Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Indonesia cloud infrastructure market is valued at approximately USD ~ billion based on a recent historical assessment from IDC and Indonesia Ministry of Communication and Informatics digital economy statistics, driven by hyperscale data center expansion, enterprise cloud migration, and strong demand for colocation and IaaS platforms. Rapid digitalization across banking, e-commerce, and public services is accelerating infrastructure investments, supported by submarine cable connectivity upgrades and domestic data localization policies encouraging local cloud deployment.

Jakarta dominates the Indonesia cloud infrastructure market due to concentration of hyperscale data centers, internet exchange points, and enterprise headquarters, while Batam is emerging as a regional interconnection hub leveraging proximity to Singapore and special economic zone incentives. Surabaya and West Java industrial corridors are also expanding cloud infrastructure capacity driven by manufacturing digitization and edge deployment needs. Strong domestic demand combined with regional connectivity positioning is reinforcing Indonesia’s role in Southeast Asia cloud infrastructure expansion.

Market Segmentation

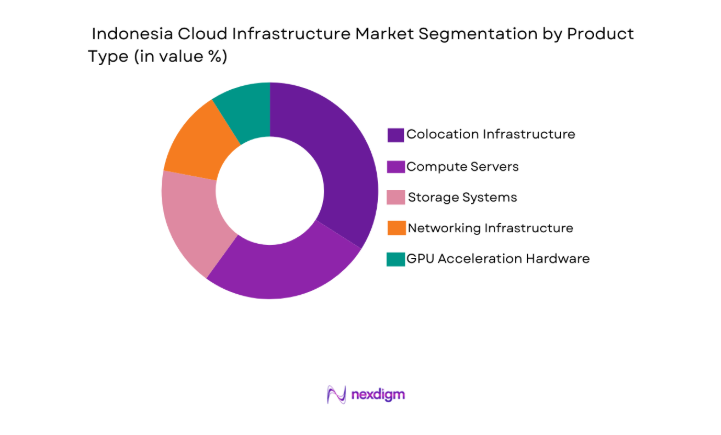

By Product Type

Indonesia cloud infrastructure market is segmented by product type into compute servers, storage systems, networking infrastructure, GPU acceleration hardware, and colocation infrastructure. Recently, colocation infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The growth of hyperscale campuses, enterprise hybrid cloud strategies, and regulatory requirements for domestic data hosting has increased reliance on carrier-neutral colocation facilities. Enterprises prefer outsourced infrastructure to reduce capital expenditure and ensure compliance with data sovereignty regulations, while hyperscalers use colocation to accelerate regional deployment. Indonesia’s geographic dispersion also favors distributed colocation nodes for latency optimization across islands.

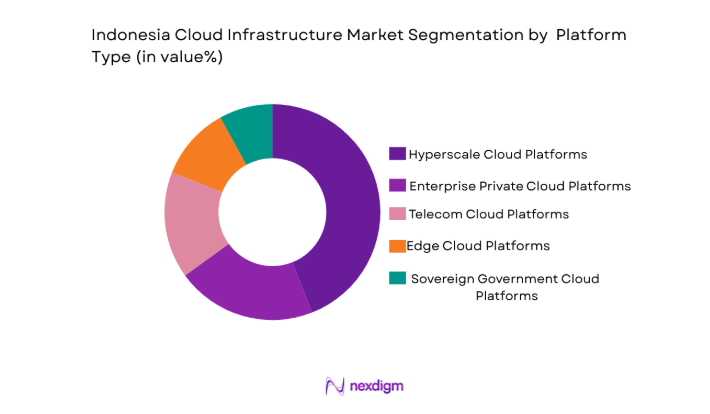

By Platform Type

Indonesia cloud infrastructure market is segmented by platform type into hyperscale cloud platforms, enterprise private cloud platforms, telecom cloud platforms, edge cloud platforms, and sovereign government cloud platforms. Recently, hyperscale cloud platforms have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Global hyperscalers have established local availability zones and high-capacity regions enabling enterprises to access scalable compute and storage services domestically. Their extensive service portfolios, developer ecosystems, and integrated AI and analytics capabilities attract startups, enterprises, and public sector users. Multi-availability-zone architectures and compliance-ready deployments further reinforce enterprise trust and large-scale workload migration toward hyperscale platforms.

