logistics infrastructure will continue strengthening across the country.

Market Challenges

Urban Infrastructure Congestion and Delivery Inefficiencies

Urban infrastructure congestion presents a major operational challenge for companies operating in the India last-mile delivery market. Large metropolitan cities experience heavy traffic congestion, limited parking infrastructure, and complex road networks that slow down delivery vehicles and increase logistics costs. Delivery riders and drivers often face unpredictable travel times, which makes it difficult for logistics providers to maintain consistent delivery schedules. Rapid urbanization and rising vehicle density continue intensifying congestion across major logistics corridors. Logistics firms must invest in route optimization technologies and advanced fleet management systems to minimize delays and improve operational efficiency. However, implementing such technologies requires substantial capital investment and technical expertise. Companies also need to manage large gig-workforce networks while ensuring service quality and timely deliveries. Increasing delivery volumes further strain urban logistics infrastructure, especially during peak shopping seasons and major promotional sales events. As order volumes continue rising, congestion related challenges will remain a significant barrier for logistics companies attempting to scale efficient last-mile delivery operations across densely populated Indian cities.

High Operational Costs and Workforce Management Complexity

Managing operational costs and workforce logistics presents another significant challenge within the India last-mile delivery market. Logistics providers must handle rising fuel costs, vehicle maintenance expenses, and technology infrastructure investments while maintaining competitive delivery pricing. Gig economy delivery models require continuous recruitment, training, and management of large delivery partner networks. Maintaining workforce retention becomes difficult due to fluctuating order volumes and varying income stability for delivery personnel. Companies must also ensure compliance with labor regulations and safety standards for delivery riders and drivers. Rapid network expansion across multiple cities increases the complexity of coordinating warehouses, fulfillment centers, and delivery fleets. Logistics firms must continuously optimize route planning, delivery batching, and warehouse operations to maintain profitability. Additionally, competition between multiple logistics startups creates pricing pressure that limits profit margins across the industry. Balancing cost efficiency while delivering faster services therefore remains a persistent operational challenge for logistics companies operating within the India last-mile delivery ecosystem.

Opportunities

Adoption of Electric Vehicles in Delivery Fleets

The rapid adoption of electric vehicles within logistics fleets presents a major opportunity for companies operating in the India last-mile delivery market. Electric two-wheelers and small commercial vehicles offer lower operating costs compared with conventional fuel-based vehicles, which significantly improves long-term delivery economics. Logistics companies are increasingly partnering with electric mobility manufacturers to deploy sustainable delivery fleets across large cities. Government incentives and supportive regulatory policies are encouraging the adoption of electric mobility within urban transportation networks. Delivery companies benefit from reduced fuel expenses, lower maintenance requirements, and improved sustainability credentials when integrating electric vehicles into their operations. E-commerce companies and logistics providers also aim to meet environmental sustainability targets by transitioning toward zero-emission delivery fleets. Charging infrastructure expansion across metropolitan areas further strengthens the viability of electric logistics vehicles. Several logistics startups have already launched pilot projects deploying electric delivery fleets for hyperlocal deliveries. As environmental regulations and sustainability expectations continue strengthening, electric vehicle adoption will become a key growth opportunity for the India last-mile delivery industry.

Integration of Artificial Intelligence and Logistics Automation Systems

Artificial intelligence and logistics automation technologies present substantial growth opportunities within the India last-mile delivery market. Logistics companies are increasingly deploying AI-driven platforms to improve route optimization, demand forecasting, and delivery scheduling. These technologies enable companies to reduce delivery times, optimize fuel consumption, and improve parcel tracking accuracy. Automated sorting centers equipped with robotics and intelligent scanning systems significantly increase parcel handling efficiency in distribution hubs. Real-time data analytics also allows logistics providers to anticipate demand surges during promotional sales and seasonal shopping periods. Delivery companies are integrating machine learning algorithms into fleet management platforms to dynamically adjust delivery routes based on traffic conditions. AI-powered customer communication tools also improve delivery transparency by providing accurate shipment tracking updates. As parcel volumes continue increasing, automation technologies will help logistics providers maintain service efficiency and scalability. Investments in logistics automation therefore represent a key opportunity for companies seeking to strengthen operational performance within India’s rapidly expanding last-mile delivery ecosystem.

