Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Indonesia online insurance market generated approximately USD ~ billion in digital gross written premiums based on recent disclosures from Indonesia Financial Services Authority and insurer annual statements covering online distribution channels across life, health, and motor categories. Market expansion is driven by rapid mobile financial adoption, widespread ecommerce usage, and integration of insurance offerings into digital ecosystems operated by banks, superapps, and marketplaces that collectively reduce distribution costs while expanding first-time policyholder access across urban and semi-urban populations.

Jakarta metropolitan region dominates Indonesia online insurance activity due to concentration of insurers, digital platforms, fintech firms, and high-income salaried professionals with established digital payment behavior and insurance awareness supported by financial literacy initiatives. Secondary growth hubs include Surabaya and Bandung where expanding middle-class populations, ecommerce penetration, and mobile connectivity enable online policy adoption across health and motor segments, while regional digital banking expansion and agent-assisted online onboarding extend coverage access across emerging urban centers.

Market Segmentation

By Product Type

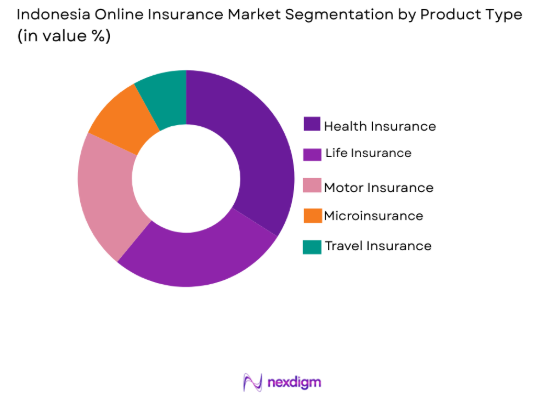

Indonesia online insurance market is segmented by product type into life insurance, health insurance, motor insurance, travel insurance, and microinsurance. Recently, health insurance has a dominant market share due to factors such as rising healthcare costs, employer-sponsored digital policy distribution, and consumer preference for cashless treatment networks integrated with mobile claims servicing platforms across urban hospitals and clinics. Digital health coverage demand is reinforced by telemedicine integration, preventive care packages, and standardized underwriting models suitable for online purchase journeys, supporting scale across individual and group policies.

By Platform Type

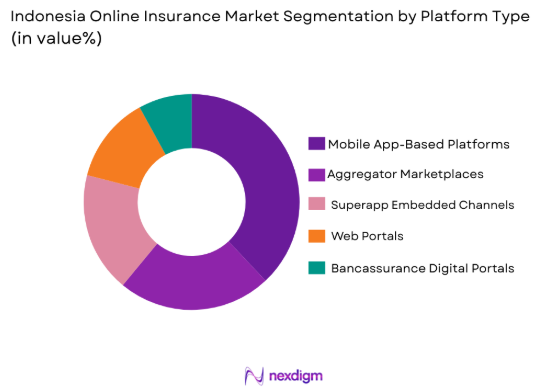

Indonesia online insurance market is segmented by platform type into mobile app-based platforms, web portals, aggregator marketplaces, superapp embedded channels, and bancassurance digital portals. Recently, mobile app-based platforms have a dominant market share due to factors such as high smartphone usage, app-centric financial behavior, and insurer investment in full-cycle mobile underwriting and claims capabilities integrated with digital identity verification and e-wallet payments. Superapp ecosystems and ecommerce integrations further channel policy purchases into mobile environments, reinforcing platform leadership across retail and microinsurance segments.

Competitive Landscape

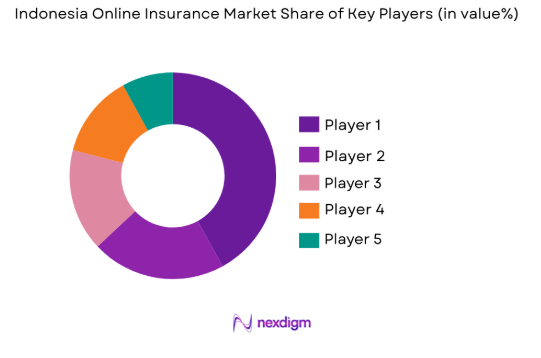

Indonesia online insurance market exhibits moderate concentration with multinational insurers and domestic financial groups controlling digital distribution through proprietary apps, bancassurance integrations, and partnerships with ecommerce and superapp ecosystems. Major players leverage brand trust, hospital networks, and capital strength to scale online underwriting and claims automation, while local insurers compete through pricing and microinsurance innovation targeting underserved segments. Platform partnerships with digital banks and mobility providers increasingly shape competitive positioning and customer acquisition strategies across urban markets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Digital Distribution Partnerships |