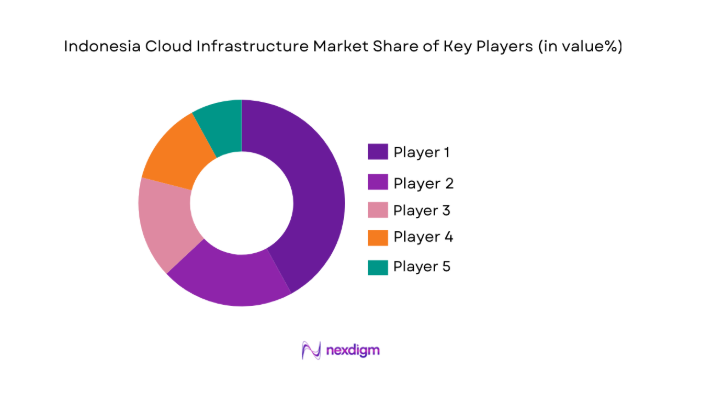

Competitive Landscape

Indonesia cloud infrastructure market shows moderate consolidation with strong presence of global hyperscalers alongside regional data center operators and domestic telecom-linked infrastructure providers. Market leadership is shaped by hyperscale capacity expansion, interconnection ecosystems, and compliance-ready sovereign infrastructure offerings. Strategic partnerships with telecom carriers, land banks for data center campuses, and multi-availability-zone architectures are key competitive differentiators influencing enterprise adoption and regional workload distribution.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Data Center Capacity in Indonesia |

| Amazon Web Services | 2006 | United States | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | United States | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | United States | ~ | ~ | ~ | ~ | ~ |

| Telkom Indonesia | 1965 | Indonesia | ~ | ~ | ~ | ~ | ~ |

| NTT Global Data Centers | 1987 | Japan | ~ | ~ | ~ | ~ | ~ |

Indonesia Cloud Infrastructure Market Analysis

Growth Drivers

Hyperscale Data Center Expansion and Regional Cloud Availability Zones

Hyperscale data center expansion and regional cloud availability zones are significantly accelerating Indonesia cloud infrastructure adoption by improving latency performance, regulatory compliance, and service reliability across the archipelagic geography. Global cloud providers have established multiple availability zones within the Jakarta metropolitan region, enabling enterprises to deploy mission-critical workloads domestically rather than relying on cross-border hosting that previously introduced latency and data sovereignty concerns. The establishment of large-scale hyperscale campuses has also catalyzed the development of supporting ecosystems including fiber backbones, internet exchange points, renewable energy sourcing, and managed services providers that collectively strengthen infrastructure readiness. As enterprises modernize legacy IT systems into cloud-native architectures, the availability of local hyperscale capacity reduces migration risk and improves workload portability across hybrid environments. Financial institutions and regulated industries particularly benefit from domestic zones that meet local data residency requirements, encouraging accelerated cloud adoption in banking, insurance, and public sector services. The presence of multiple hyperscalers also increases competitive pricing and service diversification, allowing enterprises to implement multi-cloud strategies for resilience and vendor risk management. Regional availability zones in Indonesia additionally support Southeast Asian digital traffic flows, positioning the country as a secondary cloud hub complementing Singapore’s mature ecosystem. This regional positioning attracts multinational enterprises seeking geographic redundancy across Southeast Asia while maintaining proximity to Indonesia’s large consumer market. Hyperscale expansion also stimulates colocation and edge node growth across secondary cities, enabling distributed architectures suited to Indonesia’s island-based connectivity landscape. Overall, hyperscale infrastructure deployment acts as the foundational growth engine for Indonesia cloud infrastructure market by lowering adoption barriers and enabling scalable digital transformation across industries.

