Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India warehousing aggregator market reached approximately USD ~ billion based on a recent historical assessment, driven by accelerated demand for flexible storage capacity and digital warehouse discovery platforms across supply chains. Rapid e-commerce expansion and omnichannel distribution have increased short-term storage leasing requirements, while organized logistics adoption and GST-enabled consolidation expanded multi-location inventory networks. Industry estimates from logistics associations and corporate disclosures indicate aggregator-enabled warehousing transactions surpassed USD ~ billion in value during the period.

Major logistics corridors such as Delhi NCR, Mumbai Metropolitan Region, Bengaluru, and Chennai dominate the India warehousing aggregator market due to concentration of Grade A warehousing clusters, multimodal connectivity, and dense consumption bases. These regions collectively host warehousing stock exceeding 250 million square feet across organized facilities, attracting aggregators to integrate supply. Western and southern industrial belts also lead due to port proximity, manufacturing density, and established third-party logistics ecosystems enabling platform scalability.

Market Segmentation

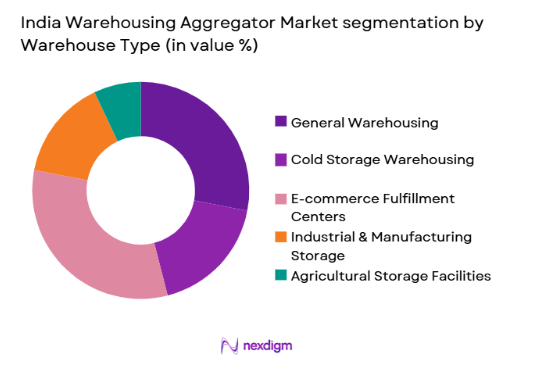

By Warehouse Type

India Warehousing Aggregator market is segmented by warehouse type into general warehousing, cold storage warehousing, e-commerce fulfillment centers, industrial and manufacturing storage, and agricultural storage facilities. Recently, e-commerce fulfillment centers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Rapid growth in online retail volumes and quick-commerce delivery models increased demand for distributed fulfillment nodes integrated into aggregator platforms. These facilities require standardized layouts, technology integration, and flexible leasing durations, making them ideal for aggregation. Additionally, major retailers and marketplaces prefer multi-client fulfillment hubs to optimize last-mile efficiency, further strengthening this segment’s dominance in aggregator networks.

By End-use

India Warehousing Aggregator market is segmented by end-use into e-commerce and retail, FMCG, pharmaceuticals and healthcare, manufacturing and industrial, and agriculture and food. Recently, e-commerce and retail has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Digital commerce players increasingly depend on asset-light warehousing models offered by aggregators to expand geographic reach without capital investment. High SKU variety and seasonal demand variability require scalable storage footprints, which aggregation platforms efficiently provide. The need for rapid order processing and distributed inventory placement across consumption centers further elevates the segment’s share within aggregated warehousing transactions.

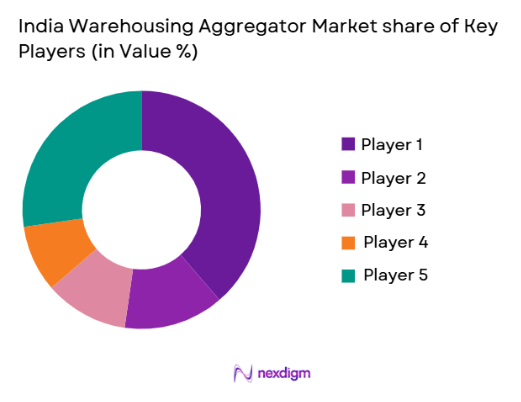

Competitive Landscape

The India warehousing aggregator market remains moderately fragmented with technology-led logistics platforms and digital freight networks expanding into storage aggregation. Major integrated logistics firms leverage nationwide warehouse partnerships and technology stacks to scale, while specialized startups focus on cold chain or e-commerce fulfillment aggregation. Consolidation is emerging through acquisitions and partnerships with Grade A warehouse developers, enabling platforms to secure capacity and enterprise clients.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Warehouse Network Scale |

| Delhivery | 2011 | Gurugram | ~ | ~ | ~ | ~ | ~ |

| BlackBuck | 2015 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| Rivigo | 2014 | Gurugram | ~ | ~ | ~ | ~ | ~ |

| ElasticRun | 2016 | Pune | ~ | ~ | ~ | ~ | ~ |

| Mahindra Logistics | 2007 | Mumbai | ~ | ~ | ~ | ~ | ~ |

India Warehousing Aggregator Market Analysis

Growth Drivers

E-commerce-led demand for distributed fulfillment infrastructure:

