Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Indonesia home finance market reached approximately USD ~ billion in outstanding residential mortgage value based on Bank Indonesia financial stability statistics and Financial Services Authority housing finance disclosures. Market expansion is driven by large-scale subsidized housing credit programs, rapid urban household formation, and increasing banking sector penetration of long-tenor mortgages across middle-income borrowers. State housing liquidity facilities and interest subsidy schemes have expanded loan affordability, while commercial banks have increased mortgage allocation within retail lending portfolios to support sustained residential financing growth.

Jakarta metropolitan region dominates Indonesia home finance activity due to the country’s largest concentration of formal employment, banking infrastructure, and residential property development supported by extensive urban transport connectivity and income levels exceeding national averages. Surrounding West Java cities including Bekasi, Bogor, and Depok show strong mortgage uptake driven by suburban housing expansion and commuter demand. Secondary urban centers such as Surabaya and Bandung also exhibit high financing volumes because of industrial employment bases, developer-led housing supply, and regional banking network presence facilitating mortgage accessibility.

Market Segmentation

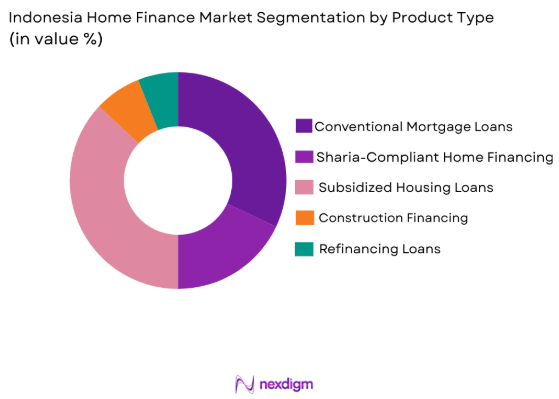

By Product Type

Indonesia home finance market is segmented by product type into conventional mortgage loans, Sharia-compliant home financing, subsidized housing loans, construction financing, and refinancing loans. Recently, subsidized housing loans has a dominant market share due to factors such as government affordability programs, large low-income borrower base, nationwide developer participation, and state-backed interest subsidy infrastructure that lowers repayment burden and expands credit eligibility across first-time homebuyers in urbanizing regions where formal mortgage affordability remains constrained.

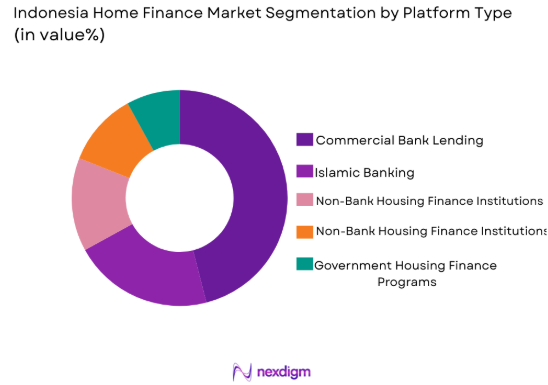

By Platform Type

Indonesia home finance market is segmented by platform type into commercial bank lending, Islamic banking, non-bank housing finance institutions, digital mortgage platforms, and government housing finance programs. Recently, commercial bank lending has a dominant market share due to extensive branch distribution, stable funding bases from deposits, regulatory mortgage prioritization, and deep partnerships with large property developers that streamline loan origination and property verification processes across major urban housing corridors.

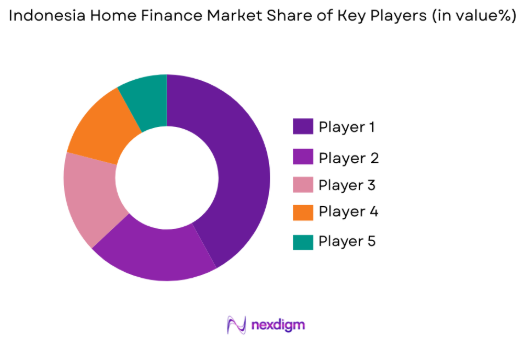

Competitive Landscape

Indonesia home finance market exhibits moderate concentration with large state-owned banks and leading private banks controlling the majority of mortgage portfolios supported by strong deposit funding and developer alliances. Islamic banking institutions maintain growing participation through Sharia-compliant financing products, while specialized housing finance and secondary mortgage entities support liquidity. Competitive dynamics are shaped by interest subsidy distribution, branch reach, and digital origination capability across urban growth regions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio Strength |

| Bank Tabungan Negara | 1897 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| Bank Mandiri | 1998 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| Bank Rakyat Indonesia | 1895 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| Bank Central Asia | 1957 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| Bank Syariah Indonesia | 2021 | Jakarta | ~ | ~ | ~ | ~ | ~ |

