Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Indonesia Cold Chain Logistics Market was valued at approximately USD ~ billion, supported by the country’s growing food distribution networks, pharmaceutical supply chains, and expanding retail grocery infrastructure. Rapid development of temperature-controlled warehousing refrigerated transportation fleets, and integrated logistics platforms has significantly improved distribution efficiency. The Ministry of Agriculture and industry trade bodies highlight strong demand from seafood exports, frozen food processing, pharmaceutical distribution, and urban retail supply chains, which collectively support the continued expansion of refrigerated logistics infrastructure.

Major cold chain logistics activity is concentrated around Jakarta, Surabaya, Medan, and Makassar due to their strong port connectivity, population density, and proximity to food production clusters. Jakarta functions as the primary logistics and import distribution hub because of its port infrastructure and large consumer markets. Surabaya supports eastern Indonesia distribution networks, while Medan plays a critical role in seafood and agricultural export logistics. These cities benefit from extensive warehousing infrastructure, access to transportation corridors, and strong food processing industries that depend heavily on temperature-controlled logistics systems.

Market Segmentation

By Service Type

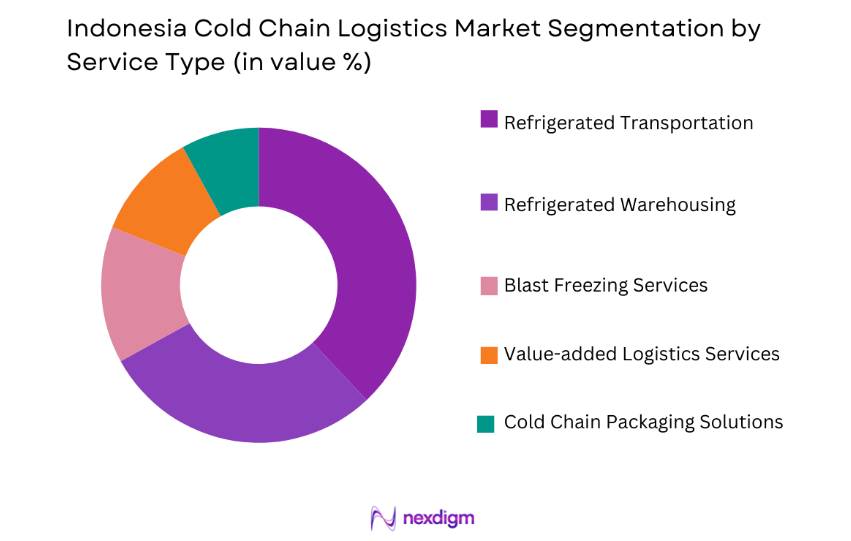

Indonesia Cold Chain Logistics Market is segmented by service type into refrigerated warehousing, refrigerated transportation, blast freezing services, value-added logistics services, and cold chain packaging solutions. Recently, refrigerated transportation has a dominant market share due to the country’s archipelagic geography and the need to transport perishable food products across long distances between islands. Seafood exports, frozen foods, dairy distribution, and pharmaceutical shipments depend heavily on reliable temperature-controlled transportation networks. Logistics companies invest in refrigerated truck fleets, containerized shipping solutions, and temperature monitoring technologies to maintain product quality during transit. Increasing inter-island trade and food distribution across urban centers significantly reinforce the demand for refrigerated transportation services across Indonesia’s cold chain logistics ecosystem.

