Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Israel aerospace bearing market is valued at USD ~million, based on extensive research and historical data from key aerospace manufacturers and suppliers in the region. This market is primarily driven by the significant demand from Israel’s defense and aerospace sector, supported by the country’s strong presence in military aviation and satellite technologies. Additionally, advancements in UAVs and an increasing number of commercial aircraft projects contribute to the robust growth of the aerospace bearing market. Notably, government spending on defense, technological innovation, and the growing reliance on local manufacturing hubs are all key contributors to the market’s size and expansion.

Israel is at the forefront of the aerospace bearing market due to its robust aerospace and defense ecosystem, with major players like Israel Aerospace Industries and Elbit Systems leading the way. Tel Aviv and Herzliya are the key cities driving the market due to their concentration of aerospace R&D facilities, manufacturing plants, and defense contractors. These cities host several aerospace hubs and act as centres for advanced technological innovation in bearings, particularly those needed for high-stress environments such as military and space applications. The dominance of Israel in this market can be attributed to its strong government defense expenditure, advanced technological capabilities, and strategic partnerships with global aerospace players.

Market Segmentation

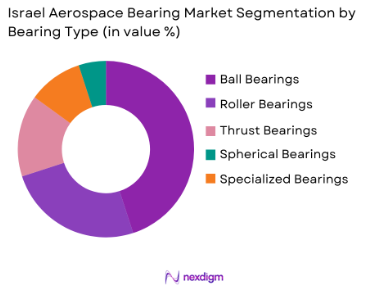

By Bearing Type

The Israel aerospace bearing market is segmented by bearing type into ball bearings, roller bearings, thrust bearings, spherical bearings, and specialized aerospace bearings. The ball bearing segment currently dominates the market share, particularly in military aircraft and UAV applications. This dominance is driven by the reliability and high-performance characteristics of ball bearings in critical aerospace systems. They offer superior load distribution, reduced friction, and are highly suitable for environments that require minimal maintenance. This makes them a preferred choice for both commercial and defense aerospace platforms, where reliability and operational efficiency are paramount.

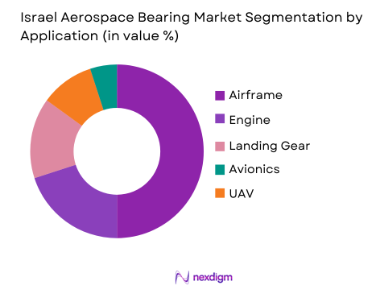

By Application

The market is also segmented by application into airframe, engine, landing gear, avionics, and UAV components. The airframe bearing segment leads the market share, primarily due to the large demand for aerospace bearings used in flight control systems, fuselage assembly, and wing structures. Airframe bearings are integral to the structural integrity and movement of major flight control surfaces, such as ailerons and rudders. The increasing need for efficient and reliable bearings in airframe applications, especially for military aircraft and next-generation UAVs, has contributed significantly to the growth and dominance of this segment.

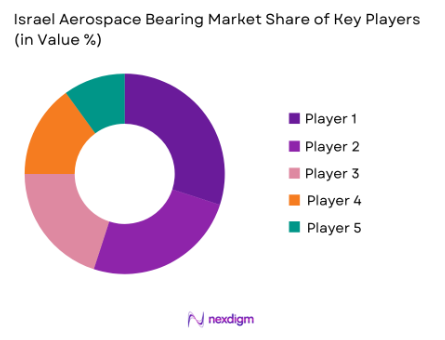

Competitive Landscape

The Israel aerospace bearing market is dominated by a combination of domestic players and global aerospace bearing manufacturers. Companies such as Israel Aerospace Industries (IAI) and Elbit Systems are leaders in the domestic market, benefiting from strong government contracts and high-demand defense projects. Meanwhile, international players like SKF Group and Timken Corporation also play a significant role due to their well-established product portfolios and global supply chains.

| Company Name | Establishment Year | Headquarters | Revenue ($M) | Product Portfolio | Technology Focus | Key Markets |

| Israel Aerospace Industries (IAI) | 1953 | Tel Aviv, Israel | ~ | ~ | ~ | ~ |

| Elbit Systems | 1966 | Haifa, Israel | ~ | ~ | ~ | ~ |

| SKF Group | 1907 | Gothenburg, Sweden | ~ | ~ | ~ | ~ |

| Timken Company | 1899 | North Canton, USA | ~ | ~ | ~ | ~ |

| RBC Bearings | 1919 | Oxford, USA | ~ | ~ | ~ | ~ |

Israel Aerospace Bearing Market Dynamics

Growth Drivers

Defense Modernization

Defense modernization is one of the primary growth drivers for the Israel aerospace bearing market. Israel has been increasing its defense budget year after year, with defense spending reaching approximately USD ~billion in 2023, constituting nearly 5.5% of its GDP. The focus on modernizing military platforms, including fighter jets, drones, and air defense systems, is leading to a higher demand for advanced aerospace components, such as bearings. The Israeli government’s commitment to upgrading its defense infrastructure aligns with global defense spending trends, which are projected to increase as geopolitical tensions persist. The growing investment in defense modernization is evident in the acceleration of the development of Israel’s F-35 fleet and other advanced aerospace programs, which require high-precision bearings. This focus on modern, capable military technology, bolstered by continued national security priorities, continues to drive growth in the aerospace bearing sector.

