Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India wealth management market demonstrates substantial scale with assets under management exceeding USD ~ trillion across mutual funds, portfolio management services, and alternative investment structures, supported by rising financial savings and equity participation reported by the Reserve Bank of India and the Securities and Exchange Board of India. Expanding high-net-worth individual population above sustained capital market inflows exceeding USD ~ billion annually into managed investment products are primary growth drivers.

Mumbai and Delhi National Capital Region dominate the India wealth management market due to concentration of financial institutions, stock exchanges, and ultra-high-net-worth households with investable wealth exceeding USD 5 million per family. Bengaluru and Hyderabad also exhibit strong expansion because of technology wealth creation, startup exits exceeding USD ~ billion, and rising family office formations supported by venture liquidity and global employment income streams across multinational technology firms.

Market Segmentation

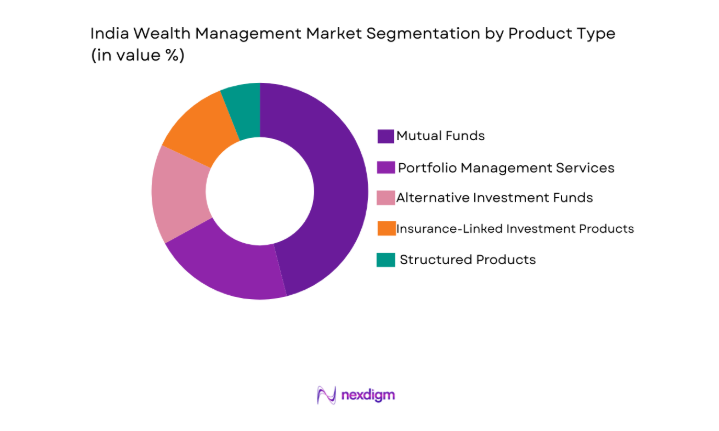

By Product Type

India wealth management market is segmented by product type into mutual funds, portfolio management services, alternative investment funds, insurance-linked investment products, and structured products. Recently, mutual funds has a dominant market share due to factors such as strong retail investor participation, extensive distributor networks, digital onboarding infrastructure, regulatory transparency under SEBI norms, tax efficiency, systematic investment plan culture, and widespread brand trust built by large asset management companies and banking distribution channels across metropolitan and tier-2 cities.

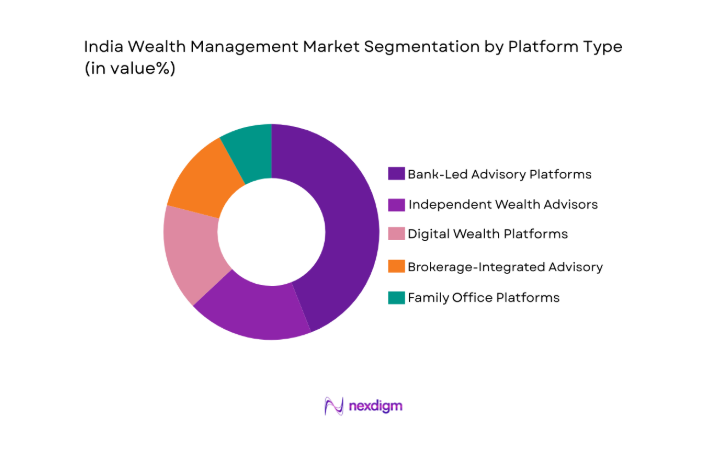

By Platform Type

India wealth management market is segmented by platform type into bank-led advisory platforms, independent wealth advisors, digital wealth platforms, brokerage-integrated advisory, and family office platforms. Recently, bank-led advisory platforms has a dominant market share due to factors such as legacy client trust, integrated financial product access, relationship-based advisory models, custody and lending integration, regulatory credibility, nationwide branch presence, and cross-selling capabilities within private banking divisions serving affluent households and corporate promoter families across financial hubs.

Competitive Landscape

India wealth management market shows moderate consolidation with large private banks and established asset managers controlling affluent and ultra-high-net-worth client assets, while independent advisors and fintech platforms expand in emerging affluent segments through digital distribution and low-cost advisory models. Global investment firms and domestic financial conglomerates influence product innovation, alternative investment access, and cross-border portfolio allocation capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Client Segment Focus |

| HDFC Asset Management | 1999 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| ICICI Prudential AMC | 1998 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| Kotak Wealth Management | 1995 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| SBI Funds Management | 1987 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| IIFL Wealth | 2008 | Mumbai | ~ | ~ | ~ | ~ | ~ |

