Download PDF

Download PDFMarket Overview

The India shipbuilding market was valued at USD ~ billion in 2024 and is projected to expand at a CAGR of ~% during the 2026–2032 forecast period. According to data published by the Ministry of Ports, Shipping and Waterways and the Directorate General of Shipping, India currently operates more than 30 shipbuilding yards of varying sizes and capabilities along its approximately 7,500-kilometre coastline, with the sector spanning naval defence shipbuilding, commercial vessel construction, offshore vessel fabrication, inland waterways vessel manufacturing, and ship repair and conversion. India’s shipbuilding industry is anchored by a cluster of large government-owned defence shipyards including Mazagon Dock Shipbuilders, Cochin Shipyard, Garden Reach Shipbuilders and Engineers, Goa Shipyard, and Hindustan Shipyard, alongside a growing private sector ecosystem. Data from the Indian Register of Shipping and the Society of Indian Shipbuilders indicates that domestic order books have grown significantly in recent years, driven by a large and accelerating naval vessel construction pipeline under the Indian Navy’s fleet expansion program, expanding coast guard procurement, and new vessel orders under the Sagarmala Programme and the Jal Marg Vikas inland waterways project. Growth is further supported by the government’s Shipbuilding Financial Assistance Policy, the Aatmanirbhar Bharat defence manufacturing mandate, rising domestic steel supply, and emerging interest from foreign naval and commercial customers in Indian shipbuilding capabilities.

