Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India truck aggregator market reached approximately USD ~ billion based on a recent historical assessment, reflecting rapid digitalization of freight brokerage and trucking operations nationwide. Growth is driven by rising intercity freight demand, expansion of e-commerce logistics volumes, and increased adoption of digital load-matching platforms among small fleet owners. Government logistics efficiency programs and telematics integration have further accelerated platform penetration, improving asset utilization and reducing empty return trips across long-haul trucking networks.

Delhi NCR, Mumbai Metropolitan Region, Bengaluru, and Ahmedabad dominate India truck aggregator market activity due to high industrial output, dense freight corridors, and strong presence of organized logistics operators. These cities host major manufacturing clusters, ports, and distribution hubs, enabling consistent freight demand and platform liquidity. Western and southern freight corridors show strong aggregator adoption because of developed highways, higher digital literacy among fleet operators, and concentration of e-commerce fulfillment infrastructure and third-party logistics providers.

Market Segmentation

By Service Type

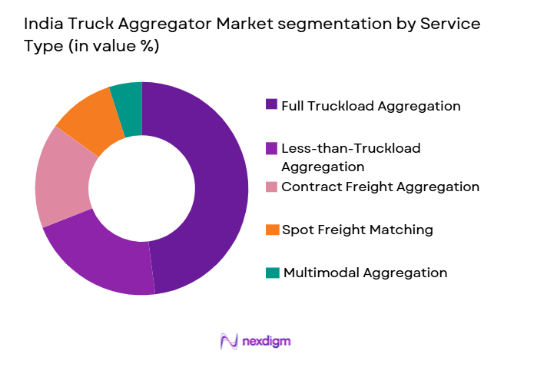

India truck aggregator market is segmented by service type into full truckload aggregation, less-than-truckload aggregation, contract freight aggregation, spot freight matching, and multimodal aggregation. Recently, full truckload aggregation has a dominant market share due to high intercity long-haul freight volumes, simpler matching requirements, and strong participation from small fleet owners seeking assured utilization. Industrial freight patterns favor dedicated truck capacity for manufacturing, FMCG, and e-commerce shipments, enabling aggregators to scale full truckload offerings faster than fragmented consolidation-based models.

By End-user

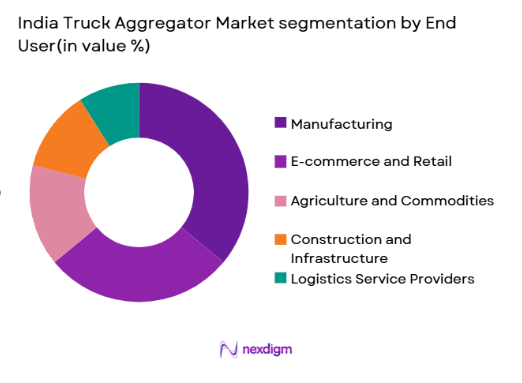

India truck aggregator market is segmented by end-user industry into manufacturing, e-commerce and retail, agriculture and commodities, construction and infrastructure, and logistics service providers. Recently, manufacturing has a dominant market share due to continuous outbound freight flows, predictable shipment schedules, and strong corridor concentration across industrial belts. Aggregators benefit from recurring factory dispatches, enabling platform stickiness and higher transaction volumes compared with seasonal agricultural flows or project-based construction logistics demand patterns.

Competitive Landscape

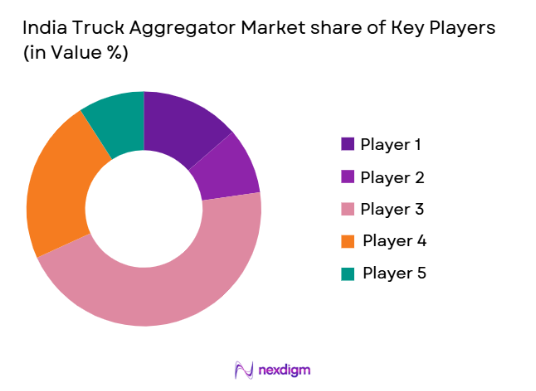

India truck aggregator market shows moderate consolidation with a few large digital freight platforms controlling nationwide shipper and carrier networks while numerous regional aggregators operate corridor-specific marketplaces. Major players influence pricing transparency, technology standards, and digital onboarding of truck owners. Competitive intensity centers on fleet coverage, real-time tracking capability, enterprise shipper integration, and value-added services such as financing and fuel management, creating barriers for new entrants lacking capital and network density.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Network Scale |

| BlackBuck | 2015 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| Rivigo | 2014 | Gurugram | ~ | ~ | ~ | ~ | ~ |

| Delhivery | 2011 | Gurugram | ~ | ~ | ~ | ~ | ~ |

| LetsTransport | 2015 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| Porter | 2014 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

India Truck Aggregator Market Analysis

Growth Drivers

Digitalization of Fragmented Trucking Supply:

India truck aggregator market expansion is strongly supported by the structural digitalization of a highly fragmented trucking ecosystem dominated by small fleet owners and single-truck operators. Aggregator platforms enable these operators to access nationwide freight demand through mobile applications, eliminating dependence on local brokers and reducing idle time. Digital load matching improves vehicle utilization by connecting trucks to return loads across corridors, directly increasing operator earnings and platform transaction volumes. Shippers benefit from transparent pricing and real-time tracking, encouraging migration from traditional brokerage channels. Telematics integration allows aggregators to monitor fleet movement and predict availability, further enhancing matching efficiency. Government policies promoting digital logistics documentation and e-way bill integration have accelerated adoption of platform-based freight booking. Financial services such as fuel cards and working capital loans tied to platform usage increase carrier retention and network depth. As more operators digitize operations, network effects strengthen aggregator dominance and market growth.

