Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Used Tractor market current size stands at around USD ~ million, reflecting steady transactional momentum driven by replacement cycles and affordability-led demand across agricultural and allied uses. The ecosystem spans refurbishment hubs, dealer networks, digital classifieds, and financing partners, enabling circulation of pre-owned equipment. Transaction liquidity is supported by inspection protocols, warranty-backed resale programs, and growing acceptance of graded quality. Value retention dynamics, seasonal utilization, and resale turnover cycles shape pricing corridors and inventory depth across rural and peri-urban trade routes.

Demand concentrates across agrarian belts with dense dealer clusters and logistics corridors, supported by implement compatibility and service availability. Northern and western states show strong throughput due to diversified cropping systems and haulage usage, while southern clusters benefit from mechanization maturity and contractor networks. Market activity aligns with mandi access, warehousing density, and road connectivity, with institutional financing and transfer formalities influencing channel choice. Policy emphasis on mechanization, digitized registration, and rural credit deepens ecosystem maturity in multi-crop districts.

Market Segmentation

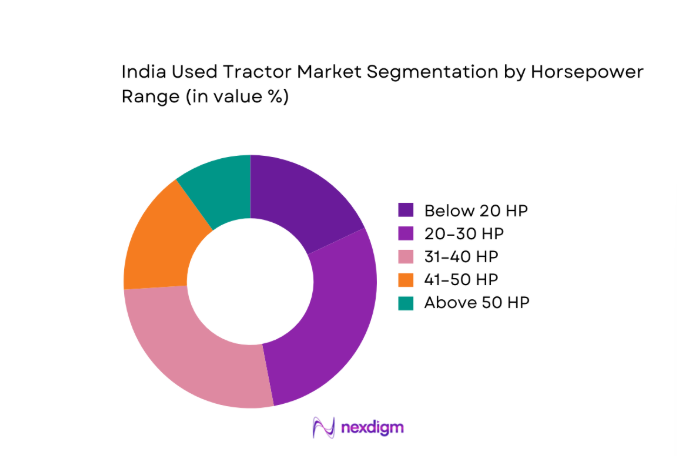

By Horsepower Range

Demand concentrates in mid-range horsepower as buyers seek versatility for tillage, haulage, and PTO-driven implements while managing acquisition risk in pre-owned purchases. This band balances fuel efficiency, parts availability, and service familiarity, improving resale confidence and downtime predictability. Lower horsepower retains relevance for small plots and inter-row tasks, while higher horsepower gains traction in transport-linked applications and contractor fleets. Refurbishment programs favor common engine platforms, improving parts pooling and turnaround time. Financing partners prefer standardized horsepower bands due to predictable utilization cycles, resale liquidity, and maintenance histories, reinforcing dominance of mid-range units across multi-crop districts with mixed duty cycles.

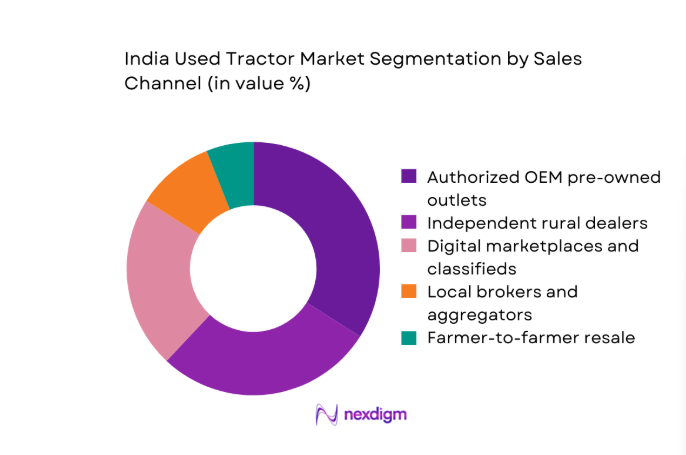

By Sales Channel

Authorized pre-owned outlets and organized dealers increasingly dominate due to standardized grading, warranty assurance, and financing tie-ups that reduce buyer risk. Digital marketplaces expand discovery and price transparency, shortening transaction cycles and widening catchment across districts. Independent rural dealers remain relevant for hyperlocal sourcing and rapid turnover but face quality signaling constraints. Broker-led trades persist for legacy inventory, yet institutional channels benefit from documented service histories and refurbishment protocols. Channel dominance aligns with transfer facilitation, inventory depth during peak seasons, and bundled offerings such as insurance and annual maintenance, improving buyer confidence and repeat transactions.