By End-User Industry

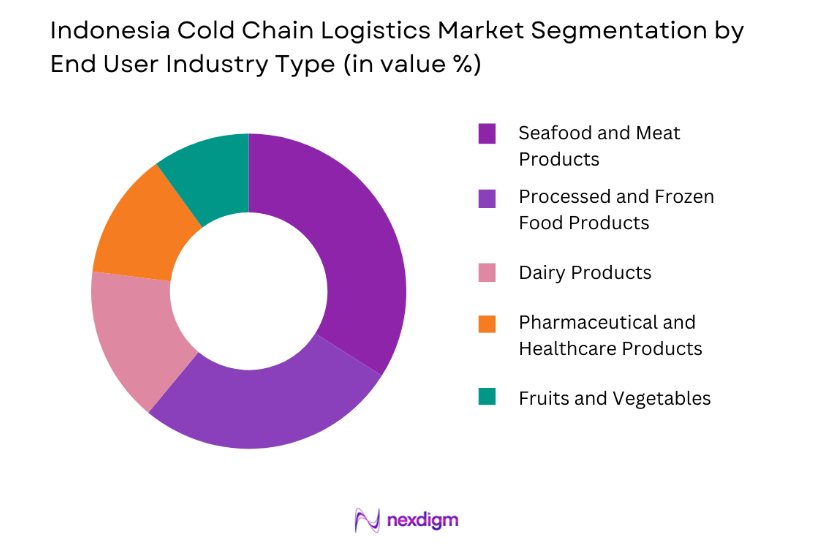

Indonesia Cold Chain Logistics Market is segmented by end-user industry into seafood and meat products, processed food and frozen food products, dairy products, pharmaceutical and healthcare products, and fruits and vegetables. Recently, seafood and meat products have a dominant market share due to Indonesia’s large fisheries industry and strong export demand for seafood products. The country ranks among the world’s major seafood producers, requiring extensive cold chain infrastructure for storage and export distribution. Fisheries processing facilities depend on refrigerated warehouses and transport systems to maintain freshness throughout supply chains. Growing international demand for frozen seafood products and expanding domestic consumption of processed meat products further increase reliance on refrigerated logistics systems across Indonesia’s food distribution networks.

Competitive Landscape

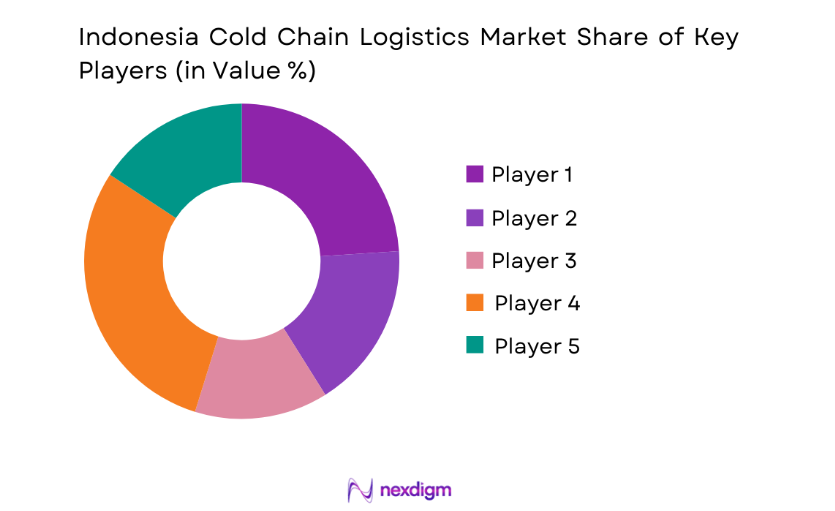

The Indonesia Cold Chain Logistics Market remains moderately fragmented with several regional logistics providers and international supply chain companies operating temperature-controlled infrastructure across the country. Large logistics firms focus on expanding refrigerated warehouse networks near major ports and urban consumption centers. Strategic partnerships between food distributors, seafood exporters, and logistics companies strengthen integrated cold chain distribution capabilities. Technology investments in real-time temperature monitoring, automated cold storage facilities, and digital logistics platforms increasingly differentiate major market participants competing for large-scale food and pharmaceutical distribution contracts.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Storage Capacity |

| Lineage Logistics | 2008 | United States | ~ | ~ | ~ | ~ | ~ |

| Nichirei Logistics Group | 1945 | Japan | ~ | ~ | ~ | ~ | ~ |

| Kiat Ananda Group | 1994 | Indonesia | ~ | ~ | ~ | ~ | ~ |

| Emergent Cold LatAm Asia | 2017 | Singapore | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

Indonesia Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Seafood Export and Fisheries Processing Infrastructure

Indonesia’s extensive fisheries industry significantly drives demand for cold chain logistics infrastructure because seafood exports require strict temperature-controlled storage and transportation systems to maintain product freshness and safety during international distribution. The country is among the world’s largest producers of tuna, shrimp, and other seafood products, which are exported to markets across Asia, North America, and Europe. Fisheries processing facilities rely heavily on blast freezing equipment, refrigerated storage warehouses, and specialized transportation services to preserve product quality. Government programs supporting fisheries modernization and export competitiveness encourage investment in cold storage infrastructure located near fishing ports and seafood processing hubs. Increasing global demand for frozen seafood products also strengthens the need for reliable refrigerated logistics services. Export-oriented seafood companies continue expanding processing plants and distribution facilities to support international trade. Cold chain logistics providers therefore invest in modern refrigerated warehouses and temperature-controlled container fleets to support growing seafood exports. These developments collectively reinforce the expansion of integrated cold chain logistics networks across Indonesia’s coastal production regions.