| Allianz Indonesia | 1981 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| Prudential Indonesia | 1995 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| AIA Financial Indonesia | 1992 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| AXA Mandiri | 2004 | Jakarta | ~ | ~ | ~ | ~ | ~ |

| BRI Life | 1987 | Jakarta | ~ | ~ | ~ | ~ | ~ |

Indonesia Online Insurance Market Analysis

Growth Drivers

Mobile-First Financial Behavior and Superapp Ecosystem Integration

Mobile-First Financial Behavior and Superapp Ecosystem Integration drives Indonesia online insurance market expansion by embedding insurance purchase, servicing, and claims functions directly within widely used mobile financial and ecommerce platforms that millions of consumers access daily for payments, transport, shopping, and banking transactions. Indonesia hosts one of the largest mobile internet user bases globally, and smartphone-centric digital engagement shapes consumer interaction with financial services including insurance discovery, quotation, and policy issuance conducted entirely through handheld interfaces without reliance on agents or physical documentation processes. Superapp ecosystems operated by technology conglomerates integrate insurance modules alongside payments, lending, and investment features, allowing users to purchase standardized coverage during routine digital activities such as ride booking or ecommerce checkout, significantly lowering customer acquisition costs for insurers. Digital wallets and instant payment rails further enable seamless premium collection and renewal automation, removing friction associated with traditional billing and improving policy persistence across low-income and gig-economy segments that historically exhibited irregular payment behavior. Insurers leverage mobile behavioral data and transaction histories from platform partners to refine underwriting, personalize product offerings, and price risk dynamically across large populations lacking formal insurance records, enabling scalable digital microinsurance distribution models. Integrated mobile claims submission using photo documentation, geolocation tagging, and automated adjudication accelerates settlement cycles and strengthens consumer trust in digital insurance services compared with historically manual claims processes. Government-backed digital identity infrastructure and electronic signature regulation frameworks support remote onboarding and authentication within mobile journeys, legitimizing online insurance contracting and reducing compliance friction for insurers operating across multiple provinces. Continuous platform engagement through push notifications, loyalty programs, and embedded financial education encourages cross-selling and policy upgrades, expanding average revenue per user within digital ecosystems. As mobile financial ecosystems deepen across urban and semi-urban Indonesia, online insurance adoption continues to expand structurally across demographic segments previously excluded from formal risk protection markets.

Rising Healthcare Costs and Demand for Cashless Digital Health Coverage

Rising Healthcare Costs and Demand for Cashless Digital Health Coverage accelerates Indonesia online insurance market growth as households seek financial protection against escalating medical expenses and prefer digital health policies offering immediate hospital access and simplified claims reimbursement processes integrated with mobile healthcare ecosystems. Urbanization and private healthcare expansion have increased out-of-pocket treatment costs across inpatient and outpatient services, encouraging middle-income families and employers to adopt health insurance coverage accessible through online enrollment platforms that provide rapid policy issuance without medical examination delays for standardized plans. Insurers digitize provider networks by linking hospitals, clinics, pharmacies, and telemedicine services into cashless treatment systems where policyholders authenticate coverage through mobile apps, eliminating reimbursement paperwork and enhancing perceived value of digital health insurance relative to traditional indemnity products. Employer-sponsored group health policies increasingly transition toward online administration portals that allow enrollment, endorsement, and claims tracking for large workforces across distributed locations, expanding digital insurance penetration among salaried populations. Telemedicine platforms integrated with insurers extend preventive consultations, diagnostics scheduling, and prescription delivery within digital health ecosystems, reinforcing recurring engagement and encouraging policy renewals through continuous service utilization rather than episodic claims interactions. Data analytics applied to healthcare utilization patterns enable insurers to design modular digital health plans tailored to demographic risk profiles and affordability thresholds, supporting scalable online distribution to both corporate and individual segments. Government health coverage gaps in private care access motivate households to supplement public schemes with private digital policies purchased via aggregators or insurer apps, particularly among urban professionals seeking faster treatment pathways. Claims automation using electronic medical records and digital billing interfaces shortens settlement cycles and reduces fraud risk, strengthening trust and encouraging online policy uptake across new customer cohorts. As healthcare demand rises alongside income growth and private hospital infrastructure expansion, digital health insurance remains the leading driver of online insurance adoption across Indonesia.

