Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Indonesia’s wealth management market oversees financial assets exceeding USD ~ billion held across bank-managed investment products, discretionary portfolios, mutual funds, pension assets, and private client mandates based on recent central bank and financial services authority disclosures. Market expansion is driven by rising affluent households, corporate wealth accumulation, and increasing financial asset formalization through regulated investment channels. Rapid growth in domestic capital markets, mutual fund penetration, and private banking offerings has expanded professionally managed wealth pools across institutional and retail high-value client segments.

Jakarta dominates Indonesia’s wealth management activity due to concentration of financial institutions, capital market infrastructure, and high-income households with diversified financial portfolios. Surabaya and Bandung follow as secondary wealth hubs supported by regional entrepreneurship, family business ownership, and property-linked wealth transitioning into financial assets. Singapore also influences Indonesian wealth management flows because affluent Indonesians maintain offshore portfolios and cross-border private banking relationships, reinforcing regional financial integration and advisory connectivity between domestic and international wealth platforms.

Market Segmentation

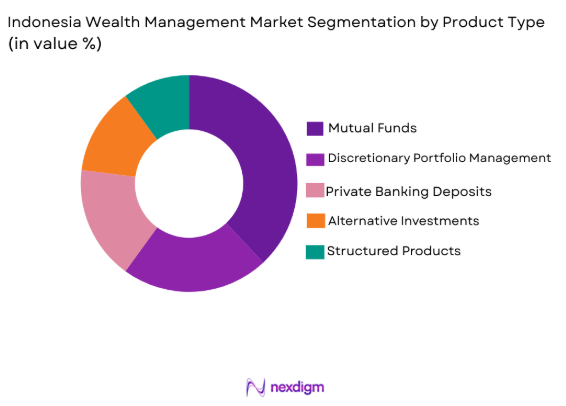

By Product Type

Indonesia Wealth Management market is segmented by product type into discretionary portfolio management, mutual funds, structured products, alternative investments, and private banking deposits. Recently, mutual funds have a dominant market share due to factors such as broad retail accessibility, strong domestic asset management brand presence, regulatory promotion of collective investment schemes, and growing investor preference for diversified professionally managed products over direct securities selection. Distribution through banks and digital investment platforms has expanded participation among affluent and emerging affluent households transitioning savings into market-linked assets. Mutual funds also benefit from tax efficiency relative to direct investments and simplified onboarding processes supported by electronic identification frameworks. Continuous product innovation across fixed income, equity, balanced, and sharia-compliant funds has enabled portfolio customization aligned with varying risk profiles, reinforcing sustained dominance within Indonesia’s wealth management asset allocation landscape.

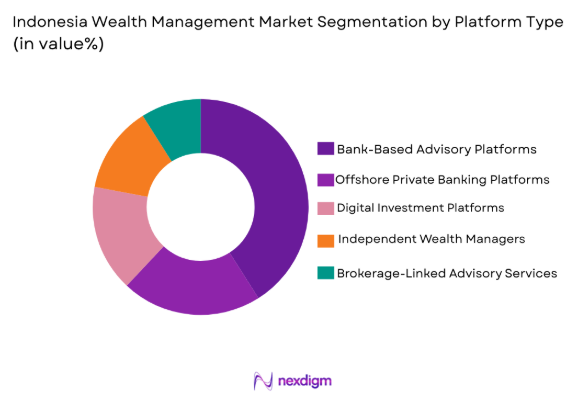

By Platform Type

Indonesia Wealth Management market is segmented by platform type into bank-based advisory platforms, independent wealth managers, digital investment platforms, offshore private banking platforms, and brokerage-linked advisory services. Recently, bank-based advisory platforms have a dominant market share due to factors such as nationwide branch infrastructure, integrated banking relationships with affluent clients, and trust advantages associated with established financial institutions managing investment assets. Indonesian high-net-worth individuals often consolidate deposits, credit, and investments within primary banks, enabling cross-selling of wealth products and discretionary mandates through relationship managers. Regulatory oversight and deposit protection frameworks also reinforce confidence in bank-led wealth channels compared with independent or digital-only providers. Banks additionally offer both onshore and offshore investment access through partnerships with global asset managers, enabling diversified portfolio allocation while maintaining centralized advisory relationships, sustaining structural leadership of bank-anchored wealth platforms.

