Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Para-Aramid Fibers market current size stands at around USD ~ million, driven by rising demand across defense, automotive, and industrial safety applications. The market reflects strong dependency on imports while gradually witnessing domestic manufacturing expansion. Increasing adoption of lightweight and high-strength materials continues to influence demand patterns. The integration of para-aramid fibers into advanced composites and protective systems is strengthening their role across critical sectors requiring durability, heat resistance, and impact protection.

Key demand centers are concentrated in regions such as Maharashtra, Tamil Nadu, and Karnataka due to strong industrial ecosystems and defense manufacturing hubs. Northern corridors including Uttar Pradesh are emerging with defense corridor initiatives. Ports and logistics infrastructure in Gujarat and Andhra Pradesh support imports and distribution. Policy-driven incentives, industrial clusters, and proximity to automotive and aerospace manufacturing units contribute to regional dominance, supported by improving supplier networks and technology adoption capabilities.

Market Segmentation

By Application

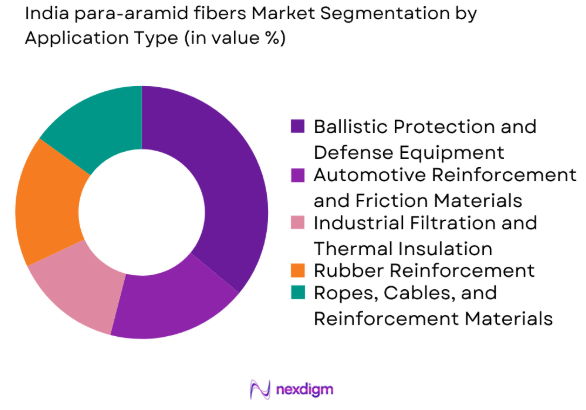

Ballistic Protection and Defense Equipment dominates the India para-aramid fibers market due to sustained procurement by defense and homeland security agencies. High demand for bullet-resistant vests, helmets, and armored systems continues to drive consumption. Automotive Reinforcement and Friction Materials follow, supported by increasing vehicle production and safety standards. Industrial Filtration and Thermal Insulation are gaining traction across high-temperature industrial environments. Rubber Reinforcement and Ropes, Cables, and Reinforcement Materials are widely used in heavy-duty applications. Aerospace and Advanced Composites are emerging segments driven by lightweight material adoption and performance requirements in aviation and defense manufacturing.

By Form

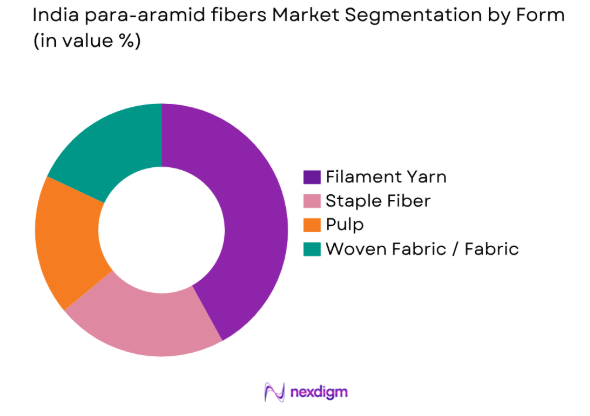

Filament Yarn dominates the market as it is extensively used in ballistic protection, composites, and reinforcement applications requiring high tensile strength and durability. Its superior mechanical properties make it suitable for advanced industrial and defense applications. Staple Fiber is widely used in filtration, protective apparel, and insulation materials due to ease of processing. Pulp finds application in friction materials such as brake pads and gaskets, particularly in the automotive sector. Woven Fabric or Fabric is increasingly utilized in protective clothing and composite structures, supported by growing industrial safety standards and expanding use in aerospace and high-performance applications.

Competitive Landscape

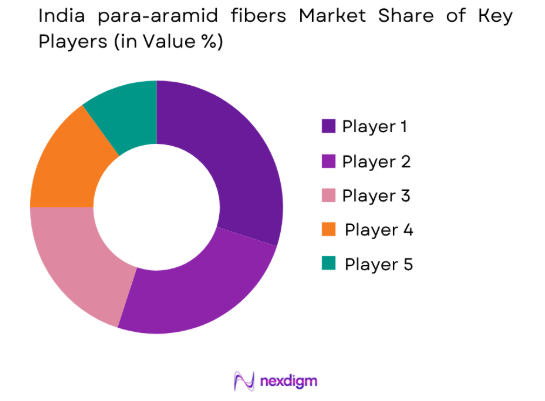

The India para-aramid fibers market is moderately consolidated with a mix of global manufacturers and emerging domestic participants. Competition is driven by product quality, supply reliability, and technological capabilities, while long-term contracts in defense and industrial sectors play a critical role in shaping competitive positioning.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| DuPont de Nemours, Inc. | 1802 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Teijin Limited | 1918 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Kolon Industries, Inc. | 1957 | South Korea | ~ | ~ | ~ | ~ | ~ | ~ |

| Hyosung Corporation | 1966 | South Korea | ~ | ~ | ~ | ~ | ~ | ~ |

| Toray Industries, Inc. | 1926 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