Market Challenges

Low Insurance Literacy and Trust Deficit in Digital Financial Products

Low Insurance Literacy and Trust Deficit in Digital Financial Products constrains Indonesia online insurance market expansion because large segments of the population lack familiarity with insurance concepts, policy terms, and digital contracting processes, leading to hesitation in purchasing intangible protection products without in-person advisory support. Insurance penetration historically remains low relative to regional peers, and many households perceive insurance as complex, unnecessary, or unreliable due to past experiences with claim disputes or unclear coverage conditions communicated through agents rather than transparent digital interfaces. Transition to online channels removes interpersonal trust cues traditionally provided by agents, requiring consumers to rely solely on platform information and brand reputation when committing to premium payments for contingent future benefits, which heightens perceived risk and slows digital conversion rates. Misinformation and limited financial literacy further complicate understanding of policy exclusions, deductibles, and benefit structures presented within mobile applications, increasing the likelihood of dissatisfaction or lapse when expectations diverge from actual coverage. Rural and lower-income populations often exhibit limited exposure to formal insurance and digital financial services, constraining adoption of online microinsurance products despite affordability and accessibility advantages offered by mobile distribution. Fraud concerns and cybersecurity awareness gaps reinforce skepticism toward online financial transactions involving personal data submission and recurring premium deductions, particularly among first-time digital users transitioning from cash-based financial behavior. Insurers invest heavily in education campaigns, simplified product design, and transparent claims communication to build trust, but behavioral change across large populations requires sustained time and outreach investment. Regulatory consumer protection enforcement remains essential to reinforce confidence, yet awareness of dispute resolution mechanisms and insurer accountability is still evolving among consumers. Without accelerated financial literacy improvement and trust building, digital insurance adoption may remain concentrated among urban educated segments rather than achieving broad national penetration.

Regulatory Fragmentation and Compliance Burden Across Digital Distribution Channels

Regulatory Fragmentation and Compliance Burden Across Digital Distribution Channels challenges Indonesia online insurance market scalability because insurers must navigate complex licensing, data protection, consumer protection, and distribution partnership regulations that vary across product categories and digital platforms. Insurance digitalization involves collaboration with banks, ecommerce firms, telecom operators, and superapp providers, each subject to separate sectoral regulations governing data sharing, customer onboarding, and financial service bundling, creating compliance complexity for integrated online insurance offerings. Electronic know-your-customer requirements, data localization rules, and cybersecurity standards impose significant technology investment obligations on insurers developing online platforms capable of securely managing sensitive personal and health information across distributed digital ecosystems. Approval processes for new digital insurance products and distribution models can be lengthy due to prudential review of pricing, underwriting algorithms, and consumer disclosure frameworks, delaying innovation and time-to-market relative to rapidly evolving fintech environments. Cross-border data processing restrictions complicate deployment of global insurer technology infrastructure and cloud-based analytics solutions, requiring localization or regulatory negotiation that increases operational costs. Compliance oversight extends to marketing practices, premium collection methods, and digital claims handling transparency, necessitating continuous monitoring and reporting systems integrated into online platforms. Smaller domestic insurers face resource constraints in meeting regulatory technology requirements compared with multinational competitors possessing advanced compliance capabilities, potentially reinforcing market concentration. Distribution partnerships with non-insurance platforms must also comply with intermediary licensing and disclosure standards, limiting flexibility in embedded insurance experimentation across ecommerce or mobility channels. Harmonization of digital financial service regulations remains ongoing, and until frameworks fully align across sectors, regulatory burden will continue to moderate pace of online insurance innovation and expansion in Indonesia.

