Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Indonesia Diagnostic Labs Market is projected to experience substantial growth, driven by increasing healthcare investments and advancements in diagnostic technologies. The market is fueled by the rising demand for accurate and timely diagnostic services across the healthcare sector, primarily supported by both public and private sector investments in healthcare infrastructure. The market size is valued at USD ~ billion, driven by the expansion of medical facilities and increasing adoption of automated diagnostic systems, improving healthcare delivery efficiency.

In terms of geographic dominance, major cities such as Jakarta, Surabaya, and Medan lead the market, driven by their dense population and well-established healthcare infrastructure. Jakarta, being the capital, hosts a significant portion of diagnostic labs due to its concentration of healthcare providers and government-funded health programs. Surabaya, with its growing healthcare services, and Medan, benefiting from both urbanization and regional healthcare development, further contribute to the strong market presence in these areas.

Market Segmentation

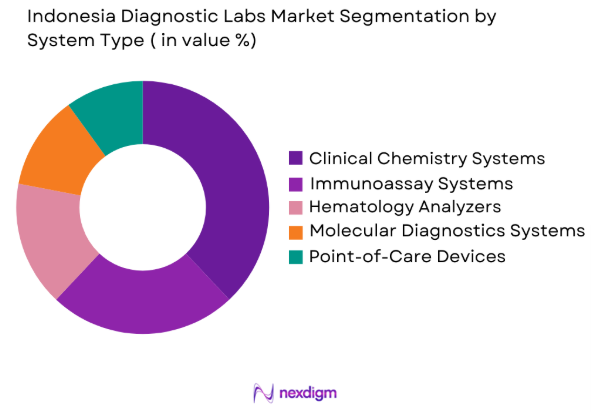

By System Type

The Indonesia Diagnostic Labs market is segmented by system type into clinical chemistry systems, immunoassay systems, hematology analyzers, molecular diagnostics systems, and point-of-care devices. Recently, clinical chemistry systems have dominated the market share due to their widespread application in routine clinical practices, offering a reliable and cost-effective approach to diagnosing diseases such as diabetes, kidney disorders, and liver diseases. The increase in patient testing, advancements in automation, and the growing demand for lab testing services drive the demand for these systems, strengthening their dominant position.

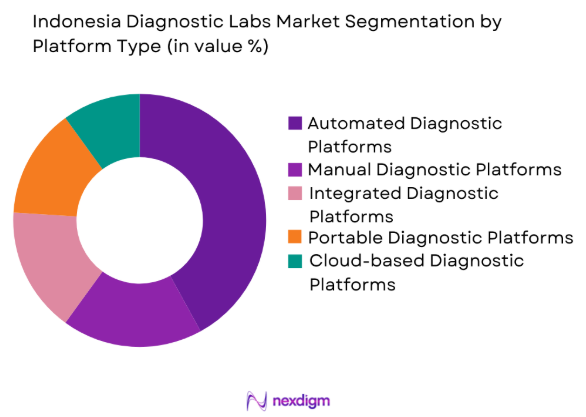

By Platform Type

The market is segmented by platform type into automated diagnostic platforms, manual diagnostic platforms, integrated diagnostic platforms, portable diagnostic platforms, and cloud-based diagnostic platforms. Automated diagnostic platforms have captured the largest share due to their efficiency in handling high volumes of tests, reducing human errors, and offering rapid test results. These platforms are crucial for diagnostic labs aiming to streamline operations and improve diagnostic throughput, especially in large healthcare institutions where quick and accurate results are essential for patient care.