Market Segmentation

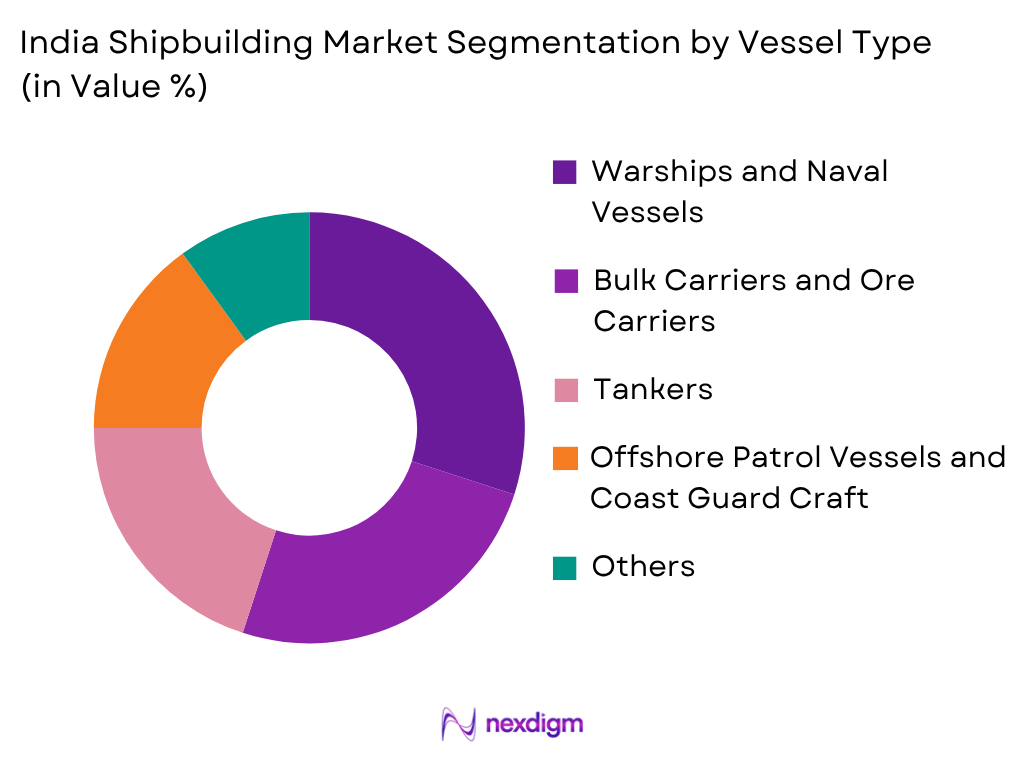

By Vessel Type

Warships and naval vessels dominate the India shipbuilding market by value, reflecting the Indian Navy’s position as the largest and most consistent customer of the domestic shipbuilding industry, with a sustained and expanding procurement program covering destroyers, frigates, corvettes, submarines, offshore patrol vessels, landing ships, and auxiliary vessels. The Indian Navy’s Maritime Capability Perspective Plan envisions a long-term fleet expansion toward a force structure exceeding 175 ships and submarines, requiring a continuous pipeline of new vessel construction orders placed predominantly at domestic shipyards under the Aatmanirbhar Bharat defence self-reliance mandate. Mazagon Dock Shipbuilders in Mumbai remains the primary builder of destroyers, frigates, and conventional submarines for the Indian Navy, while Garden Reach Shipbuilders and Engineers in Kolkata specialises in anti-submarine warfare corvettes and offshore patrol vessels. Cochin Shipyard in Kerala constructed India’s first domestically built aircraft carrier, INS Vikrant, commissioned in 2022, marking a transformational milestone for the industry. Goa Shipyard and Hindustan Shipyard contribute offshore patrol vessels, survey ships, and auxiliary craft. The naval segment commands the highest revenue per vessel across all categories given the complexity, technology content, weapons system integration, and extended construction timelines involved. Continuous investments in advanced stealth hull design, combat management systems integration, submarine propulsion technologies, and naval grade steel fabrication capabilities further reinforce the dominance of the naval segment within India’s total shipbuilding market revenue.

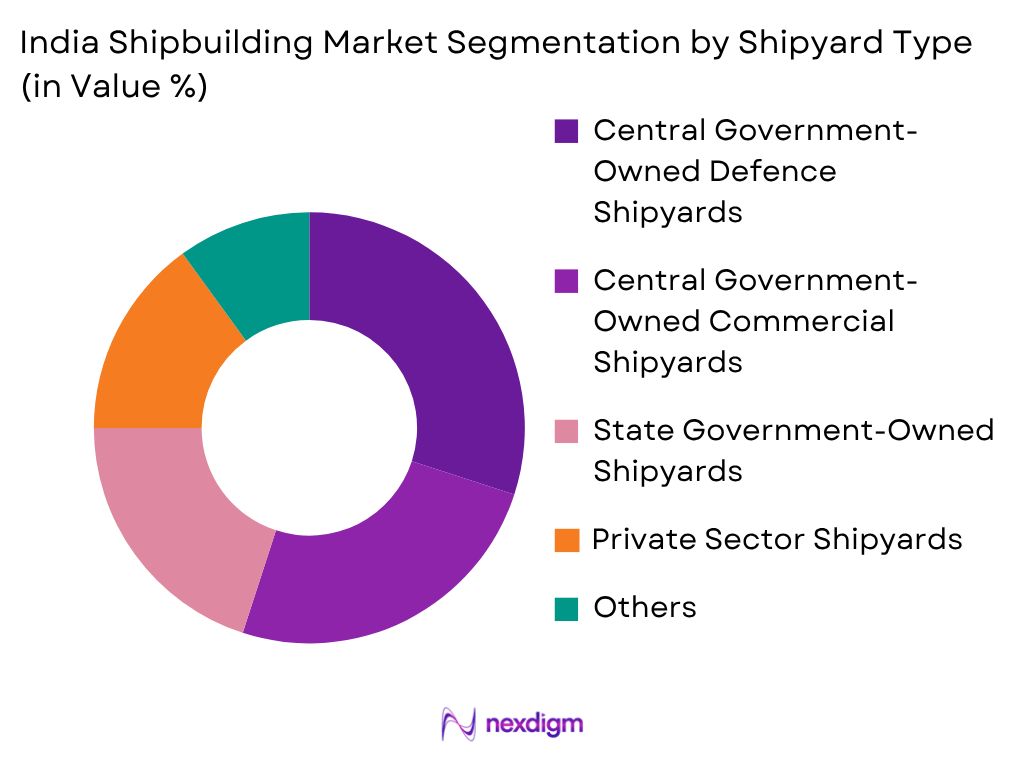

By Shipyard Type

Central government-owned defence shipyards account for the largest share of the India shipbuilding market by value, reflecting their exclusive access to classified naval construction contracts, their established technological capabilities in complex warship construction, and their privileged position within the Ministry of Defence’s vendor qualification framework. Mazagon Dock Shipbuilders, Garden Reach Shipbuilders and Engineers, Goa Shipyard, Hindustan Shipyard, and Cochin Shipyard collectively form the backbone of India’s defence shipbuilding capability and hold the majority of the active naval order book by contract value. These yards benefit from long-term sovereign procurement relationships, government-backed capital expenditure programs for infrastructure expansion, and access to defence-grade classification and quality assurance frameworks. However, the private sector is gaining ground in commercial and offshore vessel construction, with companies including L&T Shipbuilding, Bharati Defence and Infrastructure, and Chowgule and Company developing capabilities in bulk carriers, offshore support vessels, dredgers, and inland waterways craft. The government’s policy of encouraging private sector shipyard development through the Shipbuilding Financial Assistance Policy, which provides production-linked financial subsidies to eligible yards, is progressively improving the competitiveness of private yards relative to lower-cost foreign competitors, particularly for smaller commercial vessel categories where Indian yards can be cost competitive with Chinese and Vietnamese builders.