Enterprise Digital Transformation and Regulatory-Driven Data Localization Adoption

Enterprise digital transformation and regulatory-driven data localization adoption are creating sustained demand for domestic cloud infrastructure across Indonesia’s public and private sectors. Government regulations encouraging local data storage for critical sectors such as finance, telecommunications, and public services have increased enterprise preference for Indonesia-based cloud hosting environments. Organizations undergoing digital transformation initiatives are migrating core applications including ERP, customer platforms, and analytics systems into cloud environments to enhance agility and operational efficiency. The rapid growth of Indonesia’s digital economy, including e-commerce platforms, fintech ecosystems, and digital public services, requires scalable infrastructure capable of handling high transaction volumes and real-time data processing. Domestic cloud availability enables enterprises to comply with regulations while maintaining service responsiveness for local users distributed across thousands of islands. Telecom operators and domestic data center providers are partnering with global hyperscalers to deliver localized cloud offerings integrated with national connectivity networks. Enterprises also adopt hybrid architectures combining on-premise systems with localized cloud to balance compliance, performance, and cost considerations. Public sector digitalization programs such as smart city platforms and e-government services rely on domestic cloud infrastructure to ensure data governance and citizen service continuity. The localization trend additionally stimulates investment in domestic colocation campuses, sovereign cloud solutions, and managed infrastructure services tailored to regulated industries. Collectively, digital transformation pressures combined with localization policies are creating structural demand for Indonesia-hosted cloud infrastructure, reinforcing long-term market expansion.

Market Challenges

Power Infrastructure Constraints and Sustainable Energy Availability for Hyperscale Facilities

Power infrastructure constraints and sustainable energy availability for hyperscale facilities present a major structural challenge for Indonesia cloud infrastructure market expansion. Hyperscale data centers require extremely high and stable electricity supply with redundant grid connections, yet several Indonesian regions still face grid reliability limitations and constrained generation capacity. Data center operators must invest heavily in captive power systems, diesel backup generation, and power conditioning infrastructure to ensure uptime, significantly increasing capital and operating costs. Sustainability requirements from global cloud providers further complicate deployment because renewable energy sourcing in Indonesia remains geographically uneven and limited in scale relative to hyperscale demand. Operators often need to secure long-term power purchase agreements or develop private renewable installations, extending project timelines and regulatory approvals. Land parcels suitable for hyperscale campuses must also be located near high-capacity substations and transmission corridors, restricting site availability and driving land costs in preferred zones such as Greater Jakarta and Batam. Cooling infrastructure requirements in tropical climates further increase electricity intensity, necessitating advanced cooling technologies and water management systems that add engineering complexity. Grid decarbonization progress is slower than hyperscaler sustainability targets, creating gaps between corporate environmental commitments and local infrastructure realities. These energy and power constraints directly affect deployment speed, operational costs, and scalability of Indonesia cloud infrastructure capacity expansion. As hyperscale demand continues to grow, power availability and sustainability alignment remain critical bottlenecks influencing long-term market competitiveness.

Fragmented Geography and Inter-Island Connectivity Limitations Affecting Latency and Network Resilience

Fragmented geography and inter-island connectivity limitations affecting latency and network resilience create structural complexity for Indonesia cloud infrastructure deployment and service performance. Indonesia consists of thousands of islands with uneven fiber backbone distribution, resulting in concentration of high-capacity connectivity around Java while outer regions rely on limited or higher-latency links. Cloud workloads hosted in Jakarta may experience increased latency when serving users in eastern regions such as Papua or Maluku, reducing performance for real-time applications including digital payments, streaming, and IoT services. To mitigate latency, providers must deploy distributed edge nodes or secondary data centers across multiple islands, significantly increasing capital expenditure and operational complexity. Submarine cable deployments are expensive and require long regulatory and construction cycles, slowing network densification across remote regions. Network resilience is also challenged by exposure to seismic activity and marine hazards that can damage submarine cables and disrupt connectivity between islands. Enterprises seeking nationwide service delivery must architect multi-region redundancy across geographically distant nodes, increasing infrastructure costs and management complexity. The uneven connectivity landscape also affects adoption among regional enterprises that lack reliable high-bandwidth access to cloud regions. Telecom operators and infrastructure providers are investing in national fiber backbones and satellite augmentation, but coverage gaps persist across large parts of the archipelago. This geographic fragmentation remains a defining structural challenge shaping Indonesia cloud infrastructure architecture, cost structures, and service distribution models.