Indonesia Home Finance Market Analysis

Growth Drivers

Government-Subsidized Housing Credit Expansion and Urban Household Formation

Indonesia home finance growth is strongly anchored in large-scale state housing subsidy frameworks that lower mortgage interest rates and down-payment requirements for low-income households, enabling millions of first-time borrowers to access formal housing finance through regulated banking channels. Rapid urbanization and demographic expansion continue to generate new household formation across metropolitan regions where residential ownership remains a primary wealth objective, increasing structural demand for long-tenor mortgage lending supported by developer-bank partnerships. Subsidized liquidity facilities provided to banks reduce funding cost and credit risk exposure, encouraging lenders to expand mortgage allocation within retail loan portfolios and extend financing into emerging peri-urban housing corridors. Government housing programs integrate land allocation, developer incentives, and mortgage eligibility criteria to create coordinated supply and financing pipelines that stabilize loan origination volumes even during economic cycles. Commercial banks benefit from predictable borrower flows linked to public housing schemes, enabling scale efficiencies in underwriting, valuation, and servicing processes across standardized housing units targeted at low- and middle-income populations. State-owned housing banks maintain nationwide branch networks that penetrate secondary cities and provincial regions, extending mortgage accessibility beyond major urban centers where formal banking reach historically limited housing finance penetration. Continued expansion of affordable housing developments around urban employment clusters sustains collateral availability and borrower demand simultaneously, reinforcing structural mortgage growth momentum. Mortgage tenors extending beyond fifteen years improve affordability metrics for borrowers with moderate incomes, expanding eligibility and sustaining repayment performance across subsidized loan cohorts.

Banking Sector Mortgage Penetration and Middle-Income Housing Demand Expansion

Indonesia home finance market expansion is further driven by commercial banking sector strategy to increase mortgage penetration within consumer lending portfolios as retail credit diversification reduces reliance on short-term consumer loans and improves asset stability through long-duration secured lending. Rising middle-income populations with stable salaried employment seek formal homeownership in urban and suburban residential developments, generating sustained demand for conventional mortgage products aligned with long-term wealth accumulation and housing security objectives. Banks actively expand mortgage offerings through competitive interest structures, developer tie-ups, and bundled financial products that incentivize housing purchases within newly built residential clusters near transport and industrial zones. Mortgage underwriting frameworks have improved through credit scoring integration, property valuation standardization, and digital documentation processes that reduce processing time and expand borrower onboarding capacity across growing urban populations. Expansion of private housing supply by large developers creates continuous inventory of mortgage-eligible residential units targeted at middle-income buyers whose purchasing power exceeds subsidized housing thresholds yet remains dependent on bank financing. Financial sector regulatory support encourages prudent mortgage growth by maintaining capital adequacy and loan-to-value frameworks that sustain credit expansion while preserving banking stability. Increasing housing price levels in major cities make mortgage financing essential for ownership acquisition, reinforcing structural dependence on banking sector home loans across emerging middle-class households. Competitive differentiation among banks through service quality, digital channels, and developer ecosystems further accelerates mortgage adoption across urbanizing regions with rising income stability.

Market Challenges

High Informal Employment and Income Verification Constraints

Indonesia home finance market faces structural constraints from large informal employment segments where income documentation remains limited, reducing borrower eligibility under regulated banking credit assessment frameworks that rely on verifiable salary records and tax documentation for mortgage underwriting. A significant portion of the workforce operates in microenterprise, self-employment, or informal labor arrangements without stable payslips or audited financial statements, preventing banks from accurately assessing repayment capacity and credit risk for long-tenor housing loans. Mortgage lenders maintain conservative underwriting standards to preserve asset quality and regulatory compliance, excluding many potential borrowers despite genuine housing demand across lower-income and informal urban populations. Informal income volatility further increases perceived default risk, discouraging lenders from extending unsecured or partially documented housing finance even when borrowers possess adequate repayment ability through non-formal earnings streams. Subsidized housing programs partially mitigate this barrier but remain targeted to specific income thresholds and formal eligibility criteria, leaving large segments of near-eligible households without access to mortgage financing. Limited integration of alternative credit assessment tools such as utility payment history or transaction-based income analysis constrains expansion of mortgage eligibility into informal borrower segments that dominate certain urban regions. Financial inclusion initiatives have expanded basic banking access but have not fully translated into mortgage-grade credit profiles capable of supporting long-term housing loans. As urbanization continues to draw informal workers into metropolitan housing markets, the mismatch between borrower documentation capacity and mortgage underwriting requirements remains a structural limitation on home finance penetration.