Opportunities

Expansion of Embedded Insurance Across Ecommerce and Mobility Platforms

Expansion of Embedded Insurance Across Ecommerce and Mobility Platforms presents a major opportunity for Indonesia online insurance market growth by integrating contextual insurance products directly into high-frequency digital transactions across retail, transport, logistics, and travel ecosystems used daily by millions of consumers. Ecommerce marketplaces and ride-hailing applications generate vast volumes of product purchases, deliveries, and passenger journeys that create natural demand for micro-duration insurance coverage such as parcel protection, device insurance, trip accident coverage, and logistics liability policies offered seamlessly during checkout or booking flows. Embedded insurance eliminates search and onboarding friction by pre-filling customer data and aligning coverage with immediate transaction risk, enabling insurers to reach large populations without standalone marketing expenditure or complex underwriting processes. Platform operators benefit from ancillary revenue streams and enhanced customer trust through integrated protection services, incentivizing partnerships with insurers to co-design standardized digital products compatible with platform workflows and pricing structures. Behavioral data from platform transactions enables insurers to price risk dynamically and manage claims through automated verification linked to transaction records, improving profitability and scalability of low-premium insurance segments. Small merchants and gig workers participating in ecommerce or mobility ecosystems also require liability and asset protection coverage accessible digitally through platform dashboards, expanding commercial online insurance segments beyond retail consumers. Indonesia’s rapidly expanding digital commerce economy provides a structurally growing distribution channel for embedded insurance adoption across both urban and semi-urban populations. Regulatory acceptance of embedded distribution models further legitimizes integration of insurance into non-financial digital platforms. As platform ecosystems deepen and diversify services, embedded insurance is positioned to become a primary growth engine for online insurance penetration across Indonesia.

Digital Microinsurance for Underserved Rural and Informal Economy Populations

Digital Microinsurance for Underserved Rural and Informal Economy Populations offers significant expansion potential for Indonesia online insurance market by leveraging mobile connectivity and simplified digital products to extend risk protection to low-income households and workers historically excluded from formal insurance systems. Large segments of Indonesia’s population operate within agriculture, fisheries, and informal urban employment sectors characterized by income volatility and exposure to health, weather, and asset risks without access to conventional insurance distribution channels concentrated in cities. Mobile-based microinsurance products with low premiums, flexible payment schedules, and simplified claims processes can be distributed through telecom operators, rural banks, cooperatives, and government assistance programs integrated into digital platforms accessible via basic smartphones. Parametric insurance models linked to weather or yield data enable automated payouts without complex loss assessment, improving trust and feasibility in rural environments lacking insurance infrastructure. Government financial inclusion initiatives and digital identity systems support remote enrollment and subsidy targeting for vulnerable populations, reducing onboarding barriers and enhancing adoption of microinsurance delivered digitally. Partnerships with agricultural input suppliers and microfinance institutions allow bundling of crop or livestock coverage with loans or supplies, embedding insurance within existing rural economic transactions. Claims automation through mobile reporting and geospatial verification reduces administrative costs, enabling sustainable pricing of small-ticket policies across dispersed populations. Social protection gaps and climate risk exposure increase demand for affordable microinsurance coverage among rural communities seeking financial resilience. As connectivity expands and digital literacy improves, microinsurance distributed through online channels can substantially broaden Indonesia’s insurance penetration beyond urban markets.

Future Outlook

Indonesia online insurance market is expected to expand steadily as mobile financial ecosystems deepen, embedded insurance partnerships proliferate across ecommerce and mobility platforms, and digital health coverage demand rises with healthcare infrastructure growth. Regulatory frameworks supporting electronic onboarding and digital distribution are likely to mature, enabling scalable innovation in microinsurance and usage-based products. Advancements in AI underwriting, claims automation, and data-driven pricing will enhance operational efficiency and personalization. Expanding rural connectivity and financial inclusion initiatives will broaden digital insurance adoption across new demographic segments.

Major Players

- Allianz Indonesia

- Prudential Indonesia

- AIA Financial Indonesia

- AXA Mandiri Financial Services

- Manulife Indonesia

- Tokio Marine Life Insurance Indonesia

- Chubb Life Indonesia

- FWD Insurance Indonesia

- Zurich Asuransi Indonesia

- Asuransi Astra

- Asuransi Sinar Mas

- BRI Life Indonesia

- Sun Life Financial Indonesia

- Great Eastern Life Indonesia

- Bhinneka Life Indonesia

Key Target Audience

- Insurance companies

- Digital banks

- Ecommerce platforms

- Investment and venture capital firms

- Government and regulatory bodies

- Healthcare provider networks

- Telecom operators

- Superapp platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables include digital insurance premiums, platform adoption rates, product penetration across life, health, and motor segments, regulatory frameworks, and distribution partnerships shaping online insurance growth across Indonesia’s digital financial ecosystem.

