Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Indonesia’s warehousing market is valued at approximately USD ~ billion based on a recent historical assessment, supported by rapid expansion of logistics infrastructure, growing domestic consumption, and increasing trade activity across Southeast Asia. Government data from the Ministry of Trade and logistics industry statistics indicate rising demand for modern storage facilities serving manufacturing, retail, and e commerce distribution networks. The expansion of industrial estates, port connectivity projects, and national logistics integration programs continues strengthening demand for large scale distribution centers and third party logistics warehousing facilities across the country.

Major warehousing hubs are concentrated in Jakarta, Surabaya, and Batam due to strong industrial ecosystems and proximity to key maritime trade corridors. Jakarta functions as the primary logistics gateway supported by large consumer markets and port access through Tanjung Priok, while Surabaya benefits from its role as a major distribution center for eastern Indonesia. Batam supports international trade flows due to its location near Singapore shipping routes. These urban logistics clusters attract major logistics operators, manufacturing companies, and third party logistics providers seeking efficient supply chain connectivity.

Market Segmentation

By Warehouse Type

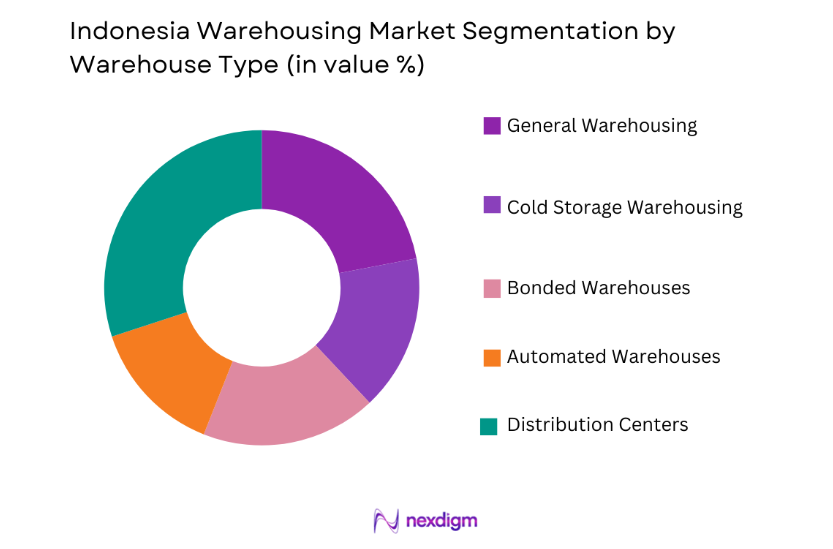

Indonesia Warehousing Market market is segmented by product type into general warehousing, cold storage warehousing, bonded warehouses, automated warehouses, and distribution centers. Recently, distribution centers have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Rapid growth of e commerce logistics and nationwide retail distribution networks requires large distribution centers capable of handling high inventory volumes and multi channel fulfillment operations. Logistics companies increasingly develop strategically located distribution hubs near major cities and transportation corridors to support fast delivery cycles and efficient inventory management. The expansion of national retail chains and manufacturing supply networks further strengthens demand for large distribution center facilities capable of serving multiple regional markets through centralized logistics operations.