Competitive Landscape

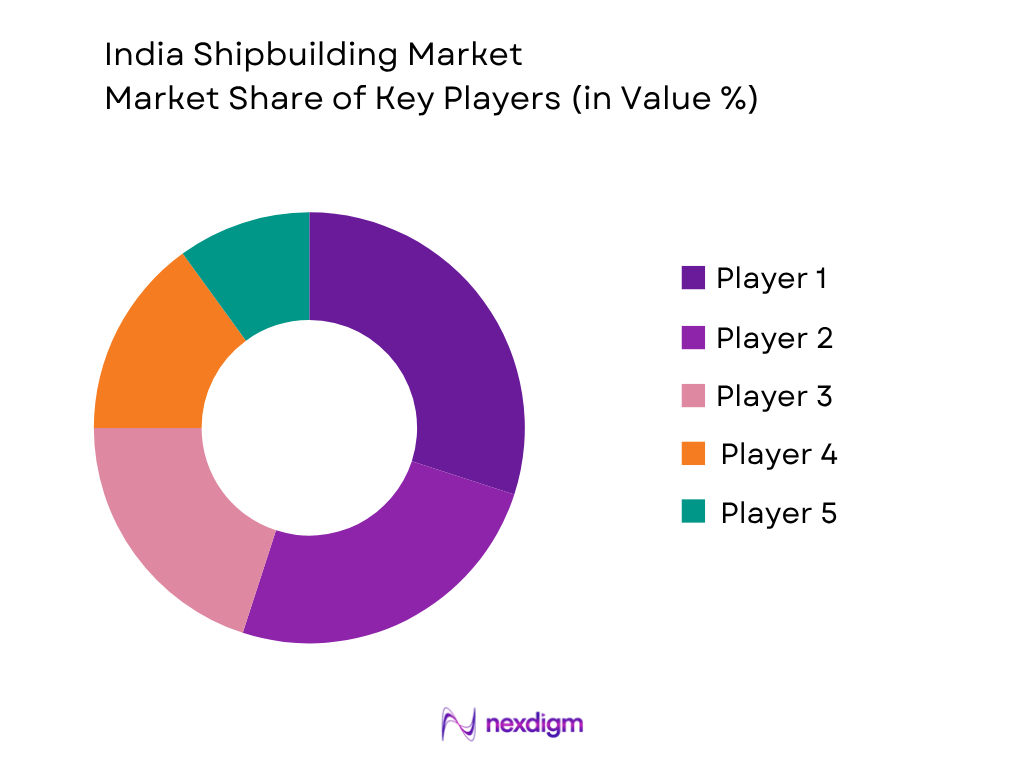

The India shipbuilding market is moderately concentrated in the defence segment, dominated by a small number of large government-owned yards with exclusive access to naval construction contracts, while the commercial and offshore segments are more fragmented with a larger number of private and smaller state-owned yards competing for vessel orders. Mazagon Dock Shipbuilders and Garden Reach Shipbuilders together account for the majority of active naval construction by value, while Cochin Shipyard occupies a unique position as the builder of India’s first indigenously constructed aircraft carrier and has expanded into commercial vessel construction and ship repair. In the commercial and private segment, L&T Shipbuilding, Bharati Defence and Infrastructure, and Drydocks World India compete alongside smaller regional yards. International classification societies including Bureau Veritas, Lloyd’s Register, and DNV maintain strong positions as quality assurance and vessel certification partners to Indian shipyards across both naval and commercial programs.

| Company | Establishment Year | Headquarters | Primary Build Focus | Dry Dock Capacity

|

Naval Order Book | Commercial Orders | Sustainability Programs | Key Vessel Portfolio |

| Cochin Shipyard Limited (CSL) | 1972 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Mazagon Dock Shipbuilders (MDL) | 1774 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Garden Reach Shipbuilders (GRSE) | 1884 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Goa Shipyard Limited (GSL) | 1957 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| L&T Shipbuilding | 2011 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