Competitive Landscape

The Indonesia Diagnostic Labs market exhibits a competitive landscape driven by both local and global players, with several companies consolidating their positions through strategic partnerships and technological innovations. These players are investing in the development of advanced diagnostic solutions, with a focus on improving testing accuracy, reducing turnaround times, and enhancing patient care. The competitive pressure is also intensified by regulatory requirements, technological integration, and cost efficiency, influencing major players’ market strategies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Ireland | ~ | ~ | ~ | ~ | ~ |

| Sysmex Corporation | 1968 | Japan | ~ | ~ | ~ | ~ | ~ |

Indonesia Diagnostic Labs Market Analysis

Growth Drivers

Increasing Healthcare Investments

Indonesia’s government and private sector are increasing investments in healthcare infrastructure, driving the demand for diagnostic services. This includes expanding medical facilities, introducing advanced diagnostic tools, and improving healthcare standards nationwide. The growth of diagnostic labs, especially in rural and semi-urban areas, is further supporting this trend. With the expanding middle class and improved access to healthcare, there is a rising demand for routine diagnostics and preventive services. Healthcare sector growth, along with technological advancements, is fueling the expansion of diagnostic labs, enhancing patient outcomes. Additionally, increased healthcare spending promotes innovation in automated diagnostic equipment and digital health solutions, accelerating market growth.

Technological Advancements in Diagnostics

The Indonesia Diagnostic Labs Market is experiencing significant growth due to technological advancements, including automation, artificial intelligence (AI), and big data integration. Automation enhances laboratory efficiency, increases throughput, and reduces human error, resulting in more accurate and faster results. AI-powered diagnostic tools enable earlier disease detection, improving treatment outcomes. Additionally, cloud-based platforms support remote diagnostics, enabling healthcare providers to serve underserved areas. These technologies have transformed traditional diagnostic methods and are central to the modernization of healthcare. Continuous innovation in diagnostics, along with the increasing demand for personalized medicine, positions technological advancements as a major driver of growth in the market.

Market Challenges

Regulatory Complexity

Indonesia’s diagnostic labs market faces several regulatory challenges, including complex and evolving regulations around medical device approvals and lab certifications. Regulatory requirements are often difficult to navigate, especially for new players entering the market. Compliance with local and international standards for quality assurance and safety protocols is a significant hurdle. The regulatory landscape is further complicated by varying standards across different regions of the country, resulting in delays in the approval process and increasing the operational costs for diagnostic labs. Furthermore, stringent data privacy regulations, particularly concerning patient information, pose a challenge for the widespread adoption of digital health and telemedicine solutions. These regulatory complexities hinder market growth, particularly for small and mid-sized labs looking to expand their operations.

High Initial Investment Costs

Establishing and operating a diagnostic lab requires significant capital investment in advanced diagnostic equipment, infrastructure, and skilled personnel. The high cost of setting up automated systems, molecular diagnostic tools, and quality control mechanisms often discourages smaller players and new entrants from joining the market. Additionally, the costs associated with ongoing maintenance, training, and upgrading of diagnostic tools put further financial pressure on labs. For smaller healthcare providers in rural or underdeveloped regions, the high capital requirement remains a significant barrier to entry, limiting the availability of modern diagnostic services across Indonesia. The financial constraints of these healthcare providers create an uneven distribution of diagnostic services, with urban areas benefiting more from the advancements in the market than rural regions.

Opportunities

Expansion of Point-of-Care Solutions

The increasing demand for accessible healthcare, particularly in rural and remote areas, presents a major opportunity for the Indonesia Diagnostic Labs market. Point-of-care (POC) testing solutions allow for rapid and accurate diagnostics outside of traditional laboratory settings, making them ideal for use in rural healthcare centers, clinics, and even at-home settings. These solutions offer cost-effective and quick testing, improving patient outcomes by enabling immediate medical interventions. The rise in chronic diseases such as diabetes and hypertension, which require frequent monitoring, further drives the demand for POC devices. Additionally, the ongoing development of portable diagnostic devices and mobile health applications presents opportunities for the expansion of healthcare services to underserved areas, making diagnostic services more accessible to the broader population.

Integration of Digital Health Technologies

The growing trend of digital health technologies, including telemedicine, mobile health apps, and AI-based diagnostics, presents a lucrative opportunity for the Indonesia Diagnostic Labs market. These technologies allow for the remote diagnosis and monitoring of patients, improving access to healthcare services in rural areas where diagnostic labs may be limited. By integrating digital platforms with diagnostic labs, patients can receive real-time results, consultations, and follow-ups without needing to visit the lab in person. This integration also enables a more holistic approach to patient care, as data can be shared seamlessly between healthcare providers, leading to better collaboration and more accurate diagnoses. As the adoption of digital health solutions increases, diagnostic labs that incorporate these technologies are poised for significant growth.

