Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Israel aerospace and defense composites market is valued at approximately USD ~billion in 2025, reflecting steady growth driven by increasing defense expenditures and the shift towards lightweight, durable materials in aerospace. The demand for composites is primarily fueled by the need for advanced materials to improve the performance, fuel efficiency, and longevity of defense and aerospace systems. Furthermore, the market’s expansion is supported by the development of cutting-edge technologies and innovations in composite manufacturing processes. The growing adoption of drones, UAVs, and military aircraft, along with increasing investments in defense research, significantly contribute to the growth trajectory.

Israel, with its robust defense sector and advanced aerospace industry, dominates the aerospace and defense composites market. The country benefits from government-backed initiatives, a strong industrial base, and high-level innovation in military and aerospace technology. Tel Aviv and Herzliya are key cities driving the market, with numerous defense and aerospace companies headquartered there, including Israel Aerospace Industries (IAI). These cities foster a thriving ecosystem for R&D, manufacturing, and the application of aerospace composites. The region’s geopolitical dynamics and its advanced technological infrastructure make Israel a dominant player in the global market.

Market Segmentation

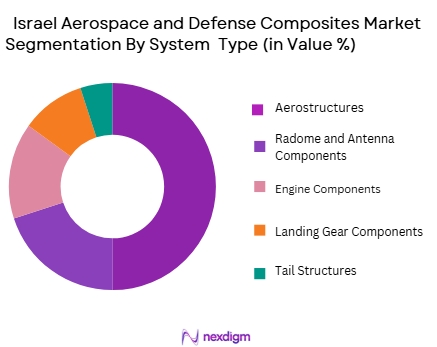

By System Type

The Israel aerospace and defense composites market is segmented by system type into aerostructures, radome and antenna components, engine components, landing gear components, and tail structures. Aerostructures hold a dominant market share, driven by the increasing demand for lightweight, high-strength materials in military and commercial aircraft. This segment benefits from technological advancements in composite materials that provide superior performance while reducing the overall weight of aircraft structures. As the need for more fuel-efficient and cost-effective aviation solutions rises, the demand for composite aerostructures is expected to continue growing in both military and commercial sectors.

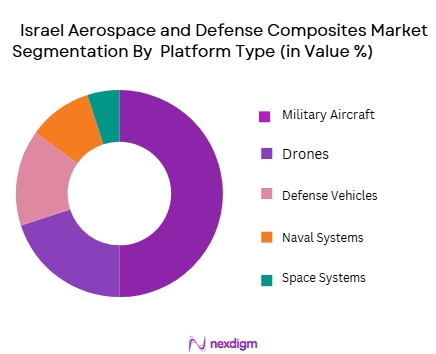

By Platform Type

The Israel aerospace and defense composites market is also segmented by platform type, including military aircraft, drones, defense vehicles, naval systems, and space systems. Military aircraft dominate this segment due to Israel’s ongoing advancements in defense technology and its significant military budget. The focus on next-generation fighter jets and surveillance aircraft increases the demand for high-performance composites that enhance the durability, stealth, and overall efficiency of these systems. Drones and UAVs are also gaining traction in the market, with increasing applications in reconnaissance, surveillance, and combat roles.

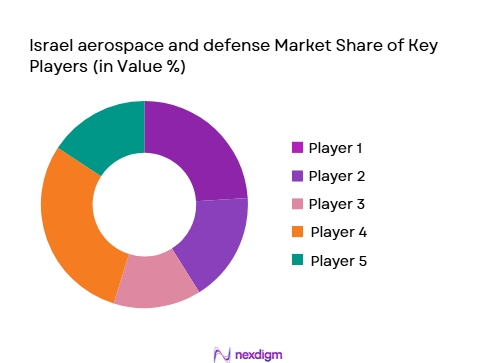

Competitive Landscape

The Israel aerospace and defense composites market is highly competitive, with several major players dominating the landscape. Companies such as Israel Aerospace Industries (IAI), Elbit Systems, and Rafael Advanced Defense Systems lead the market with a strong presence in both defense and aerospace sectors. These companies are known for their continuous innovation in composite technologies and are integral to Israel’s defense strategy. The market is characterized by a few large players with a significant technological edge, as well as several smaller companies specializing in specific aerospace components.

