Download PDF

Download PDFMarket Overview

India’s salon market expanded from USD ~ billion to USD ~ billion, reflecting stronger spending on grooming, beauty, haircare, skincare, and salon-led wellness services. The rise has been supported by urbanisation, increasing disposable income, greater workforce participation among women, higher beauty consciousness, and the faster spread of organised salon chains into non-metro locations. Public industry trackers also note that organized salons crossed 13,000 outlets nationwide, reinforcing the structural shift toward branded and standardized service formats.

The market is led by Mumbai, Delhi-NCR, Bengaluru, Hyderabad, Chennai, and Pune, where higher disposable incomes, dense white-collar populations, wedding and occasion spending, stronger mall and high-street retail ecosystems, and deeper penetration of branded chains support repeated salon consumption. These cities also dominate because major networks have scaled there first before pushing deeper into Tier 2 and Tier 3 markets. Public operator disclosures show broad multi-city expansion by Naturals, Lakmé Salon, Green Trends, Enrich, and Looks, with metros remaining their brand-building anchors.

Market Segmentation

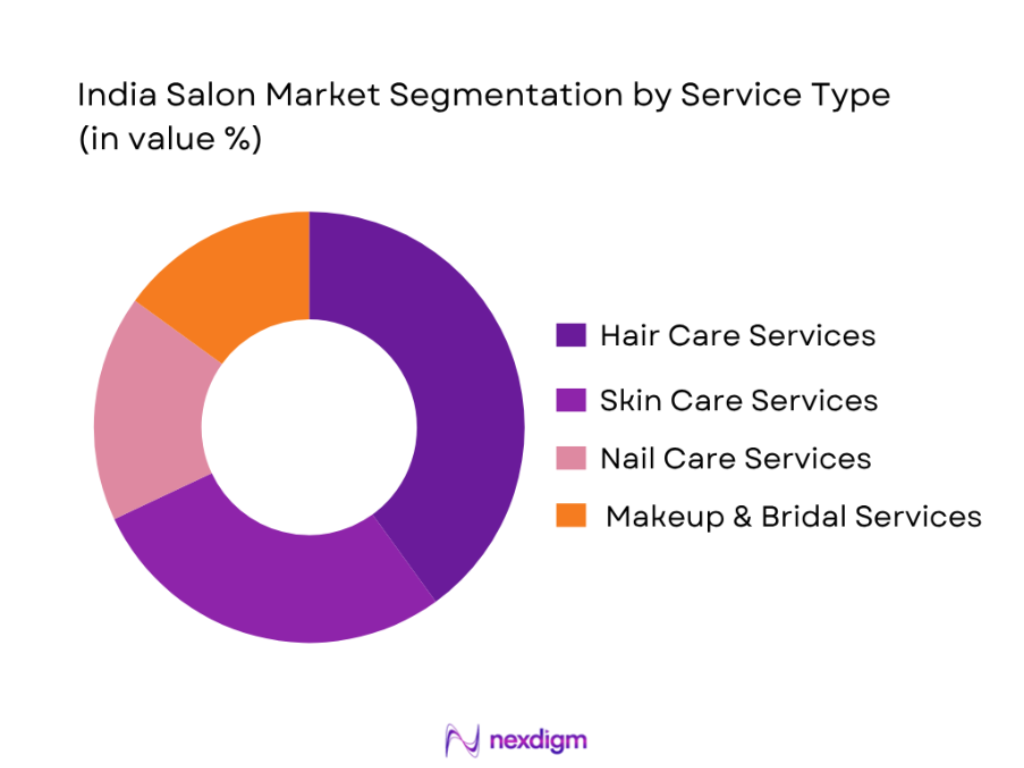

By Service Type

India salon market is segmented by service type into hair care services, skin care services, nail care services, and makeup & bridal services. Recently, hair care services have held the dominant market share in India under this segmentation, mainly because hair remains the most frequent and habit-driven salon need across both women and men. Haircuts, styling, colouring, smoothening, keratin, scalp care, and repair treatments create high visit frequency and stronger repeat traffic than most other categories. Public industry coverage states that haircare accounts for around 40% of salon demand, while multiple India-focused market trackers identify hair care as the largest service bucket. The dominance is also strengthened by the rapid scaling of chain salons, which typically use hair-led menus to build footfall and then upsell skin, nail, and bridal treatments.

