Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Tractor market reached approximately USD ~ billion based on a recent historical assessment derived from tractor production volumes, average selling prices, and mechanization statistics reported by the Ministry of Agriculture and industry bodies such as FICCI and CII. Demand is driven by expanding farm mechanization, replacement of aging tractors, and rising adoption of higher horsepower models for multi-crop operations. Government mechanization subsidies and rural financing access further stimulate procurement across small and medium landholding segments.

Major activity centers are concentrated in Uttar Pradesh, Punjab, Haryana, Maharashtra, and Madhya Pradesh due to intensive cultivation, high tractor density, and strong dealer networks. Cities such as Ludhiana, Hoshiarpur, Pune, and Chennai function as manufacturing hubs hosting major tractor OEM plants and component ecosystems. These regions benefit from fertile agro-climatic conditions, commercial farming practices, and logistics connectivity, enabling sustained tractor demand and localized supply chains supporting distribution and service infrastructure.

Market Segmentation

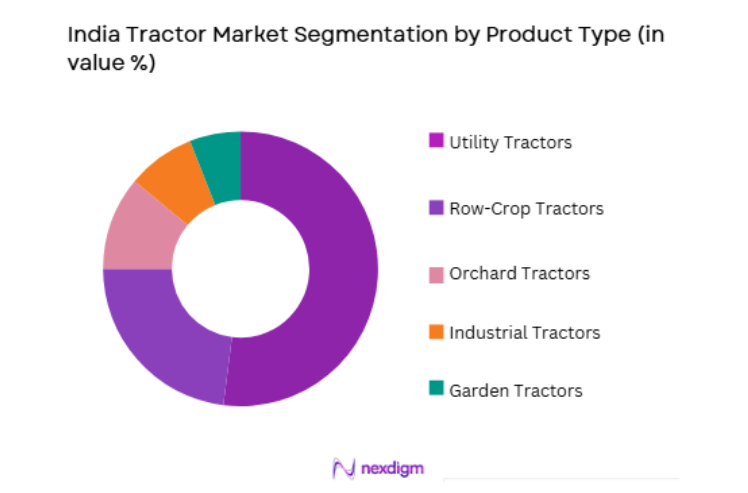

By Product Type

India Tractor market is segmented by product type into utility tractors, row-crop tractors, orchard tractors, garden tractors, and industrial tractors. Recently, utility tractors has a dominant market share due to factors such as versatility across multiple farming tasks, suitability for small and medium landholdings, and affordability relative to specialized tractor categories. Utility tractors support plowing, hauling, and implement operations across diverse crops and terrains, aligning with fragmented farm structures and mixed farming systems prevalent across India, ensuring consistent demand.

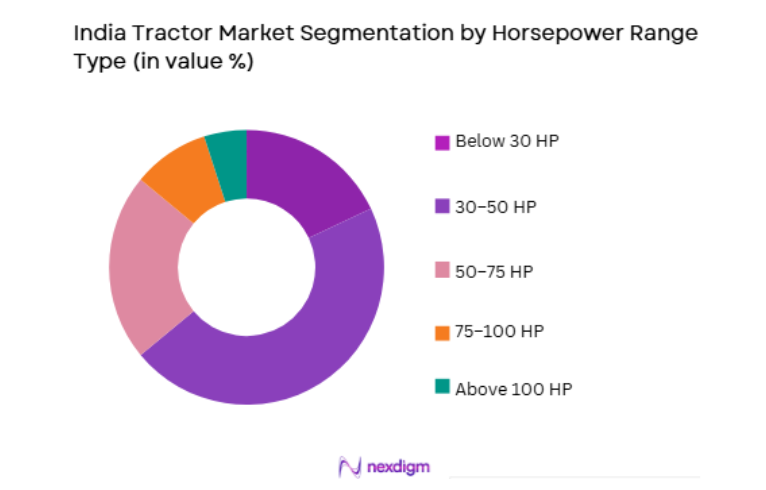

By Horsepower Range

India Tractor market is segmented by horsepower range into below 30 HP, 30–50 HP, 50–75 HP, 75–100 HP, and above 100 HP. Recently, 30–50 HP has a dominant market share due to factors such as compatibility with average farm size, suitability for major crop operations, and balance between power and fuel efficiency. This range supports primary tillage, transport, and implement applications while remaining affordable for smallholder farmers, making it the most practical and widely adopted horsepower category across India.