Competitive Landscape

The competitive environment features organized pre-owned programs alongside independent dealer networks and digital intermediaries, differentiated by refurbishment depth, documentation rigor, financing partnerships, and service reach. Channel strength and regulatory readiness increasingly shape buyer trust and repeat purchase behavior across districts.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Mahindra First Choice Wheels | 2008 | Mumbai | ~ | ~ | ~ | ~ | ~ | ~ |

| Tafe Access | 2017 | Chennai | ~ | ~ | ~ | ~ | ~ | ~ |

| Escorts Kubota Pre-Owned | 2022 | Faridabad | ~ | ~ | ~ | ~ | ~ | ~ |

| Sonalika Tiger Pre-Owned | 2019 | Hoshiarpur | ~ | ~ | ~ | ~ | ~ | ~ |

| Tractor Junction Used | 2018 | Jaipur | ~ | ~ | ~ | ~ | ~ | ~ |

India Used Tractor Market Analysis

Growth Drivers

High new tractor prices driving downtrading to used units

Elevated capital thresholds in new equipment purchases are steering buyers toward pre-owned alternatives as input costs and credit scrutiny tighten. In 2024, policy lending rates averaged 6.5, while rural bank branch density improved to 14 per 100000 residents, expanding access to formal credit for refurbished assets. Registration transfers processed through digitized portals reached 220000 in 2025, shortening transaction timelines. Average tractor service life extended beyond 9000 operating hours with standardized refurbishment protocols adopted by organized channels, reducing perceived risk. District road connectivity improved by 3100 kilometers in 2024, lowering logistics friction for inter-district sourcing and supporting broader availability.

Expanding custom hiring centers increasing demand for affordable fleets

Custom hiring centers expanded fleet utilization as peak-season access constraints persisted across multi-crop districts. In 2025, documented center registrations increased to 11800, with average fleet sizes rising to 7 units per center, favoring refurbished acquisitions to manage capex exposure. Government-backed equipment pools added 4200 tractors in 2024, emphasizing availability over ownership. Seasonal utilization averaged 210 operating days in irrigated belts, supporting predictable maintenance cycles. Financing approvals for pre-owned equipment shortened to 12 days through NBFC digitization in 2025, improving procurement velocity and enabling rapid fleet refresh without prolonged downtime.

Challenges

Fragmented dealer network with inconsistent quality grading

Quality inconsistency persists across fragmented dealer ecosystems, undermining buyer confidence and resale liquidity. In 2024, inspection coverage reached only 38 percent of transacted units within organized channels, leaving large volumes ungraded. Complaint filings related to documentation errors recorded 14600 cases in 2025 through state transport portals, extending transfer cycles beyond 21 days in several districts. Parts standardization remains uneven, with 4600 SKU variants circulating across common engine platforms, complicating refurbishment turnarounds. Service technician density averaged 1 per 5200 rural vehicles in 2024, constraining post-purchase reliability assurances across dispersed markets.

Information asymmetry on tractor condition and service history

Opaque service histories impede price discovery and elevate post-purchase risk. In 2024, only 41 percent of listings carried verifiable maintenance records, while telematics penetration across legacy fleets remained limited to 9 percent of units retrofitted. Average inter-owner documentation gaps spanned 3 custodial transfers, diluting traceability. District-level registration databases recorded 87000 ownership corrections in 2025, reflecting legacy record fragmentation. Average inspection lead times stretched to 9 days during peak seasons, delaying transactions. Limited standardized grading scales across channels perpetuate valuation dispersion and buyer hesitation, suppressing velocity in secondary markets.

Opportunities

Expansion of OEM-certified pre-owned programs into tier 3–4 towns

Extending certified programs into tier 3–4 towns can formalize fragmented trade and unlock latent demand. In 2025, organized outlets covered 312 towns, leaving 1280 underserved service centers within 50 kilometers of high-activity mandis. Mobile refurbishment units piloted in 2024 processed 180 units per month, reducing turnaround time by 4 days versus depot-based workflows. Digitized transfer kiosks cut documentation queues to 2 visits per transaction. Partner financing branches increased to 640 locations in 2025, improving approvals. Standardized warranty coverage of 180 days boosts buyer confidence and accelerates repeat purchases.

Digital marketplaces enabling price discovery and wider reach

Digital platforms can compress discovery cycles and improve cross-district liquidity. In 2024, verified listings increased to 265000 with average listing-to-sale cycles falling to 17 days where inspections were integrated. App-based scheduling enabled 42000 on-site inspections in 2025, reducing buyer travel by 28 kilometers per transaction. Integration with state transport APIs cut ownership transfer errors by 1900 cases annually. AI-assisted grading pilots processed 12000 images monthly, improving condition scoring consistency. Embedded financing workflows shortened approvals to 9 days, supporting faster turnover and inventory optimization across seasonal demand spikes.

Future Outlook

The market is set to formalize further through certified pre-owned expansion, deeper financing integration, and digital inspection workflows. Regional logistics improvements and digitized transfers will compress transaction cycles. OEM-led refurbishment standards and warranty adoption will elevate trust. Channel consolidation is likely as organized platforms extend reach into underserved districts. Policy continuity around mechanization and rural credit should sustain transactional momentum through the next decade.

