Download PDF

Download PDF Download PDF

Download PDF- Automotive manufacturers

- Battery manufacturers

- Electric vehicle component suppliers

- Charging infrastructure developers

- Logistics and fleet operators

- Investment and venture capitalist firms

- Government and regulatory bodies

- Energy utilities and grid operators

Market Overview

The Indonesia Electric Vehicle Market has reached an approximate valuation of USD ~ billion based on a recent historical assessment, reflecting accelerating adoption of electrified mobility solutions supported by national decarbonization policies and industrial strategy focused on battery production. Government-backed EV ecosystem development, rising urban air quality concerns, domestic nickel reserves enabling battery manufacturing, and expanding charging infrastructure have significantly strengthened demand for electric two-wheelers, passenger vehicles, and electric buses across urban mobility systems and logistics applications.

Jakarta, Surabaya, and Bandung act as the most influential electric mobility hubs due to higher urban density, strong purchasing capacity, and early infrastructure deployment supported by municipal electrification programs. These cities host most charging networks, EV pilot fleets, and policy incentives that accelerate adoption among private consumers and ride-hailing operators. Industrial clusters in West Java and Sulawesi also support dominance by integrating battery supply chains, vehicle assembly plants, and technology partnerships that strengthen domestic EV manufacturing capacity.

Market Segmentation

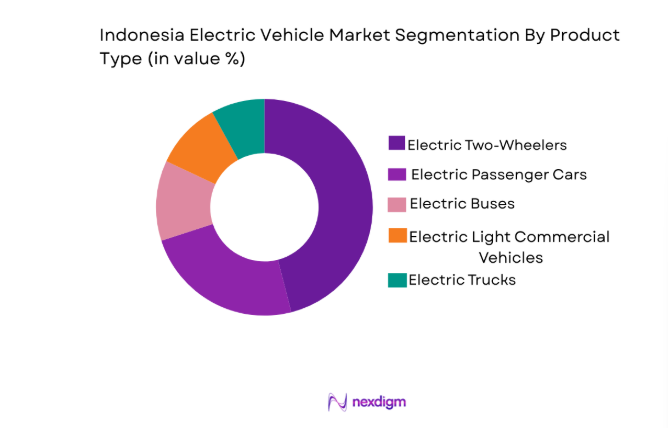

By Product Type

Indonesia Electric Vehicle market is segmented by product type into electric two-wheelers, electric passenger cars, electric buses, electric light commercial vehicles, and electric trucks. Recently, electric two-wheelers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. Two-wheelers represent the backbone of daily mobility across Indonesian urban regions where affordability, parking flexibility, and operational cost efficiency drive widespread adoption among commuters and delivery fleets. Rapid electrification programs for ride-hailing platforms and courier services have further accelerated electric motorcycle demand as operators seek lower fuel expenditure and regulatory compliance with urban emission policies. Domestic manufacturers and international partnerships have expanded product offerings, improving battery durability and charging convenience, which increases consumer confidence in electric mobility solutions. Government subsidies and battery swap infrastructure programs have also played a critical role in encouraging electric two-wheeler purchases. In addition, urban congestion and fuel cost fluctuations have reinforced consumer preference toward compact electric mobility solutions, positioning electric two-wheelers as the most accessible and scalable EV category in Indonesia’s transportation landscape.

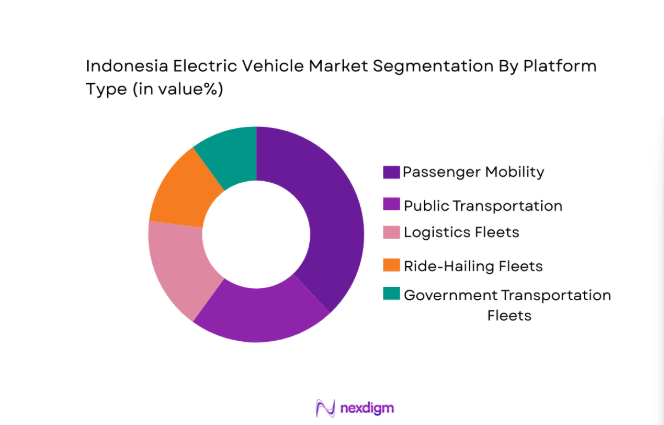

By Platform Type

Indonesia Electric Vehicle market is segmented by platform type into passenger mobility, public transportation, logistics fleets, ride-hailing fleets, and government transportation fleets. Recently, passenger mobility has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. Personal vehicle electrification is accelerating as middle-income urban consumers increasingly adopt electric vehicles to reduce fuel expenditure and benefit from policy incentives introduced to support low-emission transport systems. Expansion of EV charging infrastructure in residential complexes, commercial buildings, and transport corridors has also improved convenience for private vehicle owners. Domestic automotive manufacturers and global EV brands entering the Indonesian market have expanded product portfolios that cater to multiple price segments, enabling broader consumer adoption. Consumer awareness of sustainability and long-term operating cost advantages further strengthens the demand for personal electric vehicles. Ride-hailing operators and leasing companies also contribute indirectly by introducing electric vehicles into consumer mobility ecosystems, familiarizing users with EV technology and increasing confidence among private buyers.