UAV Proliferation

The proliferation of unmanned aerial vehicles (UAVs) is another significant driver of the aerospace bearing market. Israel remains one of the global leaders in UAV technology, with the country exporting over USD~billion in UAV systems annually, accounting for a significant portion of its defense exports. UAVs, particularly for military surveillance, reconnaissance, and combat, are becoming increasingly popular, pushing demand for lightweight, high-durability aerospace bearings. As per the Israel Defense Export Statistics, Israel’s UAV exports saw a 10% increase in 2023 compared to previous years. The rapid development of UAV technology requires precision bearings that can withstand extreme conditions and stress. The UAV industry’s robust growth is pushing the need for high-performance bearings, designed to endure long missions in harsh environmental conditions, thus contributing to the market’s expansion.

Market Restraints

Certification Costs

Certification remains a significant restraint in the Israel aerospace bearing market. The cost of obtaining certifications for aerospace bearings, such as AS9100, NADCAP, and other military-grade certifications, is a substantial barrier to entry for smaller manufacturers and an ongoing financial burden for existing players. Certification costs can range from USD ~to USD ~ million, depending on the specific requirements for each bearing type, especially in military or space applications. Furthermore, the stringent approval processes from authorities like the Israel Civil Aviation Authority (ICAA) and international regulatory bodies add additional layers of complexity and cost. As Israel continues to focus on expanding its aerospace and defense capabilities, these rising certification and compliance costs are a major constraint, limiting the pace at which some manufacturers can introduce innovative bearing solutions into the market.

Raw Material Price Volatility

Raw material price volatility continues to challenge the aerospace bearing market. The prices of key materials such as stainless steel, titanium, and ceramic are highly volatile and are subject to fluctuations in global supply chains. For instance, the price of titanium surged by 30% in 2023 due to supply disruptions caused by geopolitical tensions and restrictions on Russian exports, a major global supplier. The aerospace bearing sector heavily depends on these raw materials, and price increases directly impact production costs. The World Bank’s Commodity Markets Outlook notes that materials essential to aerospace manufacturing, such as titanium and steel, are expected to experience continued price volatility through 2025, adding pressure to manufacturers relying on cost-effective materials for aerospace bearings. This volatility, exacerbated by geopolitical tensions, limits the ability of manufacturers to predict long-term production costs and makes raw material procurement a key challenge.

Opportunities

Advanced Material Adoption

The increasing adoption of advanced materials in the aerospace sector presents substantial growth opportunities for the Israel aerospace bearing market. Materials such as ceramic composites, carbon fiber-reinforced polymers (CFRPs), and lightweight alloys are being integrated into aerospace bearings to meet the rising demand for high-performance components. The Israeli Aerospace Industries (IAI) and other major manufacturers are already incorporating these advanced materials in various aerospace applications, leading to a growing trend of lightweight and more durable bearings in the market. For example, the adoption of ceramic hybrid bearings, which offer high performance at extreme temperatures, is growing due to their lower weight and enhanced reliability. Additionally, CFRPs are increasingly used in military and commercial aircraft components to reduce overall weight, thereby enhancing fuel efficiency and performance. With continued technological advancements, the demand for aerospace bearings made from these materials is expected to increase, providing a fertile ground for innovation and growth in the sector.

Expansion of Space Exploration

The ongoing expansion of space exploration is a key opportunity for the Israel aerospace bearing market. Israel’s growing interest in space, demonstrated by the success of its SpaceIL mission and partnerships with global space agencies, has created new opportunities for aerospace bearing manufacturers. Space exploration projects require highly specialized, durable, and high-performance bearings capable of withstanding extreme conditions, such as temperature fluctuations and intense pressures. With Israel’s space sector continuing to grow, driven by initiatives like the National Space Program and private sector collaborations, the demand for space-grade bearings is expected to rise. The Israel Space Agency (ISA) reports an increasing number of satellite launches and space-related projects, which directly impacts the need for precision bearings designed for space applications. These initiatives, alongside Israel’s technological advancements in space research, position the aerospace bearing market for significant growth in the coming years.