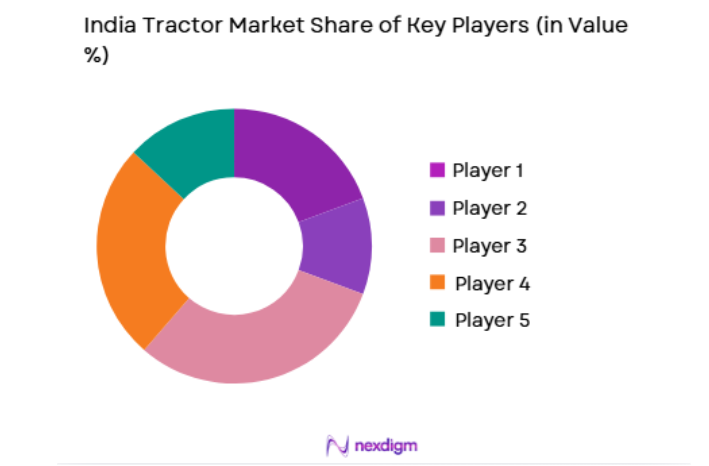

Competitive Landscape

The India Tractor market is moderately consolidated with a few dominant domestic manufacturers controlling large volumes through extensive dealer networks and localized manufacturing. Major players leverage brand trust, financing support, and product range breadth to maintain leadership, while global OEMs compete in higher horsepower and specialized segments. Consolidation is reinforced by scale economies, nationwide distribution, and strong aftermarket ecosystems that lock in customer loyalty and lifecycle revenue streams.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Size |

| Mahindra & Mahindra Farm Equipment | 1945 | India | ~ | ~ | ~ | ~ | ~ |

| TAFE | 1960 | India | ~ | ~ | ~ | ~ | ~ |

| Escorts Kubota | 1944 | India | ~ | ~ | ~ | ~ | ~ |

| Sonalika International | 1996 | India | ~ | ~ | ~ | ~ | ~ |

| John Deere India | 1998 | India | ~ | ~ | ~ | ~ | ~ |

India Tractor Market Analysis

Growth Drivers

Rising Farm Mechanization and Productivity Enhancement Imperatives

The India Tractor market is strongly driven by structural expansion of farm mechanization as agricultural productivity requirements increase across diverse cropping systems and regions. Mechanization reduces dependence on manual labor, improves timeliness of operations, and enhances yield potential, making tractors essential assets for modern farming practices. Labor migration to non-farm sectors creates workforce shortages that accelerate tractor adoption to maintain operational continuity. Government mechanization programs and rural development policies actively promote tractor ownership through subsidies and financing schemes. Increasing commercialization of agriculture and shift toward market-oriented crop production further raise demand for mechanized field operations and transport capacity. Tractors enable multi-functional applications including tillage, sowing, spraying, and hauling, making them central to farm mechanization ecosystems. Replacement demand from aging tractor fleets sustains market volume alongside new adoption. Expansion of irrigation and double-cropping intensifies machinery utilization and reinforces tractor necessity. Mechanization penetration into eastern and central India expands the addressable market beyond traditional high-density states. As productivity and efficiency imperatives deepen across Indian agriculture, tractors remain the foundational mechanization platform driving sustained market growth.

Growth of Rural Financing and Tractor Ownership Accessibility

The India Tractor market benefits from expanding rural credit availability and innovative financing mechanisms that improve tractor affordability for small and medium farmers. Public and private sector banks, non-bank financial institutions, and OEM-linked financing arms provide tailored loan products aligned with agricultural income cycles. Low down-payment schemes and extended repayment tenures reduce upfront acquisition barriers for farmers with limited capital reserves. Government interest subvention programs further reduce financing cost and stimulate tractor procurement. OEM dealers integrate financing support into sales processes, simplifying purchase decisions and expanding customer reach in rural markets. Availability of second-hand tractor financing also encourages replacement purchases and market liquidity. Financing penetration increases adoption in regions with emerging mechanization demand where farm incomes alone would not support cash purchases. Structured credit systems also enable farmers to upgrade to higher horsepower models as operational scale expands. Financial inclusion initiatives and rural banking expansion strengthen long-term purchasing capacity for farm equipment. Improved access to credit therefore acts as a major driver sustaining tractor demand growth across India.

