Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the India Semiconductor Manufacturing Market is valued at approximately USD 34 Billion supported by increasing demand for integrated circuits across electronics, automotive, telecommunications, and industrial automation sectors. Government initiatives such as semiconductor incentive programs and fabrication subsidies are encouraging domestic manufacturing capabilities. Rising demand for smartphones, consumer electronics, and data center infrastructure further accelerates semiconductor production. Expanding investments in wafer fabrication plants, semiconductor assembly, and packaging facilities also contribute significantly to market expansion.

Major semiconductor manufacturing activities are concentrated in regions such as Gujarat, Karnataka, and Tamil Nadu due to strong industrial infrastructure, technology parks, and favorable policy incentives. Cities including Bengaluru, Chennai, and Ahmedabad serve as semiconductor technology hubs hosting electronics manufacturing clusters and research institutions. Collaboration between international semiconductor companies and domestic technology firms strengthens manufacturing capabilities. Access to skilled engineering talent, advanced manufacturing facilities, and supportive government initiatives positions these regions as central nodes for semiconductor production.

Market Segmentation

By Product Type

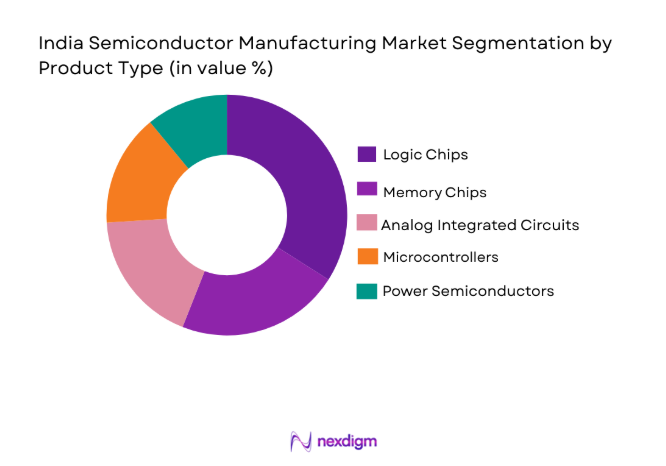

India Semiconductor Manufacturing Market is segmented by product type into Logic Chips, Memory Chips, Analog Integrated Circuits, Microcontrollers, and Power Semiconductors. Recently, Logic Chips has a dominant market share due to factors such as strong demand from consumer electronics, smartphones, computing devices, and telecommunications infrastructure. Increasing deployment of artificial intelligence processors, data center chips, and advanced computing hardware further strengthens demand for logic semiconductor fabrication. Domestic electronics manufacturing growth and increasing semiconductor design activities also reinforce demand for logic integrated circuits.

By Platform Type

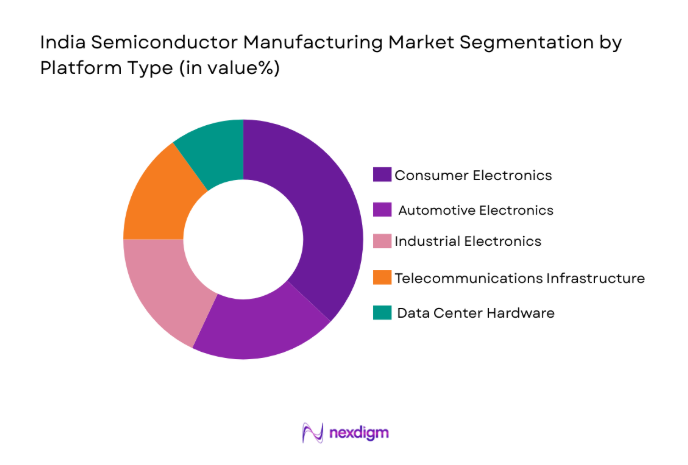

India Semiconductor Manufacturing Market is segmented by platform type into Consumer Electronics, Automotive Electronics, Industrial Electronics, Telecommunications Infrastructure, and Data Center Hardware. Recently, Consumer Electronics has a dominant market share due to factors such as high demand for smartphones, laptops, wearable devices, and home appliances requiring integrated circuits. Rapid expansion of electronics manufacturing services within India supports large scale semiconductor consumption for assembly and product manufacturing. Growing domestic demand for smart devices and connected consumer technologies also contributes to the dominance of consumer electronics platforms.