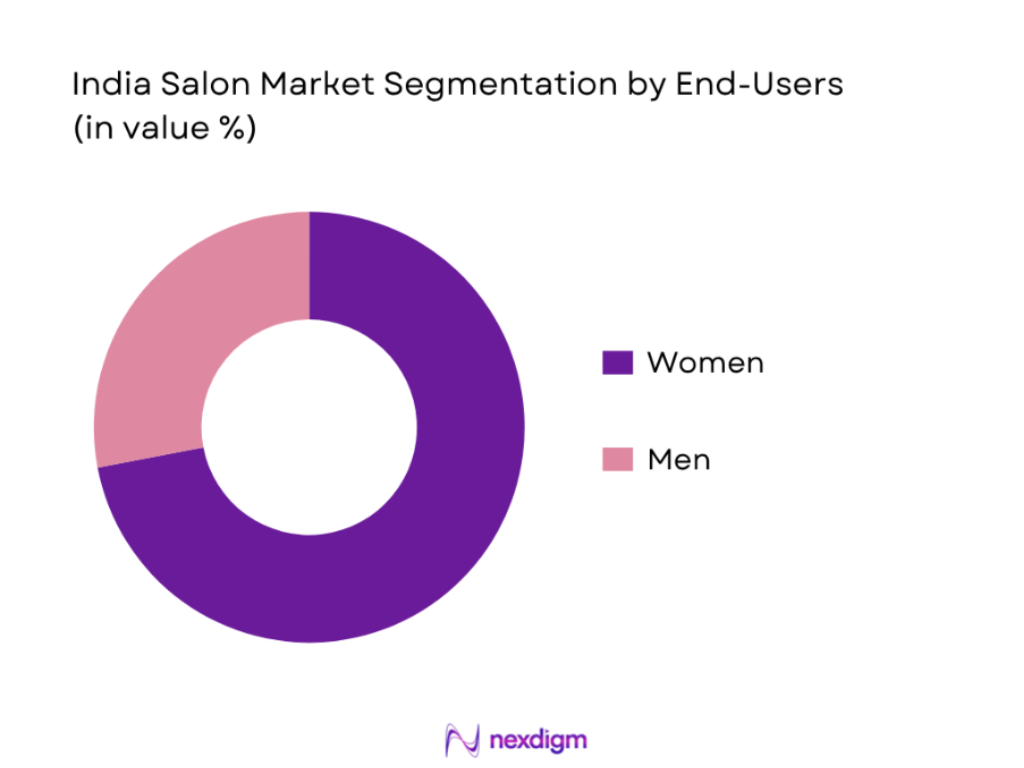

By End User

India salon market is segmented by end user into women and men. Recently, the women segment has held the dominant market share in India under this segmentation due to its broader service basket and higher ticket depth. Female consumers typically account for stronger demand across facials, hair colour, advanced treatments, manicure-pedicure, bridal makeup, and festive packages, whereas male visits are still more concentrated around haircutting, beard grooming, and selected skin treatments. Public market commentary for salon services shows the female segment accounting for more than 72% of spending, while India-focused salon studies also identify women as the clear leading user group. The dominance is reinforced by wedding-related consumption, routine grooming cycles, and the higher relevance of premium and specialty beauty categories among women in chain-led urban markets.

