Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Israel Digital Glass Military Aircraft Cockpit Systems market is expected to witness significant growth due to the rising demand for advanced cockpit systems in military aircraft. The market is driven by the growing need for enhanced pilot situational awareness, integration of smart technologies, and military modernization programs. The increasing adoption of digital glass technology, particularly in head-up displays and touchscreen systems, has led to greater efficiency, safety, and operational capabilities for military aviation. This market is forecasted to generate a value of USD 1.8 billion by 2024 based on a recent historical assessment.

Dominant countries in the Israel Digital Glass Military Aircraft Cockpit Systems market include Israel, the United States, and several European nations. Israel’s dominance in this field is largely due to its advanced aerospace technology sector, government support for defense innovations, and significant investments in R&D. Additionally, Israel’s strategic partnerships with leading defense contractors and its focus on military-grade technology development further contribute to its leadership in the market.

Market Segmentation

By Product Type

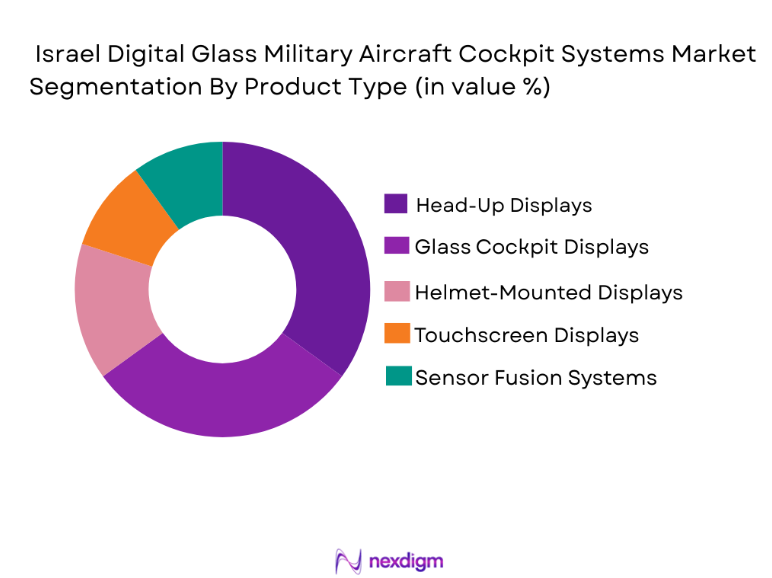

Israel Digital Glass Military Aircraft Cockpit Systems market is segmented by product type into Head-Up Displays, Glass Cockpit Displays, Helmet-Mounted Displays, Touchscreen Displays, and Sensor Fusion Systems. Recently, the Head-Up Display (HUD) sub-segment has dominated the market due to its critical role in improving situational awareness for pilots during combat and adverse conditions. HUD systems allow pilots to view essential flight information directly in their line of sight, reducing the need for head movement and increasing operational efficiency. Furthermore, advancements in optical technology and a growing preference for integration into digital glass systems have made HUDs increasingly popular in military aircraft.

By Platform Type

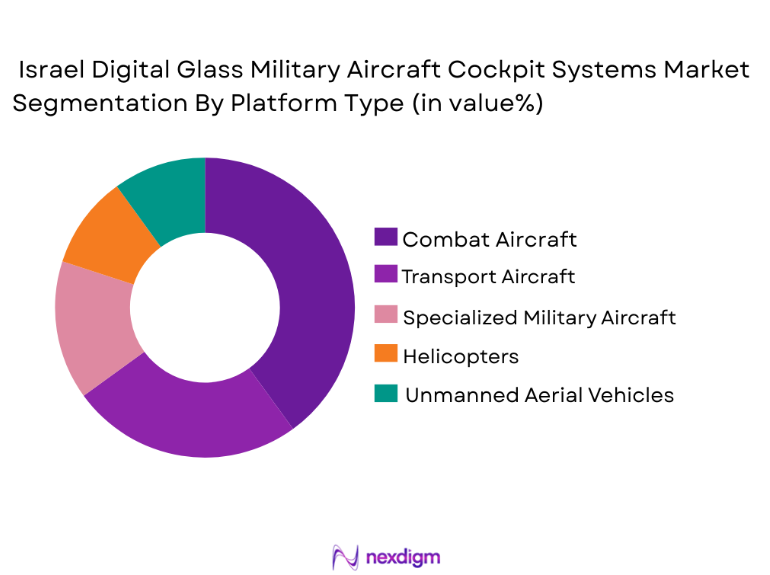

Israel Digital Glass Military Aircraft Cockpit Systems market is segmented by platform type into Combat Aircraft, Transport Aircraft, Specialized Military Aircraft, Helicopters, and Unmanned Aerial Vehicles (UAVs). The Combat Aircraft sub-segment leads the market due to the increasing integration of digital cockpit systems in high-performance military jets, essential for enhanced situational awareness during combat operations. These aircraft require cutting-edge display technologies for real-time data processing, advanced navigation, and communication systems, which have driven demand for digital glass cockpit solutions. The growing complexity of combat missions and the need for immediate decision-making capabilities are further contributing to the widespread adoption of these systems in combat aircraft.