India Para-Aramid Fibers Market Analysis

Growth Drivers

Rising defense expenditure and demand for ballistic protection materials

India’s defense allocation reached 74 billion in 2024 with increasing focus on soldier protection systems and advanced armor solutions. Procurement of over 0.18 million bulletproof jackets and 0.12 million helmets has driven consumption of para-aramid fibers. Domestic manufacturing initiatives have accelerated under strategic programs, increasing demand for high-performance fibers. Border security requirements and modernization of armed forces continue to boost adoption. Additionally, paramilitary forces have expanded protective gear usage by 22 units per operational group, further supporting fiber demand across applications requiring impact resistance and thermal stability in extreme operating conditions.

Increasing adoption in automotive lightweighting and safety applications

India produced 28 million vehicles in 2024, with growing emphasis on fuel efficiency and safety standards driving lightweight material adoption. Para-aramid fibers are increasingly used in brake pads, tires, and reinforcement components. Electric vehicle production crossed 1.6 million units, accelerating demand for advanced materials with high strength-to-weight ratios. Regulatory safety norms have mandated improved braking systems and durability standards. Automotive OEMs have integrated composite materials in over 35 new models, enhancing structural efficiency. This shift is reinforcing demand for para-aramid fibers in high-performance automotive components across passenger and commercial vehicle segments.

Challenges

High production cost and complex manufacturing process

Para-aramid fiber production involves advanced polymerization processes requiring high precision and controlled environments. Manufacturing facilities typically operate at temperatures exceeding 200 degrees and require specialized equipment. Capital intensity remains high with setup timelines extending beyond 24 months. Limited domestic expertise increases dependency on imported technology. Production inefficiencies can lead to yield losses of up to 12 units per batch. Skilled labor shortages in chemical processing further complicate operations. These complexities restrict new entrants and limit rapid scalability of domestic manufacturing, impacting overall supply availability within the country.

Dependence on imported raw materials and technology

India relies heavily on imported precursors such as para-phenylenediamine and terephthaloyl chloride, with import volumes exceeding 85 units per supply cycle. Limited domestic chemical production capacity constrains backward integration. Technology transfer barriers and licensing restrictions hinder local innovation. Lead times for raw material procurement often extend beyond 60 days, affecting production planning. Currency fluctuations further impact procurement stability. Additionally, reliance on foreign technical expertise slows development of indigenous capabilities, making the market vulnerable to global supply chain disruptions and geopolitical uncertainties affecting material availability.

Opportunities

Localization of para-aramid fiber production

Government initiatives have identified high-performance fibers as strategic materials, with over 12 industrial projects approved under manufacturing incentive schemes. Domestic production capacity expansion is supported by new industrial zones across 6 states. Investment in chemical manufacturing infrastructure has increased significantly, enabling backward integration potential. Indigenous development programs have accelerated collaboration between defense laboratories and private manufacturers. Local production can reduce import dependency cycles currently exceeding 70 units annually. Improved supply chain resilience and reduced lead times are expected to strengthen domestic competitiveness and enable export opportunities across neighboring regions.

Expansion in electric vehicle and advanced mobility sectors

Electric vehicle adoption reached 1.6 million units in 2024, with projections indicating continued expansion across urban mobility segments. Advanced mobility solutions require lightweight, durable materials for battery protection, insulation, and structural reinforcement. Para-aramid fibers are increasingly integrated into battery casings and thermal management systems. Charging infrastructure installations exceeded 0.09 million units, supporting EV ecosystem growth. Automotive manufacturers are investing in new material technologies across 18 production facilities. This expansion is creating sustained demand for high-performance fibers capable of meeting stringent safety and performance requirements in next-generation mobility platforms.

Future Outlook

The India para-aramid fibers market is expected to witness sustained growth through 2035, driven by defense modernization, automotive innovation, and industrial safety requirements. Increasing domestic production capabilities and policy support will gradually reduce import dependency. Technological advancements and expanding end-use applications will further strengthen market penetration across emerging sectors.

Major Players

- DuPont de Nemours, Inc.

- Teijin Limited

- Kolon Industries, Inc.

- Hyosung Corporation

- Yantai Tayho Advanced Materials Co., Ltd.

- Huvis Corporation

- Toray Industries, Inc.

- SRO Aramid Co., Ltd.

- Kermel S.A.

- China National Bluestar

- Aramid HPM LLC

- Kamenskvolokno JSC

- Sinopec Yizheng Chemical Fibre Company

- Pingmei Shenma Group

- JSC Kamenskvolokno

Key Target Audience

- Defense procurement agencies including Ministry of Defence, India

- Automotive manufacturers and OEMs

- Aerospace component manufacturers

- Industrial safety equipment manufacturers

- Telecommunications infrastructure companies

- Chemical and advanced materials manufacturers

- Investments and venture capital firms

- Government and regulatory bodies including Bureau of Indian Standards

Research Methodology

Step 1: Identification of Key Variables

Key variables include fiber types, end-use industries, import dependency, and manufacturing capacity. Supply chain nodes, regulatory requirements, and procurement cycles are also identified. Demand drivers across defense and industrial sectors are mapped for analysis.