Future Outlook

The future outlook for the Indonesia Diagnostic Labs market is highly positive, with expected growth driven by continued investments in healthcare infrastructure, technological innovations, and the adoption of digital health solutions. The ongoing expansion of diagnostic services, particularly in underserved areas, combined with the increasing demand for advanced diagnostic technologies such as AI-powered diagnostics and molecular testing, will further fuel market growth. Government initiatives aimed at improving healthcare accessibility and quality will also play a pivotal role in shaping the future of diagnostic labs in Indonesia. Over the next few years, the market will likely witness the development of more affordable and efficient diagnostic solutions, along with greater integration of digital platforms, further enhancing healthcare delivery.

Major Players

- Siemens Healthineers

- Roche Diagnostics

- Abbott Laboratories

- Medtronic

- Sysmex Corporation

- Bio-Rad Laboratories

- ThermoFisher Scientific

- Mindray

- GE Healthcare

- PerkinElmer

- Danaher Corporation

- Agilent Technologies

- Fujifilm Holdings Corporation

- Becton Dickinson

- Horiba Ltd

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers and diagnostic labs

- Medical device manufacturers

- Health insurance companies

- Digital health technology providers

- Pharmaceutical companies

- Medical research institutions

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the key variables impacting the market, including market drivers, restraints, opportunities, and challenges.

Step 2: Market Analysis and Construction

This step involves collecting and analyzing data on market size, trends, competitive landscape, and segment performance to build a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through expert consultations with industry leaders, stakeholders, and market participants to refine insights.

Step 4: Research Synthesis and Final Output

The final output synthesizes all research findings, providing actionable insights for market participants to make informed decisions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Healthcare Investments

Technological Advancements in Diagnostic Systems

Government Initiatives to Improve Healthcare Infrastructure - Market Challenges

Regulatory Complexity in Diagnostic Labs

High Initial Capital Investment for Diagnostic Systems

Lack of Skilled Workforce in Diagnostics - Market Opportunities

Expansion of Home Healthcare and Point-of-Care Solutions

Integration of AI and Big Data in Diagnostic Systems

Rising Demand for Molecular Diagnostics - Trends

Adoption of AI-Driven Diagnostic

ToolsGrowing Focus on Early Disease Detection

Shift Towards Remote Diagnostics - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Systems

Immunoassay Systems

Hematology Analyzers

Molecular Diagnostics Systems

Point-of-Care Devices - By Platform Type (In Value%)

Automated Diagnostic Platforms

Manual Diagnostic Platforms

Integrated Diagnostic Platforms

Portable Diagnostic Platforms

Cloud-Based Diagnostic Platforms - By Fitment Type (In Value%)

On-premise Systems

Cloud-Based Systems

Hybrid Systems

Portable Systems

Laboratory-Integrated Systems - By End User Segment (In Value%)

Hospitals

Clinical Laboratories

Research Institutions

Home Healthcare Providers

Public Health Institutions - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Integration, Diagnostic Accuracy, Cost Efficiency, Regulatory Compliance, Market Reach)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

PT Kalbe Farma Tbk

Medion Healthcare

Siemens Healthineers

Thermo Fisher Scientific

Roche Diagnostics

Abbott Laboratories

GE Healthcare

PerkinElmer

Mindray

Sysmex Corporation

Bio-Rad Laboratories

Danaher Corporation

Agilent Technologies

Fujifilm Holdings Corporation

Becton Dickinson

Horiba Ltd

- Growing Demand for Diagnostic Testing in Rural Areas

- Increased Adoption of Molecular Diagnostics in Hospitals

- Shift Towards Home-Based Diagnostics

- Rise in Research Institutions Focusing on Healthcare Innovations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now