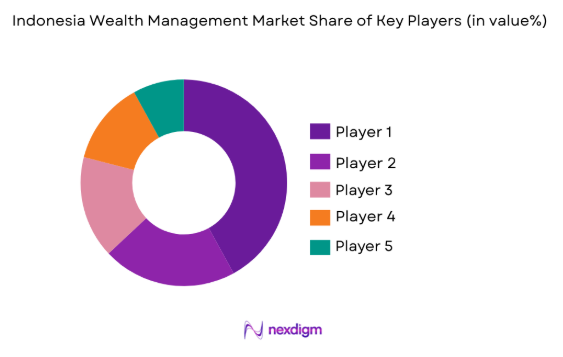

Competitive Landscape

Indonesia’s wealth management market shows moderate consolidation led by large domestic banks and international private banking institutions that control high-value client relationships and product distribution channels. Major players leverage integrated banking, asset management, and offshore advisory capabilities to capture affluent clients transitioning into financial assets. Competition centers on portfolio customization, cross-border investment access, and digital advisory integration. Domestic banks maintain scale advantages through branch reach and deposit relationships, while global private banks compete through offshore diversification and sophisticated discretionary mandates.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Client Segment Focus |

| Bank Mandiri | 1998 | Jakarta | Digital wealth advisory | ~ | ~ | ~ | ~ |

| Bank Central Asia | 1957 | Jakarta | Integrated wealth platform | ~ | ~ | ~ | ~ |

| Bank Negara Indonesia | 1946 | Jakarta | Hybrid advisory systems | ~ | ~ | ~ | ~ |

| HSBC Indonesia | 1884 | London | Global private banking tech | ~ | ~ | ~ | ~ |

| UBS Indonesia | 1862 | Zurich | Discretionary mandate platforms | ~ | ~ | ~ | ~ |

Indonesia Wealth Management Market Analysis

Growth Drivers

Rising Affluent Population and Financial Asset Formalization

Indonesia’s wealth management market expansion is fundamentally driven by sustained growth in affluent and high-net-worth households generated through entrepreneurship, family business ownership, corporate leadership compensation, and capital market participation that collectively increase demand for professional asset allocation and advisory services across domestic financial institutions. As Indonesian companies expand regionally and domestic capital markets deepen, business owners and executives accumulate investable financial assets requiring structured portfolio diversification beyond traditional real estate and bank deposits. Wealth holders increasingly transition assets into regulated financial instruments such as mutual funds, discretionary mandates, and structured investments due to improved investor education, regulatory oversight, and trust in institutional asset managers. Intergenerational wealth transfer dynamics are also intensifying demand because second-generation heirs prefer professionally governed portfolios with transparent reporting and risk management frameworks rather than informal family asset management practices. Domestic banks and asset managers capture this demand through dedicated wealth divisions, priority banking tiers, and portfolio management services tailored to affluent and high-net-worth segments. Indonesia’s expanding middle-upper class with rising disposable income further contributes to emerging affluent investors entering managed investment channels earlier in their wealth accumulation cycle. Regulatory strengthening by financial authorities has formalized investment distribution and enhanced investor protection, reinforcing migration from unregulated assets into supervised wealth products. Tax incentives for certain investment vehicles and improved capital market accessibility through electronic platforms also support financial asset formalization. Collectively these structural shifts expand the addressable wealth pool managed by professional institutions and sustain long-term growth in Indonesia’s wealth management market.