The explosive expansion of digital commerce across metropolitan and non-metro regions has fundamentally transformed storage requirements, creating sustained demand for flexible, distributed warehousing capacity accessible through aggregator platforms. Online marketplaces, direct-to-consumer brands, and omnichannel retailers increasingly maintain multi-node inventory networks to ensure rapid delivery commitments and localized stock availability. Aggregators enable this distributed model by connecting enterprises with ready warehouse capacity across cities without long-term leases or capital investment. The proliferation of quick-commerce and same-day delivery formats further accelerates micro-fulfillment adoption, which aggregators facilitate through short-term space matching and technology-enabled inventory visibility. Retailers also rely on aggregators to handle seasonal peaks, promotional surges, and geographic demand variability. As SKU diversity and order fragmentation grow, enterprises prioritize scalable storage ecosystems rather than centralized mega-warehouses. Consequently, aggregator platforms become essential intermediaries linking warehouse supply with dynamic e-commerce demand, driving sustained market expansion.

Formalization and digitization of India’s warehousing ecosystem

: Structural reforms in taxation and logistics policy have accelerated the transition from fragmented, informal storage networks toward organized, technology-integrated warehousing, creating favorable conditions for aggregation platforms. Standardized compliance requirements and quality certifications encourage warehouse operators to integrate into digital marketplaces to access enterprise demand. Aggregators provide technology layers such as warehouse management integration, inventory tracking, and booking interfaces that formalize previously unstructured capacity. Institutional investors and developers are also expanding Grade A warehousing stock, which aggregators onboard to increase supply depth. Enterprises increasingly prefer digitally discoverable, compliant facilities with transparent pricing and service metrics, reinforcing aggregator relevance. The broader logistics digitization trend, including transport management integration and supply-chain analytics, further embeds aggregation platforms into enterprise operations. This ecosystem transformation elevates aggregator adoption across industries and regions.

Market Challenges

Fragmented ownership and inconsistent infrastructure quality:

India’s warehousing landscape remains highly fragmented with numerous small and medium operators offering heterogeneous facility standards, creating significant challenges for aggregation platforms attempting to ensure consistent service quality across networks. Aggregators must invest heavily in onboarding audits, compliance verification, and facility upgrades to meet enterprise expectations. Variability in ceiling height, flooring strength, fire safety systems, and automation readiness limits interoperability within aggregated networks. Enterprises often require standardized service-level agreements, which fragmented supply struggles to meet uniformly. Aggregators therefore face operational complexity in maintaining reliability across geographically dispersed partners. Additionally, limited digitization among small warehouse owners complicates real-time capacity visibility and integration. This structural fragmentation slows scalable expansion and increases platform operational costs.

Regulatory variability and state-level compliance complexities: Warehousing

operations in India are governed by diverse state regulations related to land use, labor compliance, safety standards, and taxation procedures, creating a complex environment for aggregation platforms operating nationwide networks. Aggregators must navigate differing licensing norms and inspection regimes when onboarding facilities across regions. Variability in infrastructure approvals and zoning classifications can delay warehouse integration into platforms. Enterprises seeking multi-state aggregated storage often encounter compliance inconsistencies affecting service continuity. Aggregators therefore require region-specific compliance management frameworks, increasing administrative overhead. Differences in cold chain certification and pharmaceutical storage regulations further complicate specialized aggregation segments. These regulatory complexities constrain seamless national scalability for warehousing aggregation platforms.

Opportunities

Expansion of cold chain aggregation for pharmaceuticals and perishable logistics:

Rapid growth in temperature-sensitive supply chains such as pharmaceuticals, biologics, food processing, and fresh commerce creates substantial opportunity for specialized cold chain aggregation platforms linking compliant refrigerated storage facilities across regions. Enterprises increasingly require distributed temperature-controlled nodes to maintain product integrity and regulatory compliance during storage and distribution. Aggregators can integrate certified cold storage operators into unified digital networks offering real-time monitoring and capacity matching. Rising pharmaceutical manufacturing and healthcare distribution volumes strengthen demand for compliant aggregated cold storage. Additionally, organized food retail and export supply chains require geographically distributed refrigerated hubs. Cold chain aggregation thus represents a high-value segment with strong enterprise adoption potential.

Rise of micro-fulfillment and urban warehousing aggregation:

Urban consumption density and rapid delivery expectations are driving demand for micro-fulfillment centers located within city peripheries, creating opportunities for aggregators to integrate small urban warehouses into distributed networks serving e-commerce and quick-commerce operators. Retailers and logistics providers increasingly seek short-term urban storage capacity to reduce last-mile delivery times and transportation costs. Aggregators can monetize underutilized urban industrial spaces by onboarding them into fulfillment networks. High rental costs in metropolitan zones encourage shared multi-client warehousing models facilitated by aggregation platforms. As urban logistics infrastructure evolves, micro-fulfillment aggregation enables scalable, asset-light expansion for retailers and delivery platforms.

