Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India’s oleochemicals market is valued at approximately USD ~ billion based on a recent historical assessment, driven by strong downstream demand from personal care, homecare, food additives, lubricants, and pharmaceutical excipients. Expansion of domestic surfactant and specialty chemical manufacturing, supported by vegetable oil availability and integrated refining capacity, has strengthened feedstock linkages. Government incentives for bio-based chemicals and rising substitution of petrochemicals with renewable fatty derivatives continue to accelerate industrial adoption across multiple end-use sectors.

Western and southern industrial corridors dominate India’s oleochemicals market due to port-based feedstock access, established oleochemical clusters, and proximity to FMCG, specialty chemical, and pharmaceutical manufacturing ecosystems. Gujarat and Maharashtra lead production through integrated fatty acid and glycerin facilities, while Tamil Nadu supports downstream surfactants and personal care intermediates manufacturing. Export-oriented processing zones and refinery-linked chemical parks in these regions enable efficient logistics, contract manufacturing scale, and supply continuity for domestic and international buyers.

Market Segmentation

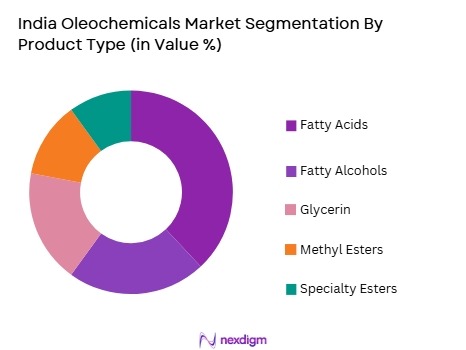

By Product Type

India oleochemicals market is segmented by product type into fatty acids, fatty alcohols, glycerin, methyl esters, and specialty esters. Recently, fatty acids has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Fatty acids serve as foundational intermediates across soaps, detergents, rubber additives, lubricants, and personal care formulations, ensuring consistent high-volume consumption. Domestic vegetable oil refining generates reliable fatty acid feedstock streams, supporting integrated production economics. Large FMCG and surfactant manufacturers maintain long-term procurement contracts, stabilizing demand cycles. Additionally, fatty acids enable derivative production into alcohols, amides, and esters, reinforcing their central position across oleochemical value chains and sustaining dominant share across industrial and consumer applications.

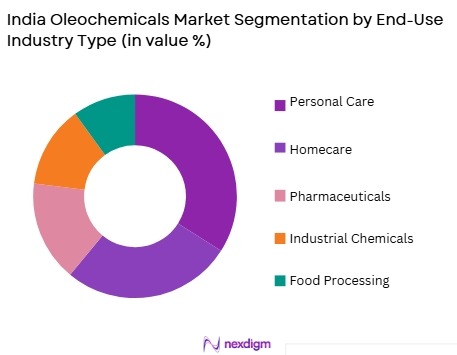

By End-Use Industry

India oleochemicals market is segmented by end-use industry into personal care, homecare, pharmaceuticals, food processing, and industrial chemicals. Recently, personal care has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Rapid growth of domestic cosmetics, toiletries, and hygiene products has increased consumption of fatty alcohols, glycerin, and esters. Rising disposable incomes and urban grooming trends sustain product innovation and ingredient demand. Multinational and domestic brands maintain local sourcing strategies, reinforcing stable procurement volumes. Regulatory preference for bio-based ingredients in cosmetics further supports oleochemical substitution, consolidating personal care leadership within India’s downstream oleochemical consumption landscape.

Competitive Landscape

India’s oleochemicals market exhibits moderate consolidation with integrated vegetable oil refiners and specialty chemical producers controlling upstream fatty intermediates and downstream derivatives. Major players leverage feedstock integration, export channels, and FMCG supply agreements to maintain scale advantages. Regional clusters support contract manufacturing, while multinational ingredient companies compete through specialty esters and high-purity glycerin. Capacity expansions and derivative diversification remain key competitive strategies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Feedstock Integration |

| Godrej Industries | 1897 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| VVF Ltd | 1939 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| KLK Oleo India | 1994 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| Adani Wilmar | 1999 | Ahmedabad | ~ | ~ | ~ | ~ | ~ |

| Emery Oleochemicals India | 1840 | Cincinnati / India ops | ~ | ~ | ~ | ~ | ~ |

India Oleochemicals Market Analysis

Growth Drivers

Expansion of domestic personal care and homecare manufacturing demand

Rapid expansion of domestic personal care and homecare manufacturing has increased demand for fatty acids, glycerin, and specialty esters, supported by urban consumption growth and organized retail penetration across India. Rising disposable incomes and hygiene awareness have expanded soap, detergent, and cosmetics production volumes, directly increasing oleochemical intermediate consumption across large FMCG manufacturing clusters located in western and southern India. Domestic brands and multinational subsidiaries increasingly localize ingredient sourcing to manage supply reliability and cost stability, strengthening long term procurement agreements with integrated oleochemical producers and reinforcing domestic capacity utilization. Growth of premium skincare, haircare, and specialty cleansing formulations requires higher purity fatty alcohols and esters, encouraging domestic manufacturers to expand derivative portfolios and upgrade refining technologies across established oleochemical clusters. Expansion of contract manufacturing for global personal care brands has increased export oriented production of oleochemical intermediates, positioning India as a regional supply hub and stabilizing demand cycles for fatty derivatives.