Future Outlook

The Israel aerospace bearing market is expected to show consistent growth over the next decade, primarily driven by the increasing demand for advanced defense technologies, aerospace platforms, and unmanned aerial vehicles (UAVs). With continuous government investment in aerospace and defense programs, the market is projected to witness robust growth. Innovations in bearing technologies, such as ceramic bearings and high-performance composites, are expected to further fuel the demand. Additionally, the rising global need for space exploration and satellite systems will create new opportunities for bearing manufacturers specializing in space-grade components.

Major Players

- Israel Aerospace Industries (IAI)

- Elbit Systems

- SKF Group

- Timken Company

- RBC Bearings

- Thomson Industries

- Rollon Group

- Schaeffler Group

- JTEKT Corporation

- NTN Corporation

- Precision Bearing Services

- Kaman Aerospace

- Aerospace Bearing Company

- Woodward Inc.

- Carter Bearings

Key Target Audience

- Aerospace Manufacturers

- Military and Defense Agencies

- UAV Manufacturers

- Aviation OEMs

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodie

- Aerospace Tier-1 Suppliers

- Aerospace Component Distributors

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the core variables influencing the Israel aerospace bearing market, which includes aircraft demand, defense budget allocation, technological advancements, and government regulations. This is done through comprehensive desk research, utilizing secondary and proprietary databases.

Step 2: Market Analysis and Construction

We then gather historical and current data to assess the market size, segmentation, and key players. Market penetration, revenue generation, and service performance are analyzed to ensure the accuracy of the data.

Step 3: Hypothesis Validation and Expert Consultation

We test market hypotheses with industry experts through surveys, interviews, and computer-assisted telephone interviews (CATIs). This allows us to obtain firsthand insights regarding product specifications, pricing strategies, and consumer needs.

Step 4: Research Synthesis and Final Output

Finally, the synthesized data is validated by engaging with leading aerospace bearing manufacturers to confirm the accuracy of the data and ensure the final report reflects a comprehensive view of the market.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Data Sources and Verification, Macro‑Micro Market Sizing Approaches, Supply Chain Mapping Methodology, Industry Expert Interview Framework, Limitations and Future Directions)

- Market Definition & Scope

- Israel Aerospace Industry Ecosystem

- Role of Aerospace Bearings in Platform Reliability

- National Aviation Standards & Compliance Regimes

- Regional Aerospace Supply Chain & Value Chain

- Israel’s Export Orientation & Dual‑Use Technology Influence

- Growth Drivers

Defense Modernization

UAV proliferation - Market Restraints

Certification Costs

Raw Material

Price Volatility - Market Opportunities

Advanced Material Adoption

Expansion of Space Exploration - Key Market Trends

Digital Twins

Predictive Bearing Health

- Total Market Value, 2020-2025

- Volume Output, 2020-2025

- Market Price Trends, 2020-2025

- By Material & Engineering Class (In Value %)

High‑Grade Stainless & Aerospace Alloys

Ceramic Hybrid Bearings

Titanium & Super‑Alloy Bearings

Composite & Coated Bearings

Corrosion‑Resistant Specialty Materials - By Application (In Value %)

Airframe & Flight Control Bearings

Engine / Turbine Bearings

Landing Gear & Actuation Bearings

Avionics & Precision Instrument Bearings

UAV / Drone Bearings - By End Market (In Value %)

Commercial Aviation OEMs

Military & Defense Platforms

MRO

Space & Satellite Components

Aerospace Sub‑Contractors & Integrators

- By Distribution Channel (In Value %)

Direct OEM Supply Contracts

Authorized Distributors

Aftermarket / MRO Distribution

Export / Global Trade Flows

Local Israeli Procurement Channels

- Market Share by Value & Volume

- Cross Comparison Parameters (Technical Certification Levels, Precision Engineering Capabilities, Product Portfolio Breadth, Production Capacity & Scalability Metrics, R&D Intensity, Aftermarket Support Infrastructure, Defense & Civil Contract Backlog, Export Footprint & Trade Compliance)

- Porter’s Five Forces

- Major Profiles

Israel Aerospace Industries

Elbit Systems

Wipro Givon Ltd.

Ashot Ashkelon Industries

ACS Motion Control

BTS Components Ltd.

Local Authorized Distributors of Aerospace Bearings

SKF Group

Timken Company

NSK Ltd.

NTN Corporation

RBC Bearings Incorporated

JTEKT Corporation

Pacamor Kubar Bearings

Schatz Bearing Corporation

- Demand concentration among defense and military aviation operators

- Growing utilization by UAV manufacturers and integrators

- Stable replacement demand from commercial aviation MRO activities

- Emerging demand from space and satellite subsystem suppliers

- Projection: Value Growth – Commercial + Defense, 2026-2035

- Volume Forecast – High‑Precision Bearings, 2026-2035

- Price & Product Mix Evolution, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now