Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Indonesia Last-Mile Delivery Market recorded an estimated market size of approximately USD ~ billion, supported by strong growth in e-commerce transactions, expanding digital payment adoption, and rapid urbanization across major metropolitan regions. Logistics providers continue expanding courier networks, automated sorting hubs, and urban delivery fleets to support increasing parcel volumes. Data reported by Indonesia’s Ministry of Trade and national digital economy studies highlight strong demand from online retail, food delivery services, and third-party logistics companies operating across digital marketplaces.

Jakarta, Surabaya, Bandung, and Medan represent the most active last-mile delivery hubs due to dense population clusters, strong e-commerce penetration, and extensive transportation infrastructure. Jakarta functions as the central logistics hub because of its large consumer base and presence of national fulfillment centers. Surabaya and Bandung support regional distribution networks across Java, while Medan facilitates delivery operations across Sumatra. These cities host major courier sorting facilities, logistics technology platforms, and large retail fulfillment warehouses supporting high-frequency parcel distribution operations.

Market Segmentation

By Delivery Mode

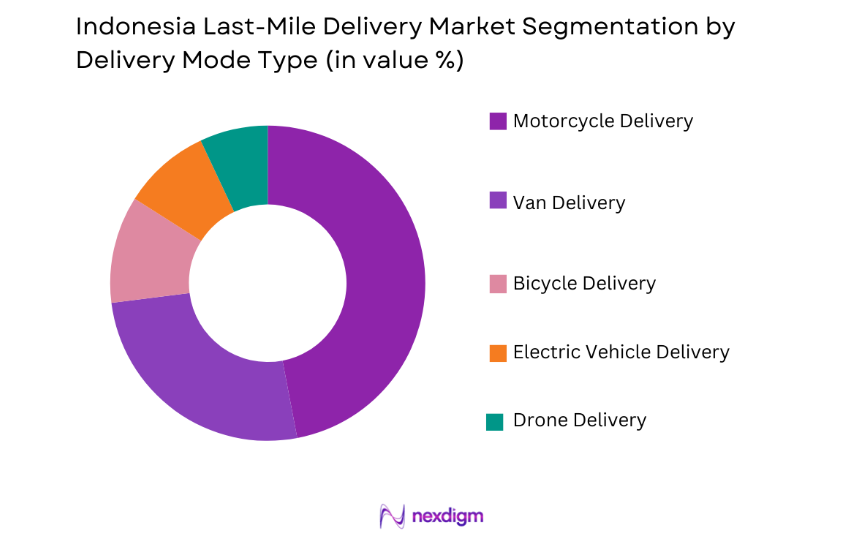

Indonesia Last-Mile Delivery Market is segmented by delivery mode into motorcycle delivery, van delivery, bicycle delivery, electric vehicle delivery, and drone delivery. Recently, motorcycle delivery has a dominant market share due to Indonesia’s dense urban traffic conditions and narrow street networks that require agile delivery vehicles capable of navigating congested city roads. Motorcycle fleets allow logistics providers to maintain faster delivery times across highly populated urban districts. E-commerce platforms and food delivery companies widely deploy motorcycle couriers because they offer lower operational costs and greater route flexibility compared with larger vehicles. The rapid expansion of gig-economy courier networks and digital delivery platforms further strengthens the dominance of motorcycle-based parcel distribution systems across Indonesia’s last-mile logistics ecosystem.