Step 2: Market Analysis and Construction

Market size and segmentation are constructed through aggregation of insurer digital premium disclosures, regulator statistics, platform transaction data, and distribution channel analysis across mobile, aggregator, and embedded insurance environments.

Step 3: Hypothesis Validation and Expert Consultation

Findings are validated through consultation with insurers, digital platform operators, regulators, and healthcare network administrators to confirm distribution dynamics, adoption drivers, and competitive positioning across Indonesia online insurance market.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights are synthesized into structured market estimates, segmentation shares, competitive analysis, and forward outlook reflecting Indonesia’s digital insurance evolution and platform-driven distribution landscape.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid Smartphone Penetration and Mobile Internet Adoption

Expansion of Digital Payments and Ewallet Ecosystems

Insurance Inclusion Policies Promoting Microinsurance Digitization - Market Challenges

Low Insurance Awareness and Trust Barriers

Regulatory Compliance Complexity for Digital Distribution

Limited Actuarial Data for Emerging Risk Segments - Market Opportunities

Expansion of Embedded Insurance Across Ecommerce and Mobility Platforms

Growth of Microinsurance in Underserved Rural Populations

Partnerships Between Insurers and Superapp Ecosystems - Trends

Shift Toward Instant Policy Issuance and Claims Automation

Rise of Usage-Based and On-Demand Insurance Products

Integration of Insurance Within Digital Financial Superapps

Adoption of AI Chatbots for Customer Servicing

Expansion of Digital Microinsurance Offerings - Government Regulations & Defense Policy

OJK Digital Insurance Licensing and Supervision Frameworks

National Financial Inclusion Strategy Supporting Microinsurance

Electronic Know Your Customer and Digital Signature Regulations

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Life Insurance Digital Platforms

Health Insurance Digital Platforms

Motor Insurance Digital Platforms

Travel Insurance Digital Platforms

Microinsurance Digital Platforms - By Platform Type (In Value%)

Mobile App-Based Insurance Platforms

Web Portal Insurance Platforms

Aggregator Comparison Platforms

Embedded Insurance APIs

Superapp Integrated Insurance Modules - By Fitment Type (In Value%)

Standalone Digital Insurer Platforms

Insurer-Aggregator Integrated Systems

Bank-Insurer Digital Integration

Ecommerce Embedded Insurance Integration

Telecom-Linked Insurance Platforms - By EndUser Segment (In Value%)

Individual Retail Policyholders

SME Commercial Policyholders

Gig Economy Workers

Rural Microinsurance Customers

Corporate Employee Benefit Buyers - By Procurement Channel (In Value%)

Direct Insurer Online Sales

Aggregator Marketplace Purchases

Superapp Embedded Purchases

Bancassurance Digital Channels

Ecommerce Checkout Insurance - By Material / Technology (in Value %)

AI-Based Underwriting Engines

Cloud-Native Insurance Platforms

API Integration Frameworks

Digital Identity Verification Systems

Data Analytics Risk Scoring Models

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Product Portfolio Breadth, Digital Platform Capability, Distribution Partnerships, Customer Acquisition Model, Pricing Competitiveness)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Allianz Indonesia

Prudential Indonesia

AIA Financial Indonesia

AXA Mandiri Financial Services

Manulife Indonesia

Tokio Marine Life Insurance Indonesia

Chubb Life Indonesia

FWD Insurance Indonesia

Zurich Asuransi Indonesia

Asuransi Astra

Asuransi Sinar Mas

Bhinneka Life Indonesia

BRI Life Indonesia

Sun Life Financial Indonesia

Great Eastern Life Indonesia

- Urban Millennials Driving Mobile-First Policy Purchases

- Gig Workers Seeking Flexible Low-Premium Coverage

- SMEs Adopting Digital Commercial Insurance Products

- Rural Households Accessing Microinsurance via Mobile Channels

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now