Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the India telemedicine market generated approximately USD ~ billion according to digital health ecosystem evaluations by the National Health Authority and industry assessments referenced by NITI Aayog. Market expansion is driven by large-scale digital healthcare programs, growing internet connectivity exceeding 900 million users according to the Telecom Regulatory Authority of India, and increasing demand for remote consultations. Hospital networks, digital health platforms, and public telehealth services are accelerating the adoption of telemedicine technologies across primary and specialty care delivery.

Major metropolitan regions including Bengaluru, Hyderabad, Mumbai, Delhi NCR, and Chennai dominate the India telemedicine market because these cities host strong healthcare infrastructure, advanced hospital networks, and large digital health startup ecosystems. These technology hubs benefit from high smartphone penetration, strong IT capabilities, and venture capital funding supporting telemedicine innovation. Urban healthcare providers integrate virtual consultations, AI-enabled triage systems, and remote diagnostics within clinical workflows, making these cities central hubs for telemedicine deployment and healthcare technology development.

Market Segmentation

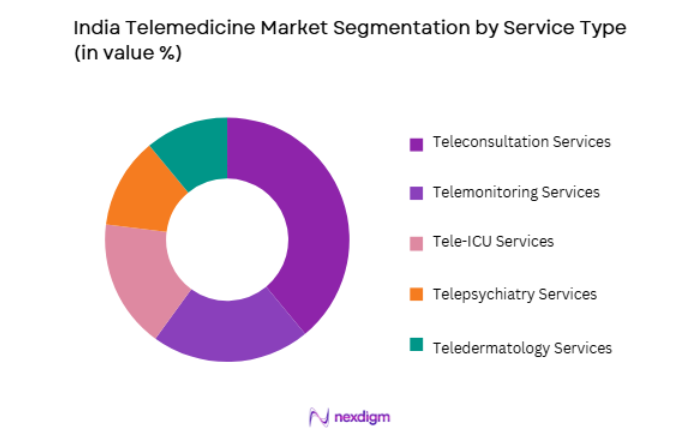

By Service Type

India Telemedicine market is segmented by service type into teleconsultation services, telemonitoring services, tele-ICU services, telepsychiatry services, and teledermatology services. Recently, teleconsultation services have a dominant market share due to factors such as demand patterns for remote healthcare access, growing smartphone connectivity, strong hospital adoption, and patient preference for virtual consultations. Teleconsultation platforms allow patients to connect with physicians through mobile applications or web portals without visiting hospitals physically. Public telemedicine systems integrated within national healthcare programs also provide remote consultations through government healthcare centers. Hospitals increasingly integrate teleconsultation platforms to manage outpatient demand efficiently and extend specialist services to rural areas. Private healthcare providers deploy digital consultation services across specialties including general medicine, cardiology, pediatrics, and dermatology.

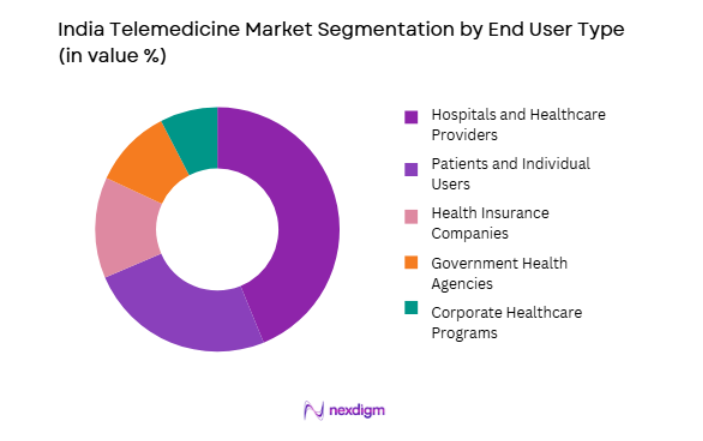

By End User

India Telemedicine market is segmented by end user into hospitals and healthcare providers, patients and individual users, health insurance companies, government health agencies, and corporate healthcare programs. Recently, hospitals and healthcare providers have a dominant market share due to factors such as rapid digital transformation within hospital systems, integration of telehealth services into clinical operations, and increasing patient demand for remote consultations. Large hospital chains implement telemedicine platforms to expand specialist access and improve patient engagement beyond physical facilities. Telemedicine allows hospitals to deliver consultations to rural health centers and smaller clinics lacking specialist expertise. Hospitals also integrate remote patient monitoring technologies that support chronic disease management through continuous health tracking. Digital appointment systems, electronic medical records integration, and AI-based triage tools enhance operational efficiency within telemedicine frameworks.

