Download PDF

Download PDFMarket Overview

The India Ship Management, Chandling & Marine Logistics Market was valued at USD ~ billion in 2024 and is projected to expand at a CAGR of ~% during the 2026–2035 forecast period. According to data published by the Directorate General of Shipping (DGS), the Ministry of Ports, Shipping and Waterways (MoPSW), and the Indian Ports Association (IPA), India’s maritime sector handles over 95 percent of the country’s trade volume by weight and approximately 70 percent by value, making it one of the most critical enablers of the Indian economy. India’s 12 major ports and over 200 non-major ports collectively handled cargo exceeding 1,500 million metric tonnes in recent reporting periods, generating significant demand for ship management, chandling, port agency, bunker supply, crew manning, and marine freight logistics services. Growth is supported by the Government of India’s Sagarmala Programme, which is driving port-led development and maritime logistics modernisation across the country’s 7,517-kilometre coastline, combined with India’s growing international shipping trade volumes, an expanding Indian-flagged fleet, and the country’s position as one of the world’s largest suppliers of trained maritime officers and ratings to the global shipping industry.

Market Segmentation

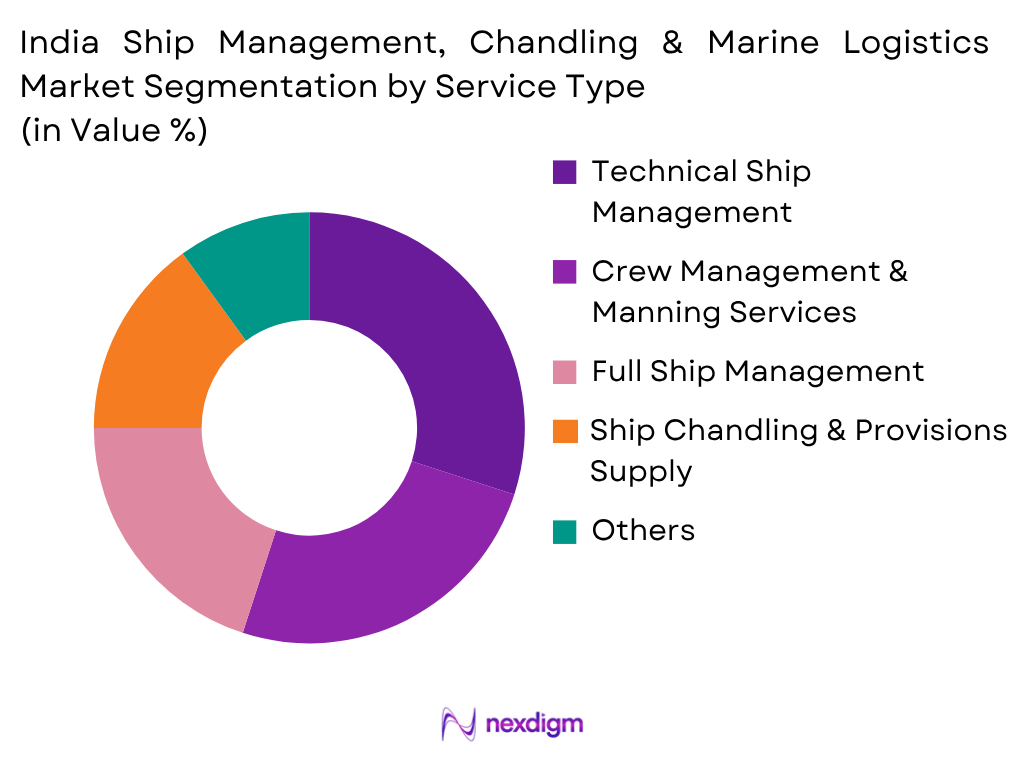

By Service Type

Technical ship management represents the largest service segment within the India Ship Management, Chandling & Marine Logistics Market, driven by the sustained global demand for cost-effective, high-quality vessel technical operations management from India-based ship management companies that leverage the country’s deep maritime expertise and cost-competitive service proposition. India-headquartered or India-presence offices of leading global ship management companies including Synergy Marine Group, Anglo-Eastern, Fleet Management, Bernhard Schulte Shipmanagement (BSM), and V.Ships manage a significant portion of the global merchant fleet from their Mumbai-based operations centres, providing technical superintendence, planned maintenance system oversight, dry-docking management, and regulatory compliance services to ship owners across Asia, Europe, and the Middle East. Mumbai serves as the pre-eminent hub for India’s ship management industry, hosting the regional or global operations of most major third-party ship managers due to its established maritime professional ecosystem, proximity to major Indian port clusters at JNPA and Mumbai Port, and deep talent pool of experienced marine superintendents and