Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Indonesia Used Agricultural Equipment market current size stands at around USD ~ million, reflecting steady transactional activity across refurbished tractors, harvesters, and power tillers circulated through dealer networks and informal resale channels. Demand is supported by replacement cycles for aging machinery, constrained access to new equipment financing, and active cross-border inflows of refurbished units. The market operates through a fragmented ecosystem of independent dealers, service workshops, auctions, and peer-to-peer exchanges, with quality variability influencing purchasing confidence and lifecycle value.

Java remains the dominant demand center due to dense farm clusters, superior logistics, and proximity to dealer and service ecosystems. Secondary hubs across Sumatra and Sulawesi benefit from plantation agriculture and contract service providers, while Kalimantan and eastern regions exhibit emerging demand tied to infrastructure access and mechanization programs. Ecosystem maturity varies by province, shaped by availability of refurbishment capabilities, parts distribution, and local policy support for mechanization adoption and aftersales service development.

Market Segmentation

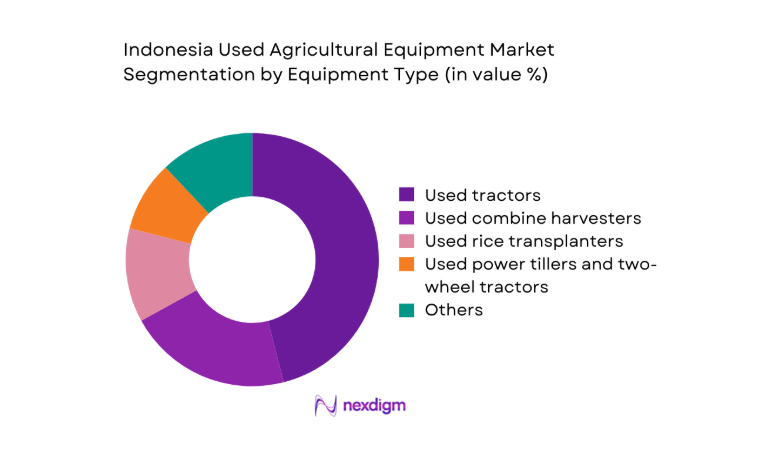

By Equipment Type

Used tractors dominate transactional activity due to broad applicability across rice, corn, and mixed farming systems, supported by abundant availability from fleet turnover and imports of refurbished compact models. Harvesters and transplanters follow, driven by labor substitution needs in rice-growing regions, while post-harvest equipment demand reflects smallholder efforts to reduce losses and improve throughout. Irrigation pumps and sprayers exhibit resilient turnover because of shorter service lives and frequent replacement cycles. Dealer stocking strategies prioritize fast-moving compact units with standardized parts, while specialized equipment circulates through targeted regional channels.

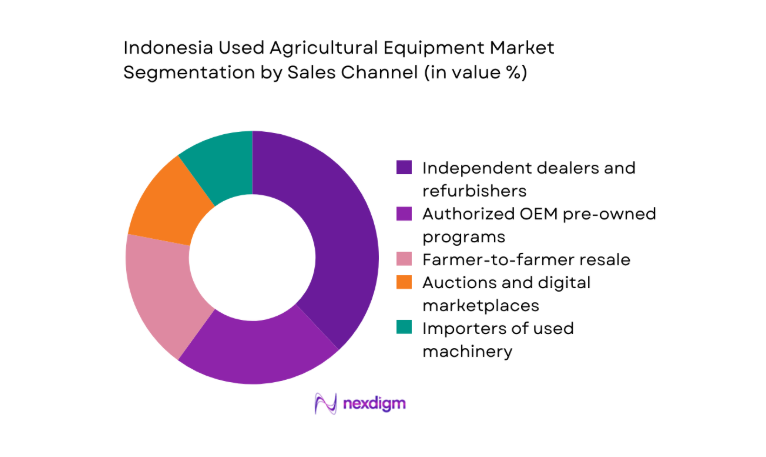

By Sales Channel

Independent dealers and refurbishers lead transactions due to price flexibility, localized service access, and acceptance of mixed-condition inventory. Authorized pre- owned programs attract risk-averse buyers seeking warranties and standardized refurbishment, particularly among cooperatives and commercial farms. Farmer-to-farmer resale remains active in remote areas where formal channels are thin, while auctions and digital marketplaces improve discovery and price transparency. Importers of used machinery serve regional dealers with bulk supply, influencing channel dynamics through inventory availability, lead times, and compliance readiness.

