Download PDF

Download PDF Download PDF

Download PDF- Policybazaar

- Coverfox Insurance Broking

- Acko General Insurance

- Digit Insurance

- HDFC ERGO General Insurance

- ICICI Lombard General Insurance

- Bajaj Allianz General Insurance

- Tata AIG General Insurance

- Reliance General Insurance

- SBI General Insurance

- Aditya Birla Health Insurance

- Niva Bupa Health Insurance

- Paytm Insurance Broking

- PhonePe Insurance Broking

- Amazon Pay Insurance Marketplace

Market Overview

India online insurance market recorded approximately USD ~ billion in digital gross written premiums based on a recent historical assessment, reflecting the value of policies sold through insurer websites, mobile apps, and aggregator platforms. Growth has been driven by expanding internet penetration exceeding ~ million users, regulatory enablement of eKYC and paperless onboarding, and rising consumer preference for instant policy issuance. Health and motor insurance digitization, alongside fintech distribution partnerships, has accelerated online channel adoption across insurers and intermediaries nationwide.

Major activity is concentrated in metropolitan and tier-1 urban regions including Mumbai, Bengaluru, Delhi NCR, Hyderabad, and Chennai due to higher digital literacy, insurance awareness, and fintech ecosystem density. These cities host insurer headquarters, aggregators, and technology providers, enabling rapid product innovation and distribution scale. Strong financial services infrastructure, startup investment flows, and smartphone-first consumer behavior further reinforce dominance. Tier-2 cities such as Pune, Ahmedabad, and Jaipur are emerging through mobile-led insurance access and regional language digital interfaces.

Market Segmentation

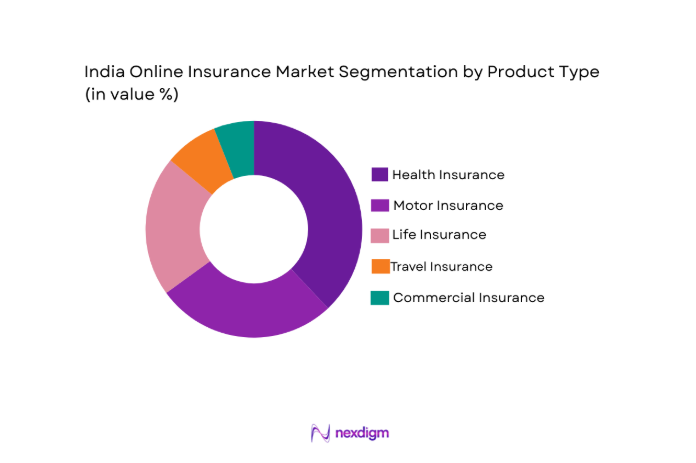

By Product Type

India online insurance market is segmented by product type into life insurance, health insurance, motor insurance, travel insurance, and commercial insurance. Recently, health insurance has a dominant market share due to rising medical inflation concerns, increased awareness after pandemic-era health risks, broader insurer product portfolios, and seamless digital underwriting. Cashless hospital networks integrated into apps, preventive wellness features, and family-floater policy demand have further strengthened online health insurance adoption among urban and semi-urban consumers seeking faster coverage issuance and policy management.

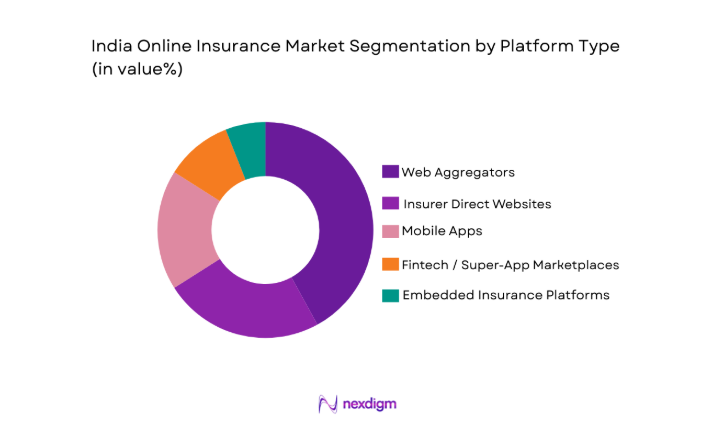

By Platform Type

India online insurance market is segmented by platform type into web aggregators, insurer direct websites, mobile apps, embedded insurance platforms, and fintech or super-app marketplaces. Recently, web aggregators have a dominant market share due to multi-insurer comparison capability, price transparency, marketing scale, and consumer trust in neutral platforms. Extensive digital advertising, simplified onboarding journeys, and policy servicing integrations have positioned aggregators as primary discovery and purchase channels, particularly for first-time buyers evaluating premiums and benefits across insurers.