India Wealth Management Market Analysis

Growth Drivers

Expansion of High-Net-Worth and Ultra-High-Net-Worth Population

Expansion of high-net-worth and ultra-high-net-worth population in India significantly accelerates demand for sophisticated wealth management solutions because entrepreneurial wealth creation, promoter equity monetization, technology sector compensation, and global professional income streams are increasing the pool of individuals requiring structured portfolio advisory, estate planning, and diversified asset allocation services. Rapid appreciation in listed equity valuations, startup liquidity events, and private market exits has transformed founder and executive wealth profiles, generating substantial investable surpluses that require professional management beyond traditional savings instruments. Family business succession transitions across manufacturing, real estate, and services sectors are prompting intergenerational asset restructuring, trust creation, and global diversification mandates that expand demand for institutional wealth advisory frameworks. Migration of wealthy individuals into metropolitan financial hubs is deepening client density for private banking and multi-family office platforms, enabling scale economics for advisory firms and expanding product penetration across alternatives, discretionary mandates, and offshore investments. Rising financialization of household savings supported by capital market participation and regulatory investor protection mechanisms increases trust in managed investment vehicles compared with physical assets such as gold and real estate. Increased cross-border exposure of Indian entrepreneurs and professionals generates demand for global asset allocation, tax optimization, and currency diversification services provided by integrated wealth management platforms. Institutionalization of family offices among ultra-wealthy households creates demand for governance advisory, risk management, philanthropy structuring, and private market access services that extend beyond conventional portfolio management. Continuous growth in affluent demographics therefore structurally enlarges the addressable market for wealth management providers across advisory tiers, product sophistication levels, and geographic clusters.

Digitalization and Regulatory Formalization of Investment Distribution

Digitalization and regulatory formalization of investment distribution infrastructure in India is transforming accessibility, transparency, and efficiency of wealth management services, thereby accelerating market expansion across affluent and emerging affluent investor segments who historically relied on informal or product-biased advisory channels. Regulatory frameworks introduced by securities and financial authorities standardize disclosure norms, fiduciary responsibilities, and product classification, strengthening investor confidence in managed investment vehicles and professional advisors while reducing mis-selling risk perceptions. Nationwide digital identity, electronic know-your-customer onboarding, and interoperable payment systems enable seamless account creation, portfolio execution, and monitoring through mobile platforms, significantly lowering acquisition and servicing costs for wealth managers targeting dispersed high-income clients. Data analytics and algorithmic portfolio construction tools allow scalable advisory personalization across risk profiles and financial goals, enabling hybrid advisory models that combine human relationship managers with automated portfolio allocation engines. Integration of brokerage, banking, and asset management platforms within unified digital ecosystems simplifies product access and reporting transparency, encouraging multi-product adoption including mutual funds, discretionary mandates, alternatives, and insurance-linked investments. Digital engagement channels increase investor education, behavioral nudging toward systematic investing, and long-term portfolio discipline, supporting sustained inflows into managed products. Fintech partnerships expand distribution into tier-2 and tier-3 cities where rising incomes create new affluent cohorts previously underserved by traditional private banking. Technology-enabled compliance monitoring and reporting automation also improves regulatory adherence efficiency for wealth firms, lowering operational risk and supporting industry credibility, thereby reinforcing structural growth momentum.

Market Challenges

Low Penetration of Professional Advisory Beyond Top Wealth Tiers

Low penetration of professional wealth advisory services beyond top wealth tiers remains a structural challenge in India wealth management market because a substantial proportion of financially capable households still rely on informal advisors, bank relationship managers with product bias, or self-directed investing behavior shaped by legacy preferences for physical assets and transactional trading approaches. Cultural familiarity with gold, real estate, and bank deposits reduces perceived necessity for diversified portfolio construction and long-term asset allocation planning, limiting adoption of fee-based advisory models among emerging affluent investors. Financial literacy gaps in portfolio risk management, tax efficiency, and global diversification constrain willingness to pay for professional wealth management services despite rising investable surplus among salaried professionals and business owners. Distribution economics for independent advisors remain constrained by regulatory costs, compliance requirements, and client acquisition expenses, restricting scalable penetration into mid-wealth segments outside metropolitan regions. Trust deficits arising from historical mis-selling episodes and commission-driven product distribution practices continue to influence investor skepticism toward advisory motivations and fee transparency. Fragmented client asset bases across multiple institutions complicate holistic portfolio oversight and discourage discretionary mandates that require consolidated custody and reporting frameworks. Limited awareness of estate planning, succession structuring, and intergenerational wealth transfer services among affluent families delays engagement with comprehensive wealth management offerings until late wealth stages. These structural behavioral, cultural, and economic barriers collectively restrict market depth expansion despite favorable macroeconomic wealth creation trends.