India Shipbuilding Market Analysis

Growth Drivers

Indian Navy Fleet Expansion and Aatmanirbhar Bharat Defence Mandate

The Indian Navy’s sustained and accelerating fleet expansion program, underpinned by the government’s Aatmanirbhar Bharat defence self-reliance mandate, represents the single largest and most structurally significant growth driver for the India shipbuilding market over the forecast period. The Indian Navy’s Maritime Capability Perspective Plan articulates a long-term objective of expanding the fleet toward a force structure exceeding 175 ships and submarines, from a current inventory of approximately 130 commissioned vessels, requiring the continuous construction and delivery of new destroyers, frigates, conventional and nuclear submarines, offshore patrol vessels, mine countermeasure vessels, landing platform docks, survey ships, and replenishment vessels across multiple simultaneous shipyard programs. The Ministry of Defence has placed Indigenous Design and Construction at the apex of its vessel procurement hierarchy through the Defence Acquisition Procedure 2020, mandating that the overwhelming majority of naval vessel orders be placed at domestic shipyards and that platform designs originate from Indian defence research establishments, including the Warship Design Bureau of the Indian Navy and the Defence Research and Development Organisation. Active programs currently under construction or under contract at Indian yards include the P-17A Stealth Frigate program at Mazagon Dock and GRSE, the P-75 Scorpene submarine fleet at Mazagon Dock, the Next Generation Destroyer program, a second Indigenous Aircraft Carrier, the NGOPV offshore patrol vessel program, and numerous survey and auxiliary vessel orders across Cochin, Hindustan, and Goa Shipyards. The aggregate contract value of active and planned naval shipbuilding programs across Indian yards is estimated in the tens of billions of USD over the coming decade, providing the domestic shipbuilding industry with the most substantial and visible revenue pipeline in its post-independence history and creating cascading demand for domestic steel, marine equipment, combat systems, propulsion technologies, and specialised skilled labour.

Shipbuilding Financial Assistance Policy and Commercial Order Incentivisation

The Government of India’s Shipbuilding Financial Assistance Policy (SBFAP), administered by the Ministry of Ports, Shipping and Waterways, provides a critical demand-side and supply-side stimulus for the growth of commercial and offshore vessel construction at Indian yards. The policy provides financial assistance to Indian shipyards at a specified percentage of the contract price for vessels constructed and delivered from eligible domestic yards, with the objective of bridging the estimated 20 to 30 percent cost competitiveness gap between Indian shipyards and lower-cost competitors in China, Vietnam, and Bangladesh for comparable commercial vessel types. The policy also provides purchase preference advantages to Indian-flag shipowners procuring domestically built vessels, encouraging domestic shipping companies to order tonnage from Indian shipyards rather than sourcing ready-built vessels from foreign yards at lower acquisition costs. The Ministry of Ports, Shipping and Waterways has indicated that the revised SBFAP framework targets significantly increased disbursements to eligible shipyards over the policy period, creating a sustained financial incentive that is expected to improve the attractiveness of Indian yards for commercial vessel orders in categories including bulk carriers, product tankers, offshore support vessels, dredgers, and coastal cargo vessels. The policy’s financial support, combined with rising domestic steel availability from producers including SAIL and JSW Steel, improving shipyard infrastructure at both government and private yards, and a growing domestic order base from the Sagarmala Programme and inland waterways expansion, is expected to progressively expand India’s commercial shipbuilding market share from its current sub-one-percent of global tonnage toward a more meaningful contribution over the forecast period. Government support for cluster development around major shipyards and the creation of dedicated maritime industrial zones adjacent to key yards will further reduce input logistics costs and attract marine equipment sub-suppliers.

Market Challenges

Global Competitiveness Gap and Dominance of China, South Korea and Japan

The most structurally entrenched challenge facing the India shipbuilding industry is the profound competitiveness gap between domestic yards and the globally dominant shipbuilding nations of China, South Korea, and Japan, which together account for more than 90 percent of global commercial vessel construction by compensated gross tonnage. Chinese shipyards, supported by substantial state financing, government-directed steel pricing, vast economies of scale at mega-yards such as CSSC and CSIC, and decades of accumulated construction efficiency, can deliver standard commercial vessel categories including bulk carriers, product tankers, and container vessels at prices estimated to be 20 to 35 percent below comparable quotations from Indian yards, after accounting for the Shipbuilding Financial Assistance Policy subsidy. South Korean yards including Hyundai Heavy Industries, Samsung Heavy Industries, and Daewoo Shipbuilding and Marine Engineering dominate the high-value LNG carrier, large container vessel, and complex offshore construction segments that offer the highest revenue and margin per unit, segments where Indian yards currently lack the technical capability, experience base, and precision fabrication infrastructure to compete effectively. Indian shipyards face additional structural disadvantages including higher domestic financing costs relative to export credit facilities available to Korean and Japanese buyers of foreign-built ships, longer construction cycle times reflecting lower levels of production automation and block assembly standardisation, limited domestic availability of high-quality marine propulsion systems and specialised equipment requiring import at additional cost and lead time, and a smaller pool of experienced shipbuilding engineers and naval architects relative to the large skilled workforces maintained by major East Asian yards. Bridging this competitiveness gap in the commercial segment requires sustained, multi-decade investment in shipyard infrastructure, workforce development, production technology, domestic equipment manufacturing, and competitive financing frameworks that extend beyond the current policy support horizon.