Competitive Landscape

The India salon market is still fragmented overall, but the organized end is increasingly shaped by a set of strong chain-led operators such as Naturals, Lakmé Salon, Green Trends, Enrich, and Looks Salon. Their influence comes from outlet network scale, franchising strength, training infrastructure, service standardization, digital booking capability, and deeper penetration into premium urban as well as emerging Tier 2 and Tier 3 catchments. The competitive center of gravity is shifting from standalone neighbourhood salons toward branded networks that can deliver repeatable service quality, stronger memberships, and higher customer trust.

| Company | Establishment Year | Headquarters | Public Network Scale | Geographic Presence | Business Model | Service Strength | Training / Academy Capability | Consumer Positioning |

| Naturals Salon | 2000 | Chennai | – | – | – | – | – | – |

| Lakmé Salon | 1952* | Mumbai | – | – | – | – | – | – |

| Green Trends | 2002 | Chennai | – | – | – | – | – | – |

| Enrich | 1997 | Mumbai | – | – | – | – | – | – |

| Looks Salon | 1989 | New Delhi | – | – | – | – | – | – |

India Salon Market Analysis

Growth Drivers

Increasing Shift Toward Organized Salon Chains

India’s move toward organized salon chains is being supported by stronger household spending capacity, faster formalization, and visible network expansion by branded operators. The World Bank places India’s GDP at USD 3.91 trillion in 2024, with GDP per capita at USD 2,694.74 and real GDP growth at 6.5. On the consumer side, MOSPI’s Household Consumption Expenditure Survey shows urban monthly per-capita consumption expenditure at ₹6,996, of which ₹4,220 is non-food spending, indicating room for discretionary beauty and grooming services. Formalization is also improving: gross GST collections reached ₹22.08 lakh crore in 2024-25, while the taxpayer base rose to over 1.5 crore by early 2026. At the operator level, Naturals reports 800+ locations, Green Trends 375+ salons in 50+ cities, and Enrich 100+ locations. This combination of higher discretionary spend, a stronger tax-compliant ecosystem, and visible chain scaling is pushing consumers toward branded formats that offer standardized hygiene, trained staff, digital booking, and repeatable service quality.

Expansion of Franchise-Based Salon Networks

Franchise-led growth is becoming central to India salon market expansion because the macro backdrop now supports faster rollout of branded service businesses across urban India. The World Bank notes that India’s urban economy already contributes nearly 70 of GDP and that the country is moving toward 600 million urban residents by 2036, creating a wider customer base for chain-led personal care services. Formal small-business creation is also being encouraged by policy: the Union Budget 2025-26 raised the MSME classification threshold for micro enterprises to ₹2.5 crore of investment and ₹10 crore of turnover, while the credit guarantee cover for micro and small enterprises was increased from ₹5 crore to ₹10 crore. The Ministry of MSME also reported 84,034 new micro enterprises assisted during 2025-26 up to mid-December, generating employment for more than 6.7 lakh people. For salon chains, these changes matter because franchising depends on local entrepreneurs, accessible credit, and micro-enterprise viability. As organized brands standardize fit-outs, service menus, training, and procurement, franchise-based salon expansion becomes easier to replicate city by city.

Market Challenges

High Dependence on Skilled Workforce

The India salon market remains highly dependent on skilled labour because service quality is produced in real time by trained stylists, beauty therapists, colorists, and nail technicians rather than by standardized products alone. NSDC’s official curricula show that a Hair Stylist requires 390 training hours, an Assistant Hair Stylist 340 hours, a Beauty Therapist 390 hours, and a Pedicurist and Manicurist 290 hours. NSDC also lists a Senior Colourist role at NSQF Level 5, underscoring the advanced skill requirements of premium services. While the Beauty & Wellness Sector Skill Council has trained and certified more than 13 lakh youth, organized chains are scaling quickly, with Naturals at 800+ locations, Green Trends at 375+, and Enrich at 100+. That expansion multiplies demand for job-ready staff across every new outlet. The market challenge is not just finding people; it is finding people who can deliver chain-standard consultation, chemistry-led treatments, hygiene protocols, and upselling. In a service business, any skill shortage shows up immediately in customer experience.