officers. Ship chandling, covering the supply of provisions, deck stores, engine spares, bonded stores, and safety equipment to vessels calling at Indian ports, represents a complementary high-frequency revenue segment with strong recurring demand driven by the large number of vessel port calls across India’s major and non-major ports. Continuous investments in digital ship management platforms, predictive maintenance technology, seafarer welfare programmes, and integrated maritime logistics capabilities have further strengthened India’s competitive positioning as a globally preferred ship management and maritime services destination.

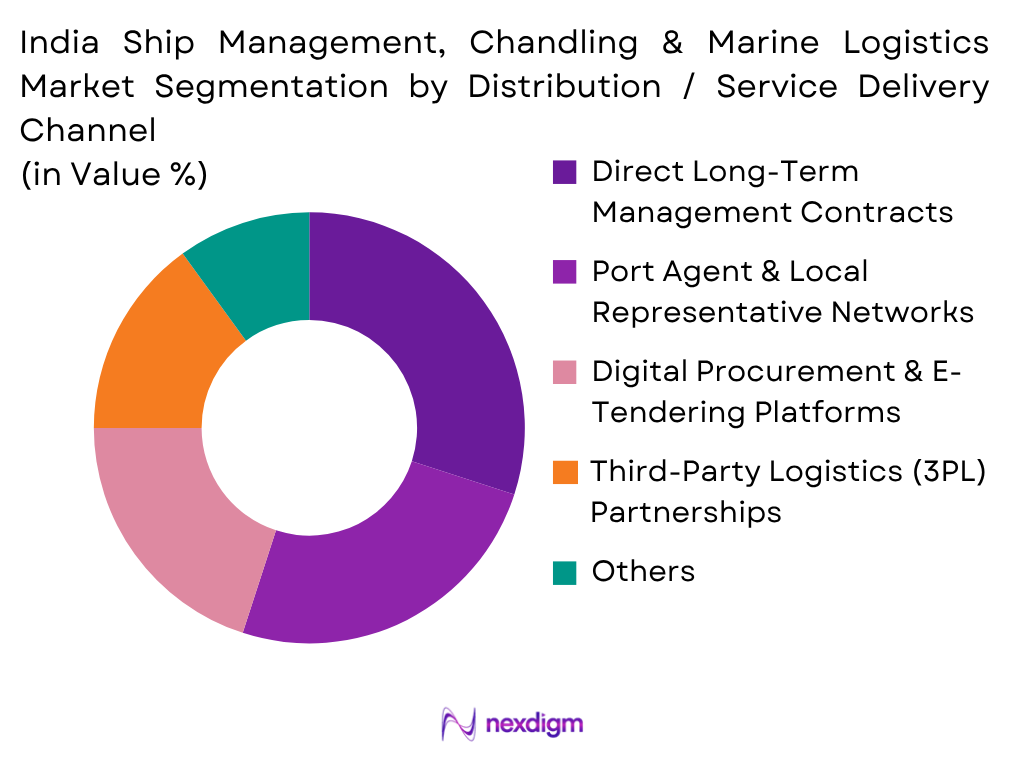

By Distribution / Service Delivery Channel

Direct long-term management contracts represent the dominant service delivery model in the India Ship Management, Chandling & Marine Logistics Market, as ship owners and operators typically engage third-party ship management companies through multi-year technical, crew, or full management agreements that provide operational continuity, regulatory compliance assurance, and cost predictability across their managed fleets. Leading ship management companies including Anglo-Eastern, Synergy Marine Group, and BSM India maintain long-term contractual relationships with international and domestic ship owners, often managing fleets of dozens to hundreds of vessels under comprehensive ISM-compliant management agreements. Port agent and local representative networks serve as the primary delivery channel for chandling, port agency, and marine logistics services, as vessels calling at Indian ports require licensed port agents to coordinate berth bookings, customs documentation, crew changes, provisions delivery, bunker arrangements, and ship repair coordination on behalf of ship owners and operators. The network depth of a port agent or ship chandler across India’s major port clusters, including Mumbai, JNPA, Kandla, Chennai, Kochi, Visakhapatnam, Kolkata, and Haldia, is a critical competitive differentiator determining service capability and client retention. Digital procurement and e-tendering platforms are increasingly being adopted by large shipping companies and PSU clients including the Shipping Corporation of India, Oil India Limited, and ONGC for competitive procurement of chandling and logistics services. Government and PSU tender procurement through platforms such as GeM (Government e-Marketplace) and centralised procurement committees represents a significant and growing segment for marine logistics and chandling contracts covering government-owned or operated vessels.