Dry Dock Capacity Constraints and Infrastructure Limitations

India’s existing dry dock and shipyard infrastructure presents a significant bottleneck to rapid expansion of domestic shipbuilding capacity across both the naval and commercial segments. The total number and size distribution of operational dry docks at Indian shipyards currently limits the maximum vessel dimensions that can be constructed domestically, with only a small number of facilities capable of accommodating large commercial vessels exceeding 50,000 deadweight tonnes or naval vessels of destroyer and aircraft carrier class. Cochin Shipyard’s new dry dock, commissioned to support the construction of INS Vikrant, represents the largest dry dock in India and one of the largest in South Asia, but the overall inventory of large-capacity dry docks across the country remains limited relative to the scale of vessel construction programs being contemplated under naval and commercial expansion plans. Construction of new large dry docks is a capital-intensive, technically complex, and time-consuming undertaking, typically requiring investment of several hundred crore rupees per facility and construction timelines of several years before operational commissioning. Several government-owned yards including Hindustan Shipyard in Vizag are in various stages of dry dock expansion and modernisation, but timelines for completion and commissioning have historically experienced delays attributable to funding constraints, procurement procedures, and civil construction challenges. Private sector investment in new dry dock capacity has been limited by uncertain commercial order books, high capital costs, and access to long-term project financing at competitive rates. These capacity constraints mean that even if commercial demand and policy incentives generate increased vessel orders at Indian yards, the physical infrastructure required to execute multiple simultaneous large-vessel construction contracts may not be immediately available, creating a potential supply-side bottleneck that constrains market growth in the near to medium term.

Market Opportunities

Naval Export Orders and Indian Ocean Region Defence Partnerships

India’s growing strategic influence in the Indian Ocean Region and the Ministry of Defence’s active promotion of defence exports under the Aatmanirbhar Bharat export initiative create a significant and increasingly concrete opportunity for Indian shipyards to expand their order books through foreign naval and paramilitary vessel exports. The Ministry of Defence has set an ambitious defence export target and has specifically identified naval platforms including offshore patrol vessels, fast interceptor craft, coastal surveillance vessels, training ships, and hydrographic survey vessels as categories where Indian shipyards can competitively offer indigenously designed and constructed platforms to partner nations. Several Indian Ocean Region countries, including Mauritius, Sri Lanka, Maldives, Seychelles, Vietnam, and Bangladesh, have already received or are in discussions to procure Indian-built naval and coast guard vessels through government-to-government defence cooperation frameworks and Lines of Credit extended by the Indian government. Cochin Shipyard and Garden Reach Shipbuilders have already delivered vessels to foreign navies and coast guards, establishing an early export track record that can be leveraged to pursue larger and more complex export programs. The strategic alignment between India’s neighbourhood foreign policy and defence cooperation commitments creates a government-backed diplomatic channel that facilitates naval vessel export discussions at the highest levels of bilateral engagement. Beyond the immediate Indian Ocean Region, Indian shipyards are exploring opportunities in Southeast Asia, Africa, and Latin America for patrol vessel, training ship, and utility craft exports, particularly in markets where cost-competitive alternatives from China face political or strategic resistance. Scaling naval export revenues requires sustained investment in international marketing capabilities, competitive export financing structures, after-sales service networks, and the development of a portfolio of export-optimised vessel designs certified by internationally recognised classification societies.

Green Shipbuilding, Dual-Fuel Vessel Construction and IMO Compliance Demand

The global maritime industry’s accelerating transition toward lower-emission vessel designs and alternative fuel propulsion systems, driven by the International Maritime Organization’s 2050 decarbonisation roadmap and strengthening carbon intensity regulations, creates a substantial new market opportunity for Indian shipyards that proactively develop green shipbuilding design and construction capabilities. The IMO’s Carbon Intensity Indicator regulations, which require operating vessels to progressively reduce their carbon intensity ratings on an annual basis or face trading restrictions, are already generating retrofitting demand at Indian ship repair yards while simultaneously creating new-build demand for vessels designed with alternative fuel readiness, improved hull efficiency, waste heat recovery systems, and energy-saving devices. The global orderbook for dual-fuel LNG vessels, methanol-ready tankers, and ammonia-capable bulk carriers has grown substantially in recent years as international shipowners seek to future-proof new vessel investments against tightening emission regulations, and Indian shipyards that develop the engineering competencies, classification approvals, and yard infrastructure to construct dual-fuel vessels can position themselves to capture a share of this growing order category. The government’s National Hydrogen Mission and the developing LNG import and bunkering infrastructure at Indian ports, supported by investments from Petronet LNG and major port operators, provide the enabling supply-side ecosystem for LNG-propelled vessel operations in Indian waters, strengthening the commercial case for domestic shipowners to order LNG dual-fuel vessels at Indian yards. For the inland waterways segment specifically, the Inland Waterways Authority of India’s procurement of electric and hybrid propulsion vessels for national waterway operations under the Jal Marg Vikas Project creates an immediate and government-backed order opportunity for Indian yards capable of constructing zero or low-emission inland vessels, a category where the technology barriers are lower than deep-sea green propulsion and domestic yards can develop competitive construction capabilities in a shorter timeframe.

