Download PDF

Download PDFMarket Overview

Indonesia’s third-party logistics industry forms a core component of the country’s trade and distribution infrastructure, with the market valued at approximately USD ~ billion based on a recent historical assessment derived from logistics industry revenue statistics published by the Indonesian Ministry of Transportation and national logistics sector reports. Market growth is primarily supported by expanding domestic consumption, rising e-commerce shipments, increasing manufacturing exports, and large investments in logistics infrastructure including seaports, industrial corridors, warehouse facilities, and multimodal transportation networks connecting major economic regions.

Major logistics operations are concentrated in Jakarta, Surabaya, Bandung, and Batam due to their strategic proximity to manufacturing clusters, large consumer populations, and international cargo gateways. Jakarta operates as the central logistics hub supported by Tanjung Priok Port and extensive distribution infrastructure, while Surabaya serves as a major maritime gateway for eastern Indonesia. Batam functions as an export logistics hub due to its connectivity with Singapore, and Bandung supports manufacturing supply chain logistics for industrial production zones.

Market Segmentation

By Service Type

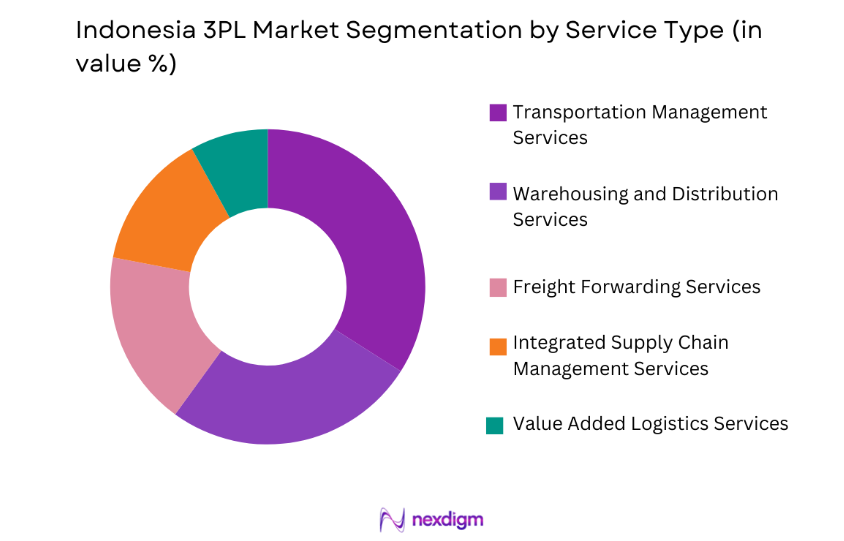

Indonesia 3PL market is segmented by product type into transportation management services, warehousing and distribution services, freight forwarding services, value added logistics services, and integrated supply chain management services. Recently, transportation management services has a dominant market share due to factors such as Indonesia’s archipelagic geography, complex domestic transportation requirements, and the strong demand for freight movement across islands. Companies rely heavily on logistics providers to coordinate road freight, maritime shipping, and intermodal cargo transport across the country’s vast territory. Third-party logistics operators manage trucking fleets, shipping schedules, and cargo routing systems to ensure efficient movement of goods between industrial production centers, seaports, and consumer markets. The growth of domestic trade and manufacturing production further increases demand for transportation coordination services throughout Indonesia’s national logistics network.