Property Titling Complexity and Land Registration Inefficiencies

Indonesia home finance growth is constrained by complex land ownership documentation, fragmented cadastral systems, and protracted property registration processes that create legal uncertainty and collateral risk for mortgage lenders evaluating residential assets for secured lending. In many regions, land parcels lack standardized titles or contain overlapping ownership claims arising from historical customary rights, informal settlements, or incomplete registration, complicating mortgage collateral verification and enforceability under banking regulations. Lengthy bureaucratic procedures for property certification and transfer increase transaction time and cost for borrowers and developers, delaying mortgage approval cycles and discouraging formal housing finance adoption. Banks require legally clear and transferable titles before loan disbursement, excluding properties within partially registered or disputed land areas from mortgage eligibility despite substantial housing demand. Developers face challenges securing fully certified land for large-scale residential projects, limiting supply of mortgage-ready housing units and slowing expansion of financed housing stock across rapidly urbanizing regions. Legal disputes and administrative inconsistencies across local land offices increase collateral enforcement risk, elevating lender caution and tightening mortgage underwriting thresholds in affected areas. Government land reform and digital registry initiatives aim to improve titling clarity, but nationwide implementation remains uneven across provinces with varying administrative capacity. Persistent property documentation challenges therefore continue to restrict mortgage market scalability by constraining both collateral availability and borrower access to formally registrable housing assets.

Opportunities

Digital Mortgage Origination and Alternative Credit Assessment Expansion

Indonesia home finance market presents significant opportunity through digitalization of mortgage origination processes combined with alternative credit analytics capable of evaluating informal and semi-formal borrower income streams beyond traditional salary documentation frameworks used by banks. Digital platforms integrating electronic identity verification, automated property valuation, and online loan application workflows can substantially reduce processing costs and approval timelines, enabling lenders to expand mortgage access across geographically dispersed urban populations. Transactional banking data, mobile payment histories, and utility bill records provide alternative indicators of repayment capacity for borrowers lacking formal payslips, allowing financial institutions to broaden eligibility without compromising credit risk management. Fintech partnerships with banks can deliver scalable mortgage onboarding through mobile interfaces accessible to emerging middle-income households in secondary cities where branch penetration remains limited. Government digital identity infrastructure and electronic land registry modernization further enhance reliability of borrower and collateral verification in remote origination channels. Automated underwriting models supported by large borrower datasets improve risk segmentation and pricing accuracy across diverse income profiles, enabling differentiated mortgage products tailored to varying borrower risk levels. Expansion of digital mortgage ecosystems also facilitates refinancing, loan servicing, and subsidy integration within unified platforms that improve borrower experience and retention. As digital financial adoption increases nationwide, technology-enabled mortgage origination can significantly accelerate home finance penetration into underserved demographic and geographic segments.

Affordable Housing Public-Private Partnerships and Secondary Mortgage Market Development

Indonesia home finance sector holds strong growth opportunity through expanded collaboration between government housing programs, private developers, and financial institutions to scale affordable residential supply supported by structured long-term mortgage funding mechanisms. Public-private housing partnerships can align land provision, infrastructure development, and construction incentives with bank financing channels to create coordinated pipelines of mortgage-eligible housing targeted at low- and middle-income households across expanding urban corridors. Secondary mortgage market institutions purchasing housing loans from banks provide liquidity recycling that enables lenders to originate additional mortgages without balance sheet constraints, supporting sustained expansion of home finance portfolios. Mortgage-backed securities issuance can mobilize long-term capital from institutional investors such as pension funds and insurance companies, improving funding maturity alignment with long-tenor housing loans and reducing reliance on short-term deposits. Risk-sharing frameworks between government and lenders lower default exposure on affordable housing loans, encouraging broader borrower inclusion while preserving financial stability. Large-scale planned housing developments supported by infrastructure investment generate stable collateral pools suitable for securitized mortgage financing, reinforcing scalability of secondary markets. Integration of subsidy schemes within structured mortgage products improves affordability and investor confidence simultaneously, enhancing funding availability for mass housing finance. Strengthening secondary mortgage mechanisms therefore enables systemic expansion of home finance capacity while supporting national housing ownership objectives.