Future Outlook

The India shipbuilding market is expected to witness sustained and substantial growth throughout the forecast period, supported by the Indian Navy’s multi-decade fleet expansion program, coast guard vessel procurement, Sagarmala-driven coastal and inland vessel demand, and progressive improvements in the commercial competitiveness of domestic yards under the Shipbuilding Financial Assistance Policy. Shipyards are increasingly investing in dry dock expansion, production automation, digital ship design, green vessel construction capabilities, and domestic marine equipment sourcing. Growing naval export opportunities, inland waterways fleet renewal, offshore energy vessel construction, and emerging demand for green and dual-fuel vessels are expected to create significant additional revenue opportunities beyond traditional naval construction. Continued investments in workforce development, classification society partnerships, international marketing, and strategic dry dock capacity expansion will be critical to translating India’s policy ambition into a globally recognised and commercially competitive shipbuilding industry by 2032.

Major Players

- Cochin Shipyard Limited (CSL)

- Mazagon Dock Shipbuilders Limited (MDL)

- Garden Reach Shipbuilders and Engineers Limited (GRSE)

- Hindustan Shipyard Limited (HSL)

- Goa Shipyard Limited (GSL)

- Hooghly Dock and Port Engineers Limited (HDPEL)

- ABG Shipyard

- Bharati Defence and Infrastructure Limited

- Shoft Shipbuilders

- Alcock Ashdown Gujarat Limited

- Chowgule and Company Shipyard

- Titagarh Rail Systems (Shipbuilding Division)

- SECON Engineering and Projects

- Drydocks World India

- L&T Shipbuilding (Larsen and Toubro)

Key Target Audience

- Naval Architects and Shipyard Engineering Teams

- Shipyard Operators and Yard Management Companies

- Marine Equipment and Component Manufacturers and Suppliers

- Naval Procurement and Defence Acquisition Authorities

- Commercial Shipping Companies and Fleet Operators

- Offshore Oil and Gas Vessel Operators

- Investments and Private Equity Firms

- Government and Regulatory Bodies (Ministry of Defence, Ministry of Ports, Shipping and Waterways, Directorate General of Shipping (DGS), Indian Register of Shipping (IRS), Defence Research and Development Organisation (DRDO))

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the major stakeholders across the India shipbuilding value chain, including naval procurement authorities, shipyard management, marine equipment suppliers, steel producers, classification societies, naval architects, defence research establishments, and commercial vessel operators. Extensive secondary research is conducted using Ministry of Defence publications, Ministry of Ports, Shipping and Waterways data, Directorate General of Shipping reports, Indian Register of Shipping vessel registry, Indian Ports Association statistics, company annual reports, and proprietary databases to establish the key variables influencing market performance.

Step 2: Market Analysis and Construction

Historical market information is compiled and evaluated to estimate the overall shipbuilding market size, gross tonnage delivered, vessel order books, shipyard revenue, steel and equipment input costs, and growth across major vessel categories and customer segments. Both demand-side and supply-side indicators are analyzed using bottom-up and top-down market sizing approaches to ensure comprehensive coverage across naval, commercial, offshore, inland waterways, and fishing vessel construction segments.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates and analytical assumptions are validated through Computer Assisted Telephone Interviews (CATIs) and structured discussions with shipyard executives and production managers, naval procurement officers, marine equipment suppliers, naval architects, classification society surveyors, defence policy experts, and commercial vessel operators. These interviews provide critical on-ground insights into production capacity, order pipeline visibility, cost structures, and competitive positioning that strengthen the reliability of market estimates.