Competitive Landscape

The India Semiconductor Manufacturing Market features a mix of domestic semiconductor firms, multinational technology companies, and global chip manufacturers establishing partnerships with Indian electronics manufacturers. Industry competition is shaped by technological capability, wafer fabrication capacity, advanced packaging technologies, and semiconductor design expertise. Large global semiconductor companies maintain strong influence through technology licensing, supply chain partnerships, and investment in fabrication facilities. Increasing government incentives and strategic alliances encourage international players to expand manufacturing presence within the Indian semiconductor ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fabrication Capability |

| Intel Corporation | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | USA | ~ | ~ | ~ | ~ | ~ |

| Micron Technology | 1978 | USA | ~ | ~ | ~ | ~ | ~ |

| Tata Electronics | 2020 | India | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

India Semiconductor Manufacturing Market Analysis

Growth Drivers

Growth of Electronics Manufacturing Ecosystem and Device Production Demand

The rapid expansion of India’s electronics manufacturing ecosystem significantly drives demand for semiconductor manufacturing across multiple industrial sectors. Large scale smartphone production facilities located across Indian electronics manufacturing clusters require steady supplies of integrated circuits, memory chips, and power management semiconductors. Consumer electronics manufacturers increasingly localize component supply chains to reduce dependency on imported semiconductor components. Government initiatives encouraging domestic electronics manufacturing also stimulate semiconductor demand through production linked incentive programs supporting electronics device assembly. The rapid expansion of data center infrastructure and cloud computing platforms increases demand for processors and high performance semiconductor chips required for computational workloads. Automotive electronics systems integrated into electric vehicles and advanced driver assistance systems further increase semiconductor consumption within the domestic manufacturing ecosystem. Industrial automation systems including robotics, sensors, and control equipment also require sophisticated semiconductor devices supporting digital manufacturing technologies. As electronics manufacturing capacity continues expanding across India, semiconductor manufacturing demand correspondingly increases across the entire technology supply chain.

Government Semiconductor Incentive Programs and Strategic Technology Investments

Government policy initiatives supporting semiconductor fabrication development significantly accelerate market growth by encouraging domestic manufacturing capabilities and foreign investment partnerships. National semiconductor incentive programs provide financial subsidies, infrastructure support, and tax benefits designed to attract global semiconductor fabrication companies to establish production facilities. Large scale semiconductor manufacturing projects including wafer fabrication plants and advanced packaging facilities strengthen domestic semiconductor supply chain capabilities. Strategic collaborations between global semiconductor companies and Indian technology firms facilitate knowledge transfer and technology adoption across the semiconductor ecosystem. Government investments in semiconductor research centers and technology parks promote innovation in chip design, materials engineering, and fabrication technologies. Semiconductor manufacturing also receives policy support due to its strategic importance for national electronics security and technology independence. Increasing public sector investment in advanced electronics manufacturing clusters improves infrastructure required for semiconductor fabrication including power supply, water availability, and clean room manufacturing environments. These coordinated policy measures create favorable investment conditions that significantly stimulate semiconductor manufacturing expansion across India.

Market Challenges

High Capital Investment Requirements for Semiconductor Fabrication Facilities

Semiconductor fabrication facilities require extremely high capital investment levels due to the complexity of advanced wafer manufacturing technologies and clean room production environments. Establishing semiconductor fabrication plants involves large financial commitments for lithography equipment, wafer processing machinery, advanced metrology systems, and specialized clean room infrastructure. Semiconductor manufacturing equipment supplied by global technology companies often involves high procurement costs and long installation timelines. Operating semiconductor fabrication facilities also requires continuous investment in process technology upgrades to maintain competitiveness with global semiconductor manufacturing standards. The requirement for highly reliable power supply, water purification systems, and contamination free manufacturing environments further increases operational infrastructure costs. Semiconductor manufacturers must also maintain large research and development budgets to improve chip designs and manufacturing efficiency. These financial barriers limit entry of smaller companies into semiconductor fabrication activities within the Indian market. As a result, semiconductor manufacturing remains concentrated among large technology firms capable of sustaining high investment cycles required for advanced chip fabrication.