Competitive Landscape

The India Ship Management, Chandling & Marine Logistics Market is characterised by a mix of large multinational ship management companies with India-based operations, established domestic shipping and logistics conglomerates, specialist chandling and port agency firms, and an extensive network of regional port agents and marine service providers across India’s major and non-major port clusters. Multinational third-party ship managers including Synergy Marine Group, Anglo-Eastern, Fleet Management, BSM, V.Ships, Columbia Shipmanagement, and Wilhelmsen leverage global fleet management platforms, international certification frameworks, and established owner relationships to operate large-scale ship management operations from India. Domestic companies including the Shipping Corporation of India, Seven Islands Shipping, Transworld Group, and Seahorse Ship Agencies compete through deep local port knowledge, government relationships, regulatory compliance expertise, and price-competitive service delivery. Competition in chandling and port agency services is intense at individual port level, with local specialist firms often outcompeting larger multinational players on responsiveness, local vendor relationships, and cost in specific port clusters.

| Company | Establishment Year | Headquarters | Primary Service Focus | Port Presence

|

Fleet Under Management | Technology Platforms | Certifications & Standards | Value-Added Services |

| Synergy Marine Group India | 1994 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Anglo-Eastern Ship Management India | 1974 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Fleet Management India | 1993 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Shipping Corporation of India (SCI) | 1961 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Univan Ship Management India | 1977 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

India Ship Management, Chandling and Marine Logistics Market Analysis

Growth Drivers

Sagarmala Programme Port Modernisation and Rising India-Linked Trade Volumes

The Government of India’s Sagarmala Programme, overseen by the Ministry of Ports, Shipping and Waterways (MoPSW), continues to be one of the primary structural growth drivers for the India Ship Management, Chandling & Marine Logistics Market by transforming port infrastructure, enabling coastal shipping, and generating sustained growth in maritime trade volumes that directly expand demand for marine services. According to the Ministry of Ports, Shipping and Waterways, the Sagarmala Programme encompasses over 800 projects across port modernisation, port-led industrialisation, coastal community development, and inland waterways development, with a total investment outlay exceeding INR 5.5 lakh crore over its implementation period. India’s major ports collectively handled record cargo volumes in recent years, with JNPA (Jawaharlal Nehru Port Authority) remaining South Asia’s largest container port and Deendayal Port (Kandla) the country’s highest-volume port by total cargo tonnage. The World Bank estimated India’s GDP at approximately USD 3.7 trillion in 2024 and projected sustained growth making India the world’s third-largest economy by 2030, a trajectory that will substantially expand India’s import-export trade flows and correspondingly increase vessel traffic, port calls, and maritime service demand at Indian ports. The International Monetary Fund (IMF) similarly projected India as the fastest-growing major economy globally through the forecast period, supporting rising containerised trade, bulk commodity imports including coal, crude oil, LNG, and fertilisers, and export growth across automobiles, pharmaceuticals, engineering goods, and agricultural products. These trade volume trends directly translate into growing demand for ship chandling, port agency, freight forwarding, bunker supply, and marine logistics services at Indian ports, creating a sustained and expanding revenue base for maritime service providers operating across India’s port network.