Future Outlook

India warehousing aggregator market is expected to expand steadily as enterprises adopt flexible storage networks and digital logistics platforms. Growth will be supported by continued e-commerce penetration, organized logistics investment, and expansion of Grade A warehousing supply. Technology integration such as automation-ready facilities and AI-enabled capacity matching will strengthen platform efficiency. Policy initiatives promoting logistics infrastructure and multimodal connectivity are likely to enhance regional aggregation networks. Demand for distributed fulfillment and cold chain aggregation will remain key expansion drivers.

Major Players

- Delhivery

- BlackBuck

- Rivigo

- ElasticRun

- Mahindra Logistics

- Loadshare Networks

- Xpressbees

- Shiprocket

- LetsTransport

- Freight Tiger

- Vahak

- Porter

- FarEye

- WareIQ

- Stockarea

Key Target Audience

- E-commerce platforms

- Retail chains

- FMCG companies

- Pharmaceutical manufacturers

- Third-party logistics providers

- Real estate warehouse developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Core market variables including aggregated warehouse capacity, platform transaction value, end-use demand distribution, and regional warehousing stock were identified from industry reports, logistics associations, and corporate disclosures.

Step 2: Market Analysis and Construction

Supply and demand mapping across warehousing clusters and aggregator platforms was constructed to estimate transaction value and segment shares based on enterprise adoption patterns and facility integration levels.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through expert interviews with logistics operators, warehouse developers, and platform providers to confirm adoption drivers, constraints, and segment dominance patterns across regions.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into market sizing, segmentation, competitive landscape, and forecast outlook ensuring consistency with industry data, infrastructure trends, and enterprise logistics behavior.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid growth of e-commerce fulfillment demand across Tier I and Tier II cities

Increasing need for flexible and asset-light warehousing models

Expansion of organized logistics and supply chain digitization initiatives - Market Challenges

Fragmented warehouse ownership and quality standardization issues

Limited technology adoption among small warehouse operators

Regulatory and compliance variability across states - Market Opportunities

Expansion of cold chain aggregation for pharmaceuticals and food logistics

Growth of micro-fulfillment networks for quick commerce delivery

Integration of automation-ready Grade A warehousing supply - Trends

Shift toward multi-client shared warehousing models

Adoption of AI-driven warehouse matching and pricing algorithms

Rise of Tier II and Tier III city warehouse aggregation hubs - Government Regulations & Defense Policy

Implementation of national logistics policy and warehousing standards

GST-driven warehouse network consolidation incentives

State-level warehousing and logistics park development policies - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

On-demand Warehousing Platforms

Shared Warehouse Networks

Dedicated Contract Warehousing Platforms

Cold Chain Aggregation Platforms

Micro-fulfillment Aggregation Systems - By Platform Type (In Value%)

Web-based Aggregator Platforms

Mobile Application-based Platforms

API-integrated Logistics Platforms

Cloud-native Warehouse Marketplaces

AI-enabled Matching Platforms - By Fitment Type (In Value%)

Third-party Warehouse Integration

Owned and Managed Warehouse Integration

Partner-operated Warehouse Integration

Franchise Warehouse Integration

Hybrid Multi-operator Integration - By EndUser Segment (In Value%)

E-commerce and Retail Companies

Manufacturing and Industrial Firms

FMCG and Consumer Goods Companies

Pharmaceutical and Healthcare Firms

Agriculture and Food Processing Firms - By Procurement Channel (In Value%)

Direct Enterprise Contracts

Digital Marketplace Bookings

Logistics Service Provider Partnerships

3PL and 4PL Integrator Contracts

Government and Institutional Tenders - By Material / Technology (in Value %)

Warehouse Management Software Integration

IoT-enabled Storage Monitoring

Automation and Robotics-enabled Facilities

Temperature-controlled Storage Technology

AI-based Demand and Space Optimization

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Warehouse Network Scale, Technology Integration Depth, Geographic Coverage, Industry Specialization, Pricing Model Flexibility, Cold Chain Capability, Automation Readiness, Enterprise Client Base, Partner Ecosystem Strength, Value-added Services)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Delhivery

BlackBuck

Rivigo

ElasticRun

Shiprocket

Pickrr

TruckSuvidha

Freight Tiger

LetsTransport

Porter

Vahak

FarEye

Loadshare Networks

Xpressbees

Mahindra Logistics

- E-commerce firms increasingly rely on distributed on-demand storage networks

- Manufacturers adopt flexible warehousing to reduce fixed logistics costs

- FMCG firms use aggregation to expand regional distribution reach

- Pharma firms prioritize compliant temperature-controlled aggregated storage

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now