Competitive Landscape

The competitive landscape is characterized by a mix of authorized pre-owned programs, independent refurbishes, regional distributors, and importers supplying reconditioned machinery. Differentiation centers on refurbishment depth, service coverage, parts availability, financing partnerships, and channel reach across key agricultural provinces.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Kubota Corporation | 1890 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Yanmar Co., Ltd. | 1912 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | Duluth, United States | ~ | ~ | ~ | ~ | ~ | ~ |

| John Deere | 1837 | Moline, United States | ~ | ~ | ~ | ~ | ~ | ~ |

Indonesia Used Agricultural Equipment Market Analysis

Growth Drivers

Rising mechanization needs among smallholders

Smallholders cultivate fragmented plots averaging 2 hectares, with labor shortages accelerating adoption of compact machinery for land preparation and harvesting. Government extension services recorded 124 district mechanization clinics operational in 2024, facilitating equipment access and operator training. Rural wage rates increased by 18 between 2022 and 2024, raising demand for labor-substituting equipment. Import clearances for reconditioned compact tractors reached 6420 units in 2024, improving availability. Road density expanded by 312 kilometers across key agricultural corridors in 2025, reducing transport friction for equipment distribution and service access in peri-urban farming clusters.

High new equipment prices driving secondary market demand

Access to new machinery is constrained by household credit limits and collateral requirements, pushing buyers toward refurbished alternatives. Agricultural credit approvals totaled 194000 accounts in 2024, while rejection rates remained elevated across smallholder segments. Public procurement programs prioritized shared machinery pools, recording 2860 units deployed through district cooperatives in 2023 and 2024. Import lead times for refurbished units averaged 47 days in 2025, enabling faster acquisition than new equipment allocations. Dealer inventory turnover improved to 5 cycles annually in high-demand provinces, reflecting substitution behavior toward used equipment pathways.

Challenges

Limited access to financing for used equipment purchases

Formal lenders favor new assets with standardized documentation, limiting credit for refurbished machinery lacking verifiable condition histories. In 2024, only 31 cooperative-linked financing schemes included used equipment as eligible collateral. Microfinance penetration in rural districts reached 284 institutions in 2025, yet underwriting criteria excluded older serials. Loan tenors averaged 24 months, misaligned with equipment life cycles extending beyond 60 months. Default management protocols tightened following 2023 portfolio stress tests conducted by regulators. Limited insurance coverage options further restrict bankability, dampening purchase conversion among smallholders and contractors.

Inconsistent quality and lack of refurbishment standards

Refurbishment practices vary widely across workshops, creating information asymmetry and performance uncertainty. Provincial industry offices accredited 79 repair centers in 2024, covering only major corridors. Parts traceability remains fragmented, with 412 distinct aftermarket suppliers operating in 2025. Inspection protocols differ by dealer, and standardized grading is absent across regions. Failure rates for hydraulic systems reported by service centers rose by 14 between 2022 and 2024. Regulatory audits increased in 2025, yet enforcement capacity remains constrained by limited inspectors and uneven compliance documentation across provincial jurisdictions.

Opportunities

Expansion of OEM-certified pre-owned programs

Certified programs can address quality risk through standardized inspection, warranties, and parts support. In 2024, authorized service outlets expanded to 268 locations nationwide, enabling scalable certification workflows. Training enrollments for certified technicians reached 1840 in 2025, improving refurbishment consistency. Digital service records adoption across dealer networks increased to 61 sites in 2024, supporting lifecycle tracking. Customs clearance processing for certified imports shortened by 9 days following documentation harmonization in 2025. These institutional improvements create pathways to formal financing acceptance and cooperative procurement inclusion for certified used equipment.

Growth of digital marketplaces for farm machinery resale

Online platforms improve discovery, price transparency, and regional liquidity for used equipment. Platform registrations by agricultural sellers reached 214000 accounts in 2024, with verified listings growing across Java and Sumatra. Mobile broadband coverage expanded to 96 subdistricts in 2025, improving rural access to listings and escrow services. Logistics partnerships onboarded 37 regional carriers in 2024, reducing delivery times for inter-island shipments. E-contract adoption increased to 128 cooperatives in 2025, streamlining transactions and documentation for financing eligibility, strengthening trust and transaction velocity in secondary markets.

Future Outlook

The Indonesia Used Agricultural Equipment market is expected to mature through standardized refurbishment, broader financing acceptance, and deeper digital intermediation across provinces. Policy emphasis on mechanization, coupled with improvements in logistics and service networks, will support wider adoption. Certified pre-owned channels and platform-led discovery will shape buyer confidence. Regional expansion beyond Java will accelerate as infrastructure improves. Cross-border sourcing and localized remanufacturing will influence supply reliability through 2035.

Major Players

- Kubota Corporation

- Yanmar Co., Ltd.

- Mitsubishi Agricultural Machinery

- Iseki & Co., Ltd.