Dependence on Global Semiconductor Supply Chains and Technology Imports

India’s semiconductor manufacturing ecosystem continues to depend heavily on global semiconductor technology providers and imported manufacturing equipment. Advanced semiconductor fabrication processes require specialized lithography systems, wafer processing tools, and semiconductor materials sourced primarily from global technology suppliers. Domestic semiconductor companies often rely on international technology licensing agreements and equipment imports to operate fabrication facilities. This dependence increases supply chain vulnerability during global semiconductor shortages or geopolitical trade disruptions affecting technology transfers. Semiconductor manufacturing also requires highly specialized materials including high purity silicon wafers, photoresists, and advanced semiconductor chemicals which are largely imported from international suppliers. Limited domestic manufacturing capability for semiconductor equipment further increases reliance on foreign technology ecosystems. Any disruption in global semiconductor supply chains can significantly affect production schedules within domestic fabrication facilities. Strengthening local semiconductor equipment manufacturing capabilities remains a key challenge that must be addressed to reduce dependence on international semiconductor supply networks.

Opportunities

Development of Advanced Semiconductor Fabrication Clusters and Industrial Technology Parks

Establishment of semiconductor manufacturing clusters across industrial technology parks presents a major opportunity for expanding domestic semiconductor fabrication capacity. Dedicated semiconductor industrial zones equipped with advanced infrastructure such as uninterrupted power supply, high purity water systems, and logistics connectivity create favorable conditions for semiconductor manufacturing operations. Technology parks designed specifically for semiconductor fabrication can support wafer manufacturing facilities, semiconductor packaging units, and integrated circuit design companies within the same ecosystem. These clusters enable collaboration between semiconductor manufacturers, equipment suppliers, materials providers, and technology research institutions. Concentrated semiconductor ecosystems also improve supply chain efficiency by reducing transportation time for critical semiconductor materials and equipment components. Governments and private investors increasingly support development of semiconductor clusters through infrastructure investments and policy incentives. Such integrated industrial ecosystems can accelerate semiconductor manufacturing capabilities while attracting foreign semiconductor companies seeking strategic production locations. As semiconductor industrial clusters expand, India’s semiconductor manufacturing ecosystem gains significant long term growth potential.

Expansion of Automotive Electronics and Electric Vehicle Semiconductor Demand

The rapid growth of automotive electronics and electric vehicle technologies creates strong opportunities for semiconductor manufacturing within India’s automotive industry supply chain. Electric vehicles require large numbers of semiconductor components including power semiconductors, microcontrollers, battery management chips, and advanced sensor integrated circuits. Automotive safety systems such as advanced driver assistance systems also rely heavily on semiconductor processors and sensing technologies. Increasing production of electric vehicles by domestic automobile manufacturers stimulates demand for locally produced automotive grade semiconductors. Semiconductor manufacturers can benefit from supplying specialized automotive chips supporting vehicle electrification and autonomous driving technologies. Automotive semiconductor demand also extends to onboard infotainment systems, connectivity modules, and digital control units integrated into modern vehicles. As India continues expanding its electric vehicle manufacturing ecosystem, semiconductor companies have opportunities to establish dedicated production capabilities serving automotive electronics manufacturers. This growing automotive semiconductor demand creates strong potential for long term expansion within the domestic semiconductor manufacturing sector.

Future Outlook

The India Semiconductor Manufacturing Market is expected to experience strong expansion driven by growing electronics production, increasing demand for advanced computing chips, and expansion of semiconductor fabrication infrastructure. Government incentive programs supporting semiconductor fabrication plants and technology development are expected to accelerate domestic manufacturing capacity. Growing demand for electric vehicles, artificial intelligence processors, and data center hardware will further increase semiconductor consumption. Strategic collaborations between international semiconductor companies and domestic electronics manufacturers are likely to strengthen technology capabilities across the semiconductor ecosystem.