Step 4: Research Synthesis and Final Output

The final stage integrates primary research findings with secondary information to develop a comprehensive assessment of market size, segmentation, competitive landscape, customer procurement behaviour, and future opportunities. Multiple validation techniques, including data triangulation across vessel registry data, Ministry of Defence procurement disclosures, shipyard annual reports, and IRS classification records, are employed to ensure the consistency, accuracy, and credibility of the final market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Aatmanirbhar Bharat Defence Shipbuilding Push, Indian Navy Fleet Expansion Program, Indian Coast Guard Vessel Procurement, Sagarmala Programme Coastal and Inland Vessel Demand, Shipbuilding Financial Assistance Policy (SBFAP), Rising Offshore Oil and Gas Vessel Demand, Inland Waterways Vessel Fleet Expansion, Green and Dual-Fuel Vessel New Builds)

- Market Challenges (Global Competitiveness Gap with China, South Korea and Japan, High Steel and Raw Material Input Costs, Limited Domestic Marine Equipment and Component Manufacturing, Skilled Shipbuilding Workforce Shortage, Long Build Cycles and Delivery Delays, Access to Competitive Shipbuilding Finance and Credit, Dry Dock Capacity Constraints, Complex Multi-Agency Regulatory and Procurement Environment)

- Market Opportunities (Naval Export Orders to Indian Ocean Region Partner Nations, Green Shipbuilding and Dual-Fuel Vessel Orders, Inland Waterways Fleet Procurement Under Jal Marg Vikas Project, Cruise and Passenger Ferry Vessel Construction, Fisheries Modernisation Vessel Replacement, Expansion of Private Sector Shipbuilding Capacity, Domestic Marine Equipment Manufacturing Under Make in India, Submarine Construction and Nuclear Propulsion Program)

- Market Trends (Integrated Construction and Block Assembly Methodology Adoption, Modular Shipbuilding Techniques, Digital Twin and Computer-Aided Ship Design, Green Ship Design and Alternative Fuel Readiness, Automation in Steel Fabrication and Outfitting, Naval Stealth and Signature Reduction Technologies, Unmanned Surface and Undersea Vessel Development, Hybrid Electric Propulsion for Inland and Coastal Vessels)

- Government Regulations and Policy Framework (Defence Acquisition Procedure (DAP) 2020 and Make in India Categories, Shipbuilding Financial Assistance Policy (SBFAP), Ministry of Ports, Shipping and Waterways Shipbuilding Promotion Framework, Directorate General of Shipping (DGS) Vessel Classification and Certification, Indian Register of Shipping (IRS) Classification Society Rules, Merchant Shipping Act 1958, SOLAS and MARPOL Compliance Requirements, IMO Tier III Emission Standards, International Load Line Convention, Cabotage Policy for Domestically Built Vessels)

- Steel and Raw Material Supply Analysis (Domestic Shipbuilding Steel Supply from SAIL and JSW Steel, High-Tensile Steel Plate Availability, Aluminium and FRP Material Sourcing, Steel Price Volatility and Input Cost Trends, Import Dependency for Specialised Marine Alloys, Anchor Chain and Propeller Casting Supply)

- Dry Dock and Shipyard Capacity Analysis (Number and Size Distribution of Dry Docks, Maximum Vessel Size Capability, Dry Dock Availability and Utilisation Rates, Planned Dry Dock Expansion Projects, Graving Dock vs Floating Dock Capacity, Ship Lift and Transfer System Availability)

- Naval Shipbuilding Pipeline Analysis (Indian Navy Warship Construction Program, P-17A Stealth Frigates, P-75I Submarine Program, Next Generation Destroyers, Landing Platform Docks, Aircraft Carrier INS Vikrant Follow-On, Indigenous Aircraft Carrier 2 (IAC-2) Planning, Auxiliary and Support Vessel Orders)

- Commercial Shipbuilding Order Book Analysis (Bulk Carrier Orders, Tanker Construction Pipeline, OSV and Offshore Vessel Orders, Inland Waterways Vessel Orders, Ferry and Passenger Vessel Construction, Dredger Procurement)

- Marine Equipment and Outfitting Analysis (Propulsion Systems Procurement, Marine Diesel Engine Sourcing, Deck Machinery and Anchoring Equipment, Navigation and Communication Systems, Accommodation and Interior Outfitting, Domestic vs Imported Marine Equipment Share)

- Innovation Landscape (Computer-Aided Design and Finite Element Analysis, Robotic Welding and Fabrication, 3D Printing for Marine Components, Digital Twin for Lifecycle Management, AI-Based Quality Control, LNG and Methanol Dual-Fuel Engine Integration, Integrated Platform Management Systems for Naval Vessels)

- Sustainability Analysis (IMO 2050 Decarbonisation Roadmap Compliance, Energy Efficiency Design Index (EEDI) and EEXI Standards, Carbon Intensity Indicator (CII) Readiness, Ballast Water Treatment System Integration, Green Shipbuilding Certification, Sustainable Steel and Material Sourcing, Emission-Compliant Paint and Coating Systems)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Gross Tonnage Delivered (2020-2025)

- By Number of Vessels Constructed (2020-2025)

- By Vessel Type (In Value %)