By End User Industry

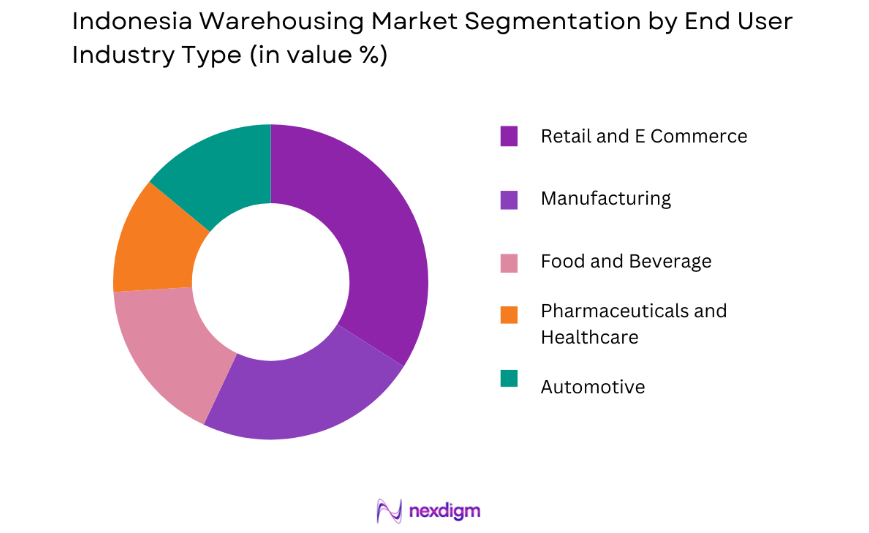

Indonesia Warehousing Market market is segmented by product type into retail and e commerce, manufacturing, food and beverage, pharmaceuticals and healthcare, and automotive. Recently, retail and e commerce has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Indonesia’s rapidly expanding digital retail ecosystem significantly increases demand for modern warehousing capacity capable of supporting high order volumes and fast delivery operations. Online marketplaces and omnichannel retailers rely on large fulfillment warehouses to manage product storage, order processing, and last mile distribution activities. Rapid urban population growth and increasing internet penetration encourage retailers to invest in strategically located warehouses that can serve metropolitan consumer markets efficiently.

Competitive Landscape

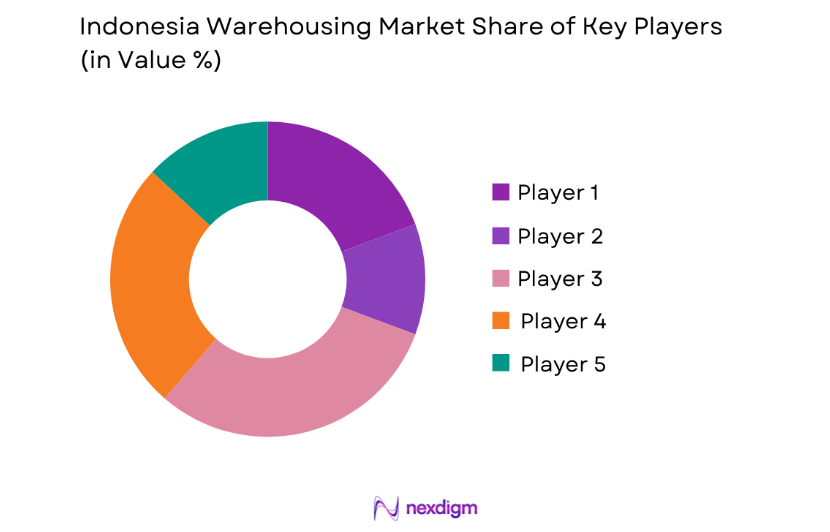

The Indonesia warehousing market demonstrates a moderately consolidated structure where large logistics operators coexist with regional warehouse developers and third party logistics providers. International logistics companies and domestic logistics groups are expanding storage capacity through industrial estate developments and logistics parks across major urban corridors. Major players compete through integrated logistics services, advanced warehouse automation, and nationwide distribution networks. Strategic partnerships with e commerce platforms and manufacturing companies further strengthen market positioning.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity Focus |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Germany | ~ | ~ | ~ | ~ | ~ |

| CEVA Logistics | 2007 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Agility Logistics | 1979 | Kuwait | ~ | ~ | ~ | ~ | ~ |

Indonesia Warehousing Market Analysis

Growth Drivers

Expansion of E Commerce Logistics and Omnichannel Retail Distribution Networks

Indonesia’s rapidly expanding digital commerce ecosystem significantly accelerates demand for modern warehousing infrastructure capable of supporting high volume fulfillment operations across major metropolitan markets. Online retail platforms require strategically located distribution centers to manage inventory storage, product sorting, and last mile logistics operations efficiently within dense urban environments. The rapid growth of online marketplaces encourages logistics providers to invest in automated warehouses equipped with advanced inventory management technologies and high capacity order processing systems. Large scale fulfillment facilities located near urban population centers enable retailers to deliver products within shorter delivery windows while maintaining efficient inventory turnover. Warehousing operators increasingly collaborate with e commerce platforms to develop specialized logistics facilities dedicated to digital retail supply chains. Rapid smartphone adoption and digital payment systems contribute to rising online transaction volumes that directly increase demand for storage infrastructure across logistics networks.

Expansion of Industrial Manufacturing and Export Oriented Logistics Infrastructure

Indonesia’s manufacturing sector continues expanding across automotive, electronics, and consumer goods industries, which significantly increases demand for large scale industrial warehousing facilities supporting supply chain operations. Manufacturing companies rely on warehouse infrastructure for raw material storage, component inventory management, and finished product distribution across domestic and international markets. Industrial estate development programs supported by government investment attract manufacturing companies seeking integrated logistics connectivity with ports, highways, and industrial clusters. Warehousing facilities located near manufacturing hubs enable companies to manage supply chain flows efficiently and reduce transportation costs across regional distribution networks. Export oriented industries require large storage facilities near port terminals to manage containerized goods awaiting international shipment through maritime trade routes. The expansion of Indonesia’s maritime logistics infrastructure strengthens the strategic role of warehouse facilities within global supply chains. Industrial logistics providers increasingly invest in specialized storage facilities designed for manufacturing supply chain operations including bonded warehouses and customs regulated logistics zones. As manufacturing output continues expanding across industrial clusters, demand for integrated warehouse infrastructure remains a critical component supporting national industrial development and trade logistics efficiency.