Competitive Landscape

The India telemedicine market demonstrates moderate consolidation with multiple digital health platforms, hospital telehealth divisions, and technology startups competing through integrated teleconsultation, remote monitoring, and AI-enabled diagnostic platforms. Leading telemedicine companies operate nationwide platforms connecting doctors, pharmacies, laboratories, and patients within digital healthcare ecosystems. Venture capital investment and government digital health initiatives continue strengthening the competitive landscape, while hospital chains increasingly partner with technology companies to develop scalable telemedicine infrastructure and integrated healthcare delivery models.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Telemedicine Service Model |

| Practo Technologies | 2008 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| Tata 1mg | 2015 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Apollo TeleHealth | 1999 | Hyderabad, India | ~ | ~ | ~ | ~ | ~ |

| mfine | 2017 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| Lybrate | 2013 | Delhi, India | ~ | ~ | ~ | ~ | ~ |

India Telemedicine Market Analysis

Growth Drivers

Expansion of Government Digital Health Infrastructure and National Telemedicine Programs

India’s telemedicine market is expanding rapidly due to large scale government investments designed to build national digital healthcare infrastructure and improve access to medical services across geographically diverse populations. The Ayushman Bharat Digital Mission implemented by the National Health Authority establishes interoperable digital health systems that connect patients, hospitals, laboratories, pharmacies, and insurance providers through unified health identification systems and electronic health records. Government telemedicine platforms such as eSanjeevani provide virtual consultations for patients visiting public health centers across rural and semi urban regions where medical specialists may not be physically available. Public health authorities deploy telemedicine services to strengthen primary healthcare delivery while enabling doctors located in urban hospitals to consult patients in remote villages through digital networks. These programs reduce geographical barriers to healthcare access while improving clinical decision making through digital patient records accessible across healthcare institutions. Hospitals participating in national telehealth networks can share patient data, diagnostic reports, and treatment histories within standardized digital platforms that improve coordination between healthcare providers. Government supported digital registries for doctors and healthcare facilities strengthen transparency and trust within telemedicine ecosystems. Telemedicine also enables public health authorities to respond quickly to disease outbreaks and manage patient consultations during healthcare emergencies when physical hospital visits may be limited. Large population scale digital health programs also encourage private sector innovation because startups and technology companies can develop applications that integrate with government digital health architecture. Telecommunication providers further support these initiatives by expanding broadband connectivity and mobile internet infrastructure across rural regions where telemedicine demand continues increasing.

Rapid Growth of Smartphone Connectivity and Consumer Adoption of Virtual Healthcare Services

The rapid expansion of smartphone connectivity across India has significantly accelerated adoption of telemedicine services by enabling millions of patients to access healthcare consultations directly through mobile devices. India hosts one of the largest smartphone user bases globally with hundreds of millions of internet connected devices capable of supporting telehealth applications and video consultations with medical professionals. Mobile healthcare platforms allow patients to schedule doctor consultations, upload medical records, receive electronic prescriptions, and arrange laboratory tests through integrated digital applications accessible anywhere with internet connectivity. This accessibility is particularly valuable for patients living in rural areas where travel to major hospitals can require significant time and transportation costs. Telemedicine platforms also improve healthcare accessibility for elderly patients, individuals with mobility limitations, and people requiring frequent consultations for chronic disease management. Healthcare providers benefit from telemedicine because digital consultation systems reduce overcrowding in hospital outpatient departments while allowing doctors to manage patient interactions more efficiently. Mobile healthcare applications also integrate digital payment systems, pharmacy ordering platforms, and diagnostic appointment scheduling features that simplify the healthcare process for patients. Health insurance providers increasingly support telemedicine consultations within digital policyholder platforms to encourage preventive healthcare and reduce long term treatment costs. Venture capital funding continues supporting telehealth startups developing innovative mobile consultation services, remote monitoring technologies, and AI based patient triage systems tailored to India’s diverse population.

Market Challenges

Fragmented Healthcare Delivery Systems and Limited Telemedicine Infrastructure in Rural Regions

A major challenge affecting the India telemedicine market involves the fragmented nature of healthcare delivery systems combined with uneven access to digital healthcare infrastructure across rural regions. India’s healthcare ecosystem consists of numerous public hospitals, private clinics, diagnostic centers, and independent medical practitioners that often operate using different information systems or manual patient record processes. Many smaller healthcare facilities continue relying on paper based documentation which prevents seamless integration with telemedicine platforms and electronic health record systems. Rural healthcare centers frequently experience limited broadband connectivity and unstable internet services that restrict the effectiveness of video consultations and remote monitoring technologies. Healthcare workers in remote clinics may also lack sufficient digital training required to operate telemedicine platforms efficiently. Limited availability of diagnostic equipment in rural health facilities can also reduce the effectiveness of remote consultations because doctors require laboratory tests and imaging reports to make accurate diagnoses. Smaller healthcare providers may face financial constraints that limit investment in telemedicine equipment such as digital consultation software, secure data storage systems, and telehealth communication infrastructure. Interoperability issues between different digital health platforms further complicate the exchange of patient information between hospitals, pharmacies, laboratories, and insurance providers. These technical limitations reduce the efficiency of telemedicine services and hinder large scale integration of digital healthcare systems. Patients in remote communities may also have limited digital literacy which affects their ability to use telemedicine applications effectively.