By End-User Industry

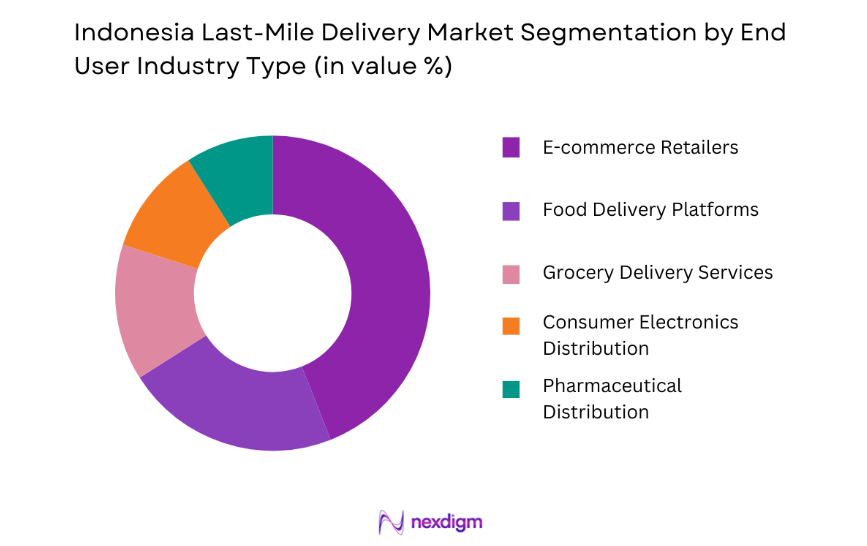

Indonesia Last-Mile Delivery Market is segmented by end-user industry into e-commerce retailers, food delivery platforms, grocery delivery services, pharmaceutical distribution, and consumer electronics distribution. Recently, e-commerce retailers have a dominant market share due to the rapid growth of digital marketplaces and online retail transactions across Indonesia’s expanding digital economy. Online retail platforms generate large parcel volumes that require high-frequency delivery services across urban and suburban residential areas. Major e-commerce companies rely on integrated logistics networks consisting of fulfillment centers, parcel sorting hubs, and courier fleets to ensure timely delivery operations. Increasing smartphone adoption, digital payment usage, and consumer preference for online shopping significantly strengthen the demand for last-mile parcel delivery services within Indonesia’s retail distribution ecosystem.

Competitive Landscape

The Indonesia Last-Mile Delivery Market is characterized by a highly competitive environment where domestic logistics companies, technology-driven delivery platforms, and global courier providers compete for market share. Digital logistics platforms, gig-economy courier networks, and integrated e-commerce logistics systems significantly shape competition. Major players invest heavily in automated parcel sorting centers, route optimization technologies, and real-time tracking platforms to improve delivery efficiency. Strategic partnerships between e-commerce companies and logistics providers further strengthen large players’ dominance across Indonesia’s rapidly expanding parcel delivery ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet Size |

| J&T Express | 2015 | Indonesia | ~ | ~ | ~ | ~ | ~ |

| SiCepat Ekspres | 2014 | Indonesia | ~ | ~ | ~ | ~ | ~ |

| Ninja Van | 2014 | Singapore | ~ | ~ | ~ | ~ | ~ |

| DHL eCommerce | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Pos Indonesia | 1746 | Indonesia | ~ | ~ | ~ | ~ | ~ |

Indonesia Last-Mile Delivery Market Analysis

Growth Drivers

Rapid Expansion of Indonesia’s E-commerce Economy and Digital Marketplaces

Indonesia’s rapidly expanding e-commerce sector significantly drives the growth of last-mile delivery services as millions of online retail transactions require efficient parcel distribution across densely populated urban areas and emerging suburban regions. Digital marketplaces such as Tokopedia, Shopee, and Lazada generate substantial daily parcel volumes that depend heavily on reliable courier networks capable of delivering packages directly to consumers’ homes. Increasing smartphone adoption and widespread digital payment usage enable consumers to purchase products conveniently through mobile applications. Logistics providers respond by expanding automated sorting facilities, courier fleets, and fulfillment warehouses located near major urban centers. Online retail platforms also establish strategic partnerships with logistics companies to improve delivery speed and customer satisfaction. The rising popularity of same-day and next-day delivery services further increases operational demand for high-frequency last-mile logistics networks. E-commerce companies continue investing in proprietary logistics systems to reduce delivery costs and improve supply chain control. These developments collectively strengthen the role of last-mile delivery providers within Indonesia’s rapidly expanding digital commerce ecosystem.