Market Challenges

Limited Availability of Modern Warehouse Infrastructure Across Secondary Cities

One of the primary challenges affecting the Indonesia warehousing market involves uneven distribution of modern logistics infrastructure across the country’s vast geographic regions. While major metropolitan areas such as Jakarta and Surabaya host advanced logistics facilities and industrial logistics parks, many secondary cities continue facing shortages of modern warehouse capacity. Limited infrastructure availability restricts efficient supply chain distribution networks serving smaller regional markets and rural consumer populations. Logistics providers often rely on outdated storage facilities that lack advanced inventory management systems and modern material handling equipment. Transportation bottlenecks and inconsistent infrastructure connectivity further complicate the development of new warehouse projects outside major urban logistics hubs. Investors and logistics companies face higher operational risks when expanding storage infrastructure into regions with limited logistics ecosystems and lower industrial activity levels. The lack of standardized warehouse design and limited adoption of automation technologies also affects operational efficiency across smaller logistics operators. Addressing infrastructure imbalances remains essential for developing nationwide warehousing networks capable of supporting Indonesia’s rapidly expanding logistics sector.

High Capital Investment Requirements for Automated Warehousing Facilities

Development of modern automated warehouses requires substantial capital investment in robotics systems, warehouse management technologies, and advanced material handling equipment. Logistics companies investing in automated distribution centers must allocate significant financial resources toward infrastructure construction, technology integration, and workforce training programs. High initial investment requirements often limit the ability of smaller logistics providers to adopt advanced warehouse technologies capable of improving operational efficiency. Companies must carefully evaluate long term return on investment before implementing large scale automation systems across logistics facilities. In addition, the integration of automated storage and retrieval systems requires highly specialized technical expertise and operational planning to ensure efficient performance. Maintenance costs and system upgrades further increase long term operational expenses associated with advanced warehouse automation infrastructure. These financial barriers slow the pace of technology adoption across segments of the warehousing industry and create operational disparities between large international logistics companies and smaller domestic operators.

Opportunities

Development of Smart Logistics Parks and Integrated Industrial Warehousing Zones

The development of large scale logistics parks across Indonesia creates significant opportunities for the warehousing industry as logistics providers seek integrated facilities combining storage, transportation, and distribution infrastructure within strategic industrial locations. Logistics parks enable companies to centralize warehousing operations while benefiting from direct connectivity to ports, highways, and manufacturing clusters. Industrial developers increasingly design logistics parks equipped with modern warehouse facilities capable of accommodating high capacity storage systems and automated logistics operations. These integrated logistics ecosystems support efficient supply chain management for manufacturing companies, retail distributors, and international trade logistics operators. Government initiatives aimed at strengthening national logistics competitiveness encourage investment in large scale logistics infrastructure projects across key economic corridors. Logistics parks also enable companies to consolidate distribution activities into centralized warehouse hubs capable of serving multiple regional markets efficiently. As industrial development expands across Indonesia’s economic zones, integrated logistics parks represent an important opportunity for expanding national warehousing capacity and improving supply chain efficiency.

Expansion of Cold Storage Infrastructure for Food and Pharmaceutical Supply Chains

Rising demand for temperature controlled logistics infrastructure presents significant opportunities for warehousing operators specializing in cold storage facilities supporting food distribution and pharmaceutical supply chains. Indonesia’s rapidly growing food processing industry and expanding pharmaceutical sector require specialized warehouse environments capable of maintaining controlled temperature conditions during storage and distribution. Cold storage facilities enable companies to preserve perishable products including seafood, dairy products, vaccines, and biotechnology products across long logistics networks spanning multiple islands. Government initiatives focused on improving national food security and strengthening healthcare supply chains further encourage investment in temperature controlled warehouse infrastructure. Logistics companies are increasingly developing specialized cold storage warehouses equipped with advanced refrigeration systems and real time monitoring technologies to maintain product quality and safety. As demand for high quality food imports and pharmaceutical distribution continues expanding across Indonesia’s growing population centers, cold storage warehousing infrastructure represents a critical growth opportunity within the broader logistics industry.