| Company Name | Establishment Year | Headquarters | Product Focus | Market Reach | Technological Advancements | Strategic Initiatives |

| Israel Aerospace Industries | 1953 | Tel Aviv, Israel | ~ | ~ | ~ | ~ |

| Elbit Systems | 1966 | Haifa, Israel | ~ | ~ | ~ | ~ |

| Rafael Advanced Defense Systems | 1958 | Haifa, Israel | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, USA | ~ | ~ | ~ | ~ |

| Boeing | 1916 | Chicago, USA | ~ | ~ | ~ | ~ |

Israel aerospace and defense composites Market Analysis

Growth Drivers

Rising Popularity of Adventure Tourism

The global trend towards unique adventure sports has led to increased demand for hang gliding experiences, particularly in regions like Singapore, known for its scenic landscapes and tourist appeal. As tourists seek thrilling activities, hang gliding presents a popular choice. Local companies are capitalizing on this demand by offering tailored experiences, creating an accessible entry point for both tourists and locals, contributing significantly to market growth. This surge in eco‑tourism and experiential travel has directly boosted participation rates, making hang gliding a key activity for adventurous travelers and enthusiasts alike.

Advancements in Hang Glider Technology

Continuous innovation in glider design and materials, such as lightweight carbon fiber, has made hang gliders more durable, safe, and affordable. These technological improvements attract a broader audience, including those who might have been hesitant due to concerns over equipment reliability. Moreover, advancements in navigation and safety features, such as GPS tracking and improved weather prediction tools, enhance the flying experience and make it safer for both beginners and experienced pilots. As these technological enhancements continue to evolve, the market for hang gliders is expected to expand, driving more participation and investments.

Market Challenges

Regulatory & Safety Concerns

The primary challenge faced by the Singapore hang gliding market is the regulatory and safety framework that governs the sport. Hang gliding requires strict adherence to aviation safety standards, often leading to high compliance costs. Additionally, safety concerns, such as equipment failure and weather risks, may deter potential participants. Regulatory bodies have implemented measures to ensure safety, but these restrictions can slow the sport’s adoption by limiting the number of certified pilots and schools. This creates a barrier for the sport’s growth, especially in a region with strict aviation rules like Singapore.

High Cost of Participation

Despite the increasing interest in hang gliding, the sport remains relatively expensive, with high initial costs for purchasing quality equipment, including gliders, harnesses, and safety gear. Additionally, there are ongoing costs for maintenance and storage. For many individuals, these costs represent a significant barrier, preventing widespread adoption, especially in a market where leisure activities compete for disposable income. The high cost is further compounded by the need for specialized training and certification. This makes hang gliding a niche activity that may appeal only to those with sufficient disposable income or a deep passion for aviation sports.

Opportunities

Growth of Eco‑Tourism & Adventure Packages

Singapore, with its tourism-focused economy, has an excellent opportunity to integrate hang gliding into eco-tourism and adventure tourism offerings. By collaborating with travel agencies and tour operators, hang gliding experiences can be packaged with other outdoor activities, attracting both international and local tourists. Eco-conscious travelers are increasingly seeking sustainable, adrenaline‑filled experiences, making hang gliding a prime option. Operators could also offer combined packages with nature walks, wildlife tours, or aerial sightseeing tours, giving tourists a holistic adventure experience while boosting the appeal of the sport in the region’s tourism industry.

Expanding Training and Certification Programs

One of the most significant opportunities in the Singapore hang glider market lies in expanding training and certification programs. With rising interest in the sport, more professional schools and organizations can be established to provide rigorous pilot training. Offering more affordable or flexible options for certification could attract a broader range of participants. Additionally, creating corporate training programs or partnering with educational institutions for aviation-related courses could help nurture a new generation of glider pilots. Expanding these programs would help solidify hang gliding as a mainstream activity, leading to sustainable market growth.