Regulatory Complexity and Product Suitability Constraints

Regulatory complexity and evolving product suitability requirements in India wealth management market create operational and strategic challenges for providers attempting to scale advisory offerings across diverse client risk profiles, asset classes, and cross-border investment channels within stringent compliance frameworks. Multiple regulatory bodies overseeing securities, insurance, pensions, and foreign investments impose layered reporting, licensing, and distribution obligations that increase compliance costs and administrative burden for wealth firms operating multi-product advisory models. Suitability assessments, disclosure norms, and risk profiling mandates require extensive documentation and monitoring processes that can slow client onboarding and portfolio implementation timelines, particularly for high-value discretionary mandates and alternative investment allocations. Restrictions on offshore investment limits, capital controls, and tax reporting obligations complicate global diversification strategies demanded by high-net-worth clients seeking geographic asset dispersion and currency risk hedging. Frequent regulatory updates in fee structures, distributor compensation, and product classification frameworks necessitate continuous technology and training investments for advisory staff and platforms to maintain compliance alignment. Complex tax treatment across investment products including capital gains categories, pass-through structures, and inheritance considerations increases advisory liability exposure and client reporting complexity. Compliance resource requirements disproportionately affect smaller independent advisors, encouraging consolidation but reducing competitive diversity in the advisory ecosystem. Regulatory scrutiny on mis-selling and conflict-of-interest practices also constrains cross-selling strategies that historically supported revenue generation, requiring transition toward transparent fee-based advisory models that may face client resistance during adoption phases.

Opportunities

Expansion of Digital Hybrid Advisory for Emerging Affluent Segments

Expansion of digital hybrid advisory models targeting emerging affluent segments in India wealth management market represents a substantial opportunity because rising professional incomes, equity participation, and financial awareness among salaried executives and entrepreneurs are generating investable surpluses that exceed traditional retail investment thresholds yet remain below private banking entry levels. Hybrid advisory combining algorithmic portfolio construction with human financial planning support enables scalable cost-efficient service delivery to clients with moderate investable assets who seek goal-based investing, tax optimization, and retirement planning solutions without high advisory fees. Mobile-first platforms leveraging behavioral analytics, automated rebalancing, and risk profiling tools enhance engagement and portfolio discipline across geographically dispersed affluent households beyond metropolitan wealth clusters. Integration with employer compensation platforms, stock option management tools, and retirement savings vehicles enables embedded wealth management services aligned with professional income structures common in technology and corporate sectors. Digital onboarding, fractional investment access, and low-minimum alternative exposure democratize sophisticated portfolio strategies previously restricted to ultra-wealthy clients, expanding product penetration across mass affluent tiers. Data-driven personalization and lifecycle advisory models create long-term client relationships that evolve into higher-value advisory as wealth accumulates, improving customer lifetime value economics for providers. Partnerships between fintech platforms and established asset managers or banks combine distribution agility with product credibility, accelerating trust adoption among new investor cohorts. This segment expansion pathway offers scalable market depth growth while diversifying revenue beyond concentrated ultra-wealthy client bases.

Growth of Family Office and Alternative Investment Advisory Ecosystems

Growth of family office structures and alternative investment advisory ecosystems in India wealth management market presents a major opportunity because increasing promoter liquidity events, intergenerational wealth transfers, and cross-border entrepreneurial exposure are prompting ultra-high-net-worth families to institutionalize wealth governance, asset allocation, and succession planning frameworks. Dedicated family office platforms require integrated services spanning private market investments, real assets, philanthropy structuring, tax optimization, and risk management, enabling wealth firms to deliver comprehensive multi-disciplinary advisory beyond conventional portfolio management. Rising interest in private equity, venture capital, infrastructure, and global real estate allocations among wealthy Indian families expands demand for curated deal access, due diligence capabilities, and portfolio monitoring services offered by specialized wealth advisors. Global diversification mandates driven by currency risk awareness and geopolitical asset dispersion considerations encourage cross-border investment structuring expertise and international custody solutions within wealth platforms. Institutionalization of family governance including trusts, foundations, and investment committees creates recurring advisory engagement across generations, stabilizing long-term revenue streams for wealth managers. Collaboration between domestic wealth firms and global investment houses enhances alternative product availability and expertise transfer into the Indian market. Increasing professionalization of family wealth management also drives demand for reporting technology, consolidated risk analytics, and performance attribution tools supporting multi-asset portfolios. These structural shifts toward institutional wealth management frameworks significantly elevate advisory complexity and value creation potential across the ultra-wealthy segment.