Rapid Expansion of Modern Retail and Frozen Food Distribution Channels

The expansion of modern retail networks across Indonesia significantly increases demand for refrigerated logistics services as supermarkets, hypermarkets, and convenience stores require reliable cold storage and transportation infrastructure to distribute perishable food products efficiently. Urban consumer demand for frozen foods, dairy products, and ready-to-eat meals continues rising as lifestyles become more convenience oriented. Food manufacturers and distributors rely on temperature-controlled warehouses and refrigerated truck fleets to maintain product quality across retail distribution networks. Large retail chains invest heavily in centralized cold storage distribution centers located near major metropolitan areas to support efficient supply chain management. E-commerce grocery platforms also require refrigerated logistics networks capable of handling perishable food delivery across urban markets. Logistics providers therefore expand refrigerated vehicle fleets, invest in warehouse automation technologies, and implement digital monitoring systems to ensure consistent temperature control during storage and transportation. The growing scale of modern retail food distribution across Indonesia strongly supports long-term expansion of the cold chain logistics sector.

Market Challenges

High Infrastructure Investment and Energy Consumption Costs

Developing cold chain logistics infrastructure requires substantial capital investment in refrigerated warehouses, blast freezing systems, and temperature-controlled transportation fleets, which creates financial barriers for logistics companies operating within Indonesia’s complex geographic landscape. Cold storage facilities require continuous electricity supply to maintain consistent temperatures, resulting in high energy consumption costs that significantly increase operating expenses for logistics providers. In many regions, electricity infrastructure remains inconsistent, forcing cold storage operators to rely on backup power generators to maintain refrigeration systems. These additional costs raise the overall operating expenditure associated with cold chain logistics operations. Small and medium-sized logistics companies often struggle to finance large-scale refrigeration infrastructure due to high equipment costs and long payback periods. Infrastructure development also requires specialized technical expertise to ensure proper maintenance of refrigeration systems and temperature monitoring technologies. These factors collectively slow the pace of cold chain infrastructure expansion in some regions of Indonesia.

Fragmented Logistics Infrastructure Across Indonesia’s Archipelagic Geography

Indonesia’s geographic structure as an archipelago consisting of thousands of islands presents significant logistical challenges for cold chain distribution networks that must transport perishable goods across long distances while maintaining strict temperature controls. Many smaller islands lack sufficient cold storage infrastructure, refrigerated transport fleets, and efficient port logistics systems required for handling perishable food products. Transportation delays caused by limited connectivity between islands increase the risk of product spoilage within food distribution supply chains. Logistics providers must therefore rely heavily on maritime transportation combined with refrigerated containers to distribute goods across remote regions. This fragmented infrastructure environment increases transportation complexity and operational costs. Companies often need to develop decentralized cold storage facilities near production clusters to maintain supply chain efficiency. As a result, building a fully integrated nationwide cold chain logistics network remains a complex operational challenge.

Opportunities

Expansion of Pharmaceutical and Vaccine Cold Chain Distribution Networks

The pharmaceutical sector increasingly requires advanced temperature-controlled logistics infrastructure to distribute vaccines, biologic medicines, and temperature-sensitive pharmaceutical products across Indonesia’s healthcare network. Hospitals, pharmaceutical distributors, and healthcare providers depend on specialized cold storage systems capable of maintaining precise temperature ranges required for medical product safety. Increasing demand for advanced biologic medicines and vaccination programs strengthens the need for pharmaceutical-grade cold chain infrastructure. Logistics companies therefore invest in specialized refrigerated storage facilities equipped with temperature monitoring technologies and regulatory compliance systems. Pharmaceutical manufacturers also partner with logistics providers to ensure reliable nationwide distribution networks for temperature-sensitive medicines. Expansion of healthcare infrastructure across Indonesia further supports the development of pharmaceutical cold chain logistics systems.

Development of Integrated Cold Chain Logistics Hubs Near Major Seaports

Indonesia’s growing food export industry creates opportunities for the development of large-scale integrated cold chain logistics hubs located near major seaports and export processing zones. Seafood exporters, agricultural producers, and food manufacturers require efficient cold storage facilities located close to shipping terminals to support international distribution. Logistics providers therefore invest in large refrigerated warehouses equipped with automated storage systems and container handling facilities. These hubs allow exporters to consolidate shipments and maintain product freshness before international transportation. Government infrastructure development programs supporting port modernization also create favorable conditions for expanding temperature-controlled logistics infrastructure. Integrated logistics hubs therefore play a critical role in strengthening Indonesia’s position within global food export supply chains.