Competitive Landscape

The competitive landscape of the Israel Digital Glass Military Aircraft Cockpit Systems market is shaped by consolidation among a few key players who hold significant technological expertise and defense contracts. Major companies in the market focus on continuous innovation, strategic collaborations, and extensive R&D investments to maintain their market position. These players provide integrated solutions and modular systems to cater to the growing demand for advanced cockpit technology, thus driving the competitive intensity in the market.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Product Innovations |

| Elbit Systems | 1966 | Israel | ~ | ~ | ~ | ~ | ~ |

| Israel Aerospace Industries | 1953 | Israel | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 1893 | France | ~ | ~ | ~ | ~ | ~ |

| BAE Systems | 1999 | UK | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

Israel Digital Glass Military Aircraft Cockpit Systems Market Analysis

Growth Drivers

Increasing Demand for Enhanced Pilot Situational Awareness

The demand for advanced cockpit systems is primarily driven by the need to enhance pilot situational awareness in military aircraft. As military operations become more complex and fast-paced, pilots must rely on real-time data to make critical decisions. Digital glass cockpit systems, particularly head-up displays and touchscreen interfaces, offer enhanced visibility and easier access to flight data, allowing pilots to maintain focus on their missions. The integration of augmented reality (AR) and sensor fusion technologies into these systems further improves their effectiveness, providing pilots with a 360-degree view of the battle space and reducing cognitive load. Moreover, the advancements in display technology, which reduce glare and improve readability in diverse lighting conditions, make these systems indispensable for modern military aircraft. As defense budgets increase globally, especially in regions like Israel and the U.S., the market for advanced cockpit systems is expected to continue expanding.

Integration of Smart Technologies in Military Aircraft

The ongoing trend of integrating smart technologies into military aviation systems is significantly boosting the growth of digital glass cockpit systems. The integration of artificial intelligence (AI), machine learning (ML), and predictive analytics is enhancing the decision-making process for pilots, providing them with insights that would otherwise be inaccessible during high-pressure situations. For example, AI-based predictive maintenance can help identify potential failures before they occur, while machine learning algorithms can optimize flight paths based on real-time conditions. As military forces around the world invest in smarter, more autonomous aircraft, digital cockpit systems are evolving to accommodate these advanced technologies, driving further market demand. This trend is especially prominent in Israel, where there is significant government investment in cutting-edge defense technologies.

Market Challenges

High Development and Maintenance Costs

One of the major challenges facing the Israel Digital Glass Military Aircraft Cockpit Systems market is the high cost associated with the development and maintenance of these advanced systems. The cost of manufacturing sophisticated digital displays, integrating sensor technologies, and ensuring compliance with military standards for reliability and durability is significant. This has led to high upfront costs for procurement, limiting the adoption of digital glass cockpit systems, especially in countries with smaller defense budgets. Furthermore, the maintenance and calibration of these systems require specialized knowledge and equipment, which adds to the operational costs for defense contractors and military agencies. Additionally, the constant need for software updates and the integration of newer technologies also contributes to the high costs of these systems. These financial barriers can make it difficult for smaller defense contractors to enter the market, as they may lack the resources to develop and maintain these advanced system.

Security Risks and Cyber Threats

Another challenge that the market faces is the increasing security risks and cyber threats targeting military aircraft and their cockpit systems. Digital cockpit systems, being integrated with numerous sensors, displays, and data communication channels, are susceptible to hacking, malware attacks, and electronic warfare tactics. A breach in the cockpit system can result in loss of control, misinformation, or even compromised military missions. With the rise of cyber threats in the defense sector, securing digital glass cockpit systems has become a top priority for manufacturers. The need for robust cybersecurity protocols, encryption, and redundancy in the design of these systems is increasing. However, implementing such measures increases the complexity and cost of developing and maintaining these systems, creating a challenge for market players to strike a balance between security and cost-effectiveness.