Step 2: Market Analysis and Construction

Data is structured across application segments and industry verticals. Trade flows, production patterns, and adoption rates are analyzed. Market behavior is constructed based on demand concentration and technological penetration across sectors.

Step 3: Hypothesis Validation and Expert Consultation

Insights are validated through interactions with manufacturers, distributors, and industry stakeholders. Technical experts provide inputs on production feasibility and application trends. Assumptions are refined based on real-world operational data.

Step 4: Research Synthesis and Final Output

All findings are consolidated into a structured framework. Analytical models are applied to ensure consistency and accuracy. Final outputs are developed with a focus on actionable insights and strategic clarity for stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and Para-Aramid Fiber Classification Standards, Domestic Production and Import-Export Trade Analysis, End-Use Industry Consumption Mapping across Defense and Industrial Applications, Raw Material and Precursor Supply Chain Assessment, Pricing Trends and Contract Benchmarking Analysis, Regulatory and Compliance Review for High-Performance Fibers, Primary Interviews with Fiber Manufacturers and Defense Procurement Agencies)

- Definition and Scope

- Market evolution and technological advancements in high-performance fibers

- Usage across defense, aerospace, automotive, and industrial protection applications

- Ecosystem structure including raw material suppliers, manufacturers, and converters

- Supply chain dynamics including imports, domestic production, and distribution channels

- Regulatory environment including defense standards and industrial safety norms

- Growth Drivers

Rising defense expenditure and demand for ballistic protection materials

Increasing adoption in automotive lightweighting and safety applications

Growth in fiber optic cable infrastructure

Expansion of industrial safety standards and protective gear usage

Technological advancements in high-performance fiber manufacturing

Increasing domestic manufacturing initiatives under Make in India - Challenges

High production cost and complex manufacturing process

Dependence on imported raw materials and technology

Limited domestic production capacity

Price volatility of precursor chemicals

Stringent regulatory approvals in defense applications

Competition from alternative high-performance fibers - Opportunities

Localization of para-aramid fiber production

Expansion in electric vehicle and advanced mobility sectors

Increasing demand for high-strength composites in aerospace

Growth in industrial automation and safety equipment

Export potential to emerging markets

Innovation in hybrid materials and composites - Trends

Shift toward sustainable and recyclable high-performance fibers

Integration of para-aramid fibers in advanced composite materials

Strategic collaborations between defense agencies and manufacturers

Adoption of advanced manufacturing technologies

Increasing R&D investments in fiber performance enhancement

Rising demand for lightweight and durable materials - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Production Capacity, 2020–2025

- By Average Selling Price, 2020–2025

- By Application (in Value %)

Ballistic Protection and Defense Equipment

Automotive Reinforcement and Friction Materials

Industrial Filtration and Thermal Insulation

Rubber Reinforcement

Ropes, Cables, and Reinforcement Materials

Aerospace and Advanced Composites - By Form (in Value %)

Filament Yarn

Staple Fiber

Pulp

Woven Fabric / Fabric - By End-Use Industry (in Value %)

Defense and Homeland Security

Automotive and Transportation

Electrical and Electronics

Industrial Manufacturing

Aerospace and Aviation - By Distribution Channel (in Value %)

Direct Sales to OEMs

Distributors and Traders

Government and Defense Procurement

- Market structure and competitive positioning

- Market share snapshot of major players in India Para Aramid Fibers Market, 2025

- Cross Comparison Parameters (Company Overview, USP, Business Strategies, Recent Developments, Revenues, Revenue Split by End Users, Production Capacity, Product Portfolio, Pricing Strategy, End-Use Focus, Geographic Presence, R&D Capability, Strategic Partnerships, Contract Wins)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

DuPont de Nemours, Inc.

Teijin Limited

Kolon Industries, Inc.

Hyosung Corporation

Yantai Tayho Advanced Materials Co., Ltd.

Huvis Corporation

Toray Industries, Inc.

SRO Aramid (Jiangsu) Co., Ltd.

Kermel S.A.

China National Bluestar (Group) Co., Ltd.

Aramid HPM LLC

JSC Kamenskvolokno

SRO Group (China)

SRO Aramid Fiber Co., Ltd.

China Pingmei Shenma Group

- Demand and utilization drivers across defense and industrial sectors

- Procurement and tender dynamics in government and private sectors

- Buying criteria focusing on strength, durability, and certification standards

- Budget allocation and financing preferences in defense and infrastructure projects

- Implementation barriers including certification and integration challenges

- Post-purchase service expectations including technical support and customization

- By Value, 2026–2035

- By Volume, 2026–2035

- By Production Capacity, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now