Digital Investment Platforms and Distribution Modernization

Indonesia’s wealth management growth is strongly supported by rapid digitalization of investment distribution channels that enable scalable access to professionally managed financial products across geographically dispersed affluent and emerging affluent populations. Digital investment platforms operated by banks, fintech firms, and asset managers allow clients to open accounts, allocate portfolios, and monitor performance remotely without dependence on physical branches, significantly reducing onboarding friction and advisory costs. Smartphone penetration and widespread familiarity with mobile financial applications have normalized digital engagement with investments among younger affluent investors and urban professionals seeking convenient portfolio management. Wealth institutions leverage data analytics and automated risk profiling tools to deliver personalized asset allocation recommendations aligned with investor objectives, improving suitability and client experience. Integration of digital advisory interfaces with banking ecosystems allows seamless transfer of deposits into investment products, accelerating conversion from savings to managed assets. Digital reporting dashboards provide transparency and continuous portfolio visibility, strengthening investor confidence and engagement with wealth products. Fintech partnerships also enable access to diversified domestic and global funds previously available only through private banking channels, democratizing wealth services. Regulatory support for electronic identification and online distribution frameworks has legitimized digital wealth channels and encouraged institutional adoption. Continuous innovation in robo-advisory, goal-based investing tools, and hybrid advisory models combining human relationship managers with digital interfaces is expanding the reach and efficiency of wealth management delivery across Indonesia’s evolving investor landscape.

Market Challenges

Low Financial Literacy and Preference for Physical Assets

Indonesia’s wealth management market faces structural constraints from relatively low financial literacy levels among large segments of the population, which sustains strong cultural preference for tangible assets such as real estate, gold, and cash savings over diversified financial portfolios managed by institutions. Many affluent households historically accumulated wealth through property ownership or family businesses and remain cautious about allocating significant assets into market-linked investments due to perceived volatility and limited familiarity with financial instruments. Limited understanding of portfolio diversification and risk management reduces willingness to engage discretionary asset managers or invest in structured products, slowing penetration of professional wealth services. Informal advisory practices within family or community networks often substitute for institutional wealth planning, delaying transition toward regulated asset management channels. Market downturn episodes in equities or mutual funds have reinforced investor conservatism and preference for capital-preserving assets. Geographic dispersion across islands also restricts physical advisory access in some regions, reinforcing reliance on traditional asset forms. Although digital platforms are expanding reach, trust in remote financial services remains uneven outside major cities. Wealth institutions must invest heavily in investor education, advisory engagement, and relationship building to shift entrenched asset allocation behavior. This structural bias toward non-financial assets constrains the proportion of national wealth entering managed portfolios and moderates the pace of wealth management market expansion.

Offshore Wealth Migration and Cross-Border Asset Booking

Indonesia’s wealth management sector experiences persistent leakage of high-net-worth assets into offshore financial centers, particularly Singapore, where affluent Indonesians maintain bank accounts, discretionary portfolios, and investment structures managed by international private banks outside domestic institutions. Offshore booking is driven by perceptions of stronger regulatory stability, broader global investment access, confidentiality preferences, and established private banking relationships historically cultivated abroad. High-net-worth families often diversify geographically to mitigate domestic currency risk and political uncertainty, allocating substantial financial assets outside Indonesia’s regulated wealth ecosystem. Domestic wealth managers therefore compete not only with local peers but also with established offshore private banking hubs offering sophisticated discretionary mandates, alternative investments, and global custody services. Cross-border capital mobility allows affluent clients to shift assets rapidly in response to regulatory or market changes, reducing retention capacity of domestic institutions. Regulatory reporting requirements and tax considerations also influence booking location decisions among wealthy individuals. Domestic banks have expanded offshore advisory partnerships, yet full repatriation of wealth assets remains limited. This structural outflow reduces the scale of onshore assets under management and constrains development of advanced wealth products locally. Sustained offshore migration therefore remains a core challenge limiting Indonesia’s domestic wealth management market depth and institutional competitiveness.