Market Challenges

Fragmented Landholdings and Limited Farm Scale Economics

The India Tractor market faces structural challenges from highly fragmented agricultural landholdings that constrain tractor ownership economics for many farmers. Small farm sizes reduce machinery utilization rates, making capital investment in tractors financially inefficient relative to land area cultivated. Farmers operating marginal holdings often cannot generate sufficient revenue to justify tractor acquisition and maintenance costs. Shared ownership or hiring arrangements partially address this constraint but limit individual tractor demand growth. Mechanization efficiency is lower on fragmented plots due to irregular field shapes and boundaries that restrict tractor maneuverability. Smaller farms also rely more on animal or manual labor for certain operations, reducing mechanization necessity. Land fragmentation limits adoption of higher horsepower tractors that require larger operational scale for economic viability. Rural consolidation of holdings progresses slowly, maintaining structural demand constraints in several regions. Even with financing support, many farmers prefer hiring services rather than ownership. This landholding structure therefore moderates long-term tractor market expansion potential in India.

Seasonal Demand Volatility and Agricultural Income Dependence

The India Tractor market experiences demand fluctuations linked to agricultural income variability, monsoon performance, and crop price cycles that influence farmer purchasing capacity. Tractor procurement decisions are highly sensitive to harvest outcomes and commodity price realizations, creating cyclical sales patterns across years. Weak monsoon conditions reduce farm income and defer capital purchases including tractors. Agricultural credit risk perceptions also tighten financing availability during low-income periods, further dampening demand. Tractor manufacturers and dealers face inventory and production planning challenges due to seasonal buying behavior concentrated around crop cycles and subsidy disbursement timing. Regional crop failures create localized market contractions affecting distribution networks. Farmers prioritize essential input expenditure over machinery investment during uncertain income periods. Market growth therefore remains linked to broader agricultural economic stability rather than purely mechanization needs. These income-dependent demand cycles introduce volatility and constrain predictable tractor market expansion in India.

Opportunities

Adoption of Higher Horsepower and Specialized Tractors for Commercial Farming

The India Tractor market holds significant opportunity in the gradual shift toward higher horsepower and specialized tractors driven by farm consolidation, contract farming, and commercial agriculture expansion. Larger farms and agribusiness operations require powerful tractors capable of operating advanced implements and covering greater acreage efficiently. Specialized tractors for orchards, plantations, and precision agriculture applications also present growth potential beyond traditional utility segments. Mechanization of horticulture and cash crops encourages adoption of niche tractor configurations tailored to specific crop geometries. Commercial farming enterprises prioritize productivity and operational scale, supporting demand for technologically advanced tractors with higher performance. Infrastructure development and rural logistics expansion enable utilization of larger tractors across broader regions. Export-oriented agriculture and mechanized value chains further stimulate need for advanced tractor capabilities. OEMs are investing in product diversification to capture this emerging demand tier. Transition toward higher horsepower segments therefore represents a major structural opportunity for value growth in India’s tractor market.

Integration of Precision Agriculture and Smart Tractor Technologies

The India Tractor market can expand through integration of digital technologies including GPS guidance, telematics, and smart implement control systems that enhance operational efficiency and data-driven farming. Precision agriculture adoption increases demand for tractors capable of supporting automated steering, variable rate application, and field mapping functions. Smart tractors enable optimized input usage, reduced fuel consumption, and improved productivity, delivering measurable economic benefits to farmers. Digital connectivity also supports remote diagnostics, predictive maintenance, and fleet management for commercial farming operations. Government and agri-tech initiatives promoting digital agriculture create enabling environments for technology-enabled tractor adoption. Large farmers and service providers increasingly prefer tractors with integrated smart capabilities. OEMs differentiate products through technology features, creating premium segments within the market. As digital farming ecosystems expand, tractors become central platforms for integrated agricultural technology deployment.