Major Players

- Mahindra First Choice Wheels

- Tafe Access

- Escorts Kubota Pre-Owned

- Sonalika Tiger Pre-Owned

- Tractor Junction Used

- KhetiGaadi Used

- OLX Autos India

- CarDekho Tractor Exchange

- AgriBazaar Pre-Owned

- Krishi Network Marketplace

- Farm Machinery Solutions India

- Rudra Tractors and Farm Equipment

- Kisaan Tractor Bazaar

- CNH Industrial Pre-Owned India

- John Deere India Used Equipment Program

Key Target Audience

- Smallholder and marginal farmers

- Medium and large commercial farmers

- Custom hiring centers and farm contractors

- Rural logistics and haulage operators

- Equipment refurbishers and dealer networks

- Non-banking financial companies and rural lenders

- Investments and venture capital firms

- Government and regulatory bodies with agency names including Ministry of Agriculture and Farmers Welfare and state transport departments

Research Methodology

Step 1: Identification of Key Variables

Core variables included fleet age, operating hours, refurbishment depth, documentation completeness, financing access, and channel reliability. District-level infrastructure indicators and service density were mapped to transaction velocity. Policy enablers affecting transfers and warranties were prioritized to frame demand elasticity and channel adoption patterns.

Step 2: Market Analysis and Construction

Transaction flows were structured by channel, geography, and horsepower bands to build supply-demand linkages. Seasonal utilization cycles and logistics access were overlaid to explain liquidity. Refurbishment throughput and inspection capacity informed availability constraints across districts.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on buyer risk tolerance, warranty influence, and financing turnaround were tested through practitioner workshops. Transfer bottlenecks and service coverage gaps were stress-tested against institutional indicators. Iterative reviews refined channel dominance and refurbishment scalability hypotheses.

Step 4: Research Synthesis and Final Output

Insights were synthesized into actionable themes linking policy, infrastructure, and channel evolution. Findings were cross-checked for internal consistency across districts and use cases. Outputs emphasized operational levers for formalization, trust-building, and digital acceleration.

- Executive Summary

- Research Methodology (Market Definitions and used tractor lifecycle mapping, Dealer auction and rural mandis price tracking, OEM certified pre-owned program audits, Primary interviews with dealers financiers and FPOs, Telematics and service history data triangulation, State-wise registration and ownership transfer analysis)

- Definition and Scope

- Market evolution

- Usage and refurbishment pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

High new tractor prices driving downtrading to used units

Expanding custom hiring centers increasing demand for affordable fleets

Rural credit penetration and NBFC financing for pre-owned tractors

Rising mechanization among small and marginal farmers

Growing secondary markets in non-agricultural haulage uses

Increased OEM-backed refurbishment programs improving trust - Challenges

Fragmented dealer network with inconsistent quality grading

Information asymmetry on tractor condition and service history

Limited availability of formal financing in remote districts

Price volatility linked to monsoon and crop realizations

Low penetration of standardized warranties and return policies

Regulatory frictions in inter-state ownership transfer - Opportunities

Expansion of OEM-certified pre-owned programs into tier 3–4 towns

Digital marketplaces enabling price discovery and wider reach

Structured refurbishment hubs to extend tractor life cycles

Bundled financing insurance and AMC offerings

Export of used tractors to neighboring emerging markets

Formalization of aggregator-led rural distribution networks - Trends

Growth of online listings and app-based dealer networks

Rising demand for higher HP used tractors for haulage

Increased acceptance of warranty-backed refurbished units

Use of telematics and service records in valuation

Seasonal inventory stocking aligned with crop cycles

Partnerships between OEMs and NBFCs for pre-owned financing - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Horsepower Range (in Value %)

Below 20 HP

20–30 HP

31–40 HP

41–50 HP

Above 50 HP - By Application (in Value %)

Ploughing and tillage

Sowing and planting

Harvesting support

Haulage and transport

PTO-driven implements - By Age of Tractor (in Value %)

Below 3 years

3–5 years

6–8 years

Above 8 years - By Sales Channel (in Value %)

Authorized OEM pre-owned outlets

Independent rural dealers

Digital marketplaces and classifieds

Local brokers and aggregators

Farmer-to-farmer resale - By End User (in Value %)

Smallholder farmers

Medium and large farmers

Custom hiring centers

Contractors and logistics operators

Rural enterprises and cooperatives - By Geography (in Value %)

North India

West India

South India

East India

Central India

North East India

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (dealer network reach, refurbishment standards, warranty coverage, financing tie-ups, digital platform capabilities, inventory depth, price competitiveness, aftersales service coverage)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Mahindra First Choice Wheels

Tafe Access

John Deere India Used Equipment Program

Escorts Kubota Pre-Owned

CNH Industrial Pre-Owned India

Sonalika Tiger Pre-Owned

Kisaan Tractor Bazaar

Tractor Junction Used

OLX Autos India

CarDekho Tractor Exchange

Krishi Network Marketplace

AgriBazaar Pre-Owned

KhetiGaadi Used Tractor

Farm Machinery Solutions India

Rudra Tractors and Farm Equipment

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now