Competitive Landscape

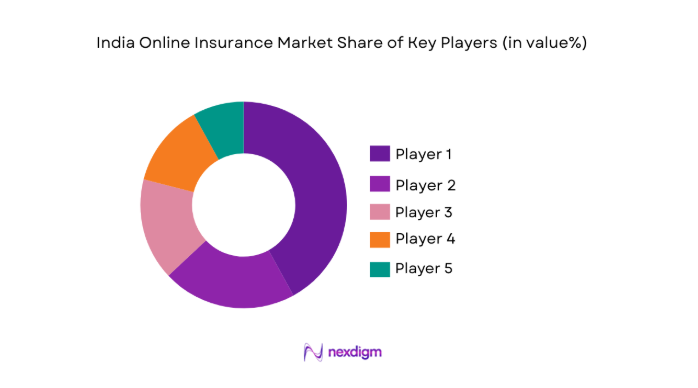

The India online insurance market shows moderate consolidation led by digital-first insurers and large aggregators that command distribution reach and brand recognition. Established insurers are strengthening proprietary digital channels while partnering with fintech ecosystems to expand embedded distribution. Technology capabilities such as AI underwriting, instant issuance, and digital claims are key competitive differentiators. Market leaders benefit from capital backing, nationwide insurer tie-ups, and advanced customer acquisition engines, creating entry barriers for smaller digital intermediaries.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Digital Channel Share |

| Policybazaar Insurance Brokers | 2008 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Acko General Insurance | 2016 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Digit Insurance | 2016 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| Coverfox Insurance Broking | 2013 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Paytm Insurance Broking | 2020 | Noida, India | ~ | ~ | ~ | ~ | ~ |

India Online Insurance Market Analysis

Growth Drivers

Digital Infrastructure Expansion and Smartphone-Led Insurance Adoption

The rapid expansion of mobile internet infrastructure and affordable smartphones has fundamentally transformed how insurance products are discovered, evaluated, and purchased across India, creating a structural shift toward online distribution channels that continues to deepen across demographics and geographies. With more than 900 million internet users and widespread 4G availability, consumers increasingly prefer mobile-first financial services experiences that mirror digital banking and payments adoption patterns, making online insurance a natural extension of established digital financial behavior. Insurers and aggregators have capitalized on this connectivity by building intuitive mobile applications, multilingual interfaces, and frictionless onboarding journeys that reduce policy purchase time from days to minutes, thereby increasing conversion rates and repeat engagement. The integration of Aadhaar-based eKYC, digital signatures, and instant document verification has removed legacy paperwork barriers that historically discouraged insurance purchases, enabling fully remote acquisition even in smaller towns and semi-urban markets where agent networks were previously limited. Digital payment ecosystems led by UPI, wallets, and embedded checkout insurance options have further simplified premium collection, allowing consumers to complete policy issuance within familiar transaction environments such as e-commerce or travel booking platforms. Insurers have also deployed targeted digital marketing, search optimization, and data-driven personalization to reach consumers at key life events such as vehicle purchase, travel planning, or health concerns, dramatically improving customer acquisition efficiency compared with traditional channels. The scalability of cloud-native policy administration systems allows insurers to handle surges in digital demand without proportional operational cost increases, improving profitability of online channels and incentivizing further investment. Regional language content and vernacular advertising campaigns are expanding adoption beyond metropolitan users, enabling new customer segments to access insurance digitally while overcoming linguistic barriers that previously constrained penetration. As telecom infrastructure continues to improve and smartphone replacement cycles increase device capability, online insurance engagement frequency, policy servicing interactions, and cross-selling potential are expected to expand further, reinforcing digital channels as the primary growth engine of the insurance distribution landscape.

