Download PDF

Download PDF Download PDF

Download PDFMarket Overview

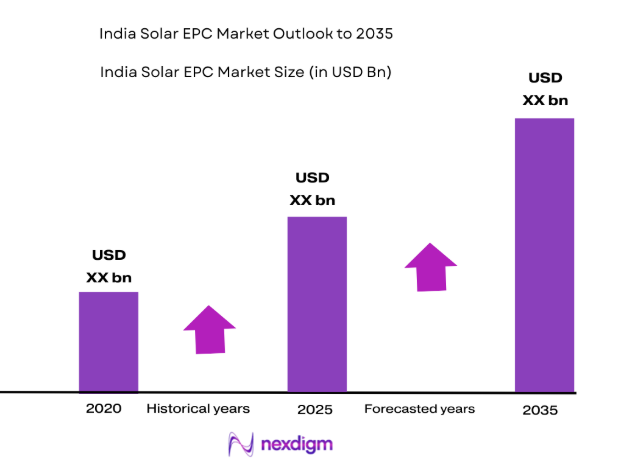

The India Solar EPC market is currently valued at USD ~ billion, driven primarily by increasing demand for renewable energy solutions. The market growth is further fueled by government policies promoting solar energy adoption, tax incentives for renewable energy projects, and a significant reduction in solar panel prices. With continuous investments in large-scale solar projects and infrastructure development, the market is witnessing accelerated growth. Additionally, the demand for energy independence and sustainability is contributing to this upward trajectory. The market is expected to expand as India strives to meet its renewable energy capacity targets.

India, particularly states like Rajasthan, Gujarat, and Tamil Nadu, holds a dominant position in the market due to favorable climate conditions for solar power generation and well-established solar energy infrastructure. The government’s strong push for clean energy has made India one of the largest markets for solar power globally. These regions have become key hubs for solar projects due to their vast land availability and high solar radiation, making them ideal for utility-scale solar projects. These areas have seen significant investments, helping propel India as a leader in solar energy deployment.

Market Segmentation

By Product Type

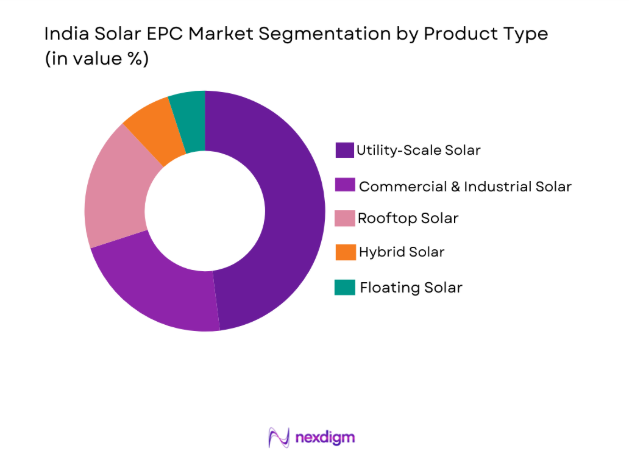

India Solar EPC market is segmented by product type into utility-scale solar, commercial and industrial solar, rooftop solar, hybrid solar systems, and floating solar systems. Utility-scale solar projects dominate the market due to their large-scale generation capacity and suitability for powering vast areas. The demand for utility-scale solar systems has been driven by government policies favoring renewable energy, as well as the growing need for sustainable, large-scale power generation. These projects provide low-cost electricity and are typically deployed in solar parks, offering the most cost-effective solution for meeting India’s growing energy demand.

By Platform Type

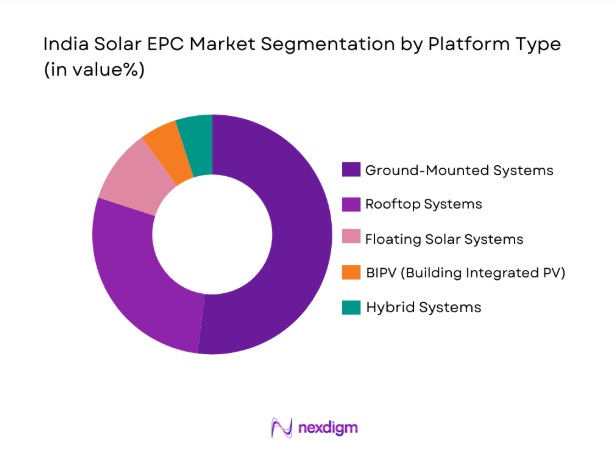

India Solar EPC market is segmented by platform type into ground-mounted systems, rooftop systems, floating solar systems, building-integrated photovoltaics (BIPV), and hybrid systems. Ground-mounted systems lead the market due to their ability to accommodate large-scale solar installations in open spaces, particularly in areas with high solar radiation. These systems are ideal for utility-scale projects and are expected to continue dominating the market as India expands its solar capacity. Ground-mounted platforms offer higher efficiency and are best suited for locations with sufficient land availability.