Growth of On-Demand Food and Grocery Delivery Platforms in Urban Centers

The rapid expansion of on-demand food delivery applications and digital grocery platforms significantly increases demand for fast and reliable last-mile logistics services across Indonesia’s urban population centers. Mobile platforms such as GoFood and GrabFood enable consumers to order meals and groceries through smartphone applications, creating constant demand for high-frequency delivery operations. Restaurants, cloud kitchens, and supermarket chains depend on real-time delivery networks capable of transporting orders quickly while maintaining food quality and freshness. Delivery companies deploy large fleets of motorcycle couriers equipped with mobile navigation systems to handle high order volumes during peak periods. Urban lifestyle changes and increasing demand for convenience services further strengthen the adoption of app-based delivery platforms. Digital logistics algorithms help optimize delivery routes and improve operational efficiency for courier fleets. Retailers also integrate food and grocery delivery services into their digital commerce platforms to attract online consumers. As urban populations continue expanding and digital ordering behavior increases, last-mile logistics providers benefit from sustained demand growth.

Market Challenges

Severe Urban Traffic Congestion Affecting Delivery Efficiency

Indonesia’s major metropolitan cities experience severe traffic congestion that significantly affects last-mile delivery efficiency and increases operational costs for logistics providers. Delivery vehicles often encounter long travel times due to crowded urban road networks and limited transportation infrastructure capacity. Traffic congestion delays parcel deliveries and reduces the number of shipments that couriers can complete during a single working shift. Logistics companies must therefore deploy larger delivery fleets and more couriers to maintain service reliability. These operational adjustments increase labor costs and vehicle maintenance expenses. Congested city environments also complicate route planning and delivery scheduling for logistics operators. Companies increasingly rely on digital route optimization systems to minimize travel delays and improve delivery efficiency. Despite these technological improvements, heavy traffic conditions remain one of the most persistent operational challenges affecting Indonesia’s last-mile logistics networks.

Fragmented Logistics Infrastructure Across Indonesia’s Archipelagic Geography

Indonesia’s geographical structure as an archipelago consisting of thousands of islands creates logistical complexity for parcel delivery networks attempting to serve both urban and remote regions. Transportation between islands often requires integration of air cargo, maritime shipping, and ground courier networks before parcels reach final customers. Remote areas frequently lack advanced parcel sorting facilities and transportation infrastructure necessary for efficient logistics operations. Delivery providers must develop decentralized distribution networks that combine regional warehouses with local courier fleets to ensure nationwide service coverage. These infrastructure limitations increase delivery times and operational costs compared with mainland logistics markets. Logistics companies therefore invest heavily in regional distribution hubs and inter-island transportation partnerships to improve delivery efficiency. Building an integrated nationwide last-mile delivery network across Indonesia’s diverse geographic environment remains a significant operational challenge for logistics providers.

Opportunities

Adoption of Electric Vehicles and Sustainable Urban Delivery Fleets

Logistics companies increasingly explore the adoption of electric motorcycles and electric delivery vans as part of sustainability strategies aimed at reducing fuel costs and urban emissions associated with last-mile logistics operations. Electric delivery fleets provide lower operating expenses because electricity costs are often lower than traditional fuel prices. Government programs promoting clean transportation and urban sustainability initiatives encourage logistics providers to adopt environmentally friendly delivery vehicles. Electric motorcycles are particularly well suited for dense urban delivery operations due to their smaller size and lower maintenance requirements. Several Indonesian logistics companies have begun pilot programs deploying electric delivery fleets within major metropolitan areas. As battery technology improves and charging infrastructure expands, electric vehicles are expected to become a larger component of urban delivery operations. The transition toward sustainable logistics solutions therefore presents long-term growth opportunities for last-mile delivery providers.

Development of Smart Logistics Platforms and Delivery Automation Technologies

Technological innovation within logistics management systems creates opportunities for improving delivery efficiency and operational scalability across Indonesia’s last-mile delivery ecosystem. Artificial intelligence powered route optimization software enables logistics companies to analyze traffic conditions and dynamically adjust delivery routes to minimize delays. Automated parcel sorting facilities significantly increase processing capacity within urban fulfillment centers. Real-time tracking systems also allow consumers and retailers to monitor parcel movement across delivery networks, improving transparency and customer satisfaction. Technology driven logistics platforms integrate warehouse management systems, courier fleet coordination, and customer order tracking into unified digital ecosystems. As Indonesia’s digital economy continues expanding, logistics providers increasingly invest in advanced delivery technologies to strengthen operational efficiency and service quality.