Service Standardization Issues Across Chain Networks

Standardization remains a key challenge because salon chains expand faster than the availability of uniformly trained personnel and monitored execution systems. Public operator data show network scale rising across India, with Naturals at 800+ locations, Green Trends at 375+ salons in 50+ cities, and Enrich at 100+ locations. Yet the skill architecture needed to standardize every chair is detailed and role-specific: NSDC assigns 390 hours to Hair Stylist, 390 hours to Beauty Therapist, 340 hours to Assistant Hair Stylist, and 290 hours to Pedicurist and Manicurist. Chains must replicate these capabilities not once, but hundreds of times across formats, cities, and franchisees. This becomes harder as brands move beyond metros into new labour pools. The issue is especially relevant in the organized salon market because premium chains are judged on whether haircut finishing, hair colour processing, hygiene, consultation, and product recommendation feel the same across outlets. Rapid network growth is therefore positive for scale, but it also raises the operational burden of keeping the brand experience consistent outlet to outlet.

Opportunities

Organized Chain Penetration in Untapped Cities

A major market opportunity lies in expanding organized salon chains deeper into untapped urban clusters, because India’s current macro and digital indicators already support wider salon formalization. The World Bank notes that India is moving toward 600 million urban residents by 2036, while urban areas already account for nearly 70 of GDP. TRAI reported 954.40 million internet subscribers in 2024, including 398.35 million rural and 556.05 million urban users, and the government reported 4.74 lakh 5G towers covering 99.6 of districts. This means beauty discovery, appointment coordination, reviews, and digital payment are now possible well beyond the largest metros. On the entrepreneurship side, the revised MSME framework allows a micro enterprise to operate up to ₹2.5 crore investment and ₹10 crore turnover, while 84,034 new micro enterprises were assisted in 2025-26 up to mid-December. For salon chains, this creates a future-ready white space: smaller cities now offer a growing urban consumer base, adequate connectivity, and a more supportive local franchise ecosystem than they did a few years ago.

Premiumization and High-Ticket Services

Premiumization is one of the clearest opportunities in the India salon market because present-day income, consumption, and skills data already favor more specialized service baskets. MOSPI’s HCES places urban monthly per-capita consumption expenditure at ₹6,996, with urban non-food spending at ₹4,220; with imputed welfare items included, urban MPCE rises to ₹7,078. The World Bank places India’s GDP per capita at USD 2,694.74 in 2024, supporting a broader shift toward discretionary service consumption. On the capability side, premium salon services are skill-intensive: NSDC lists 390 hours for Hair Stylist, 390 hours for Beauty Therapist, 290 hours for Pedicurist and Manicurist, and a distinct Senior Colourist role at NSQF Level 5. Public salon platforms also show the market architecture for premiumization already exists through categories such as scalp therapies, hair repair, advanced colour, skin systems, bridal packages, and product-backed rituals. This is why premiumization is not just a pricing story; it is a capability-led opportunity for chains that can combine trained talent, branded protocols, and higher-value service menus.

Future Outlook

India salon market is expected to remain on a strong long-term growth path as grooming shifts further from occasion-led spending to habitual consumption. Organized chains are likely to gain faster than the broader market because they combine stronger branding, franchise scalability, standardized service delivery, loyalty programs, and better unit economics. Premium hair treatments, advanced skin services, nail bars, and membership-led recurring revenue will keep expanding, while Tier 2 and Tier 3 cities should become the next major growth frontier for organized operators.