Competitive Landscape

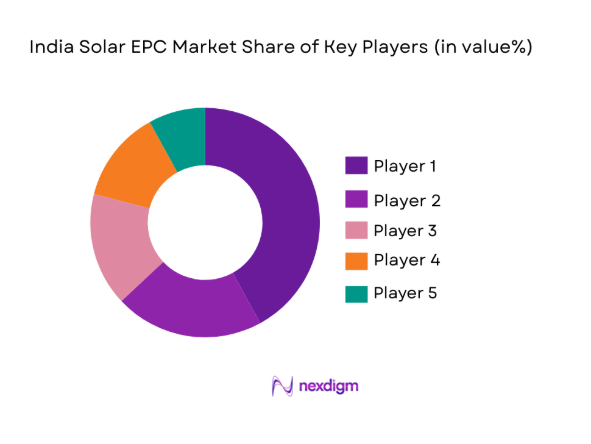

The competitive landscape of the India Solar EPC market is characterized by a mix of global and local players, with a strong focus on technological advancements and project execution capabilities. Major players are consolidating their market position by forming strategic partnerships and expanding their service offerings. The presence of large multinational companies such as Adani Green Energy and Tata Power Solar is intensifying competition, leading to price reduction and technological innovations in solar power generation systems. These companies dominate in terms of capacity installation and project management, while emerging players are also expanding their footprints through new collaborations and investments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| Tata Power Solar | 1999 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Adani Green Energy | 2010 | Ahmedabad, India | ~ | ~ | ~ | ~ | ~ |

| Sterling and Wilson Solar | 1983 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| ReNew Power | 2011 | Gurgaon, India | ~ | ~ | ~ | ~ | ~ |

| Vikram Solar | 2006 | Kolkata, India | ~ | ~ | ~ | ~ | ~ |

India Solar EPC Market Analysis

Growth Drivers

Government Incentives

The Indian government has been aggressively promoting the adoption of renewable energy, especially solar power, through various initiatives such as tax rebates, subsidies, and favorable tariffs. These incentives make solar projects more affordable, attracting both domestic and international investors. By facilitating large-scale solar projects and rooftop installations, government policies are directly influencing the growth of the solar EPC market. These incentives ensure that developers can continue to execute projects without significant financial barriers, fostering rapid growth in the sector. Furthermore, the government’s renewable energy targets, such as achieving 175 GW of renewable energy capacity by 2022 and 500 GW by 2030, have further strengthened the market’s potential. These ambitious goals have stimulated investments, making India one of the most attractive markets for solar energy developers. Government-backed schemes like the National Solar Mission and Solar Park Scheme have provided the necessary infrastructure and policy support, encouraging private sector participation in the development of solar energy projects.

Technological Advancements

The continuous advancement in solar technology, especially in solar panel efficiency, inverter technology, and energy storage solutions, is playing a crucial role in the growth of the India Solar EPC market. More efficient solar panels and inverters are reducing the overall cost of solar energy generation, making solar systems more economically viable for a broader range of consumers. Additionally, improvements in energy storage technologies ensure that solar power can be stored and used even during non-sunny periods, making solar energy more reliable. The development of innovative solutions such as bifacial solar panels, which capture sunlight on both sides, and perovskite solar cells, which are expected to be more efficient and cost-effective, is pushing the market forward. These innovations, combined with falling costs of solar components, contribute significantly to the expansion of solar power adoption in India. The adoption of smart grid technology, which allows for efficient distribution of solar energy, is also a key driver, enabling better integration of solar energy into the national grid and further accelerating growth in the sector.

Market Challenges

High Initial Capital Investment

One of the major challenges faced by the India Solar EPC market is the high capital investment required for large-scale solar projects. Despite falling component costs, the upfront expenditure for land acquisition, construction, and installation of solar systems remains a significant barrier. These costs are particularly challenging for smaller developers and startups, making it difficult for them to enter the market. Financial institutions’ reluctance to provide large loans for such projects further adds to the financial burden, limiting the growth of smaller players in the industry. The long payback period of solar projects, which can extend over 7 to 10 years, deters private investments, especially from smaller companies. Moreover, with the high initial investment, the risk factor also increases, especially with changing market conditions, which can make financing a project more complicated. This financial burden has led to the dominance of larger corporations in the market, as they have access to more significant capital investments and risk management strategies.

Regulatory Hurdles

While the Indian government supports solar energy, there are still several regulatory hurdles that hinder the faster adoption of solar energy. Long approval processes, delays in land acquisition, and complex grid connectivity requirements have slowed down the execution of solar projects. In some regions, local regulations restrict the establishment of large-scale solar farms, further limiting expansion. These hurdles increase the overall cost of project execution, thus discouraging potential investors and developers from entering the market. Moreover, inconsistent policies at the state level can further complicate the implementation of solar projects. Some states have more favorable policies for solar development, while others lack adequate incentives, which can create discrepancies in market growth. Additionally, land disputes and environmental clearance issues can delay the timely completion of projects, which is a critical factor in the long-term growth of the market. These regulatory barriers create uncertainty, making it difficult for developers to plan and execute projects efficiently.