- Mahindra & Mahindra

- CNH Industrial

- AGCO Corporation

- John Deere

- PT Kubota Indonesia

- PT Yanmar Indonesia

- PT Indotraktor Utama

- PT Traktor Nusantara

- PT United Tractors Tbk

- RDO Equipment Indonesia

- Tata Hitachi Construction Machinery Indonesia

Key Target Audience

- Smallholder farmers and farmer cooperatives

- Commercial plantation operators

- Agricultural contractors and custom hiring centers

- Equipment dealers and refurbishers

- Authorized service workshops and parts distributors

- Importers and logistics providers

- Investments and venture capital firms

- Ministry of Agriculture, Directorate General of Agricultural Infrastructure and Facilities

Research Methodology

Step 1: Identification of Key Variables

Core variables included equipment categories, refurbishment depth, service coverage, channel mix, regional access, financing eligibility, and regulatory compliance markers across provinces. Field scoping defined data boundaries and operational definitions for used machinery conditions and transaction pathways. Variables were aligned to mechanization programs and aftermarket service structures.

Step 2: Market Analysis and Construction

Analytical frameworks mapped channel flows, refurbishment capacity distribution, parts availability, and logistics connectivity across major agricultural corridors. Institutional indicators from extension services and customs processing informed supply reliability. Regional adoption dynamics were constructed using mechanization clinic coverage and service network density to assess access frictions.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on substitution from new to used equipment were validated through consultations with provincial extension officers, service managers, and cooperative procurement leads. Feedback refined assumptions on financing eligibility, certification acceptance, and refurbishment bottlenecks. Scenario testing assessed impacts of digital intermediation and certified programs on buyer confidence.

Step 4: Research Synthesis and Final Output

Findings were synthesized into coherent market narratives, segment dynamics, and competitive positioning. Cross-validation ensured consistency across regional access, channel structures, and regulatory readiness. Outputs were structured to support strategic planning, investment prioritization, and go-to-market decisions for used equipment stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and classification of used farm machinery, Dealer and refurbisher primary interviews, Farmer and cooperative procurement surveys, Import-export and customs data triangulation, Auction platform and resale price tracking, OEM authorized pre-owned channel analysis, Regional distributor and service network mapping)

- Definition and Scope

- Market evolution

- Usage and replacement pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising mechanization needs among smallholders

High new equipment prices driving secondary market demand

Expansion of rice and plantation acreage

Growth of custom hiring and contract farming services

Availability of imported refurbished machinery

Government mechanization support programs and subsidies - Challenges

Limited access to financing for used equipment purchases

Inconsistent quality and lack of refurbishment standards

Scarcity of spare parts for older models

Low transparency in pricing and equipment condition

Fragmented dealer network outside Java

Regulatory uncertainty on used equipment imports - Opportunities

Expansion of OEM-certified pre-owned programs

Growth of digital marketplaces for farm machinery resale

Development of refurbishment and remanufacturing hubs

Bundled financing and insurance for used equipment

Aftermarket service contracts and spare parts packages

Cross-border sourcing partnerships with Japan and China - Trends

Rising preference for reconditioned low-HP tractors

Increased online discovery and price comparison

Shift toward pay-per-use and rental models

Integration of basic telematics in refurbished equipment

Consolidation among regional used-equipment dealers

Growing demand for mechanization in horticulture - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Equipment Type (in Value %)

Used tractors

Used combine harvesters

Used rice transplanters

Used power tillers and two-wheel tractors

Used sprayers and spreaders

Used irrigation pumps and systems

Used threshers and post-harvest equipment - By Power Range (in Value %)

Below 30 HP

30–50 HP

51–80 HP

Above 80 HP - By Crop Application (in Value %)

Rice

Corn and secondary crops

Plantation crops

Horticulture and vegetables

Mixed farming - By Sales Channel (in Value %)

Authorized OEM pre-owned programs

Independent dealers and refurbishers

Farmer-to-farmer resale

Auctions and digital marketplaces

Importers of used machinery - By Buyer Type (in Value %)

Smallholder farmers

Medium and large commercial farms

Farmer cooperatives and associations

Agricultural contractors and service providers

Plantation operators - By Region (in Value %)

Java

Sumatra

Kalimantan

Sulawesi

Bali and Nusa Tenggara

Papua and Maluku

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (equipment portfolio breadth, refurbishment quality standards, pricing competitiveness, geographic dealer coverage, financing partnerships, spare parts availability, aftersales service network, digital sales capability)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Kubota Corporation

Yanmar Co., Ltd.

Mitsubishi Agricultural Machinery

Iseki & Co., Ltd.

Mahindra & Mahindra

CNH Industrial

AGCO Corporation

John Deere

PT Kubota Indonesia

PT Yanmar Indonesia

PT Indotraktor Utama

PT Traktor Nusantara

PT United Tractors Tbk

RDO Equipment Indonesia

Tata Hitachi Construction Machinery Indonesia

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now