Data Privacy Concerns and Regulatory Complexity in Telemedicine Service Delivery

Data privacy concerns and evolving regulatory frameworks represent another significant challenge affecting the development of the India telemedicine market. Telemedicine platforms manage extensive volumes of sensitive healthcare data including medical records, diagnostic reports, prescriptions, and patient identification information which require strict data protection protocols to prevent unauthorized access. Ensuring cybersecurity across telemedicine platforms is critical because healthcare data breaches can compromise patient confidentiality and undermine trust in digital healthcare services. Telemedicine companies must implement secure cloud infrastructure, encrypted communication systems, and robust identity verification mechanisms to protect patient information stored within digital platforms. Regulatory compliance requirements governing telemedicine practice, digital prescriptions, and cross state medical consultations also introduce operational complexity for healthcare providers and technology companies. Healthcare professionals must adhere to telemedicine practice guidelines issued by regulatory authorities to ensure legal compliance while delivering remote consultations. These regulations define standards for patient consent, prescription protocols, medical documentation, and doctor identification verification during virtual consultations. Telemedicine startups may face additional compliance costs associated with meeting cybersecurity standards and data governance requirements necessary for healthcare technology platforms. Uncertainty surrounding evolving digital health data protection policies can also influence technology investment decisions within the telemedicine sector. Hospitals and telemedicine providers must continuously update their technology systems to align with emerging healthcare information regulations and cybersecurity guidelines. Strengthening regulatory clarity and establishing standardized healthcare data governance frameworks will therefore be essential for enabling sustainable development of telemedicine services within India’s healthcare ecosystem.

Opportunities

Integration of Artificial Intelligence Driven Diagnostic Tools within Telemedicine Platforms

Artificial intelligence technologies present significant opportunities for the India telemedicine market by enhancing diagnostic capabilities, improving clinical decision support, and enabling more efficient patient triage within virtual healthcare platforms. AI driven healthcare systems can analyze medical imaging, patient health records, and symptom data to assist doctors in identifying potential medical conditions more quickly during remote consultations. These systems allow telemedicine platforms to support early detection of diseases such as cardiovascular disorders, respiratory conditions, and certain cancers by analyzing diagnostic data provided during teleconsultations. AI powered symptom assessment tools integrated within telemedicine applications can guide patients toward appropriate medical specialists by evaluating symptoms and recommending suitable consultations. Healthcare providers benefit from AI diagnostic assistance because automated analytics systems can process large volumes of clinical data and highlight potential abnormalities that require medical attention. Telemedicine platforms can also use AI algorithms to monitor patient health trends through wearable devices that track physiological indicators such as heart rate, blood pressure, and physical activity patterns. These technologies allow doctors to remotely monitor chronic disease patients and intervene quickly if abnormal health patterns emerge. Pharmaceutical companies and diagnostic laboratories can also integrate AI analytics systems with telemedicine platforms to support clinical decision making and remote diagnostic interpretation. AI enabled automation reduces the time required for medical data analysis while increasing diagnostic accuracy within telehealth environments. Venture capital investment into AI health technology startups continues supporting development of advanced telemedicine tools that combine machine learning algorithms with digital healthcare delivery systems.

Expansion of Telemedicine Services into Rural and Underserved Healthcare Markets

The expansion of telemedicine services into rural and underserved healthcare markets represents one of the most significant growth opportunities for the India telemedicine market because millions of citizens still face limited access to specialized healthcare services. Rural communities often lack sufficient numbers of qualified medical professionals, particularly specialists such as cardiologists, neurologists, and oncologists who are typically concentrated in major urban hospitals. Telemedicine platforms allow these specialists to provide consultations to patients located in remote villages through digital health centers equipped with video consultation systems and basic diagnostic tools. Government healthcare initiatives increasingly deploy telemedicine infrastructure within rural primary healthcare centers to connect patients with doctors located in urban hospitals. Mobile healthcare units and community health workers also facilitate telemedicine consultations by assisting patients in remote areas with digital health applications and telehealth communication systems. Telecommunications companies continue expanding broadband networks and mobile internet connectivity across rural India which further supports telemedicine adoption. Telemedicine services can also support preventive healthcare programs such as maternal health monitoring, vaccination follow ups, and chronic disease management programs delivered through digital health platforms. Healthcare providers benefit from telemedicine expansion because digital consultations allow them to reach larger patient populations without establishing new physical clinics in every rural region. Insurance companies also recognize telemedicine as a cost effective healthcare delivery model that reduces hospitalization costs through early diagnosis and continuous health monitoring.