Future Outlook

The Indonesia Last-Mile Delivery Market is expected to expand steadily as e-commerce transactions, food delivery services, and digital retail ecosystems continue growing across the country. Technology adoption including route optimization software, parcel automation, and digital logistics platforms will significantly improve delivery efficiency. Urban logistics infrastructure and distribution networks will continue expanding across major metropolitan regions. Increasing consumer demand for faster delivery services will further accelerate the development of advanced last-mile logistics solutions.

Major Players

- J&T Express

- SiCepat Ekspres

- Ninja Van

- Pos Indonesia

- DHL eCommerce

- FedEx Express

- UPS Logistics

- GrabExpress

- GoSend

- Lazada Logistics

- Shopee Xpress

- Lion Parcel

- SAP Express

- RPX Logistics

- Kerry Express

Key Target Audience

- Logistics and courier companies

- E-commerce retailers

- Food delivery platform operators

- Retail distribution companies

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying the major variables influencing the Indonesia Last-Mile Delivery Market including parcel volumes, e-commerce activity, courier fleet capacity, logistics infrastructure, and urban consumer demand. These variables help establish the structural drivers influencing delivery network expansion across Indonesia.

Step 2: Market Analysis and Construction

Market structure is analyzed using government publications, logistics industry reports, company financial disclosures, and trade association data. Information regarding courier fleets, delivery infrastructure, and e-commerce logistics operations is integrated to construct a comprehensive market framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry professionals including logistics managers, e-commerce operators, and supply chain specialists are consulted to validate assumptions regarding parcel delivery demand, technology adoption, and logistics infrastructure development across Indonesia’s delivery ecosystem.

Step 4: Research Synthesis and Final Output

Collected quantitative data and expert insights are synthesized to develop a detailed market report outlining segmentation structure, competitive environment, growth drivers, operational challenges, and strategic opportunities shaping Indonesia’s last-mile delivery industry.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E Commerce Marketplaces and Digital Retail Platforms

Increasing Urban Consumer Demand for Fast and Reliable Delivery Services

Growth of Mobile Commerce and Digital Payment Ecosystems - Market Challenges

Urban Traffic Congestion and Infrastructure Limitations

High Operational Costs in Urban Delivery Networks

Workforce Management and Driver Availability Constraints - Market Opportunities

Expansion of Same Day and Instant Delivery Service Models

Adoption of Smart Logistics Technologies and Route Optimization Platforms

Growth of Cross Border E Commerce Parcel Deliveries - Trends

Adoption of Electric Motorbikes for Urban Delivery Fleets

Integration of AI Based Delivery Tracking and Route Optimization Systems - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Standard Parcel Delivery Services

Same Day Delivery Services

Express Delivery Services

Scheduled Delivery Services

On Demand Delivery Services - By Platform Type (In Value%)

E Commerce Delivery Platforms

Retail Distribution Delivery Platforms

Food Delivery Platforms

Courier and Express Logistics Platforms - By Fitment Type (In Value%)

In House Logistics Operations

Third Party Logistics Providers

Crowdsourced Delivery Networks

Hybrid Logistics Delivery Models - By End User Segment (In Value%)

E Commerce Retailers

Food and Grocery Delivery Platforms

Pharmaceutical and Healthcare Product Distributors

- Market Share Analysis

- Cross Comparison Parameters (Delivery Network Coverage, Fleet Size and Vehicle Mix, Delivery Speed Capability, Technology Platform Integration, Distribution Hub Infrastructure, Last Mile Cost Efficiency, Strategic E Commerce Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

JNE Express

SiCepat Ekspres

J&T Express Indonesia

Ninja Xpress Indonesia

Pos Indonesia

Anteraja

RPX Logistics

Wahana Prestasi Logistik

GrabExpress Indonesia

GoSend by Gojek

Lalamove Indonesia

DHL eCommerce Indonesia

FedEx Indonesia

UPS Indonesia

TIKI Logistics

- E Commerce Platforms Increasing Dependence on Rapid Parcel Distribution Networks

- Retail Chains Expanding Omni Channel Logistics and Home Delivery Services

- Food Delivery Platforms Driving High Frequency Urban Delivery Volumes

- Healthcare Product Distribution Requiring Reliable Same Day Logistics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now