E-commerce and Organized Logistics Expansion:

Rapid expansion of e-commerce fulfillment networks and organized supply chains across India has significantly increased demand for reliable intercity trucking capacity accessible through digital platforms. Online retail requires predictable line-haul movement between warehouses, fulfillment centers, and regional hubs, creating recurring freight demand suited to aggregator matching systems. Aggregators provide scalable capacity without requiring asset ownership, allowing e-commerce firms to manage peak season fluctuations efficiently. Growth of third-party logistics providers has further amplified platform usage because these operators rely on flexible subcontracted trucking rather than owned fleets. Manufacturing supply chains adopting just-in-time inventory also prefer digital freight procurement for scheduling visibility and service reliability. Urbanization and rising consumption have increased freight flows between production and consumption centers, expanding aggregator addressable corridors. Integration of enterprise resource planning systems with aggregator platforms has automated shipment booking and tracking processes. These structural logistics shifts continue to drive sustained growth of digital truck aggregation.

Market Challenges

Low Digital Literacy Among Small Fleet Operators:

India truck aggregator market faces persistent constraints due to limited digital literacy and technology familiarity among a large portion of small fleet owners and drivers. Many operators remain dependent on traditional broker relationships and cash-based transactions, slowing onboarding to digital platforms. Language barriers, smartphone usability issues, and limited understanding of app-based workflows reduce adoption efficiency, particularly in rural and semi-urban regions. Aggregators must invest heavily in training, local support teams, and assisted onboarding to expand carrier networks. Resistance to transparent pricing models also persists among operators accustomed to negotiated brokerage rates. Connectivity limitations along certain freight corridors affect consistent platform usage and real-time tracking reliability. Payment digitization concerns, including delayed settlements or banking access constraints, further discourage participation among small carriers. As long as a substantial portion of the trucking base remains digitally excluded, aggregator platforms face slower network expansion and operational inefficiencies in nationwide coverage.

Freight Rate Volatility and Thin Margins:

India truck aggregator market participants operate within a freight pricing environment characterized by fuel cost fluctuations, seasonal demand cycles, and intense competition among carriers. Aggregators must balance shipper expectations for low rates with carrier profitability requirements, often compressing platform margins. Sudden diesel price changes directly alter freight rates, forcing frequent repricing and reducing contract stability. Seasonal peaks such as agricultural harvests or festive consumption create temporary capacity shortages followed by off-season oversupply, complicating dynamic pricing strategies. Competitive discounting among aggregators to acquire shippers further pressures margins and sustainability. High customer acquisition costs and incentives for carrier retention increase operating expenses. Infrastructure disruptions or regulatory changes across states can also shift corridor economics unpredictably. Maintaining profitability while ensuring network liquidity remains a core challenge for aggregators operating in a price-sensitive and highly competitive trucking market environment.

Opportunities

Integrated Digital Logistics Ecosystem Services:

India truck aggregator market has significant opportunity to expand beyond load matching into integrated digital logistics ecosystems combining freight, finance, fuel, and fleet management services. Aggregators already possess transaction data and carrier relationships enabling embedded financial products such as invoice discounting, insurance, and fuel credit. Providing these services increases platform stickiness and generates diversified revenue streams beyond brokerage fees. Shippers benefit from unified logistics procurement and payment systems, improving operational efficiency and reducing administrative complexity. Integration with warehouse booking, multimodal transport, and last-mile delivery can transform aggregators into end-to-end logistics orchestrators. Data analytics capabilities allow predictive demand forecasting and route optimization services for enterprise clients. As logistics digitization deepens, platforms offering comprehensive logistics operating systems can capture higher value across supply chains. This ecosystem approach positions aggregators as strategic infrastructure rather than transactional marketplaces, unlocking long-term growth potential and market leadership advantages.

Expansion into Multimodal and Cross-border Freight:

India truck aggregator market can expand significantly by integrating multimodal logistics including rail, coastal shipping, and cross-border road freight into existing digital platforms. National infrastructure initiatives promoting dedicated freight corridors and multimodal logistics parks create opportunities for aggregators to orchestrate intermodal transport combinations. Export-oriented manufacturers require seamless movement from inland factories to ports, a process aggregators can digitize through unified booking and tracking systems. Cross-border trade with neighboring South Asian countries presents additional digital freight matching potential where trucking remains dominant. Aggregators capable of coordinating customs documentation, border clearance scheduling, and corridor capacity can capture new logistics flows. Multimodal integration reduces dependence on long-haul trucking alone, diversifying revenue and stabilizing demand cycles. As supply chains globalize and infrastructure connectivity improves, digital aggregators positioned across transport modes can scale beyond domestic trucking into regional logistics platforms with higher transaction volumes and strategic importance.