Opportunities

Sharia-Compliant Wealth Management Expansion

Indonesia’s wealth management market holds significant growth potential through expansion of sharia-compliant investment products and advisory services aligned with the country’s large Muslim affluent population seeking financial solutions consistent with religious investment principles. Demand for halal asset allocation across equities, sukuk, mutual funds, and discretionary mandates is increasing among high-net-worth individuals and family offices prioritizing ethical investment screening and faith-aligned financial planning. Islamic wealth management platforms integrating zakat planning, inheritance structuring, and sharia portfolio construction remain underdeveloped relative to demand, creating opportunity for specialized asset managers and banks. Regulatory frameworks supporting Islamic finance and certification of sharia-compliant funds provide institutional credibility and investor assurance. Wealth institutions can capture this segment by offering integrated Islamic discretionary portfolios, global halal investment access, and family wealth governance services. Growth of Islamic capital markets and sukuk issuance expands investable asset universe for sharia portfolios. Digital platforms can further distribute halal investment products to affluent clients beyond major cities. International Islamic asset managers may partner with Indonesian banks to expand product sophistication and cross-border halal investment channels. As religiously aligned investing gains prominence among affluent Muslim investors, sharia wealth management represents a structurally significant opportunity within Indonesia’s evolving wealth ecosystem.

Domestic Capital Market Deepening and Alternative Investment Access

Indonesia’s wealth management market stands to benefit from ongoing deepening of domestic capital markets and gradual expansion of alternative investment opportunities that increase portfolio diversification avenues for affluent investors and strengthen domestic asset management capabilities. Growth in corporate bond issuance, infrastructure investment vehicles, real estate investment trusts, and private equity participation expands investable instruments available to wealth managers constructing diversified portfolios. Affluent clients increasingly seek exposure beyond traditional deposits and public equities, creating demand for structured products, private market investments, and thematic funds managed locally. Government initiatives supporting capital market development and financial sector modernization enhance market liquidity and institutional participation. Domestic asset managers can capture higher value mandates by offering sophisticated multi-asset and alternative investment strategies previously accessible mainly offshore. Pension fund and sovereign investment activity also strengthens local financial ecosystem depth and product innovation. Wealth institutions integrating domestic alternatives into client portfolios improve retention of assets onshore by reducing reliance on offshore diversification channels. As Indonesia’s financial markets mature and broaden, domestic wealth management firms gain capacity to deliver comprehensive portfolio solutions comparable to international offerings. This structural evolution creates sustained opportunity for market expansion and competitive strengthening of Indonesia’s wealth management sector.

Future Outlook

Indonesia’s wealth management market is expected to expand steadily as affluent population growth, digital investment adoption, and capital market development increase professionally managed financial assets. Banks and asset managers will enhance hybrid advisory models combining digital platforms with relationship management to reach broader investor segments. Regulatory strengthening and investor education initiatives will accelerate financial asset formalization and domestic portfolio allocation. Expansion of sharia and alternative investment products will further diversify wealth solutions across Indonesia’s evolving investor landscape.

Major Players

- Bank Mandiri

- Bank Central Asia

- Bank Negara Indonesia

- HSBC Indonesia

- UBS Indonesia

- Standard Chartered Indonesia

- CIMB Niaga

- OCBC NISP

- Maybank Indonesia

- Schroders Indonesia

- Manulife AsetManajemen Indonesia

- Eastspring Investments Indonesia

- BNP Paribas Indonesia

- Citibank Indonesia

- Danareksa Investment Management

Key Target Audience

- Domestic commercial banks

- Asset management companies

- Private banking divisions

- Family offices

- High-net-worth investors

- Investments and venture capitalist firms

- Government and regulatory bodies

- Fintech wealth platforms

Research Methodology

Step 1: Identification of Key Variables

Key market variables including assets under management, investor segmentation, product distribution channels, and institutional participation were identified through regulatory disclosures, banking reports, and capital market statistics. These variables defined the structural boundaries of Indonesia’s wealth management ecosystem and enabled segmentation mapping across products and platforms.

Step 2: Market Analysis and Construction

Market structure was constructed by aggregating financial assets managed across banks, asset managers, and private wealth institutions, integrating capital market data and institutional balance sheet disclosures. Segmentation shares were derived through analysis of product penetration trends and distribution channel dominance within Indonesia’s financial services landscape.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market assumptions were validated using insights from financial sector reports, investment industry publications, and institutional strategy disclosures. Cross-verification ensured alignment between asset allocation behavior, investor demographics, and institutional wealth service expansion patterns across Indonesia.