India as a Global Maritime Manning Hub and Growing Seafarer Workforce

India’s position as one of the world’s largest suppliers of trained maritime officers and ratings to the global merchant fleet continues to be a significant structural growth driver for the crew management and manning services segment of the India Ship Management, Chandling & Marine Logistics Market. According to the Directorate General of Shipping (DGS), India supplies approximately 240,000 seafarers to the global merchant fleet, making it the second-largest source of officers worldwide, behind only the Philippines. Indian maritime officers are widely recognised for their English proficiency, technical competence, and compliance with STCW (Standards of Training, Certification and Watchkeeping) requirements, making them preferred crew for international ship owners across Europe, the Middle East, and Asia. The DGS-approved network of maritime training institutes, including the Training Ship Rahaman in Mumbai and numerous STCW-certified maritime academies across Mumbai, Chennai, Kolkata, Kochi, and Visakhapatnam, produces a continuous supply of qualified deck officers, marine engineers, electro-technical officers, and ratings for the global fleet. India-headquartered ship management companies including Anglo-Eastern, Synergy Marine Group, and BSM India leverage this abundant seafarer supply base to offer cost-competitive crew management services to international ship owners, covering crew recruitment, STCW certification management, contract administration, travel logistics, payroll, and flag state documentation. The growing global fleet, combined with increasing regulatory requirements for crew welfare, mental health support, shore leave facilitation, and digital crew communication, is expanding the scope and value of crew management services delivered from India, positioning the country’s ship management sector for continued growth in crew-related service revenue through 2035.

Market Challenges

Dominance of Foreign Ship Managers and Limited Indian-Flagged Tonnage

The India Ship Management, Chandling & Marine Logistics Market continues to face a structural challenge arising from the limited size of the Indian-flagged merchant fleet relative to India’s trade volumes and the dominant presence of foreign-headquartered ship management companies in the third-party management segment. According to the Directorate General of Shipping (DGS), the Indian-flagged fleet comprises approximately 1,400 to 1,500 vessels, a relatively modest fleet size compared to India’s status as the world’s seventh-largest trade nation by volume, reflecting the long-standing preference of Indian cargo owners and charterers for foreign-flagged vessels operating under more cost-competitive flag state regimes. The Ministry of Ports, Shipping and Waterways has acknowledged this gap through various policy interventions, including cabotage policy reforms enabling greater flexibility for foreign-flagged vessels in coastal trade, but the fundamental challenge of building a larger nationally-flagged fleet remains a multi-decade structural objective. While India-headquartered offices of global ship management companies such as Synergy Marine Group, Anglo-Eastern, and Fleet Management manage large international fleets from Mumbai, the majority of management fees and commercial revenues are ultimately accounted for at their global headquarters in Cyprus, Hong Kong, or Singapore, limiting the direct economic value captured within India’s domestic maritime services market. Strengthening the Indian-flagged fleet through fiscal incentives, preferential cargo reservation policies, and tonage tax reforms under the Merchant Shipping Act remains a critical policy lever for expanding the addressable domestic market for Indian ship management companies and associated marine service providers.

Port Infrastructure Gaps, Cabotage Constraints and Regulatory Complexity

Despite significant Sagarmala Programme investments, persistent infrastructure gaps at secondary and non-major ports, cabotage policy limitations, and the complexity of India’s multi-agency maritime regulatory framework continue to create operational challenges for ship management, chandling, and marine logistics service providers across the country. According to the Indian Ports Association (IPA), a significant portion of India’s over 200 non-major ports under state government jurisdiction lack adequate draft depth, modern cargo handling equipment, reliable shore power, vessel traffic management systems, and cold chain or bonded warehouse facilities, restricting the types and sizes of vessels that can be economically served by chandlers and logistics providers at these locations. The Directorate General of Shipping (DGS), Customs, Port Health Organisation (PHO), Immigration, and the Central Industrial Security Force (CISF) represent multiple regulatory authorities whose overlapping jurisdictions and documentation requirements contribute to vessel turnaround time delays, crew change procedural complexity, and chandling coordination challenges at Indian ports. India’s cabotage policy, which historically restricted foreign-flagged vessels from carrying cargo between Indian ports, has been partially liberalised but continues to limit the full development of coastal shipping as a cost-competitive alternative to road and rail freight, constraining the addressable market for coastal vessel services and chandling. High bunker price volatility, driven by global crude oil price movements and the transition to VLSFO and LNG under IMO 2020 regulations, creates margin pressure for bunker traders and ship managers providing fuel management services. Streamlining inter-agency coordination at Indian ports, accelerating the development of non-major port infrastructure, and further liberalising cabotage policy are essential steps toward realising the full growth potential of India’s marine logistics and chandling market.