Opportunities

Emergence of Batam as a Cross-Border Data Center and Interconnection Hub Near Singapore

Emergence of Batam as a cross-border data center and interconnection hub near Singapore represents a major strategic opportunity for Indonesia cloud infrastructure market expansion and regional positioning. Batam’s geographic proximity to Singapore enables low-latency connectivity to Southeast Asia’s primary digital hub while offering significantly lower land and power costs for hyperscale and colocation development. Special economic zone incentives and streamlined investment approvals in Batam are attracting global data center operators seeking expansion capacity constrained in Singapore due to land and energy limitations. Submarine cable landing stations and cross-border fiber routes between Batam and Singapore enable seamless interconnection with regional cloud ecosystems and internet exchange points. Enterprises can deploy workloads in Batam while maintaining integration with Singapore’s financial and digital networks, creating hybrid cross-border architectures. Batam also provides geographic redundancy for Singapore-hosted workloads, supporting disaster recovery and multi-region resilience strategies for regional enterprises. Indonesian telecom operators are strengthening Batam connectivity to domestic networks, enabling Batam-hosted cloud services to serve both Indonesian and Southeast Asian markets. Hyperscalers and colocation providers are establishing large campuses in Batam designed for multi-tenant regional workloads and hyperscale availability zones. The hub potential additionally stimulates ecosystem growth including managed services, connectivity providers, and cloud integrators in the Batam region. As Singapore capacity constraints persist, Batam’s emergence as a complementary hyperscale hub positions Indonesia to capture regional cloud infrastructure demand beyond domestic consumption.

Edge Infrastructure Deployment Across Secondary Cities to Support Distributed Digital Economy

Edge infrastructure deployment across secondary cities to support distributed digital economy presents substantial growth opportunities for Indonesia cloud infrastructure market beyond primary metropolitan regions. Indonesia’s digital population is widely dispersed across islands and mid-tier cities where latency-sensitive applications such as e-commerce logistics, gaming, telemedicine, and smart manufacturing require localized processing. Deploying edge data centers and micro-cloud nodes in cities such as Surabaya, Makassar, Medan, and Bandung reduces latency and improves service reliability for regional users. Telecom operators and colocation providers are leveraging existing network hubs and exchange points to host edge infrastructure integrated with national fiber backbones. Industrial zones adopting Industry 4.0 technologies require localized compute and storage for automation, analytics, and IoT processing, further stimulating edge demand. Government smart city and regional digitalization initiatives also benefit from localized infrastructure supporting public services and surveillance systems. Edge deployment enables content delivery networks and streaming platforms to cache data closer to users, improving user experience across Indonesia’s dispersed geography. Cloud providers are developing edge offerings integrated with central hyperscale regions, enabling hybrid distributed architectures for enterprises. Investment in modular and prefabricated data center designs facilitates rapid edge deployment across diverse locations. As digital activity decentralizes beyond Jakarta, distributed edge infrastructure becomes a critical opportunity area enabling nationwide cloud adoption and balanced regional digital growth.

Future Outlook

Indonesia cloud infrastructure market is expected to expand steadily over the next five years driven by hyperscale capacity additions, domestic data localization policies, and rapid enterprise digitalization. Emerging interconnection hubs such as Batam and distributed edge deployments across secondary cities will reshape infrastructure geography beyond Jakarta. Renewable energy integration and national fiber backbone expansion will improve deployment feasibility. Continued hyperscaler investment and public sector digital programs will sustain long-term infrastructure demand.