Regulatory Digitization Enablement and Insurtech Ecosystem Partnerships

Progressive regulatory frameworks and active collaboration between insurers, fintech firms, and digital platforms have created an enabling environment that accelerates the expansion of online insurance distribution and product innovation across India’s financial services ecosystem. Regulatory authorities have introduced electronic KYC norms, digital policy issuance standards, and sandbox frameworks that allow insurers and technology startups to test new distribution models such as embedded insurance, usage-based coverage, and microinsurance products without prolonged approval cycles, thereby reducing innovation risk. The standardization of digital consent, document storage, and remote onboarding requirements has provided legal clarity that encourages insurers to invest in fully digital customer journeys while ensuring compliance with consumer protection and data privacy norms. Fintech platforms, payment wallets, e-commerce marketplaces, and mobility apps have integrated insurance offerings into their user journeys through APIs, creating contextual purchase opportunities at moments of financial decision-making such as travel bookings, device purchases, or loan applications, significantly expanding addressable reach beyond traditional insurance discovery channels. Venture capital investment in insurtech startups has funded advanced analytics, AI underwriting, telematics, and claims automation technologies that enhance pricing accuracy and operational efficiency, allowing insurers to offer competitively priced digital policies with faster issuance and settlement times. Partnerships between incumbent insurers and technology providers enable rapid deployment of cloud-based policy administration and customer engagement platforms without large legacy system overhauls, accelerating digital transformation timelines across the industry. Regulatory encouragement of paperless servicing, electronic policy repositories, and digital grievance redressal mechanisms has strengthened consumer trust in online insurance channels by improving transparency and accessibility of policy information. As ecosystem collaboration deepens and regulatory clarity around digital insurance operations continues to evolve, online distribution models are positioned to capture an increasing share of insurance sales, particularly among digitally engaged consumers and platform-based economic participants who prefer integrated financial services experiences.

Market Challenges

Low Insurance Literacy and Trust Deficit Among First-Time Digital Buyers

Despite rapid digital adoption in financial services, a substantial proportion of potential insurance customers remain unfamiliar with policy structures, coverage terms, and claims processes, creating hesitation and mistrust that slows conversion in online channels where human advisory support is limited. Many first-time buyers encounter difficulty interpreting exclusions, waiting periods, and benefit structures presented in digital interfaces, leading to decision deferral or reliance on offline agents perceived as more trustworthy advisors. Misunderstanding of insurance value propositions, particularly in health and life segments, reduces perceived necessity and price tolerance, constraining demand expansion beyond urban and financially literate populations. Negative perceptions arising from claim disputes or complex documentation requirements can spread quickly through social media and consumer forums, amplifying skepticism toward digital insurers and aggregators even when incidents are isolated. The absence of personalized guidance in fully digital journeys can result in inappropriate product selection, increasing dissatisfaction and policy lapse rates, which undermines long-term customer retention and brand reputation for online providers. Rural and older consumers often face additional barriers such as language limitations, low digital confidence, and limited access to reliable assistance during purchase or claims stages, reinforcing dependence on traditional intermediaries. Insurers must therefore invest significantly in educational content, assisted digital channels, and transparent policy communication to bridge literacy gaps, raising customer acquisition costs relative to digitally mature markets. Building sustained trust requires consistent claims performance, proactive communication, and simplified documentation standards that demonstrate reliability comparable to agent-mediated channels, a process that takes time and operational discipline. Until insurance literacy and digital trust levels improve broadly across demographics, online insurance penetration growth will remain uneven and concentrated among digitally confident segments.

Cybersecurity Risks, Data Privacy Compliance, and Fraud Exposure in Online Distribution

The shift toward fully digital insurance distribution exposes insurers and intermediaries to heightened cybersecurity threats, data privacy obligations, and fraud risks that increase operational complexity and compliance costs across the online insurance value chain. Online platforms collect sensitive personal, financial, and health information during policy issuance and servicing, making them attractive targets for cyberattacks such as data breaches, identity theft, and ransomware incidents that can erode consumer confidence and trigger regulatory penalties. Compliance with evolving data protection regulations requires continuous investment in secure infrastructure, encryption standards, access controls, and audit mechanisms, increasing technology expenditure and operational oversight requirements for insurers transitioning from legacy systems to cloud-based environments. Fraudulent policy applications, manipulated claims documentation, and identity impersonation attempts are more difficult to detect in remote onboarding processes, necessitating advanced analytics, biometric verification, and anomaly detection tools that raise implementation complexity. Digital aggregators and embedded insurance partners introduce additional third-party risk exposures, as vulnerabilities in partner systems can compromise shared data flows and customer information security. Regulatory scrutiny of digital consent management, cross-border data transfer, and customer data usage transparency further intensifies compliance burdens, particularly for insurers operating across multiple digital ecosystems and distribution partnerships. Any major cybersecurity incident or data misuse controversy can rapidly damage brand credibility in online channels where reputation is closely tied to perceived technological reliability. Insurers must therefore balance innovation speed with robust risk management frameworks, often slowing deployment of new digital features or partnerships due to security validation requirements. Maintaining secure, compliant, and fraud-resistant online insurance operations thus remains a significant structural challenge that demands sustained investment and specialized expertise across the industry.