Major Players

- Intel Corporation

- Samsung Electronics

- Texas Instruments

- Micron Technology

- Tata Electronics

- Tower Semiconductor

- NXP Semiconductors

- Qualcomm

- Broadcom

- GlobalFoundries

- SK Hynix

- Infineon Technologies

- STMicroelectronics

- Renesas Electronics

- Applied Materials

Key Target Audience

- Semiconductor Manufacturing Companies

- Electronics Manufacturing Companies

- Automotive Electronics Manufacturers

- Government and Regulatory Bodies

- Investments and Venture Capitalist Firms

- Semiconductor Equipment Suppliers

- Data Center Infrastructure Companies

Research Methodology

Step 1: Identification of Key Variables

The research begins with identification of core variables affecting semiconductor manufacturing including wafer fabrication capacity, electronics manufacturing demand, semiconductor technology development, and policy incentives. Industry reports, government semiconductor initiatives, and technology manufacturing data are analyzed to establish baseline market parameters.

Step 2: Market Analysis and Construction

Comprehensive analysis of semiconductor manufacturing infrastructure, fabrication capacity expansion projects, electronics manufacturing clusters, and technology investment trends is conducted. Supply chain analysis and technology ecosystem evaluation are used to construct a structured representation of the semiconductor manufacturing market.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions and analytical frameworks are validated through consultations with semiconductor industry experts, electronics manufacturers, and technology supply chain participants. Cross verification with publicly available industry data and regulatory policy frameworks ensures accuracy of market interpretation.

Step 4: Research Synthesis and Final Output

All validated datasets and analytical findings are consolidated into a structured research report providing market insights, competitive landscape analysis, segmentation breakdown, and future outlook for the India Semiconductor Manufacturing Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Incentives and Production Linked Incentive Programs Supporting Domestic Semiconductor Fabrication

Rapid Growth in Consumer Electronics and Smartphone Manufacturing Demand

Increasing Demand for Automotive and Industrial Semiconductor Components - Market Challenges

High Capital Investment Requirements for Semiconductor Fabrication Facilities

Dependence on Imported Semiconductor Manufacturing Equipment and Raw Materials

Limited Domestic Expertise in Advanced Semiconductor Process Technologies - Market Opportunities

Expansion of Government Supported Semiconductor Manufacturing Clusters and Technology Parks

Strategic Partnerships Between Global Semiconductor Companies and Indian Manufacturing Firms

Growing Demand for Semiconductor Chips in Electric Vehicles and Industrial Automation - Trends

Development of Advanced Semiconductor Packaging and Testing Capabilities

Expansion of Semiconductor Design Ecosystems Supporting Local Manufacturing - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Systems

Semiconductor Assembly and Packaging Systems

Testing and Quality Assurance Systems

Semiconductor Manufacturing Equipment

Semiconductor Materials Processing Systems - By Platform Type (In Value%)

Integrated Device Manufacturing Facilities

Pure Play Foundry Facilities

Outsourced Semiconductor Assembly and Test Facilities

Fabless Design Supported Manufacturing Platforms

Government Supported Semiconductor Manufacturing Clusters - By Fitment Type (In Value%)

New Greenfield Fabrication Facilities

Expansion of Existing Manufacturing Facilities

Technology Upgrade Installations

Contract Manufacturing Integration - By End User Segment (In Value%)

Consumer Electronics Manufacturers

Automotive Electronics Manufacturers

Industrial Electronics and Automation Companies

- Market Share Analysis

- Cross Comparison Parameters (Fabrication Technology Node, Production Capacity, Manufacturing Process Technology, Product Portfolio Diversity, Strategic Partnerships, Geographic Manufacturing Presence, R&D Investment)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intel Corporation

Taiwan Semiconductor Manufacturing Company

Samsung Electronics

GlobalFoundries

Micron Technology

Texas Instruments

STMicroelectronics

NXP Semiconductors

Infineon Technologies

Applied Materials

Lam Research

ASML Holding

Tower Semiconductor

Powerchip Semiconductor Manufacturing Corporation

Vedanta Semiconductors

- Electronics Manufacturing Companies Increasing Local Semiconductor Sourcing to Strengthen Supply Chains

- Automotive Manufacturers Integrating Advanced Semiconductor Chips for Electric Vehicles and Autonomous Systems

- Industrial Automation Companies Deploying Semiconductor Based Control Systems and Sensors

- Telecommunications Equipment Manufacturers Expanding Demand for Semiconductor Components in 5G Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now