Market Opportunities

Coastal Shipping Expansion, LNG Bunkering Infrastructure and Green Ship Management

The progressive development of India’s coastal shipping network, combined with the emerging LNG bunkering infrastructure opportunity and the global transition toward green and decarbonised shipping, presents substantial growth opportunities for the India Ship Management, Chandling & Marine Logistics Market over the forecast period. According to the Ministry of Ports, Shipping and Waterways (MoPSW), coastal shipping currently accounts for only a fraction of India’s total freight movement, representing significant untapped potential given India’s 7,517-kilometre coastline and the significant cost and carbon efficiency advantages of sea freight over road and rail transport for certain cargo categories. The Sagarmala Programme’s coastal shipping development component aims to shift a meaningful proportion of freight from road and rail to coastal sea routes, requiring investment in Roll-on Roll-off (RoRo) terminals, coastal berths, feeder vessels, and integrated intermodal logistics infrastructure that will expand the addressable chandling, port agency, and marine logistics market at secondary coastal ports. The Government of India’s LNG policy and the MoPSW’s plan to develop LNG bunkering facilities at major ports, including JNPA, Kochi, Mangaluru, and Paradip, in alignment with IMO 2050 decarbonisation targets, creates a new and growing revenue stream for LNG bunker suppliers, fuel management specialists, and green shipping consultants. Ship management companies that invest in LNG-compatible fleet management capabilities, EEXI and CII compliance advisory services, environmental performance monitoring platforms, and ESG reporting frameworks will be well positioned to capture the premium associated with green ship management mandates as Indian and international ship owners progressively align their fleets with IMO decarbonisation requirements through 2035.

Digital Ship Management Platforms, Smart Port Integration and Offshore Logistics Growth

The accelerating digitalisation of ship management operations, the development of smart port infrastructure across Indian major ports, and the expanding offshore oil and gas logistics market present significant technology-driven and sector-specific growth opportunities for the India Ship Management, Chandling & Marine Logistics Market. According to the Ministry of Electronics and Information Technology (MeitY) and the MoPSW, India’s port digitalisation agenda encompasses vessel traffic management system (VTMS) modernisation, Port Community System (PCS 1x) upgrades, single-window cargo clearance platforms, and smart container tracking across major ports, creating demand for integrated digital logistics services, maritime data analytics, and port-ship communication technology from marine logistics providers and ship agents. Leading global ship management companies including Wilhelmsen, Columbia Shipmanagement, and V.Ships are deploying proprietary digital platforms for planned maintenance management, performance monitoring, voyage optimisation, fuel efficiency tracking, and regulatory compliance management, which are increasingly being adopted and developed from their India-based operations teams. India’s offshore oil and gas production activities in the Krishna-Godavari basin, the Mumbai High field, and exploration blocks in the Mahanadi and Andaman basins generate consistent demand for offshore support vessel (OSV) management, marine logistics coordination, crew transfer services, and supply base operations, creating a specialised and recurring revenue segment for marine logistics companies with offshore service capabilities. Companies investing in integrated digital ship management platforms, offshore logistics infrastructure, smart port connectivity solutions, and sustainability reporting tools will be well positioned to capture premium service contracts and expand their addressable market as India’s maritime sector continues to modernise through 2035.

Future Outlook

The India Ship Management, Chandling & Marine Logistics Market is expected to witness sustained growth throughout the forecast period, supported by India’s rising maritime trade volumes, continued Sagarmala Programme port infrastructure investment, the country’s growing role as a global maritime manning hub, expanding coastal shipping activity, and the accelerating digital transformation of ship management and marine logistics operations. Increasing adoption of green shipping standards, LNG bunkering infrastructure development, and IMO decarbonisation compliance requirements are expected to create new premium service segments for technically capable ship managers and logistics providers. Growing offshore oil and gas activity, defence vessel support demand, cruise vessel chandling, and ship recycling logistics present additional sector-specific growth opportunities. Continued investments in digital platforms, seafarer welfare programmes, smart port integration, and value-added marine logistics capabilities will further strengthen the long-term competitive positioning of India-based ship management and marine service companies through 2035.