Major Players

- HDFC Asset Management

- ICICI Prudential Asset Management

- SBI Funds Management

- Kotak Wealth Management

- IIFL Wealth Management

- Axis Asset Management

- Nippon India Asset Management

- Aditya Birla Sun Life AMC

- Motilal Oswal Wealth Management

- Edelweiss Wealth Management

- Avendus Wealth Management

- JM Financial Wealth

- ASK Wealth Advisors

- HSBC Global Private Banking India

- Julius Baer India

Key Target Audience

- Private banks

- Asset management companies

- Family offices

- Investments and venture capitalist firms

- Brokerage and financial advisory firms

- High-net-worth investor associations

- Government and regulatory bodies

- Alternative investment funds

Research Methodology

Step 1: Identification of Key Variables

Key variables including affluent population size, investable financial assets, advisory penetration, product adoption, and regulatory environment were identified through financial authority publications and institutional disclosures. Market drivers and structural constraints were mapped across demographic, economic, and financial system dimensions. Variable relationships were structured to represent wealth creation and advisory demand linkages.

Step 2: Market Analysis and Construction

Segment structures across product types and advisory platforms were constructed using asset distribution data, institutional AUM disclosures, and industry association statistics. Market share allocation was derived by triangulating asset class penetration, distribution channel strength, and investor adoption patterns. Competitive positioning and ecosystem dynamics were analyzed across advisory tiers.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding affluent growth, advisory penetration, and product demand were validated through industry expert interviews, regulatory interpretation, and wealth firm strategic disclosures. Comparative benchmarking with global wealth markets informed structural realism. Scenario testing ensured consistency across demographic and financial variables.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into structured market narratives, segmentation tables, competitive mapping, and forward outlook. Internal consistency checks ensured alignment across drivers, challenges, and opportunity frameworks. Final output was standardized to ensure analytical coherence and decision relevance.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising high-net-worth population and financial asset accumulation

Expansion of capital markets participation across investor segments

Regulatory push for formalized financial advisory and transparency

Intergenerational wealth transfer driving professional management demand

Digital advisory platforms lowering entry barriers for affluent clients - Market Challenges

Low financial literacy and trust deficits in advisory services

Fragmented regulatory compliance across product categories

Talent shortages in certified wealth advisory professionals

High client acquisition and servicing costs in premium segments

Market volatility affecting portfolio performance perceptions - Market Opportunities

Expansion into tier-2 and tier-3 affluent investor segments

Integration of tax, estate, and succession advisory services

Growth of ESG and alternative investment advisory mandates - Trends

Shift toward fee-based advisory over commission models

Adoption of hybrid human-digital wealth advisory models

Increased allocation to global and alternative assets

Personalized goal-based financial planning frameworks

Consolidation among independent wealth management firms - Government Regulations & Defense Policy

SEBI investment advisor and portfolio management regulations

Taxation reforms affecting capital gains and inheritance planning

Cross-border investment and offshore asset disclosure norms - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory Wealth Management

Execution-Only Brokerage Services

Estate and Trust Planning Services

Alternative Investment Advisory - By Platform Type (In Value%)

Bank-Led Wealth Platforms

Independent Wealth Firms

Digital Robo-Advisory Platforms

Brokerage-Led Advisory Platforms

Family Office Platforms - By Fitment Type (In Value%)

Onshore Wealth Structures

Offshore Wealth Structures

Hybrid Advisory Models

Modular Investment Mandates

Integrated Financial Planning Suites - By End User Segment (In Value%)

Ultra High Net Worth Individuals

High Net Worth Individuals

Affluent Mass Segment

Family Offices

Institutional Wealth Clients - By Procurement Channel (In Value%)

Relationship Manager-Led Acquisition

Digital Direct Platforms

Private Banking Channels

Independent Financial Advisors

Brokerage Distribution Networks - By Material / Technology (in Value %)

AI-Driven Portfolio Analytics

Goal-Based Financial Planning Software

Robo-Advisory Algorithms

Blockchain-Based Custody Solutions

Client Lifecycle Management Platforms

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Client Segment Focus, Product Breadth, Advisory Model, Digital Capability, Geographic Presence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

360 ONE Wealth

Kotak Wealth Management

ICICI Private Banking

HDFC Private Banking

Axis Bank Burgundy Private

Edelweiss Wealth Management

Motilal Oswal Private Wealth

ASK Wealth Advisors

Nuvama Wealth Management

Anand Rathi Wealth

Avendus Wealth Management

JM Financial Wealth

DSP Wealth Management

SBI Wealth

Tata Capital Wealth

- UHNW clients demanding bespoke multi-asset global portfolios

- HNW investors seeking tax-efficient structured products

- Affluent segment adopting digital advisory for diversification

- Family offices prioritizing succession and governance structures

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now