By End User Industry

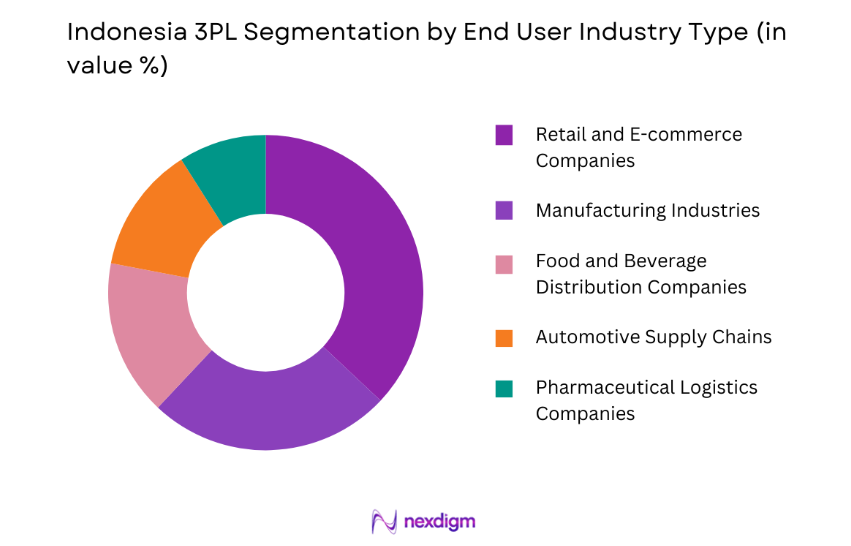

Indonesia 3PL market is segmented by product type into retail and e-commerce companies, manufacturing industries, automotive supply chains, food and beverage distribution companies, and pharmaceutical logistics companies. Recently, retail and e-commerce companies have a dominant market share due to factors such as the rapid expansion of online retail platforms, rising consumer demand for home deliveries, and the increasing need for nationwide distribution networks. E-commerce platforms rely heavily on third-party logistics providers to manage warehousing inventory handling and parcel transportation across urban and suburban markets. Logistics providers operate large distribution centers and last-mile delivery networks that enable retailers to fulfill online orders efficiently. The expansion of direct-to-consumer retail models and digital marketplaces further increases demand for professional logistics outsourcing services across Indonesia’s rapidly growing digital economy.

Competitive Landscape

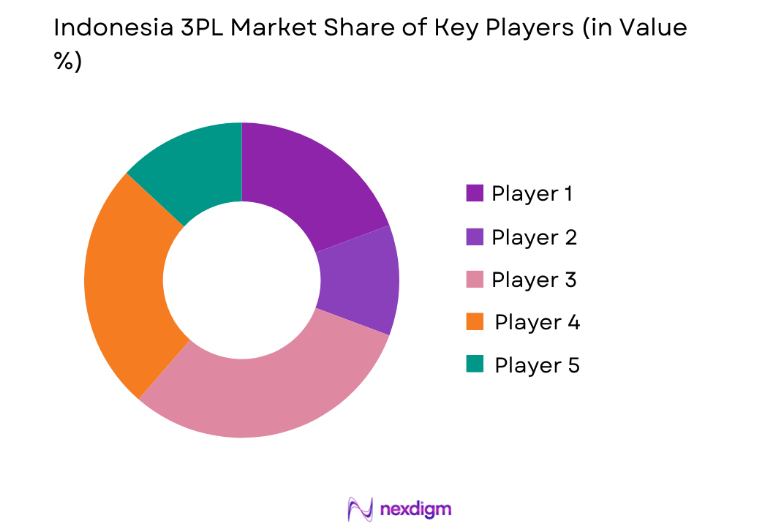

The Indonesia 3PL market is characterized by a competitive landscape involving multinational logistics providers, regional supply chain companies, and domestic logistics operators competing to expand integrated logistics services across transportation, warehousing, and supply chain management. Global logistics firms dominate complex international supply chains due to their advanced technology platforms and global shipping networks. Domestic logistics providers focus on nationwide distribution services and regional transportation networks supporting Indonesia’s manufacturing and retail industries.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Network Capacity |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| CJ Logistics | 1930 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Yusen Logistics | 1955 | Japan | ~ | ~ | ~ | ~ | ~ |

Indonesia 3PL Market Analysis

Growth Drivers

Expansion of E-commerce Logistics and Digital Retail Supply Chains

Indonesia’s rapidly expanding digital commerce ecosystem significantly drives the growth of the third-party logistics market because online retailers require reliable logistics networks capable of managing large volumes of parcel shipments and inventory distribution across multiple cities and islands. E-commerce platforms including Tokopedia Shopee and Lazada generate high order volumes that must be processed through distribution centers and delivered to consumers across urban and rural regions. Third-party logistics providers therefore play a critical role in managing warehousing operations transportation networks and last-mile delivery infrastructure that support digital retail fulfillment. Logistics companies invest heavily in automated sorting facilities digital logistics platforms and route optimization technologies to manage increasing shipment volumes. The rapid growth of direct-to-consumer brands further strengthens demand for outsourced logistics services because retailers rely on professional logistics providers rather than building their own distribution infrastructure. Increasing smartphone penetration and digital payment adoption continue to expand Indonesia’s online shopping ecosystem. Logistics providers therefore expand warehouse capacity and transportation fleets to meet rising order fulfillment requirements across Indonesia’s rapidly growing digital economy.