Major Players

- Naturals Salon

- Lakmé Salon

- Jawed Habib Hair & Beauty

- Green Trends

- Enrich

- Looks Salon

- Geetanjali Salon

- TONI&GUY India

- BBLUNT Salon

- Bodycraft

- STUDIO11 Salon & Spa

- YLG Salon

- Limelite Salon & Spa

- Affinity Salon

- Strands Salon

Key Target Audience

- Salon Chain Operators and Franchise Networks

- Professional Beauty and Haircare Product Manufacturers

- Retail and Consumer Brand Investors

- Investments and Venture Capitalist Firms

- Mall Developers and Commercial Real Estate Owners

- Beauty-Tech, Booking, CRM, and SaaS Platform Providers

- Government and Regulatory Bodies

- Beauty and Wellness Skill Development Bodies (Beauty & Wellness Sector Skill Council)

Research Methodology

Step 1: Identification of Key Variables

The first stage mapped the full India salon ecosystem, covering organized chains, franchise operators, independent salons, professional product suppliers, beauty academies, and end users. Secondary research was conducted using company websites, industry portals, open market trackers, and public business sources to identify the variables most critical to revenue generation, including outlet count, service mix, pricing ladder, visit frequency, city presence, and organized-chain penetration.

Step 2: Market Analysis and Construction

In this phase, historical market values and current public benchmarks were compiled to build a structured view of the India salon market. The analysis combined topline market size sources with bottom-up market logic around service categories, consumer groups, and the visible growth of branded salon chains. Particular attention was paid to hair-led service economics, women-led demand, and the expansion of organized salons into Tier 2 and Tier 3 markets.

Step 3: Hypothesis Validation and Expert Consultation

The initial hypotheses were stress-tested against operator disclosures and open industry commentary from salon brands and sector-focused sources. This included validating which segments dominate, which cities anchor organized consumption, and which chain attributes matter most in the Indian context, such as franchising, training, service standardization, and repeat customer monetization.

Step 4: Research Synthesis and Final Output

In the final stage, the findings were synthesized into a market-focused narrative tailored for business professionals. The output was organized to highlight current market size, long-range growth direction, segmentation logic, chain-led competition, target buyers of the report, and the structural factors likely to influence market expansion over the medium to long term. The result is a commercially usable view of India salon market dynamics rather than a generic beauty-industry summary.

- Executive Summary

- Research Methodology (Salon Industry Definition, Organized vs Unorganized Mapping, Chain Penetration Analysis, Outlet-Level Revenue Modeling, Service Mix Assessment, Franchise Network Validation, Consumer Behavior Mapping, Market Sizing & Forecasting Approach)

- Definition and Scope

- Evolution of India’s Salon Industry (Unorganized to Organized Shift)

- Industry Structure (Chain Salons vs Independent Salons Contribution)

- Business Models Across the Market (Independent, Chain, Franchise-Led)

- Value Chain Analysis (Product Suppliers → Salon Chains → End Consumers)

- Rise of Organized Salon Chains and Brand Standardization

- Franchise-Driven Expansion Model in Salon Chains

- Role of Training Academies and Skill Standardization in Chains

- Consumer Shift Toward Branded Salon Experiences

- Technology Integration (CRM, Booking, Membership Systems)

- Regional Expansion Strategy of Leading Salon Chains

- Investment and Scalability of Salon Chains

- Key Success Factors in the India Salon Market

- Growth Drivers

Increasing Shift Toward Organized Salon Chains

Expansion of Franchise-Based Salon Networks

Rising Demand for Premium Hair Treatments

Growth in Men’s Grooming Segment

Increasing Urban Disposable Income and Grooming Spend

Social Media Influence and Beauty Trends

Expansion into Tier 2 and Tier 3 Cities - Market Challenges

High Dependence on Skilled Workforce

Service Standardization Issues Across Chain Networks

High Rental and Operational Costs

Competition from Independent Local Salons

Pricing Pressure and Discounting Strategies

Talent Retention in Organized Chains - Opportunities

Organized Chain Penetration in Untapped Cities

Premiumization and High-Ticket Services

Specialized Chains (Men’s Grooming, Nail Bars)