Opportunities

Rooftop Solar Expansion

The growing interest in rooftop solar installations presents a significant opportunity for the India Solar EPC market. With the government’s focus on promoting decentralized energy solutions, more residential and commercial buildings are being encouraged to install rooftop solar systems. This opportunity is further supported by increasing electricity costs and a growing need for energy independence. As the technology continues to improve, rooftop solar will become more affordable, attracting a broader customer base. The reduction in the cost of solar panels, along with the growing popularity of energy-efficient homes and buildings, has made rooftop solar more accessible to a larger population. Additionally, the introduction of net metering policies by the government, which allow solar users to sell excess energy back to the grid, has further increased the attractiveness of rooftop solar installations. This market segment is expected to grow substantially over the next few years, driven by urbanization, the increase in electricity demand, and the government’s push for energy security. As a result, rooftop solar is set to play a crucial role in India’s overall solar capacity expansion.

Hybrid Systems Adoption

Hybrid solar systems, which integrate both solar power and energy storage solutions, present a promising opportunity in India. As the demand for reliable and uninterrupted power supply increases, hybrid systems are gaining traction among businesses and residential customers. These systems offer a sustainable solution to power outages and grid instability, making them an attractive choice. In rural areas and regions with unreliable power grids, hybrid systems can provide a continuous power supply, addressing energy security concerns. Furthermore, as battery storage technology improves, the adoption of hybrid solar systems is expected to increase significantly. With advancements in lithium-ion batteries and other storage technologies, hybrid systems are becoming more cost-competitive and are expected to become an essential part of India’s solar future. The growth of the electric vehicle (EV) market also presents a synergistic opportunity for hybrid systems, as these systems can integrate with EV charging stations to provide green and reliable power solutions. This presents a major growth avenue for the India Solar EPC market as hybrid solar systems cater to a diverse range of energy needs.

Future Outlook

The India Solar EPC market is poised for continued growth over the next five years, driven by technological advancements, supportive government policies, and an increased focus on clean energy. The growth of large-scale solar parks, coupled with a surge in rooftop solar installations, is expected to dominate the market. In addition, the integration of solar energy with energy storage systems will play a crucial role in ensuring grid stability and improving energy security. As solar power becomes more cost-competitive with conventional sources, the adoption of solar technologies will expand across various sectors, contributing to the achievement of India’s renewable energy targets.

Major Players

- Tata Power Solar

- Adani Green Energy

- Sterling and Wilson Solar

- ReNew Power

- Vikram Solar

- Mahindra Susten

- Azure Power

- First Solar

- Trina Solar

- JinkoSolar

- Canadian Solar

- BHEL

- Sungrow Power Supply

- Siemens Gamesa

- L&T Construction

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Renewable energy developers

- Large-scale solar project developers

- Utility companies

- Commercial and industrial solar energy consumers

- Private sector technology firms

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying key variables that influence the India Solar EPC market, including government policies, technological trends, market demand, and financial aspects.

Step 2: Market Analysis and Construction

This step includes the analysis of market trends, competition, and growth drivers, followed by constructing an accurate market model based on available data.

Step 3: Hypothesis Validation and Expert Consultation

Experts in the solar energy field are consulted to validate assumptions and hypotheses, ensuring the accuracy and reliability of the research findings.

Step 4: Research Synthesis and Final Output

The research findings are synthesized into a final report, which includes market insights, future forecasts, and actionable recommendations for stakeholders in the India Solar EPC market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Incentives for Renewable Energy Projects

Reduction in Solar Panel Costs

Rising Energy Demand and Power Shortages

Technological Advancements in Solar Systems

Expansion of Solar Capacity Targets - Market Challenges

High Capital Expenditure for Initial Installation

Intermittency of Solar Power

Regulatory Hurdles and Policy Changes

Lack of Skilled Workforce

Grid Integration Challenges - Market Opportunities

Rising Demand for Rooftop Solar Solutions

Government Focus on Energy Security and Sustainability

Technological Innovations in Solar Energy Storage - Trends

Growing Adoption of Hybrid Systems

Increase in Large-Scale Solar Power Projects - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility-Scale Solar Projects

Commercial & Industrial Solar Projects

Residential Solar Systems

Rooftop Solar Systems

Hybrid Solar Systems - By Platform Type (In Value%)

Ground-Mounted Systems

Rooftop Systems

Floating Solar Systems

BIPV (Building Integrated Photovoltaics)

Hybrid Systems - By Fitment Type (In Value%)

On-Grid Systems

Off-Grid Systems

Hybrid Systems

Floating Systems - By End User Segment (In Value%)

Government & Public Sector

Private Sector (Commercial & Industrial)

Residential

Utilities

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology, Pricing Strategy)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tata Power Solar Systems

Sterling and Wilson Solar

Larsen & Toubro

Adani Green Energy

Mahindra Susten

Vikram Solar

Azure Power

Renew Power

Trina Solar

First Solar

JinkoSolar

Canadian Solar

BHEL

Sungrow Power Supply

Siemens Gamesa

- Government Incentives and Policy Impact on Public Sector

- Private Sector Growth Driving Demand for Solar Energy

- Residential Market Growth Amid Rising Energy Prices

- Utility Investments in Large-Scale Solar Projects

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now