Step 4: Research Synthesis and Final Output

All validated data and qualitative insights were synthesized into structured market assessment covering size, segmentation, competitive landscape, and outlook. Final outputs were standardized to ensure consistency across market definitions, segmentation logic, and institutional participation within Indonesia’s wealth management sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising High-Net-Worth Wealth from Entrepreneurial and Family Business Expansion

Deepening Capital Market Participation and Financial Asset Formalization

Banking Sector Expansion into Affluent and Emerging Wealth Segments

Growing Demand for Sharia-Compliant Wealth Management Solutions

Digital Wealth Platforms Expanding Investor Access Beyond Major Cities - Market Challenges

Limited Financial Literacy Among Emerging Affluent Investors

Fragmented Wealth Advisory Standards Across Providers

Regulatory Constraints on Cross-Border Investment Products

High Dependence on Relationship-Based Distribution Models

Concentration of Wealth in Illiquid Family Business Assets - Market Opportunities

Expansion of Family Office and Succession Planning Services

Growth of ESG and Sustainable Investment Mandates

Offshore Diversification Advisory for Indonesian Wealth Holders - Trends

- Integration of Digital Advisory and Hybrid Wealth Models

Increasing Allocation to Global Multi-Asset Portfolios

Institutionalization of Family Wealth Governance Structures

Rise of Sharia-Compliant Investment Products

Adoption of AI-Driven Portfolio Analytics and Reporting - Government Regulations & Defense Policy

Financial Services Authority Wealth Advisory Licensing Frameworks

Tax Reporting and Offshore Asset Disclosure Regulations

Capital Market Reforms Supporting Investment Product Diversity

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management Services

Advisory and Financial Planning Services

Trust and Estate Planning Solutions

Private Banking and Custody Services

Alternative Investment Management Platforms - By Platform Type (In Value%)

Bank-Led Wealth Platforms

Independent Asset Management Firms

Digital Wealth and Robo-Advisory Platforms

Brokerage-Integrated Wealth Platforms

Family Office Platforms - By Fitment Type

Onshore Managed Accounts

Offshore Managed Accounts

Hybrid Advisory Structures

Sharia-Compliant Wealth Mandates

Structured Product-Linked Portfolios - By End User Segment (In Value%)

Ultra-High-Net-Worth Individuals

High-Net-Worth Individuals

Affluent Mass Investors

Family-Owned Conglomerates

Institutional Private Clients - By Procurement Channel

Relationship Manager-Led Acquisition

Private Banking Channels

Digital Direct Platforms

Brokerage Referral Networks

Corporate and Family Office Mandates - By Material / Technology

AI-Driven Portfolio Analytics

Risk and Compliance Platforms

Client Reporting and Performance Systems

Multi-Asset Allocation Engines

Digital Onboarding and KYC Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Client Segment Coverage, Advisory Model, Investment Product Breadth, Digital Platform Capability, Sharia Offering Strength, Offshore Access, Relationship Network Depth, Fee Structure Transparency, Portfolio Customization Level)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bank Mandiri Wealth Management

Bank Central Asia Wealth Management

Bank Negara Indonesia Private Banking

CIMB Niaga Private Banking

Danamon Wealth Management

Maybank Indonesia Private Wealth

OCBC NISP Private Banking

Standard Chartered Indonesia Wealth

HSBC Indonesia Wealth Management

UOB Indonesia Private Banking

BNP Paribas Wealth Management Indonesia

UBS Indonesia Wealth Management

Credit Suisse Indonesia Wealth Advisory

Eastspring Investments Indonesia

Schroders Indonesia Wealth Advisory

- Entrepreneurial business owners dominate wealth demand with liquidity events from private enterprises and listings

- Family conglomerates require succession and governance advisory across multi-generational ownership structures

- Urban affluent professionals adopt managed portfolios through banking and digital wealth platforms

- Institutional private clients allocate treasury wealth through discretionary mandates

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now