Future Outlook

Indonesia’s cold chain logistics market is expected to experience steady expansion over the coming years as food consumption patterns shift toward frozen and processed products while pharmaceutical distribution networks expand nationwide. Technological advancements in temperature monitoring systems, warehouse automation, and refrigerated transport fleets will improve operational efficiency across logistics networks. Government infrastructure investment in ports, highways, and logistics corridors will support inter-island food distribution systems. Increasing seafood exports and modern retail expansion will further strengthen demand for temperature-controlled logistics infrastructure across Indonesia.

Major Players

- Lineage Logistics

- Nichirei Logistics Group

- Emergent Cold

- DHL Supply Chain

- Kiat Ananda Group

- Swire Cold Storage

- Americold Logistics

- Snowman Logistics

- Cold Chain Indonesia

- YCH Group

- DB Schenker

- CEVA Logistics

- Kuehne + Nagel

- Agility Logistics

- FedEx Logistics

Key Target Audience

- Cold chain logistics companies

- Food processing and seafood export companies

- Pharmaceutical distribution companies

- Retail and supermarket chains

- Investments and venture capitalist firms

- Government and regulatory bodies

- Warehouse infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying critical variables influencing the Indonesia Cold Chain Logistics Market including refrigerated infrastructure capacity, transportation networks, seafood exports, pharmaceutical distribution, and retail food supply chains. These factors are analyzed to understand the structural dynamics influencing demand for cold chain logistics services across the country.

Step 2: Market Analysis and Construction

Market structure is constructed using industry databases, government publications, logistics trade associations, and corporate financial reports. Cold storage infrastructure capacity, logistics investments, and food distribution data are integrated to estimate the overall market size and competitive ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics operators, food exporters, and supply chain professionals are consulted to validate assumptions regarding market demand patterns, infrastructure development trends, and logistics technology adoption across Indonesia’s cold chain ecosystem.

Step 4: Research Synthesis and Final Output

Collected data and validated insights are synthesized to develop a comprehensive market report covering industry structure, segmentation analysis, competitive landscape, and future growth opportunities within Indonesia’s cold chain logistics market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Seafood and Agricultural Export Supply Chains

Growing Demand for Temperature Controlled Pharmaceutical Distribution

Rapid Growth of Frozen Food and Processed Food Consumption - Market Challenges

High Infrastructure Costs for Cold Storage Development

Limited Refrigerated Transport Capacity Across Remote Islands

Energy Consumption and Power Supply Constraints for Cold Facilities - Market Opportunities

Expansion of Vaccine and Pharmaceutical Cold Chain Infrastructure

Development of Cold Chain Logistics for E Commerce Grocery Delivery

Investment in Smart Cold Storage and Temperature Monitoring Technologies - Trends

Adoption of IoT Enabled Temperature Monitoring Systems

Integration of Automated Cold Storage Warehousing Technologies - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Warehousing Services

Temperature Controlled Transportation Services

Cold Storage Distribution Centers

Pharmaceutical Cold Chain Logistics Services

Integrated Cold Chain Monitoring Solutions - By Platform Type (In Value%)

Road Refrigerated Transport Logistics

Sea Freight Refrigerated Container Logistics

Air Cargo Cold Chain Logistics

Inter Island Refrigerated Shipping Logistics - By Fitment Type (In Value%)

Standalone Cold Storage Facilities

Integrated Cold Logistics Hub Facilities

Mobile Refrigeration Transport Units

Modular Cold Storage Infrastructure - By End User Segment (In Value%)

Food and Beverage Processing and Distribution Companies

Pharmaceutical and Biotechnology Companies

Retail and Supermarket Chains

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Temperature Range Capability, Warehouse Automation Level, Geographic Distribution Coverage, Real Time Temperature Monitoring Systems, Pharmaceutical Compliance Certification)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain Indonesia

DB Schenker Indonesia

Kuehne + Nagel Indonesia

CEVA Logistics Indonesia

DSV Indonesia

Yusen Logistics Indonesia

Nippon Express Indonesia

Agility Logistics Indonesia

CJ Logistics Indonesia

Samudera Indonesia Logistics

Wahana Prestasi Logistik

RPX Logistics

Pos Logistics Indonesia

JNE Logistics

SiCepat Ekspres Logistics

- Seafood Exporters Increasing Demand for Temperature Controlled Logistics

- Pharmaceutical Companies Expanding Cold Chain Distribution Networks

- Retail Supermarket Chains Expanding Frozen Food Distribution Systems

- Food Processing Companies Requiring Reliable Refrigerated Storage Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now