Warships and Naval Vessels (Aircraft Carriers, Destroyers, Frigates, Corvettes, Submarines)

Offshore Patrol Vessels and Coast Guard Craft

Bulk Carriers and Ore Carriers

Tankers (Crude Oil, Product, Chemical and LNG)

Container Vessels

Passenger Vessels, Ferries and Ro-Ro Ships

Offshore Support Vessels (OSVs) and Platform Supply Vessels

Dredgers and Hopper Barges

Inland Waterways Vessels and Barges

Fishing Vessels and Trawlers

Research and Oceanographic Vessels

Tugs, Workboats and Miscellaneous Craft - By Shipyard Type (In Value %)

Central Government-Owned Defence Shipyards

Central Government-Owned Commercial Shipyards

State Government-Owned Shipyards

Private Sector Shipyards

Small and Medium Shipbuilding Yards - By Construction Material (In Value %)

Steel (Mild Steel and High-Tensile Steel)

Aluminium Alloys

Fibre Reinforced Plastic (FRP)

Composite Materials

Stainless Steel - By Propulsion Technology (In Value %)

Conventional Diesel and Heavy Fuel Oil Propulsion

Dual-Fuel LNG Propulsion

Electric and Hybrid Propulsion

Gas Turbine Propulsion (Naval)

Nuclear Propulsion (Strategic Submarines)

Methanol and Green Ammonia-Ready Propulsion - By End-Use Customer (In Value %)

Indian Navy

Indian Coast Guard

Ministry of Ports, Shipping and Waterways

Oil and Natural Gas Corporation (ONGC) and Oil India Limited

Inland Waterways Authority of India (IWAI)

Private Shipping Companies

State Fisheries Departments and Fishing Cooperatives

Export Orders from Foreign Naval and Commercial Customers - By Shipyard Location (In Value %)

West Coast (Mumbai, Nhava Sheva, Goa, Mangalore, Cochin)

East Coast (Kolkata, Vizag, Chennai, Kakinada)

Gujarat (Surat, Bhavnagar, Alang Adjacent Yards)

Andaman and Nicobar Islands

Inland River Yards (Uttar Pradesh, Assam, West Bengal)

- Market Share Analysis (By Value, Gross Tonnage, Vessel Type, Customer Segment, Shipyard Location)

- Cross Comparison Parameters (Dry Dock Size and Number, Maximum Vessel Deadweight Tonnage Capability, Annual Vessel Delivery Capacity, Naval Construction Track Record, Commercial Order Book, Workforce Strength, Classification Society Approvals, Steel Fabrication Capacity, Design and Engineering Capability)

- SWOT Analysis of Major Shipyards

- Pricing Analysis (By Vessel Type, Tonnage Class, Construction Material, Propulsion System, Contract Type, Build Duration)

- Detailed Profiles of Major Companies

Cochin Shipyard Limited (CSL)

Mazagon Dock Shipbuilders Limited (MDL)

Garden Reach Shipbuilders and Engineers Limited (GRSE)

Hindustan Shipyard Limited (HSL)

Goa Shipyard Limited (GSL)

Hooghly Dock and Port Engineers Limited (HDPEL)

ABG Shipyard

Bharati Defence and Infrastructure Limited

Shoft Shipbuilders

Alcock Ashdown Gujarat Limited

Chowgule and Company Shipyard

Titagarh Rail Systems (Shipbuilding Division)

SECON Engineering and Projects

Drydocks World India

L&T Shipbuilding (Larsen and Toubro)

- Procurement Pattern Analysis (Vessel Ordering Frequency, Vessel Type and Specification Preference, Shipyard Selection Criteria, Build-to-Specification vs Standard Design Preference, Fleet Replacement Cycles)

- Customer Segmentation Analysis (Indian Navy, Indian Coast Guard, Government Commercial Shipping, Private Shipping Companies, Offshore Operators, State Fisheries, IWAI, Foreign Export Customers)

- Capital Expenditure and Lifecycle Cost Analysis

- Domestic vs Imported Vessel Preference Analysis

- Shipyard and Builder Loyalty and Repeat Order Analysis

- Regulatory and Classification Compliance-Driven Procurement Behaviour

- Vessel Specification Preference Analysis (Tonnage, Speed, Endurance, Propulsion Type, Fuel Type, Automation Level, Classification Society, Delivery Timeline, Price Competitiveness)

- Public Sector vs Private Sector Procurement Behaviour

- Export Customer Procurement Patterns and Requirements

- Customer Pain Point Analysis

- Procurement Decision-Making Process

- By Market Value (2026-2032)

- By Gross Tonnage Delivered (2026-2032)

- By Number of Vessels Constructed (2026-2032)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now