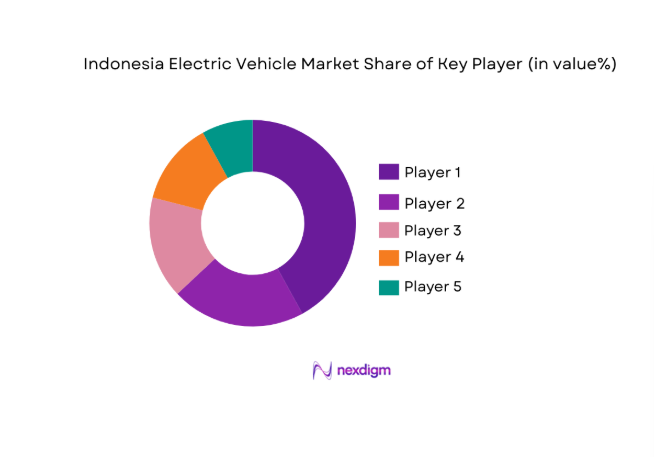

Competitive Landscape

The Indonesia Electric Vehicle market demonstrates a moderately consolidated competitive structure where global automotive manufacturers collaborate with domestic industrial players to establish EV manufacturing and battery production capabilities. Strategic investments in battery supply chains, charging infrastructure partnerships, and localized vehicle assembly have intensified competition. Major manufacturers focus on affordable EV models, battery technology partnerships, and ecosystem integration to strengthen market presence while responding to regulatory incentives supporting domestic EV adoption.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Battery Integration Capability |

| Tesla | 2003 | USA | ~ | ~ | ~ | ~ | ~ |

| BYD | 1995 | China | ~ | ~ | ~ | ~ | ~ |

| Hyundai Motor | 1967 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Toyota Motor | 1937 | Japan | ~ | ~ | ~ | ~ | ~ |

| Wuling Motors | 2002 | China | ~ | ~ | ~ | ~ | ~ |

Indonesia Electric Vehicle Market Analysis

Growth Drivers

Government-Led EV Ecosystem Development and Industrial Policy Support

Indonesia’s electric vehicle market expansion is strongly driven by national policies designed to transform the country into a global electric mobility manufacturing hub leveraging its vast nickel reserves used in lithium battery production. The government has implemented incentives including tax exemptions for EV buyers, reduced import duties for EV components, and regulatory frameworks encouraging domestic manufacturing investment. These policy mechanisms are complemented by state-supported infrastructure programs aimed at deploying public charging stations and battery swapping networks across major metropolitan regions. Industrial partnerships between Indonesian state enterprises and global automotive manufacturers have accelerated the localization of EV production, allowing manufacturers to reduce logistics costs and expand supply capacity within the domestic market. The government has also launched electrification initiatives targeting public transportation fleets and government vehicles, further stimulating EV demand. Strategic collaboration between mining companies, battery producers, and vehicle manufacturers strengthens the upstream supply chain necessary for EV ecosystem development. Infrastructure investments, combined with consumer incentives and industrial localization policies, significantly reduce market barriers for EV adoption. These initiatives also encourage private investment into charging networks, battery technology development, and EV assembly plants. As a result, the Indonesian electric vehicle sector is transitioning from an import-dependent market toward a vertically integrated manufacturing ecosystem capable of supporting large-scale domestic EV deployment and export potential across Southeast Asia.

Rapid Urbanization and Rising Urban Mobility Electrification Demand

Indonesia’s rapid urban population expansion has intensified transportation demand across metropolitan regions, creating structural pressure to adopt efficient and environmentally sustainable mobility solutions. Increasing congestion, urban air pollution, and fuel cost volatility are encouraging both policymakers and consumers to explore alternatives to conventional internal combustion engine vehicles. Electric vehicles offer significant advantages in operating cost efficiency, reduced emissions, and compatibility with emerging smart city initiatives implemented in major Indonesian urban centers. Ride-hailing companies and logistics operators are rapidly transitioning parts of their fleets toward electrified vehicles to reduce operational expenses associated with fuel consumption and vehicle maintenance. Urban delivery services, food logistics platforms, and e-commerce operators increasingly prefer electric two-wheelers and compact electric vans to optimize last-mile distribution networks. Public transport electrification programs, particularly electric bus deployments in major cities, also contribute to increasing EV adoption across mobility ecosystems. Consumer awareness regarding environmental sustainability has grown significantly, encouraging urban households to consider EV ownership as a long-term economic and ecological investment. Additionally, digital mobility platforms that integrate EV leasing, ride-sharing services, and battery swap infrastructure are making electric vehicles more accessible to urban users. These developments collectively create a structural shift toward electric mobility solutions that align with Indonesia’s broader energy transition strategy and urban transportation modernization efforts.