Future Outlook

The India Tractor market is expected to expand steadily over the next five years supported by mechanization growth, rural financing penetration, and adoption of higher horsepower models. Technological integration including precision guidance and smart tractor features will enhance productivity and value proposition. Government mechanization incentives and agricultural modernization policies will sustain demand. Expansion into emerging mechanization regions will broaden the market base. Replacement demand from aging fleets will provide consistent volume support.

Major Players

- Mahindra & Mahindra Farm Equipment

- TAFE

- Escorts Kubota

- Sonalika International

- John Deere India

- CNH Industrial India

- Kubota Agricultural Machinery India

- Yanmar Agricultural Equipment India

- VST Tillers Tractors

- Preet Tractors

- Indo Farm Equipment

- Captain Tractors

- Force Motors Agri Division

- New Holland Agriculture India

- Same Deutz Fahr India

Key Target Audience

- Agricultural equipment manufacturers

- Tractor dealerships and distributors

- Rural mechanization service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural cooperatives

- Farm equipment financing companies

- Component manufacturing companies

Research Methodology

Step 1: Identification of Key Variables

Key variables including tractor population, horsepower mix, regional demand distribution, and pricing trends were identified through agricultural mechanization statistics and industry production data. Adoption drivers such as financing penetration and mechanization policies were mapped to structure market analysis.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using tractor sales volumes, average selling prices, and horsepower category distribution across regions. Product type shares and regional clusters were derived from OEM and industry datasets.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding demand drivers, regional dominance, and technology adoption were validated through consultation with tractor manufacturers, dealers, and agricultural mechanization experts. Findings were cross-checked with institutional studies and industry insights.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, competitive landscape, and growth dynamics. Consistency checks ensured alignment with mechanization and agricultural productivity trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising agricultural mechanization intensity across diverse crop systems

Government subsidy programs supporting tractor ownership and replacement

Expansion of rural credit and farm financing access - Market Challenges

Fragmented landholdings limiting high horsepower tractor adoption

Seasonal income variability affecting equipment purchasing capacity

Dependence on monsoon impacting farm investment cycles - Market Opportunities

Electrification and autonomous tractor technology integration

Export potential for cost-competitive Indian tractor platforms

Mechanization service models expanding tractor utilization - Trends

Shift toward higher horsepower tractors in commercial agriculture

Integration of precision farming technologies in tractors

Growth of rental and custom hiring tractor services - Government regulations

Agricultural mechanization subsidy schemes

Emission standards for agricultural tractors

Rural financing and credit support policies - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compact Tractors

Utility Tractors

Row Crop Tractors

Orchard and Vineyard Tractors

High Horsepower Tractors - By Platform Type (In Value%)

Two-Wheel Drive Tractors

Four-Wheel Drive Tractors

Tracked Tractors

Autonomous Ready Platforms

Electric Tractor Platforms - By Fitment Type (In Value%)

Open Station Tractors

Cabin Enclosed Tractors

ROPS Equipped Tractors

Precision Farming Equipped Tractors

Specialty Application Tractors - By End User Segment (In Value%)

Smallholder Farmers

Medium Landholding Farmers

Large Commercial Farms

Agricultural Cooperatives

Farm Mechanization Service Providers - By Procurement Channel (In Value%)

Direct OEM Dealers

Regional Distributors

Rural Retail Networks

- Market Share Analysis

- Cross Comparison Parameters (Horsepower Range, Drive Type, Transmission Type, Emission Compliance Level, Precision Farming Integration, Electrification Readiness, Autonomous Capability Level, Hydraulic Lift Capacity, Fuel Efficiency, Distribution Network Strength)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Mahindra & Mahindra Farm Equipment

Tractors and Farm Equipment Limited

Escorts Kubota

Sonalika International Tractors

John Deere India

CNH Industrial India

Kubota Agricultural Machinery India

Yanmar Agricultural Equipment India

SDF India

VST Tillers Tractors

Captain Tractors

Preet Tractors

Force Motors Agri Division

Indo Farm Equipment

ACE Tractors

- Smallholder farmers prioritizing affordable low horsepower tractors

- Commercial farms adopting high horsepower and precision tractors

- Mechanization service providers driving fleet purchases

- Cooperatives enabling shared tractor ownership models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now