Future Outlook

Over the next decade, the Israel aerospace and defense composites market is expected to witness substantial growth, driven by continued advancements in composite materials and a growing focus on defense technologies. The integration of composite materials in UAVs, military aircraft, and drones is poised to gain significant momentum as Israel continues to modernize its defense systems. Furthermore, as demand for lightweight, fuel-efficient materials grows across both military and commercial aerospace, Israel’s dominance in composite materials will likely solidify. Continued government investments and technological advancements will fuel the expansion of the market during the forecast period.

Major Players

- Israel Aerospace Industries

- Elbit Systems

- Rafael Advanced Defense Systems

- Lockheed Martin

- Boeing

- Northrop Grumman

- Airbus

- General Dynamics

- Raytheon Technologies

- Saab

- Thales Group

- L3 Technologies

- Leonardo

- BAE Systems

- Honeywell Aerospace

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace and defense manufacturers

- Military and defense agencies

- Aerospace component suppliers

- Aircraft manufacturers

- Military equipment distributors

- Aerospace material research labs

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying all key variables that influence the Israel aerospace and defense composites market, including technology adoption, regulatory environment, and demand for advanced materials. This phase involves desk research, secondary data collection from industry sources, and stakeholder interviews to define the factors that impact market growth.

Step 2: Market Analysis and Construction

In this phase, historical data on the market is analyzed to identify patterns in demand, pricing, and material usage across different aerospace and defense applications. This data will form the basis for projecting future trends and help us to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Our market hypotheses are validated through consultations with experts from Israel Aerospace Industries, Elbit Systems, and other key market players. These consultations provide real-world insights into technological trends and future projections, which refine our initial assumptions and ensure that our forecast is accurate.

Step 4: Research Synthesis and Final Output

The final phase synthesizes the data collected through previous steps, combining both top-down and bottom-up analyses. Interviews with leading defense and aerospace manufacturers validate and complement our statistical findings, ensuring that the final market report is comprehensive, accurate, and reflective of real-world market conditions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased defense spending globally

Rising demand for lightweight and fuel-efficient materials

Technological advancements in composite manufacturing - Market Challenges

High initial manufacturing costs

Complexity in composite material certifications

Vulnerability to geopolitical tensions - Market Opportunities

Expanding defense budgets in emerging markets

Growing demand for advanced drones and UAVs

Increasing interest in military-civil integration projects - Trends

Shift toward automation in composite manufacturing processes

Integration of AI and IoT for predictive maintenance

Advancements in 3D printing for aerospace components - Government regulations

Export restrictions on defense technologies

Regulations governing composite material testing and certification

Environmental regulations on waste disposal and recycling of composites - SWOT analysis

- Porters 5 forces

- By Market Value ,2020-2025

- By Installed Units ,2020-2025

- By Average System Price ,2020-2025

- By System Complexity Tier ,2020-2025

- By System Type (In Value%)

Aerostructures

Radome and Antenna Components

Engine Components

Landing Gear Components

Tail Structures - By Platform Type (In Value%)

Military Aircraft

Drones

Defense Vehicles

Naval Systems

Space Systems - By Fitment Type (In Value%)

OEM

Aftermarket

Upgrades & Refurbishments

Maintenance

Repair & Overhaul (MRO) - By EndUser Segment (In Value%)

Military

Commercial Aerospace

Defense Contractors

Government and Law Enforcement

Space Agencies - By Procurement Channel (In Value%)

Direct Procurement from Manufacturers

Third-Party Distributors

E-commerce Platforms

Government Tenders

OEM Partnerships

- Cross Comparison Parameters (Material innovation, Production capabilities, Compliance with regulations, Price competitiveness, Distribution network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Israel Aerospace Industries

Elbit Systems

Rafael Advanced Defense Systems

Lockheed Martin

Boeing

Northrop Grumman

Airbus

General Dynamics

Raytheon Technologies

Saab

Thales Group

L3 Technologies

Leonardo

BAE Systems

Honeywell Aerospace

- Increased adoption of composites in military aircraft for enhanced performance

- Growing use of composites in drones and UAVs for lightweight design

- Rising need for advanced composites in naval and defense vehicles

- Strong demand from space agencies for durable composite materials

- Forecast Market Value,2026-2035

- Forecast Installed Units,2026-2035

- Price Forecast by System Tier,2026-2035

- Future Demand by Platform,2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now