Future Outlook

The India last-mile delivery market is expected to experience sustained expansion as digital commerce ecosystems continue evolving and consumer expectations for faster delivery services intensify. Technological innovation in logistics automation, artificial intelligence driven route optimization, and electric delivery fleets will reshape operational models across the industry. Government initiatives supporting digital infrastructure and sustainable transportation are also expected to accelerate logistics modernization. Increasing demand from quick-commerce platforms, e-commerce retailers, and direct-to-consumer brands will continue driving large parcel volumes across urban and semi-urban markets.

Major Players

- Delhivery

- Ecom Express

- Shadowfax

- XpressBees

- Blue Dart Express

- Amazon Transportation Services

- Flipkart Logistics

- DHL Supply Chain India

- FedEx Express India

- DTDC Express

- Loadshare Networks

- Rivigo Logistics

- Dunzo

- Swiggy Genie

- Borzo India

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- E-commerce companies

- Logistics and supply chain companies

- Retail and direct-to-consumer brands

- Transportation infrastructure companies

- Technology platform providers

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the India last-mile delivery market were identified through industry data analysis, logistics network assessments, and digital commerce growth trends. Variables included delivery infrastructure, e-commerce demand patterns, fleet composition, urban logistics constraints, and technology adoption across logistics operations.

Step 2: Market Analysis and Construction

Market sizing and structural analysis were conducted using secondary research sources including logistics industry reports, government transport publications, and digital commerce datasets. Data points were consolidated to construct a comprehensive view of parcel volumes, delivery infrastructure, and logistics service networks.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses were validated through expert consultations with logistics executives, supply chain managers, and technology providers operating within the Indian logistics ecosystem. These discussions helped verify operational trends, technology adoption patterns, and evolving logistics business models.

Step 4: Research Synthesis and Final Output

All research insights were synthesized through comparative data analysis and structured modeling to produce a comprehensive report. The final output integrates market size estimates, competitive dynamics, segmentation insights, and future growth drivers influencing the India last-mile delivery market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E-commerce and Online Retail Platforms

Increasing Demand for Same-Day and Express Delivery Services

Growth of Urbanization and Digital Payment Ecosystems - Market Challenges

Urban Traffic Congestion and Delivery Delays

High Operational Costs for Last-Mile Logistics

Complexities in Address Mapping and Route Optimization - Market Opportunities

Adoption of Electric Vehicles for Sustainable Delivery Operations

Expansion of Hyperlocal Delivery Networks in Tier-II and Tier-III Cities

Integration of AI-Based Route Optimization Technologies - Trends

Growing Adoption of Micro-Fulfillment Centers in Urban Areas

Increasing Use of Electric Two-Wheelers for Urban Deliveries - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Services

Hyperlocal Delivery Services

Same-Day Delivery Services

Scheduled Delivery Services

Crowdsourced Delivery Services - By Platform Type (In Value%)

Road-Based Delivery Platforms

Two-Wheeler Delivery Platforms

Electric Vehicle Delivery Platforms

Drone and Autonomous Delivery Platforms - By Fitment Type (In Value%)

Dedicated Delivery Fleet Services

Third-Party Logistics Delivery Services

Crowdsourced Delivery Networks

Integrated E-commerce Fulfillment Solutions - By End User Segment (In Value%)

E-commerce and Online Retail Companies

Food and Grocery Delivery Platforms

Pharmaceutical and Healthcare Delivery Services

- Market Share Analysis

- Cross Comparison Parameters (Delivery Network Coverage, Fleet Size and Vehicle Mix, Technology Integration Level, Delivery Speed and Service Reliability, Pricing Competitiveness, Urban Distribution Infrastructure, Partnerships with E-commerce Platforms)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Delhivery

Ecom Express

Shadowfax

XpressBees

Blue Dart Express

DHL eCommerce India

DTDC Express

Gati Limited

Amazon Transportation Services India

Flipkart Logistics

Dunzo

Borzo

Porter

Swiggy Genie

Rapido Logistics

- E-commerce Platforms Driving Demand for High-Speed Delivery Networks

- Food Delivery Companies Expanding Hyperlocal Logistics Infrastructure

- Retail Chains Integrating Online-to-Offline Delivery Capabilities

- Healthcare Providers Increasing Home Delivery of Medicines and Medical Supplies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now