Future Outlook

Indonesia’s warehousing market is expected to experience steady expansion supported by the continued growth of e commerce logistics, industrial manufacturing activity, and national infrastructure modernization programs. Increasing investment in logistics parks, port connectivity projects, and automated warehouse technologies will improve supply chain efficiency across major economic corridors. Government initiatives focused on strengthening national logistics competitiveness will encourage private sector investment in advanced warehousing facilities. Demand from retail distribution networks, manufacturing exporters, and food supply chains will continue driving expansion of storage capacity across urban and industrial regions.

Major Players

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- CEVA Logistics

- Agility Logistics

- Aramex

- FedEx Logistics

- UPS Supply Chain Solutions

- Yusen Logistics

- CJ Logistics

- Toll Group

- Sinotrans Logistics

- Kerry Logistics

- Nippon Express

- Waresix

Key Target Audience

- Logistics and supply chain companies

- E commerce retailers

- Manufacturing and industrial companies

- Food and beverage manufacturers

- Pharmaceutical and healthcare distributors

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying major variables influencing the Indonesia Warehousing Market including logistics infrastructure, industrial development, trade activity, and e commerce distribution demand. These variables help determine the structural drivers shaping storage capacity expansion and supply chain logistics performance across Indonesia.

Step 2: Market Analysis and Construction

Market analysis involves evaluating warehousing infrastructure capacity, logistics investment activity, and industry demand patterns across major industrial clusters and logistics corridors. Secondary sources such as government logistics reports, trade statistics, and corporate financial data are used to construct the market structure.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses are validated through consultation with logistics industry experts, supply chain managers, and infrastructure analysts who provide insights into warehouse utilization trends and logistics infrastructure investment patterns across Indonesia’s logistics sector.

Step 4: Research Synthesis and Final Output

All collected data and expert insights are synthesized into a structured research framework that evaluates market dynamics, infrastructure development trends, and competitive positioning within the Indonesia Warehousing Market, ensuring analytical accuracy and actionable insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E Commerce Fulfillment and Distribution Networks

Development of Industrial Logistics Parks and Trade Zones

Increasing Outsourcing of Warehousing Services by Manufacturing Companies - Market Challenges

Limited Availability of Modern Warehousing Infrastructure

High Land Acquisition and Development Costs

Infrastructure Constraints in Secondary Logistics Corridors - Market Opportunities

Growth of Smart Warehousing and Automation Technologies

Expansion of Cold Storage Warehousing for Food and Pharmaceutical Logistics

Development of Regional Distribution Centers Supporting ASEAN Trade - Trends

Adoption of Warehouse Automation and Robotics Technologies

Integration of Digital Warehouse Management Systems and Inventory Tracking - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

General Merchandise Warehousing Facilities

Automated Warehousing Systems

Cold Storage Warehousing Facilities

Bonded Warehousing Facilities

E Commerce Fulfillment Warehouses - By Platform Type (In Value%)

Industrial Logistics Parks

Urban Distribution Warehousing Hubs

Port Based Warehousing Facilities

Airport Cargo Warehousing Facilities - By Fitment Type (In Value%)

Standalone Warehousing Facilities

Integrated Logistics Hub Warehouses

Automated High Bay Warehouses

Multi Client Shared Warehouses - By End User Segment (In Value%)

Manufacturing and Industrial Companies

Retail and E Commerce Distribution Companies

Food and Pharmaceutical Distribution Companies

- Market Share Analysis

- Cross Comparison Parameters (Warehouse Storage Capacity, Automation Technology Integration, Geographic Distribution Coverage, Warehouse Facility Infrastructure Quality, Cold Storage Capability, Logistics Network Connectivity, Strategic Industry Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain Indonesia

DB Schenker Indonesia

Kuehne + Nagel Indonesia

DSV Indonesia

CEVA Logistics Indonesia

Yusen Logistics Indonesia

Nippon Express Indonesia

Agility Logistics Indonesia

CJ Logistics Indonesia

Samudera Indonesia Logistics

Wahana Prestasi Logistik

RPX Logistics

Pos Logistics Indonesia

JNE Logistics

SiCepat Ekspres Logistics

- Manufacturing Companies Expanding Inventory Storage and Distribution Infrastructure

- Retail and E Commerce Platforms Increasing Demand for Fulfillment Warehouses

- Food and Pharmaceutical Companies Requiring Temperature Controlled Storage Facilities

- Export Oriented Industries Utilizing Bonded Warehousing Facilities

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now