Market Challenges

Limited Nationwide Charging Infrastructure and Grid Readiness Constraints

One of the most critical challenges affecting Indonesia’s electric vehicle market is the uneven distribution of charging infrastructure across the country, particularly outside major metropolitan regions. While Jakarta and several large cities have begun establishing EV charging corridors, many suburban and rural areas still lack sufficient charging networks to support widespread EV usage. This infrastructure gap creates range anxiety among consumers and discourages potential buyers who rely on reliable long-distance travel capabilities. Additionally, the national electricity grid requires upgrades in several regions to accommodate increased electricity demand from EV charging stations and large-scale fleet electrification. Power distribution limitations, particularly in remote regions, restrict the rapid deployment of fast-charging stations necessary for commercial EV adoption. Infrastructure expansion also requires substantial capital investment from both public authorities and private sector energy companies. Regulatory coordination between power utilities, transport authorities, and infrastructure developers remains essential to accelerate charging network deployment. Battery swapping solutions for two-wheelers have emerged as a partial solution but still require standardized battery systems across manufacturers. Until a dense and reliable charging ecosystem is established nationwide, EV adoption may remain concentrated primarily in urban areas rather than expanding uniformly across Indonesia’s transportation system.

High Initial Vehicle Costs and Consumer Affordability Barriers

Despite long-term operational savings associated with electric vehicles, the relatively high upfront purchase cost continues to act as a major barrier to mass consumer adoption in Indonesia. Electric vehicles remain more expensive than comparable internal combustion engine vehicles due to battery manufacturing costs, imported technology components, and limited economies of scale in domestic production. Many middle-income consumers still prioritize affordability when purchasing vehicles, which slows the transition toward electric mobility despite government incentives. Financing institutions are gradually introducing EV-specific loan products and leasing options, but consumer awareness and accessibility remain limited outside major urban markets. Battery replacement costs also contribute to consumer concerns regarding long-term ownership expenses, particularly for private vehicle buyers unfamiliar with EV maintenance structures. Automotive manufacturers are working to reduce vehicle costs through localized assembly and partnerships with battery producers, but price parity with conventional vehicles has not yet been fully achieved across all EV categories. Additionally, fluctuations in raw material prices such as lithium and nickel can influence battery manufacturing costs and vehicle pricing. Addressing affordability barriers through localized manufacturing, financing innovation, and subsidy programs remains essential to accelerate large-scale EV adoption in Indonesia.

Opportunities

Domestic Battery Manufacturing Expansion Leveraging Nickel Supply Chains

Indonesia holds one of the world’s largest nickel reserves, positioning the country as a strategic hub for lithium-ion battery production essential for electric vehicle manufacturing. This resource advantage creates a major opportunity to develop a vertically integrated EV supply chain that includes mining, battery processing, cell manufacturing, and vehicle assembly. Large international battery manufacturers and automotive companies are investing in joint ventures to establish battery production facilities within Indonesia, strengthening domestic industrial capabilities. These investments reduce dependency on imported battery components while enabling the country to become a regional export hub for EV batteries and energy storage technologies. The development of battery recycling infrastructure also presents long-term opportunities for sustainable material recovery and cost optimization. As battery manufacturing capacity expands domestically, EV manufacturers will gain access to more affordable battery supply, lowering vehicle production costs and accelerating adoption.

Electric Fleet Electrification Across Logistics and Ride-Hailing Platforms

Rapid growth in Indonesia’s digital economy has significantly increased demand for logistics and ride-hailing services that rely heavily on motorized transportation fleets. Electrifying these fleets represents a major opportunity to scale EV adoption quickly due to the high daily utilization rates of commercial vehicles. Delivery companies, ride-hailing operators, and e-commerce platforms are increasingly exploring EV integration to reduce fuel costs and comply with environmental regulations introduced in urban regions. Battery swapping models and leasing arrangements allow fleet operators to transition toward electric vehicles without large upfront investments. Government incentives supporting commercial fleet electrification further strengthen this opportunity by lowering operating costs and encouraging private sector adoption. As logistics and mobility platforms continue expanding across Indonesian cities, electric fleet deployment will likely become a critical driver of EV market growth.