Future Outlook

Indonesia home finance market is expected to expand steadily over the next five years supported by continued urbanization, expansion of subsidized housing finance, and increasing mortgage penetration across middle-income households. Digital lending technologies and land registration reforms are likely to improve access and processing efficiency. Government housing infrastructure programs and secondary mortgage market development will strengthen funding capacity. Rising residential demand in metropolitan corridors will sustain long-term mortgage growth momentum.

Major Players

- Bank Tabungan Negara

- BankMandiri

- Bank Rakyat Indonesia

- Bank Central Asia

- Bank Negara Indonesia

- Bank Syariah Indonesia

- CIMB Niaga

- OCBC NISP

- Maybank Indonesia

- Panin Bank

- Permata Bank

- SMF Indonesia

- Adira Finance

- Mandiri Tunas Finance

- BCA Finance

Key Target Audience

- Commercial banks

- Housing finance institutions

- Real estate developers

- Mortgage technology providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Infrastructure financing agencies

- Institutional investors

Research Methodology

Step 1: Identification of Key Variables

Key variables including mortgage outstanding volume, borrower segments, housing supply pipeline, banking penetration, and subsidy program scale were identified from regulatory statistics and housing finance disclosures to define market structure and measurement framework.

Step 2: Market Analysis and Construction

Mortgage portfolio data, banking financial reports, housing program outputs, and developer supply indicators were integrated to construct market sizing and segmentation across product and platform dimensions aligned with national housing finance ecosystem structure.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through comparison with central bank publications, housing authority reports, and financial institution disclosures to ensure consistency in mortgage penetration trends, subsidy program impact, and borrower segmentation assumptions.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into structured analysis covering drivers, challenges, opportunities, and competitive dynamics to produce coherent market intelligence reflecting Indonesia home finance evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Subsidized Housing Finance Expansion

Urbanization and Household Formation Growth

Banking Sector Mortgage Penetration Initiatives

Middle Income Housing Demand Expansion

Sharia Mortgage Adoption Growth - Market Challenges

High Informal Employment Limiting Credit Eligibility

Property Titling and Land Registration Complexity

Interest Rate Sensitivity of Borrowers

Regional Housing Affordability Gaps

Limited LongTerm Funding for Mortgage Lenders - Market Opportunities

Digital Mortgage Origination Expansion

Affordable Housing PublicPrivate Partnerships

Secondary Mortgage Market Development - Trends

Growth of Subsidized Housing Loan Programs

Integration of Digital Credit Assessment Tools

Expansion of Islamic Home Financing Products

Partnerships Between Banks and Developers

Government Housing Infrastructure Acceleration - Government Regulations & Defense Policy

National Housing Finance Subsidy Schemes

Macroprudential Mortgage Lending Regulations

Land and Property Registration Reforms

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Conventional Mortgage Loans

Sharia-Compliant Home Financing

Subsidized Housing Loans

Construction Financing Facilities

Home Equity and Refinancing Loans - By Platform Type (In Value%)

Commercial Bank Lending Platforms

Islamic Banking Platforms

NonBank Housing Finance Institutions

Digital Mortgage Platforms

Government Housing Finance Programs - By Fitment Type (In Value%)

Primary Home Purchase Financing

Secondary Home Purchase Financing

Self Construction Financing

Renovation and Improvement Financing

Land Purchase Financing - By EndUser Segment (In Value%)

FirstTime Homebuyers

Upgraders and Existing Homeowners

Informal Sector Borrowers

Affordable Housing Beneficiaries

Real Estate Investors - By Procurement Channel (In Value%)

Direct Bank Origination

Developer Linked Financing

Government Subsidy Programs

Mortgage Brokers and Agents

Digital Loan Marketplaces - By Material / Technology (in Value %)

Credit Scoring and Risk Analytics Systems

Digital Loan Origination Systems

Property Valuation Technologies

Identity Verification and eKYC Systems

Automated Underwriting Platforms

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Loan Type Diversity, Funding Cost Efficiency, Distribution Reach, Digital Origination Capability, Sharia Financing Strength)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bank Tabungan Negara

Bank Mandiri

Bank Rakyat Indonesia

Bank Central Asia

Bank Negara Indonesia

Bank Syariah Indonesia

CIMB Niaga

OCBC NISP

Maybank Indonesia

Panin Bank

Permata Bank

SMF Indonesia

Adira Finance

Mandiri Tunas Finance

BCA Finance

- Urban salaried households drive formal mortgage uptake

- Subsidized borrowers dominate affordable housing finance demand

- Informal income households rely on alternative financing pathways

- Property investors utilize mortgages for portfolio expansion

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now