Opportunities

Embedded Insurance Integration Across Digital Commerce and Mobility Ecosystems

The rapid growth of digital commerce, mobility services, travel platforms, and subscription-based consumer ecosystems creates significant opportunities for insurers to embed contextual insurance offerings seamlessly within everyday digital transactions, expanding reach to previously untapped customer segments. Consumers purchasing flights, booking cabs, renting vehicles, ordering electronics, or subscribing to digital services increasingly encounter integrated insurance options tailored to specific risks associated with those activities, reducing discovery friction and improving relevance compared with standalone policy marketing. Embedded insurance models leverage APIs to connect insurer underwriting and issuance systems directly into partner platforms, enabling real-time premium calculation and instant coverage activation within the host application’s checkout flow, which significantly increases conversion rates. Such integrations allow insurers to access high-frequency digital engagement environments with millions of active users, dramatically lowering customer acquisition costs relative to independent online marketing channels. Platform operators benefit from incremental revenue streams and enhanced customer value propositions, creating mutually reinforcing incentives for deeper insurance integration across ecosystems. Embedded models also facilitate microinsurance and short-duration coverage products suited to gig workers, travelers, device owners, and mobility users, expanding insurance penetration among populations historically underserved by traditional annual policies. Data generated within partner platforms, such as transaction history or usage behavior, supports more accurate risk assessment and personalized pricing, improving underwriting performance and product attractiveness. As digital commerce and service platforms continue expanding across India’s consumer economy, embedded insurance distribution is poised to become a major growth avenue for online insurance providers seeking scalable, context-driven customer acquisition.

AI-Driven Personalization and Usage-Based Insurance Product Innovation

Advances in artificial intelligence, telematics, wearable integration, and behavioral analytics enable insurers to design highly personalized and usage-based insurance products that align premiums more closely with individual risk profiles and lifestyle patterns, creating strong opportunities for differentiation and market expansion in online channels. AI-driven underwriting engines can analyze diverse data inputs such as driving behavior, health activity metrics, purchase patterns, and demographic attributes to generate individualized pricing and coverage recommendations in real time, enhancing perceived fairness and affordability for customers. Usage-based motor insurance leveraging telematics devices or smartphone sensors allows drivers to pay premiums proportional to actual driving habits, attracting cost-sensitive consumers and encouraging safer behavior while improving insurer loss ratios. Health insurance products incorporating wearable fitness data and preventive wellness engagement can reward healthy lifestyles with premium discounts or benefits, increasing customer engagement and retention through digital platforms. Personalized coverage bundles tailored to life stage events such as travel frequency, family structure, or employment type can be dynamically offered through online interfaces, improving relevance and cross-selling potential. AI-enabled claims automation using image recognition, document parsing, and predictive analytics accelerates settlement times, strengthening customer satisfaction and trust in digital insurers. Continuous learning from user interaction data allows insurers to refine product design and marketing strategies, increasing conversion efficiency over time. As regulatory acceptance of alternative data underwriting expands and consumer comfort with data-driven personalization grows, AI-enabled insurance innovation represents a substantial opportunity to deepen online insurance adoption and reshape product economics across the market.

Future Outlook

The India online insurance market is expected to expand steadily over the next five years as digital distribution becomes the primary channel for policy acquisition and servicing across major insurance segments. Continued smartphone growth, embedded insurance integration, and AI-enabled underwriting will enhance accessibility and personalization of coverage. Regulatory support for paperless processes and digital innovation will sustain industry transformation. Rising health awareness, mobility risks, and platform-based employment will further stimulate demand for flexible online insurance solutions nationwide.

Major Players

Key Target Audience

- Insurance companies

- Digital insurance aggregators

- Fintech and super-app platforms

- E-commerce platforms

- Mobility and travel platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Reinsurance companies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including digital gross written premiums, online policy volumes, platform penetration, consumer adoption drivers, and regulatory factors were identified through secondary research and industry frameworks. These variables defined the analytical scope and segmentation boundaries applied across the India online insurance ecosystem.