Future Outlook

The Indonesia Electric Vehicle market is expected to experience strong expansion driven by increasing infrastructure investment, battery manufacturing growth, and supportive government policies encouraging low-emission transportation systems. Continued partnerships between global EV manufacturers and domestic industrial players will accelerate local production capabilities. Charging infrastructure expansion, battery technology improvements, and fleet electrification programs are expected to further stimulate demand across both private and commercial mobility segments.

Major Players

- Tesla

- BYD

- Hyundai Motor

- Toyota Motor

- SAIC Motor

- Nissan Motor

- Mitsubishi Motors

- Wuling Motors

- VinFast

- BMW Group

- Mercedes-Benz Group

- Geely Auto

- Honda Motor

- Kia Corporation

- Chery Automobile

Key Target Audience

Research Methodology

Step 1: Identification of Key Variables

Primary variables including vehicle demand patterns, charging infrastructure availability, battery production capacity, and policy incentives are identified. These variables define the structural components influencing EV adoption within the Indonesian mobility ecosystem.

Step 2: Market Analysis and Construction

Data from industry reports, government policy documents, corporate disclosures, and automotive industry databases are analyzed to construct the market framework and estimate demand patterns across vehicle categories.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, EV manufacturers, energy providers, and mobility service operators are consulted to validate assumptions regarding technology adoption, infrastructure deployment, and market growth trajectories.

Step 4: Research Synthesis and Final Output

All validated data sources are synthesized to produce the final market insights, including segmentation, competitive landscape evaluation, and long-term market outlook assessments.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government incentives for electric vehicles

Increasing environmental awareness

Technological advancements in battery systems

Rising fuel prices and fuel shortages

Improved charging infrastructure - Market Challenges

High upfront costs of electric vehicles

Limited charging infrastructure in rural areas

Battery disposal and recycling concerns

Supply chain disruptions for EV parts

Resistance to change in traditional vehicle markets - Market Opportunities

Expansion of electric bus fleets

Partnerships between government and private players

Growing demand for electric two-wheelers in urban areas - Trends

Development of fast-charging technologies

Rise of battery leasing models

Increased focus on autonomous electric vehicles

Adoption of renewable energy for charging stations

Growth in local EV manufacturing - Government Regulations & Defense Policy

Government incentives for electric vehicle adoption

Regulations on emissions and vehicle standards

Import duties and taxes for electric vehicle parts - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Vehicles

Plug-in Hybrid Electric Vehicles

Hybrid Electric Vehicles

Electric Two-Wheelers

Electric Buses - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Public Transport Vehicles

Two-Wheelers

Electric Buses - By Fitment Type (In Value%)

Original Equipment Manufacturer (OEM)

Aftermarket Solutions

Integrated Systems

Modular Systems

Custom Fitments - By End User Segment (In Value%)

Private Owners

Fleet Operators

Government Agencies

Ride-sharing Services

Logistics Providers - By Procurement Channel (In Value%)

Direct Sales

Government Tenders

Dealers & Distributors

Online Platforms

Corporate Procurement

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Battery technology, Platform type, Fitment type, End User segment, Procurement channel, Material/Technology)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tesla

BYD

Nissan

BMW

Honda

Toyota

LG Chem

Volkswagen

Hyundai

Ford

General Motors

Rivian

Lucid Motors

Xpeng Motors

Geely

- Private owners looking for eco-friendly alternatives

- Fleet operators’ focus on cost-efficiency

- Government agencies pushing for greener transportation

- Ride-sharing services adopting electric vehicles for sustainability

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

The Indonesia Electric Vehicle Market is valued at approximately USD ~ billion based on recent industry assessments and national EV deployment data. The market includes electric two-wheelers, passenger vehicles, buses, and commercial EV platforms supported by government electrification policies.

Growth of the Indonesia Electric Vehicle Market is primarily driven by strong government incentives, battery manufacturing investments, and increasing urban mobility electrification initiatives. Expansion of charging infrastructure and partnerships with global EV manufacturers further strengthen the market ecosystem.

Electric two-wheelers currently dominate the Indonesia Electric Vehicle Market due to affordability, urban commuting convenience, and high adoption among ride-hailing and delivery services. Their operational cost advantages and battery swapping solutions also accelerate adoption.

Major urban centers such as Jakarta, Surabaya, and Bandung lead adoption in the Indonesia Electric Vehicle Market due to charging infrastructure availability, consumer purchasing power, and early EV policy implementation programs.

Key companies operating in the Indonesia Electric Vehicle Market include Tesla, BYD, Hyundai Motor, Toyota Motor, Wuling Motors, and several international EV manufacturers collaborating with Indonesian industrial partners.

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now