Major Players

- Synergy Marine Group India

- Anglo-Eastern Ship Management India

- Fleet Management India

- Shipping Corporation of India (SCI)

- Univan Ship Management India

- Bernhard Schulte Shipmanagement (BSM) India

- V.Ships India

- Columbia Shipmanagement India

- Wilhelmsen Ship Management India

- Inchcape Shipping Services India

- Mach1 Global Services

- Seven Islands Shipping

- Seahorse Ship Agencies

- Transworld Group (Marine Division)

- Peterson India (Offshore Marine Logistics)

Key Target Audience

- Third-Party Ship Management Companies

- Ship Chandlers and Provisions Suppliers

- Port Agents and Shipping Agents

- Bunker Traders and Fuel Management Companies

- Marine Freight Forwarders and Customs Brokers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Directorate General of Shipping (DGS), Ministry of Ports, Shipping and Waterways (MoPSW), Indian Ports Association (IPA), Shipping Corporation of India (SCI), Inland Waterways Authority of India (IWAI), Major Port Authorities)

- Ship Repair Yards and Dry-Dock Operators

- Maritime Training Institutes and Seafarer Certification Bodies

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the major stakeholders across the India Ship Management, Chandling & Marine Logistics value chain, including ship management companies, chandlers, port agents, bunker suppliers, freight forwarders, ship owners, port authorities, regulatory agencies, and maritime training institutions. Extensive secondary research is conducted using DGS publications, MoPSW reports, Indian Ports Association data, maritime trade publications, company annual reports, and proprietary maritime databases to establish the key variables influencing market performance.

Step 2: Market Analysis and Construction

Historical market information is compiled and evaluated to estimate overall market size, service revenue by category, port call volumes, fleet under management data, chandling expenditure per port call, and bunker supply volumes across major Indian port clusters. Both demand-side (vessel traffic, trade volumes, fleet composition, offshore activity) and supply-side (service provider capacity, port infrastructure, seafarer supply, chandling network depth) indicators are analysed using bottom-up and top-down approaches to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates and assumptions are validated through Computer Assisted Telephone Interviews (CATIs) and structured discussions with ship management executives, chandling company operators, port agents, bunker traders, shipping company procurement managers, port authority officials, and maritime industry association representatives. These consultations provide critical commercial insights into service pricing, contract structures, client preferences, port-level competitive dynamics, and emerging technology adoption trends.

Step 4: Research Synthesis and Final Output

The final stage integrates primary research findings with secondary data to develop a comprehensive market assessment covering service segments, vessel categories, port clusters, client profiles, competitive landscape, and future opportunities. Multiple validation techniques including cross-verification with DGS fleet registry data, port throughput statistics, and maritime trade association reports are employed to ensure the consistency and credibility of the final market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Sagarmala Programme Port Modernisation, Rising India-Linked Shipping Trade Volumes, Expanding Indian-Flagged Fleet, Growing Seafarer Workforce and Manning Services Demand, Oil & Gas Offshore Logistics Growth, Increasing Port Connectivity and Coastal Shipping, Digital Transformation in Ship Management, Expanding Ship Repair and Dry-Docking Capacity)

- Market Challenges (Dominance of Foreign Ship Management Companies, Limited Indian Tonnage Under National Flag, Inadequate Port Infrastructure at Secondary Ports, Cabotage Policy Limitations, Skilled Seafarer Retention, Regulatory Complexity Across DG Shipping, Customs and Port Health Frameworks, High Bunker Price Volatility, Cybersecurity Risks in Digital Ship Management)

- Market Opportunities (Coastal Shipping and Inland Waterways Expansion, LNG Bunkering Infrastructure Development, Green Shipping and Alternative Fuel Management, Cruise and Passenger Vessel Chandling, Defence Vessel Logistics and Chandling, Smart Port and Digital Logistics Platforms, Ship Recycling and End-of-Life Vessel Services, Export of Manning and Crew Management Services)

- Market Trends (Digitalisation of Ship Management Operations, Remote Vessel Monitoring and Predictive Maintenance, IMO 2020 and EEXI/CII Compliance-Driven Service Demand, ESG Reporting and Green Fleet Management, Integrated Maritime Logistics Platforms, IoT-Enabled Chandling and Provisions Tracking, Crew Welfare Technology Adoption, Just-In-Time Port Arrival Coordination)

- Government Regulations and Policies (Directorate General of Shipping (DGS) Regulations, Merchant Shipping Act 1958 and Amendments, Cabotage Policy Reforms, Sagarmala Programme Framework, Major Port Authorities Act 2021, Customs Act and EXIM Documentation, MARPOL Compliance Framework, IMO STCW Standards for Seafarer Certification)

- Port Infrastructure and Capacity Analysis (Major Port Throughput, Non-Major Port Development, Draft Limitations, Container and Bulk Terminal Capacity, Berth Availability, Port Turnaround Time)