Integrated vegetable oil refining and feedstock availability advantages

India’s large scale vegetable oil refining infrastructure provides abundant fatty feedstock streams, enabling competitive oleochemical production economics and supporting expansion of fatty acids, alcohols, and glycerin manufacturing capacity across integrated coastal industrial zones. Port based refineries in Gujarat and Maharashtra facilitate import of palm and other oils, ensuring continuous raw material availability and reducing supply volatility for downstream oleochemical producers operating within adjacent chemical clusters. Integrated processing allows producers to capture value across refining, splitting, and derivative synthesis stages, lowering production costs and strengthening global competitiveness of India’s oleochemical exports in fatty intermediates and specialty esters.

Market Challenges

Volatility in imported vegetable oil feedstock pricing

India relies heavily on imported palm and other vegetable oils for oleochemical feedstock, exposing producers to global commodity price fluctuations that directly impact fatty acid and alcohol production costs and margins. International edible oil price volatility driven by weather disruptions, geopolitical factors, and export policies introduces procurement uncertainty for domestic oleochemical manufacturers operating within integrated refining value chains. Feedstock cost surges compress profitability of downstream derivatives such as esters and surfactants, particularly for contract manufacturers operating under fixed supply agreements with FMCG and chemical companies. Currency fluctuations further amplify import cost variability, creating planning challenges for producers managing long term procurement and pricing commitments in both domestic and export markets. Sudden feedstock price spikes may reduce competitiveness of bio based oleochemicals relative to petrochemical substitutes, affecting demand elasticity in cost sensitive industrial applications such as lubricants and rubber additives.

Competition from petrochemical substitutes in industrial applications

Despite sustainability advantages, oleochemicals compete with established petrochemical intermediates across lubricants, plasticizers, and surfactant applications where cost and performance consistency remain critical procurement criteria for industrial consumers. Petrochemical derivatives often benefit from large scale production and stable pricing linked to hydrocarbon feedstocks, creating competitive pressure on oleochemical alternatives during periods of elevated vegetable oil prices. Industrial buyers in rubber, coatings, and polymer additives sectors prioritize formulation stability and compatibility with existing petrochemical based systems, limiting rapid substitution toward bio based fatty derivatives in certain applications. Technical performance gaps in oxidative stability or temperature tolerance for some oleochemical esters restrict adoption in high performance industrial lubricants and specialty chemical formulations. Established supply chains and supplier relationships for petrochemical intermediates create switching barriers for downstream manufacturers evaluating oleochemical substitution strategies within cost sensitive product categories.

Opportunities

Growth of bio-based and sustainable chemical demand across industries

Increasing regulatory and consumer emphasis on renewable and biodegradable inputs is expanding demand for oleochemical intermediates across personal care, packaging, lubricants, and specialty chemical applications within India’s manufacturing ecosystem. Corporate sustainability commitments by FMCG and chemical companies are accelerating substitution of petrochemical surfactants and additives with plant derived fatty alcohols, acids, and esters sourced from domestic oleochemical producers. Government initiatives promoting green chemistry and bio based industrial materials create favorable policy conditions encouraging investment in oleochemical derivatives and specialty renewable intermediates across integrated chemical clusters. Export markets in Europe and Asia increasingly require renewable content and lifecycle emission reductions, positioning Indian oleochemical producers to capture growing international demand for certified bio-based ingredients.

Expansion of downstream specialty oleochemical derivatives manufacturing

Moving up the value chain into specialty esters, amides, and functional additives offers significant opportunity for Indian oleochemical producers to enhance margins and reduce exposure to commodity fatty intermediate price volatility. Specialty derivatives used in cosmetics, pharmaceuticals, lubricants, and food additives command higher value due to performance specificity, purity requirements, and formulation functionality demanded by advanced manufacturing sectors. India’s strong pharmaceutical and personal care manufacturing base provides domestic demand for high purity oleochemical derivatives, encouraging investment in advanced fractionation and synthesis technologies across established chemical clusters. Export potential for specialty esters and green additives continues expanding as global manufacturers diversify sourcing toward Asian producers offering competitive costs and technical capabilities. Integration of research and development with downstream application industries enables co development of customized oleochemical derivatives aligned with evolving formulation requirements and regulatory standards. Transition from bulk fatty acids toward functional ingredients increases differentiation and reduces direct competition with global commodity producers, strengthening strategic positioning of Indian firms.