Future Outlook

India truck aggregator market is expected to expand steadily over the next five years as logistics digitization accelerates across freight corridors and supply chains. Increasing enterprise adoption of digital freight procurement and telematics-enabled fleet visibility will deepen platform penetration nationwide. Government logistics infrastructure programs and multimodal integration initiatives will broaden aggregator service scope. Growing e-commerce and manufacturing distribution networks will sustain freight demand. Technology convergence with financing, analytics, and multimodal orchestration will shape competitive evolution of digital freight platforms.

Major Players

- BlackBuck

- Rivigo

- Delhivery

- LetsTransport

- Porter

- TruckSuvidha

- FreightTiger

- Vahak

- TrucksUp

- LocoNav

- ElasticRun

- TruckGuru

- Cogoport

- Gati

- Ecom Express

Key Target Audience

- Truck aggregator platform operators

- Third-partylogistics providers

- E-commerce logistics companies

- Manufacturing enterprises with freight operations

- Fleet management and telematics providers

- Automotive and commercial vehicle OEMs

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Market structure, digital freight penetration, fleet digitization levels, and logistics demand indicators were identified through secondary research and industry databases. Key performance metrics included platform transaction volumes, carrier network size, and corridor coverage across India trucking routes.

Step 2: Market Analysis and Construction

Supply and demand mapping across freight corridors was conducted using logistics flow data and platform adoption trends. Market sizing incorporated digital brokerage revenue, transaction fees, and value-added service income derived from truck aggregation activities nationwide.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics operators, fleet owners, and digital freight platform executives validated adoption drivers and constraints. Carrier onboarding patterns, pricing dynamics, and technology usage assumptions were cross-checked against operational insights and market behavior observations.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative findings were synthesized to construct market segmentation, competitive landscape, and growth projections. Analytical models integrated logistics demand indicators, digital adoption rates, and platform scaling factors to produce consistent market outlook conclusions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of digital freight marketplaces in organized logistics

Rising e-commerce freight volumes across intercity corridors

Adoption of telematics and fleet digitization by truck owners

Government push for logistics efficiency and cost reduction

Increasing SME participation in digital freight platforms - Market Challenges

Fragmented trucking ownership structure in India

Low digital literacy among small fleet operators

Freight rate volatility and pricing transparency issues

Infrastructure bottlenecks in rural logistics corridors

Regulatory compliance variability across states - Market Opportunities

Integration of multimodal freight aggregation capabilities

Fintech-enabled freight payments and credit services

Cross-border South Asia digital freight corridors - Trends

Shift toward AI-driven dynamic freight pricing engines

Growth of app-first booking among small shippers

Integration of fleet telematics with aggregator platforms

Rise of contract freight digitization for enterprises

Platform consolidation through mergers and acquisitions - Government Regulations & Defense Policy

National Logistics Policy digitalization initiatives

E-way bill and FASTag data integration frameworks

State-level freight and transport compliance digitization - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Full Truckload Aggregation Platforms

Less Than Truckload Matching Platforms

On-demand Spot Freight Platforms

Contract Freight Aggregation Systems

Multimodal Freight Aggregators - By Platform Type (In Value%)

Mobile App-based Platforms

Web-based Freight Marketplaces

API-integrated Enterprise Platforms

Cloud-native Logistics Platforms

AI-enabled Dispatch Platforms - By Fitment Type (In Value%)

Shipper-integrated Solutions

Carrier-integrated Solutions

Broker-integrated Platforms

Third-party Logistics Integrated Systems

Standalone Aggregator Platforms - By EndUser Segment (In Value%)

Manufacturing Enterprises

E-commerce and Retail Companies

Logistics Service Providers

SME Shippers and Traders

Agriculture and Commodity Firms - By Procurement Channel (In Value%)

Direct Platform Subscription

Freight Brokerage Partnerships

Enterprise Contract Procurement

Digital Freight Exchanges

Third-party Logistics Bundling - By Material / Technology (in Value %)

AI-based Load Matching Algorithms

Telematics and GPS Tracking Integration

Blockchain-enabled Freight Contracts

IoT-enabled Fleet Monitoring

Data Analytics and Route Optimization Engines

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Fleet Size Coverage, Geographic Reach, Load Matching Efficiency, Pricing Transparency, Technology Integration Level, Carrier Network Strength, Enterprise Client Base, Multimodal Capability, Value-added Services, Data Analytics Capability)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

BlackBuck

Rivigo

Delhivery

LetsTransport

TruckSuvidha

FreightTiger

Vahak

TrucksUp

LocoNav

ElasticRun

TruckGuru

Cogoport

Gati

Ecom Express

Porter

- Manufacturers increasingly digitizing primary freight procurement

- E-commerce firms prioritizing real-time capacity visibility

- SME shippers adopting aggregators for cost optimization

- 3PL providers integrating aggregator platforms for scale

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now