- Fleet and Trade Volume Analysis (India-Flagged Fleet Composition, Vessels Calling at Indian Ports, Import-Export Trade Volume Growth, Coastal Shipping Volume Trends)

- Seafarer and Manning Market Analysis (Indian Seafarer Supply, STCW Certification Levels, Officer vs Rating Composition, Global Demand for Indian Seafarers, Training Institute Capacity)

- Bunker Market Analysis (Bunker Fuel Availability at Indian Ports, HFO vs VLSFO vs LNG Pricing, Bunkering Infrastructure Gap Analysis)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Fleet and Port Call Volume (2020-2025)

- By Average Service Contract Value (2020-2025)

- By Service Type (In Value %)

Technical Ship Management

Crew Management & Manning Services

Full Ship Management (Technical + Crew + Commercial)

Ship Chandling & Provisions Supply

Marine Logistics & Port Agency Services

Freight Forwarding & Customs Clearance

Bunker Supply & Fuel Management

Ship Repair Coordination & Dry-Docking Services - By Vessel Type Served (In Value %)

Bulk Carriers

Tankers (Crude, Product & Chemical)

Container Vessels

General Cargo & Multi-Purpose Vessels

Offshore Support Vessels (OSVs)

LNG & LPG Carriers

Passenger & Cruise Vessels

Naval & Government Vessels - By Client Type (In Value %)

Ship Owners & Shipping Companies

Charterers & Trading Companies

Oil & Gas Companies

Port Authorities & Terminal Operators

Government & Public Sector Shipping

Defence & Coast Guard - By Distribution / Service Delivery Channel (In Value %)

Direct Long-Term Management Contracts

Port Agent & Local Representative Networks

Digital Procurement & E-Tendering Platforms

Third-Party Logistics (3PL) Partnerships

Government & PSU Tender Procurement

Spot & Voyage-Based Service Contracts

- By Region / Major Port Cluster (In Value %)

Mumbai & JNPA (Nhava Sheva) Cluster

Chennai & Ennore (Kamarajar Port) Cluster

Kandla (Deendayal Port) & Gujarat Cluster

Kolkata & Haldia Cluster

Kochi & Mangaluru Cluster

Visakhapatnam & East Coast Cluster

- Market Share Analysis (By Value, Service Type, Vessel Category, Port Cluster, Client Segment)

- Cross Comparison Parameters (Fleet Under Management Size, Number of Active Port Representations, Chandling Network Depth Across Indian Ports, Crew Manning Volume, Digital Platform Maturity, ISM and ISO Certification Coverage, Bunker Supply Capability, Ship Repair and Dry-Dock Coordination Capability)

- SWOT Analysis of Major Players

- Pricing Analysis (By Service Type, Contract Duration, Vessel Type, Fleet Size, Scope of Services)

- Detailed Profiles of Major Companies

Synergy Marine Group India

Anglo-Eastern Ship Management India

Fleet Management India

Shipping Corporation of India (SCI)

Univan Ship Management India

Bernhard Schulte Shipmanagement (BSM) India

V.Ships India

Columbia Shipmanagement India

Wilhelmsen Ship Management India

Inchcape Shipping Services India

Mach1 Global Services

Seven Islands Shipping

Seahorse Ship Agencies

Transworld Group (Marine Division)

Peterson India (Offshore Marine Logistics)

- Procurement Pattern Analysis (Long-Term Management Contract Preference, Spot vs Retainer Procurement, Tender vs Negotiated Contracts, Multi-Service vs Specialist Provider Preference)

- End-User Demand Analysis (Ship Owner Requirements, Charterer Service Needs, PSU Shipping Demand, Government & Coast Guard Logistics Requirements)

- Budget and Expenditure Analysis by Vessel Type and Client Segment

- Full-Service vs Specialist Provider Preference Analysis

- Brand, Certification and ISM Compliance Preference Analysis

- After-Sales Support and 24×7 Operations Centre Preference

- Service Attribute Preference Analysis (Response Time, ISM/ISO Certification, Port Network Depth, Crew Quality, Digital Reporting, Cost Transparency, Regulatory Compliance Track Record)

- Technology Adoption Behaviour in Ship Management

- Online vs Traditional Service Procurement Behaviour

- Client Pain Point Analysis

- Contract Renewal and Switching Behaviour

- By Market Value (2026-2035)

- By Fleet and Port Call Volume (2026-2035)

- By Average Service Contract Value (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now