Future Outlook

The India telemedicine market is expected to expand significantly over the next five years as healthcare providers continue integrating digital consultation systems within hospital networks and outpatient services. Artificial intelligence diagnostic tools, remote monitoring technologies, and mobile health platforms will further enhance telemedicine capabilities. Government digital health programs will continue strengthening telehealth infrastructure across rural healthcare centers. Increasing smartphone connectivity and healthcare technology investment will further accelerate demand for telemedicine services nationwide.

Major Players

- PractoTechnologies

- Tata 1mg

- Apollo TeleHealth

- mfine

- Lybrate

- Netmeds

- DocsApp

- HealthifyMe

- PharmEasy

- Medlife

- Portea Medical

- Innovaccer

- Qure.ai

- MedGenome

- Remedico

Key Target Audience

- Healthcare providers and hospital networks

- Pharmaceutical companies

- Telemedicine platform developers

- Health insurance companies

- Medical device manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare IT solution providers

Research Methodology

Step 1: Identification of Key Variables

Key variables including telemedicine adoption rates, digital health infrastructure development, smartphone connectivity, healthcare IT investments, and government digital health programs were identified through analysis of national healthcare policies and digital healthcare technology adoption trends.

Step 2: Market Analysis and Construction

The telemedicine market structure was constructed through evaluation of service categories including teleconsultation, telemonitoring, tele-ICU services, and specialty telemedicine solutions deployed across hospitals, digital health platforms, and government healthcare networks.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions were validated through consultations with healthcare technology specialists, hospital administrators, digital health entrepreneurs, and telemedicine platform developers to ensure accuracy regarding technology adoption patterns and regulatory frameworks.

Step 4: Research Synthesis and Final Output

Research findings were synthesized through triangulation of multiple data sources, comparative technology adoption analysis, and structured evaluation of healthcare digitalization trends to produce a comprehensive assessment of the India telemedicine market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of digital health infrastructure and broadband connectivity across urban and rural regions

Rising demand for remote medical consultations to improve healthcare accessibility

Government initiatives promoting telehealth services under national digital health programs - Market Challenges

Concerns regarding patient data security and digital health privacy

Limited awareness and digital literacy in rural populations

Integration challenges between telemedicine platforms and hospital information systems - Market Opportunities

Expansion of telemedicine services in rural and underserved healthcare regions

Adoption of AI powered diagnostic support within teleconsultation platforms

Partnerships between hospitals and digital health startups to scale telehealth services - Trends

Rapid growth of mobile based teleconsultation applications

Integration of wearable health monitoring devices with telemedicine platforms - Government Regulations

Telemedicine Practice Guidelines issued by national health authorities

Digital health data management frameworks under national digital health programs

Regulatory standards for online medical consultation and e prescriptions - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Real Time Video Consultation Platforms

Store and Forward Telemedicine Systems

Remote Patient Monitoring Systems

Mobile Based Telemedicine Applications

AI Assisted Teleconsultation Platforms - By Platform Type (In Value%)

Hospital Integrated Telemedicine Platforms

Cloud Based Telemedicine Platforms

Mobile Telemedicine Platforms

Wearable Device Integrated Telemedicine Platforms

Government Telehealth Service Platforms - By Fitment Type (In Value%)

Standalone Telemedicine Applications

Integrated Hospital Telemedicine Systems

Cloud Hosted Telemedicine Infrastructure

AI Enabled Clinical Teleconsultation Systems - By End User Segment (In Value%)

Hospitals and Multi Specialty Clinics

Diagnostic Centers and Laboratories

Individual Patients and Remote Healthcare Users

- Market Share Analysis

- Cross Comparison Parameters (Consultation Platform Capability, Data Security Compliance, Integration with Hospital Systems, User Accessibility Interface, AI Assisted Diagnostic Support, Video Consultation Quality, Electronic Prescription Integration, Remote Patient Monitoring Compatibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Practo

Tata 1mg

PharmEasy

Apollo 24 7

Mfine

DocsApp

HealthPlix

CureFit Healthcare

Netmeds

MediBuddy

Lybrate

DocOnline

Tricog Health

Dozee

HealthifyMe

- Hospitals integrating teleconsultation services to extend healthcare outreach

- Diagnostic centers using telemedicine platforms for remote reporting and consultation

- Patients adopting digital consultation services for convenience and accessibility

- Insurance providers integrating telemedicine services for preventive healthcare management

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now