Opportunities

Emerging Demand for Autonomous and Unmanned Aircraft Cockpit Systems

One of the most significant opportunities in the Israel Digital Glass Military Aircraft Cockpit Systems market is the growing demand for autonomous and unmanned aircraft systems (UAS). As the military sector continues to explore unmanned aerial vehicles (UAVs) for a wide range of operations, including surveillance, reconnaissance, and even combat missions, the need for sophisticated cockpit systems for these aircraft is also increasing. These systems are being designed to provide autonomous capabilities, such as automated flight control, real-time mission data analysis, and remote piloting. Digital glass cockpit systems for UAVs are being integrated with advanced technologies, including AI, to enable autonomous flight paths, dynamic mission planning, and improved operational efficiency. The growing investments in UAV technology, particularly in Israel, which has a strong focus on drone warfare and autonomous aircraft, present a major growth opportunity for digital glass cockpit systems

Advancements in Augmented Reality for Aircraft Displays

Another opportunity in the market is the increasing integration of augmented reality (AR) into cockpit display systems. AR enhances the pilot’s ability to interpret data by overlaying critical information directly onto the cockpit’s visual field, allowing for faster decision-making in critical situations. As AR technology continues to evolve, its applications in military aviation are expanding, particularly in training, mission planning, and flight operations. Israel, known for its technological innovations in defense, is at the forefront of this trend, and the country’s military forces are increasingly adopting AR-based cockpit systems to improve pilot efficiency and safety. This opportunity is expected to grow as the global defense sector invests in next-generation technologies to enhance the effectiveness and safety of military aircraft.

Future Outlook

The Israel Digital Glass Military Aircraft Cockpit Systems market is expected to experience substantial growth over the next five years, driven by advancements in display technologies, artificial intelligence integration, and the increasing demand for unmanned and autonomous aircraft systems. Technological developments in augmented reality, artificial intelligence, and sensor fusion are expected to shape the future of military cockpit systems, making them more intuitive and efficient for pilots. Additionally, growing defense budgets and increased government support for military modernization initiatives will further propel market growth. With countries like Israel leading the way in defense innovation, the market is poised for significant technological advancements and continued expansion.

Major Players

- Elbit Systems

- Israel Aerospace Industries

- Thales Group

- BAE Systems

- Northrop Grumman

- Honeywell International

- L3 Technologies

- Safran

- Saab Group

- General Electric

- Textron

- Harris Corporation

- Lockheed Martin

- Raytheon Technologies

- Rockwell Collins

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Military contractors

- Aerospace manufacturers

- Aircraft operators

- Aircraft maintenance and repair organizations

- Defense technology providers

- Aviation authorities

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the critical factors that drive market growth, such as technological advancements, regulatory changes, and defense spending.

Step 2: Market Analysis and Construction

In this step, a detailed analysis of historical data, market trends, and key factors influencing market demand is conducted to build a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

The findings from market analysis are validated through consultations with industry experts, key stakeholders, and primary data sources to ensure the reliability and accuracy of the research.

Step 4: Research Synthesis and Final Output

The final market report is synthesized, integrating all research findings, data analysis, and expert insights into a structured format to provide actionable recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Demand for Enhanced Pilot Situational Awareness

Rising Military Aircraft Modernization Programs

Technological Advancements in Glass Cockpit Systems

Increase in Aerospace Defense Budgets

Integration of Smart Technologies in Military Aircraft - Market Challenges

High Development and Maintenance Costs

Interoperability Issues with Legacy Systems

Regulatory and Compliance Barriers

Security Risks and Cyber Threats

Long Product Development Cycles - Market Opportunities

Emerging Demand for Autonomous and Unmanned Aircraft Cockpit Systems

Advancements in Augmented Reality for Aircraft Displays

Integration of Artificial Intelligence in Pilot Assistance Systems - Trends

Integration of Artificial Intelligence for Display Management

Growing Adoption of Multi-Function Displays

Increased Use of Augmented Reality in Cockpits

Evolution of Smart HUD (Head-Up Display) Systems

Development of Modular and Scalable Cockpit Solutions - Government Regulations & Defense Policy

Compliance with International Aviation Standards

Regulations on Exporting Military-Grade Technologies

Government Funding for Aerospace Defense R&D - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Head-Up Displays

Glass Cockpit Displays

Helmet-Mounted Displays

Touchscreen Displays

Sensor Fusion Systems - By Platform Type (In Value%)

Combat Aircraft

Transport Aircraft

Specialized Military Aircraft

Helicopters

Unmanned Aerial Vehicles (UAVs) - By Fitment Type (In Value%)

Retrofit Solutions

OEM (Original Equipment Manufacturer) Solutions

Modular Systems

Integrated Systems

Customization Solutions - By EndUser Segment (In Value%)

Military Forces

Government Defense Agencies

Private Defense Contractors

Aerospace Technology Providers

Airline Operators (military support) - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Military Auctions

Third-Party Distributors - By Material / Technology (In Value%)

OLED Displays

LCD Displays

LED Displays

Waveguide Technology

Fused Glass Technology

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Elbit Systems

Israel Aerospace Industries

Rockwell Collins

Thales Group

BAE Systems

Northrop Grumman

Honeywell International

L3 Technologies

Safran

Saab Group

General Electric

Textron

Harris Corporation

Lockheed Martin

Raytheon Technologies

- Military Forces’ Requirement for Advanced Display Systems

- Government Defense Agencies’ Procurement Patterns

- Private Defense Contractors’ Role in Technological Integration

- Aerospace Technology Providers’ Focus on Innovation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now