Infrastructure Development and Government Investment in National Logistics Connectivity

Indonesia’s government investment in transportation infrastructure significantly supports the development of the third-party logistics market by improving connectivity between production centers ports and consumer markets. National infrastructure programs include the development of new seaports airports highways and industrial logistics zones designed to strengthen cargo transportation efficiency across the archipelago. Major port modernization projects increase container handling capacity while new highway corridors improve freight movement between industrial regions and distribution centers. Logistics providers benefit from improved infrastructure because efficient transport networks reduce cargo transit times and operational costs. Government initiatives such as the National Logistics Ecosystem program aim to streamline customs procedures improve digital logistics platforms and strengthen supply chain integration. These infrastructure improvements encourage businesses to outsource logistics operations to specialized providers capable of managing complex supply chain activities. As transportation connectivity continues improving third-party logistics providers will benefit from rising demand for integrated supply chain services across Indonesia’s expanding trade economy.

Market Challenges

Fragmented Logistics Infrastructure and Inter-Island Transportation Complexity

Indonesia’s geography as an archipelago consisting of thousands of islands creates logistical challenges for transportation and distribution networks that directly affect the efficiency of third-party logistics operations. Goods must often be transported across multiple transportation modes including trucks ships and air cargo services before reaching final destinations. This complex transportation environment increases cargo handling requirements and operational coordination challenges for logistics providers. Limited logistics infrastructure in certain regions also results in longer delivery times and higher transportation costs for businesses operating outside major economic centers. Logistics companies must manage multiple shipping routes and coordinate with local transportation providers to ensure reliable cargo movement between islands. Supply chain visibility also becomes more complex when shipments travel through multiple transit points across maritime networks. These logistical complexities increase operational costs and require significant planning and coordination for logistics service providers operating across Indonesia’s national distribution network.

Rising Operational Costs and Limited Skilled Logistics Workforce

The Indonesia 3PL market faces operational challenges related to rising fuel costs labor expenses and the need for skilled logistics professionals capable of managing advanced supply chain technologies. Logistics companies require large fleets of trucks cargo vessels and warehouse infrastructure to manage national distribution networks. Maintaining these assets requires continuous investment in maintenance technology systems and workforce training. Recruiting qualified logistics professionals with expertise in supply chain analytics warehouse management and digital logistics platforms remains difficult in certain regions. Labor shortages can affect operational efficiency and service quality particularly in rapidly growing logistics hubs. Logistics companies must therefore invest heavily in workforce development programs and digital logistics technologies to improve operational productivity. These financial and workforce constraints may limit the expansion capacity of smaller logistics providers competing within Indonesia’s growing logistics industry.

Opportunities

Expansion of Regional Trade and Cross Border Logistics Integration

Indonesia’s increasing participation in regional trade agreements creates significant opportunities for third-party logistics providers to support cross border supply chains connecting Southeast Asia and global markets. Manufacturers exporters and retailers require logistics partners capable of managing international freight transportation customs clearance and distribution operations across multiple countries. Third-party logistics providers can expand services such as international freight forwarding cargo consolidation and cross border distribution management. Growing export industries including electronics automotive components and agricultural products also increase demand for international logistics coordination services. Logistics companies that develop strong cross border transportation networks and customs expertise will benefit from expanding trade flows. Strategic partnerships with global logistics providers also enable domestic companies to participate in international supply chain networks. As regional trade volumes increase third-party logistics companies will play an increasingly important role in facilitating international cargo movement.

Adoption of Smart Warehousing and Digital Logistics Platforms

The integration of smart logistics technologies presents significant opportunities for improving operational efficiency across Indonesia’s third-party logistics sector. Logistics companies increasingly adopt warehouse automation systems artificial intelligence based inventory management platforms and digital shipment tracking technologies to manage complex supply chains. Smart warehousing solutions enable faster order processing and improved inventory accuracy for retailers and manufacturers. Digital freight platforms allow logistics providers to coordinate shipments manage cargo documentation and optimize transportation routes through centralized logistics systems. The adoption of data analytics tools also enables logistics companies to forecast demand patterns and optimize warehouse capacity utilization. Technology driven logistics services improve service quality while reducing operational costs for businesses outsourcing supply chain operations. As digital transformation continues across the logistics sector third-party logistics providers that invest in advanced technologies will gain significant competitive advantages within Indonesia’s rapidly evolving logistics industry.