Major Players

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Telkom Indonesia

- NTT Global Data Centers

- Alibaba Cloud

- Huawei Cloud

- EdgeConneX

- Princeton Digital Group

- ST Telemedia Global DataCentres

- Keppel DataCentres

- GDS Holdings

- Equinix

- Digital Realty

- DCI Indonesia

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hyperscale cloud providers

- Telecom operators

- Data center developers

- Enterprise IT infrastructure buyers

- Digital platform companies

- Colocation service providers

Research Methodology

Step 1: Identification of Key Variables

Key demand drivers, infrastructure capacity indicators, regulatory frameworks, investment flows, and technology adoption variables specific to Indonesia cloud infrastructure market were mapped across supply and demand sides to define analytical scope and segmentation structure.

Step 2: Market Analysis and Construction

Data from infrastructure deployments, hyperscale capacity announcements, telecom connectivity expansion, enterprise cloud adoption trends, and policy frameworks were synthesized to construct market structure, segmentation, and competitive positioning across Indonesia regions.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with cloud architects, telecom infrastructure specialists, data center developers, and enterprise IT strategists to ensure alignment with deployment realities, regulatory constraints, and technology evolution trajectories.

Step 4: Research Synthesis and Final Output

Validated insights were integrated into a structured analytical framework covering market dynamics, segmentation, competition, and outlook to produce a coherent assessment of Indonesia cloud infrastructure market development trajectory.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid expansion of hyperscale data centers driven by domestic digital economy growth

Government digital transformation initiatives and sovereign data policies

Rising enterprise migration to hybrid and multi-cloud architectures - Market Challenges

Limited power and land availability in primary data center clusters

Fragmented connectivity infrastructure across archipelagic regions

Shortage of advanced cloud engineering and data center operations skills - Market Opportunities

Expansion of edge infrastructure across secondary cities and islands

Localization of cloud regions to meet data residency requirements

Green data center investments using renewable energy integration - Trends

Shift toward AI-ready cloud infrastructure with GPU acceleration capacity

Adoption of modular and prefabricated data center architectures

Growth of telecom cloud convergence with 5G network virtualization - Government Regulations & Defense Policy

Data localization mandates for strategic and public sector data

National data center roadmap and digital sovereignty initiatives

Energy efficiency and sustainability standards for data centers - Swot Analysis

Strong demand from digital platforms and fintech ecosystem expansion

Infrastructure constraints in power, land, and connectivity

Opportunities in regional edge and sovereign cloud deployments - Porters 5 forces

High capital intensity and barriers to entry in hyperscale infrastructure

Supplier concentration in advanced compute and networking hardware

Increasing buyer power from large cloud and telecom operators

- By Market Value 2020-2025

- By Installed Units 2020-2025

- By Average System Price 2020-2025

- By System Complexity Tier 2020-2025

- By System Type (In Value%)

Compute Infrastructure

Storage Infrastructure

Networking Infrastructure

Data Center Interconnect Systems

Cloud Management and Orchestration Platforms - By Platform Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Multi-Cloud Infrastructure

Edge Cloud Infrastructure - By Fitment Type (In Value%)

Hyperscale Data Centers

Enterprise Data Centers

Colocation Facilities

Telecom Cloud Nodes

Edge Micro Data Centers - By End User Segment (In Value%)

Telecommunications Providers

Financial Services Institutions

E-commerce and Digital Platforms

Government and Public Sector

Manufacturing and Industrial Enterprises - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrators and VARs

Cloud Service Providers

Telecom Infrastructure Vendors

Managed Service Providers

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Infrastructure Scale, Cloud Service Integration, Data Center Footprint, Network Connectivity, Energy Efficiency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

PT Telkom Indonesia

Indosat Ooredoo Hutchison

XL Axiata

Alibaba Cloud

Amazon Web Services

Google Cloud

Microsoft

Equinix

Digital Realty

ST Telemedia Global Data Centres

Keppel Data Centres

NTT Global Data Centers

Huawei Cloud

EdgeConneX

Princeton Digital Group

- Telecom operators driving distributed cloud and edge node deployments for 5G services

- Financial institutions accelerating secure private and hybrid cloud adoption

- Digital platforms requiring hyperscale compute and storage scalability

- Public sector entities prioritizing sovereign and localized cloud environments

- Forecast Market Value 2026-2035

- Forecast Installed Units 2026-2035

- Price Forecast by System Tier 2026-2035

- Future Demand by Platform 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now