Step 2: Market Analysis and Construction

Comprehensive secondary data from regulatory filings, insurer disclosures, and digital platform metrics were synthesized to construct market size estimates and segmentation shares. Adoption drivers, technology trends, and distribution models were analyzed to map structural dynamics and competitive positioning within online insurance channels.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings and market assumptions were validated through consultations with insurance executives, digital distribution specialists, and technology providers. Expert insights refined segmentation logic, adoption drivers, and competitive dynamics, ensuring alignment with operational realities across insurers and digital intermediaries.

Step 4: Research Synthesis and Final Output

Validated data and insights were integrated into a structured analytical framework covering market size, segmentation, competitive landscape, and growth outlook. Quantitative estimates and qualitative drivers were synthesized to produce coherent conclusions on the evolution and future trajectory of the India online insurance market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising internet and smartphone penetration enabling digital policy purchases

Regulatory push for paperless onboarding and eKYC in insurance

Growth of fintech and super app ecosystems distributing insurance

Increasing consumer preference for instant policy issuance and servicing

Expansion of health and motor insurance awareness via digital channels - Market Challenges

Low insurance literacy among rural and first-time digital users

Fraud risks and cybersecurity concerns in online policy issuance

Dependence on aggregators impacting insurer margins

Complex claim servicing expectations in digital-only models

Regulatory compliance costs for digital distribution and data privacy - Market Opportunities

Embedded insurance across mobility, travel, and e-commerce platforms

AI-driven personalized insurance products and pricing

Expansion of microinsurance for underserved digital populations - Trends

Shift toward app-based policy lifecycle management

Integration of wellness and telematics data into underwriting

Growth of instant claim intimation and digital settlement

Rise of sachet and short-duration digital insurance products

Partnerships between insurers and fintech ecosystems - Government Regulations & Defense Policy

IRDAI digital insurance guidelines and sandbox frameworks

Data protection and digital consent compliance requirements

eKYC, Aadhaar, and digital document verification mandates - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Life Insurance Online Platforms

Health Insurance Online Platforms

Motor Insurance Online Platforms

Travel Insurance Online Platforms

Commercial Insurance Online Platforms - By Platform Type (In Value%)

Web Aggregator Platforms

Mobile App Platforms

Insurer Direct Portals

Embedded Insurance APIs

Marketplace Super Apps - By Fitment Type (In Value%)

Standalone Online Policies

Add-on Digital Riders

Usage-based Digital Policies

Subscription-based Coverage

On-demand Microinsurance - By End User Segment (In Value%)

Individual Retail Customers

SME Policyholders

Corporate Employee Groups

Gig and Platform Workers

Rural and Microinsurance Users - By Procurement Channel (In Value%)

Insurance Aggregator Websites

Insurer Direct Online Sales

Bancassurance Digital Channels

Fintech and Wallet Platforms

E-commerce Embedded Sales

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product Breadth, Distribution Model, Digital UX Capability, Pricing Transparency, Claims Digitization)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Policybazaar Insurance Brokers

Coverfox Insurance Broking

Acko General Insurance

Digit Insurance

HDFC ERGO General Insurance

ICICI Lombard General Insurance

Bajaj Allianz General Insurance

Tata AIG General Insurance

Reliance General Insurance

SBI General Insurance

Aditya Birla Health Insurance

Niva Bupa Health Insurance

Paytm Insurance Broking

PhonePe Insurance Broking

Amazon Pay Insurance Marketplace

- Urban millennials driving adoption of app-based insurance purchases

- SMEs adopting online commercial and employee coverage platforms

- Gig workforce demand for flexible and short-term policies

- Rural users accessing microinsurance through mobile channels

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

India online insurance market recorded about USD ~ billion in digital premiums.

This reflects policies sold through websites, apps, and aggregators.

Health insurance leads India online insurance market share. It holds about 38 percent of digital premiums.

Web aggregators dominate India online insurance market platforms. They account for about 42 percent share.

Policybazaar, Acko, and Digit lead India online insurance market. Large insurers and fintech platforms also participate.

Digital adoption and regulatory eKYC enable India online insurance market. Smartphone penetration and fintech partnerships accelerate sales.

India online insurance market will expand with embedded insurance. AI underwriting and mobile distribution will drive adoptio

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now