Product Retailing Through Salon Chains

Digital CRM and Membership Programs

Training Academies as Growth Enablers - Trends

Increasing Market Share of Organized Salon Chains

Membership and Subscription-Based Revenue Models

Experience-Led Premium Salon Formats

Hair Treatment-Led Revenue Growth

Omnichannel Customer Journey

Brand-Led Consumer Loyalty - Franchise Economics and Expansion Analysis (Capex, Payback Period, Revenue per Outlet, EBITDA Margins, Breakeven Timeline, Royalty Structure, Expansion ROI)

- Salon Chain Unit Economics (Revenue per Chair, Revenue per Stylist, Average Ticket Size, Utilization Rate, Service Mix Contribution, Peak vs Off-Peak Revenue)

- Talent and Training Ecosystem (Stylist Productivity, Training Programs, Certification, Attrition Rates, Academy Infrastructure)

- Pricing and Revenue Model Analysis (Service Pricing, Membership Revenue, Package Sales, Upselling Efficiency, Discounting Impact)

- Regulatory Landscape (Trade Licensing, GST, Hygiene Compliance, Labour Regulations, Safety Norms)

- Porter’s Five Forces Analysis

- SWOT Analysis

- By Value, 2020-2025

- By Number of Salon Outlets, 2020-2025

- By Organized vs Unorganized Share, 2020-2025

- By Chain vs Independent Salon Revenue Contribution, 2020-2025

- By Average Revenue per Outlet, 2020-2025

- By Average Ticket Size, 2020-2025

- By Salon Format (In Value %)

Economy / Value Salons

Mid-Market Unisex Salons

Premium Salons

Luxury Salons

Express / Quick Service Salons - By Consumer Focus (In Value %)

Women-Centric Salons

Men’s Grooming Salons

Unisex Salons

Family Salons

Specialized Beauty Studios - By Service Category (In Value %)

Haircut, Wash, and Styling

Hair Color and Chemical Treatments

Skin and Facial Services

Nail and Beauty Services

Bridal and Occasion Services

Membership and Package Services - By Business Model (In Value %)

Independent Salons

Regional Chains

National Organized Chains

Franchise-Owned Franchise-Operated (FOFO)

Company-Owned / Hybrid Models - By Price Positioning (In Value %)

Mass / Affordable

Mid-Priced

Premium

Luxury

Celebrity / Stylist-Led - By City Tier (In Value %)

Metro Cities

Tier 1 Cities

Tier 2 Cities

Tier 3 Cities

Emerging Urban Clusters - By Region (In Value %)

North India

South India

West India

East India

Central India - By Booking and Customer Acquisition Mode (In Value %)

Walk-In

Appointment-Based

Brand App / Website

Aggregator Platforms

Membership / Subscription-Based

- Market Share of Major Players (By Revenue, Outlet Count, Organized Segment Share, Franchise Network Size)

- Cross Comparison Parameters (Number of Outlets, City Presence, Franchise Network Strength, Service Portfolio Depth, Average Pricing, Membership Penetration, Training Academy Strength, Brand Positioning)

- Competitive Positioning Map

- Pricing Benchmarking Analysis

- Franchise Expansion Strategy Comparison

- Digital Capability Benchmarking

- Detailed Profiles of Major Companies

Naturals Salon

Lakmé Salon

Jawed Habib Hair & Beauty

Green Trends Salon

Enrich

Looks Salon

Geetanjali Salon

TONI&GUY India

BBLUNT Salon

Bodycraft

STUDIO11 Salon & Spa

YLG Salon

Limelite Salon & Spa

Affinity Salon

Strands Salon

- Consumer Preference for Chain vs Independent Salons

- Visit Frequency and Service Consumption Patterns

- Average Spend per Visit

- Membership and Package Adoption

- Key Decision Drivers (Brand, Price, Location, Stylist Expertise)

- Customer Retention in Salon Chains

- Pain Points in Salon Experience

- Digital Booking and Engagement Behavior

- By Value, 2026-2032

- By Outlet Count, 2026-2032

- By Organized vs Unorganized Share, 2026-2032

- By Chain vs Independent Contribution, 2026-2032

- By Average Ticket Size, 2026-2032

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now