Future Outlook

India’s oleochemicals market is expected to witness sustained expansion driven by rising bio-based chemical adoption, downstream FMCG and specialty chemical growth, and integrated refining capacity advantages. Technological upgrades in fractionation and derivative synthesis will enable higher value specialty production. Policy emphasis on renewable industrial inputs and sustainability will further accelerate substitution trends. Export demand and domestic consumption expansion together will reinforce capacity additions across oleochemical clusters over the coming years.

Major Players

- VVF Ltd

- Adani Wilmar

- KLK Oleo

- Emery Oleochemicals

- Oleon

- Musim Mas

- IOI Oleochemicals

- AAK

- Jocil Ltd

- 3F Industries

- Fine Organics

- Croda India

- BASF India

- Fairchem Organics

Key Target Audience

- FMCG manufacturers

- Personal care product manufacturers

- Pharmaceutical ingredient manufacturers

- Industrial lubricant producers

- Specialty chemical manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Packaging material producers

Research Methodology

Step 1: Identification of Key Variables

Key variables including feedstock availability, downstream demand sectors, production capacity, trade flows, and pricing dynamics were mapped across India’s oleochemical value chain to establish analytical scope and segmentation structure.

Step 2: Market Analysis and Construction

Supply demand balances, industry capacity distribution, downstream consumption patterns, and trade statistics were synthesized to construct market sizing and segmentation estimates aligned with industrial production and application trends.

Step 3: Hypothesis Validation and Expert Consultation

Industry participants including producers, downstream manufacturers, and sector specialists were consulted to validate demand drivers, competitive positioning, technological trends, and structural constraints shaping India’s oleochemical industry landscape.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights were integrated to develop market structure, competitive landscape, and strategic outlook, ensuring consistency across segmentation, growth factors, and industry dynamics reflected in the final analysis.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for bio-based surfactants in home and personal care manufacturing

Expansion of domestic palm oil refining and downstream oleochemical capacity

Policy push for green chemicals and biodegradable industrial inputs - Market Challenges

Feedstock price volatility linked to edible oil supply cycles

Competition from petrochemical derived substitutes in industrial applications

Import dependence for specific fatty alcohol and specialty derivatives - Market Opportunities

Development of high purity specialty oleochemicals for pharma and cosmetics

Export growth in Asia and Europe for sustainable fatty acid derivatives

Integration with biodiesel and glycerin downstream value chains - Trends

Shift toward RSPO certified sustainable palm based oleochemicals

Capacity expansion in fatty alcohol and specialty ester segments

Adoption of continuous processing and green chemistry technologies - Government regulations

Environmental norms on effluent discharge and chemical processing emissions

Import duties and tariff structures on edible oils and oleochemical intermediates

Standards for biodegradable surfactants and cosmetic ingredient safety - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fatty Acids

Fatty Alcohols

Glycerin

Methyl Esters

Specialty Oleochemicals - By Platform Type (In Value%)

Palm Oil Based Feedstock

Soybean Oil Based Feedstock

Sunflower Oil Based Feedstock

Tallow Based Feedstock

Multi Feedstock Integrated Plants - By Fitment Type (In Value%)

Standalone Oleochemical Units

Integrated Oleochemical Complexes

Refinery Integrated Units

Downstream Derivative Plants

Toll Manufacturing Facilities - By End User Segment (In Value%)

Personal Care and Cosmetics

Soaps and Detergents

Food and Nutrition Ingredients

Lubricants and Greases

Pharmaceutical and Healthcare - By Procurement Channel (In Value%)

Direct Industrial Supply Contracts

Distributor and Chemical Traders

Export Trading Houses

- Market Share Analysis

- Cross Comparison Parameters (Product Portfolio Diversity, Feedstock Integration, Production Capacity, Sustainability Certification, Export Presence, Downstream Derivatives Integration, Cost Competitiveness, Application Industry Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Godrej Industries Chemicals

VVF India Limited

Adani Wilmar Limited

KLK Oleo India Pvt Ltd

Emami Agrotech Limited

3F Industries Limited

Aarti Industries Limited

Jayant Agro Organics Limited

Nuberg EPC Chemicals

VVF LLC India Operations

Wilmar Oleochemicals India

Patanjali Foods Limited

Bharat Petroleum Biofuels Division

Southern Petrochemical Industries Corporation

Ruchi Soya Industries Limited

- Personal care manufacturers increasing use of plant-based emollients and surfactants

- Detergent producers shifting to fatty acid based biodegradable ingredients

- Food ingredient firms using glycerin and esters in processing applications

- Pharma companies adopting oleochemical excipients and solvents

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now