Future Outlook

Indonesia’s third-party logistics market is expected to expand significantly as domestic consumption, e-commerce activity, and international trade volumes continue increasing across the country. Investment in logistics infrastructure, digital supply chain platforms, and warehouse automation technologies will strengthen operational efficiency across national distribution networks. Government policies supporting logistics connectivity and trade facilitation will further encourage market development. Rising demand for integrated supply chain outsourcing services will continue driving the growth of the Indonesia 3PL market over the coming years.

Major Players

- DHL Supply Chain

- DB Schenker

- Kuehne + Nagel

- CJ Logistics

- Yusen Logistics

- CEVA Logistics

- DSV

- Nippon Express

- Kerry Logistics

- Expeditors International

- Agility Logistics

- Sinotrans

- Bollore Logistics

- Hellmann Worldwide Logistics

- Tiki Jalur Nugraha Ekakurir

Key Target Audience

- Retail and e-commerce companies

- Manufacturing and industrial companies

- Automotive supply chain companies

- Food and beverage distribution companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Logistics infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key variables including logistics service revenues transportation volumes warehouse infrastructure capacity trade statistics and supply chain outsourcing trends were identified using government logistics databases and industry trade reports.

Step 2: Market Analysis and Construction

The market structure was developed by analyzing logistics service demand transportation infrastructure distribution networks and operational data from logistics providers operating across Indonesia.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through interviews with logistics managers supply chain experts freight forwarding specialists and transportation infrastructure professionals active in Indonesia’s logistics sector.

Step 4: Research Synthesis and Final Output

Validated logistics data infrastructure insights and market trends were integrated to produce the final market assessment including segmentation competitive landscape and long term growth outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E Commerce and Digital Retail Distribution Networks

Development of National Logistics Infrastructure and Transport Corridors

Increasing Outsourcing of Supply Chain Operations by Manufacturing Companies - Market Challenges

High Logistics Costs Across Indonesia’s Archipelagic Geography

Infrastructure Bottlenecks in Secondary Ports and Transport Corridors

Limited Integration of Digital Logistics Technologies - Market Opportunities

Expansion of Integrated Supply Chain Solutions for E Commerce Logistics

Growth of Cold Chain Logistics Services for Food and Pharmaceutical Distribution

Adoption of Digital Logistics Platforms and Smart Warehouse Technologies - Trends

Adoption of Automated Warehousing and Robotics Technologies

Integration of Digital Freight Visibility and Logistics Management Platforms - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Transportation Management Services

Warehousing and Distribution Services

Integrated Supply Chain Management Services

Freight Transportation Services

Value Added Logistics Services - By Platform Type (In Value%)

Road Transportation Logistics Platforms

Maritime Logistics Platforms

Air Cargo Logistics Platforms

Rail Freight Logistics Platforms - By Fitment Type (In Value%)

Asset Light Logistics Models

Asset Based Logistics Models

Hybrid Logistics Service Models

Integrated End to End Logistics Models - By End User Segment (In Value%)

Manufacturing and Industrial Companies

Retail and E Commerce Enterprises

Energy and Natural Resources Companies

- Market Share Analysis

- Cross Comparison Parameters (Logistics Network Coverage, Warehouse Infrastructure Capacity, Multimodal Transport Capability, Technology Platform Integration, Fleet and Asset Availability, Service Portfolio Diversity, Strategic Industry Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain Indonesia

DB Schenker Indonesia

Kuehne + Nagel Indonesia

DSV Indonesia

CEVA Logistics Indonesia

Yusen Logistics Indonesia

Nippon Express Indonesia

Agility Logistics Indonesia

CJ Logistics Indonesia

JNE Logistics

SiCepat Ekspres Logistics

Samudera Indonesia Logistics

Wahana Prestasi Logistik

RPX Logistics

Pos Logistics Indonesia

- Manufacturing Companies Increasingly Outsourcing Transportation and Warehousing Services

- Retail and E Commerce Companies Expanding Nationwide Logistics Networks

- Energy and Mining Companies Requiring Specialized Logistics Support

- SME Exporters Utilizing Third Party Logistics Providers for International Trade

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now