Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Israel Intelligence Surveillance Reconnaissance Market was valued at USD ~ billion based on a recent historical assessment derived from official Israeli defense budget disclosures, Ministry of Defense procurement records, and publicly reported contract values associated with intelligence, surveillance, and reconnaissance programs. Market expansion is driven by sustained investments in unmanned aerial systems, satellite reconnaissance assets, advanced sensor payloads, and artificial intelligence–enabled data fusion platforms. Continuous modernization of intelligence infrastructure, emphasis on persistent situational awareness, and integration of multi-domain surveillance systems across air, land, sea, cyber, and space environments continue to support stable procurement volumes and long-term system deployment programs.

Based on a recent historical assessment, market dominance is concentrated within Israel, supported by key defense and intelligence hubs located in Tel Aviv, Haifa, Beersheba, and surrounding aerospace and technology corridors. Israel maintains dominance due to persistent regional security pressures, advanced domestic defense manufacturing capabilities, and strong alignment between intelligence agencies and indigenous technology developers. Government-backed research initiatives, high defense R&D spending, and deep integration between operational intelligence units and system developers reinforce national leadership. Strategic collaboration with allied nations further strengthens domestic production, system refinement, and sustained demand for intelligence, surveillance, and reconnaissance solutions.

Market Segmentation

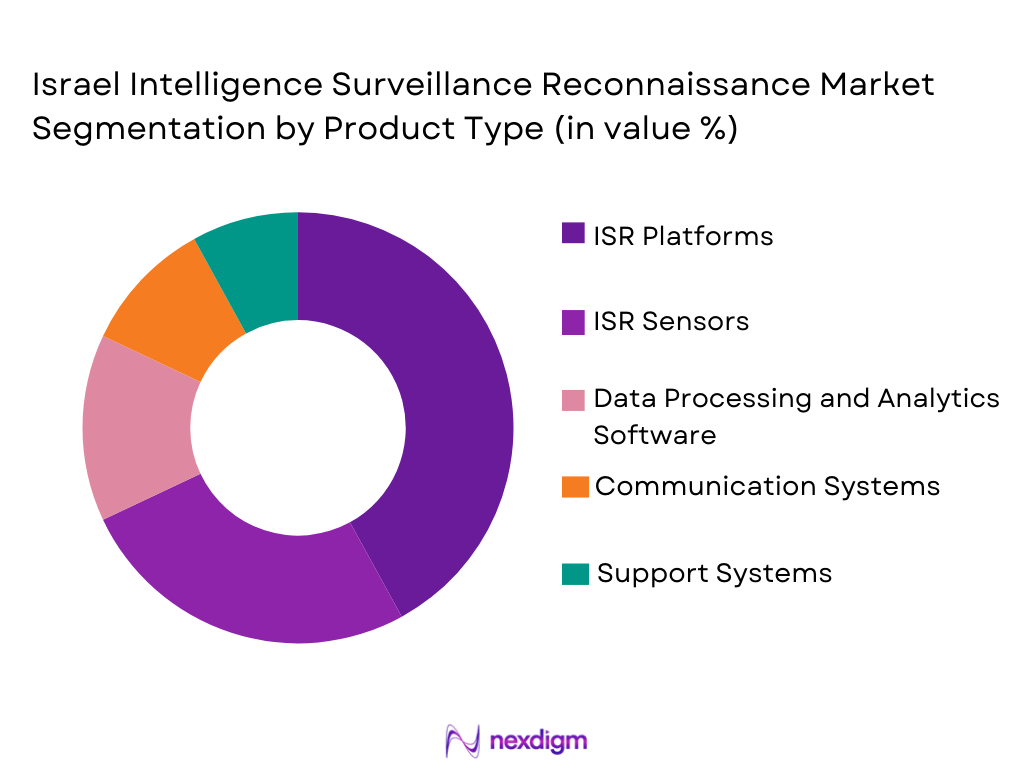

By Product Type:

Israel Intelligence Surveillance Reconnaissance Market is segmented by product type into ISR platforms, ISR sensors, data processing and analytics software, communication systems, and support services. Recently, ISR platforms have a dominant market share due to extensive procurement of unmanned aerial vehicles, manned reconnaissance aircraft, and satellite systems forming the core of national intelligence operations. Platform dominance is reinforced by defense doctrines prioritizing persistent surveillance, multi-mission adaptability, and rapid deployment. These platforms integrate advanced sensors and secure communication architectures, making them indispensable assets. Long acquisition cycles, high unit costs, and continuous upgrade programs further consolidate dominance, while government preference for indigenous platform development ensures sustained capital allocation toward platform-centric ISR capabilities.

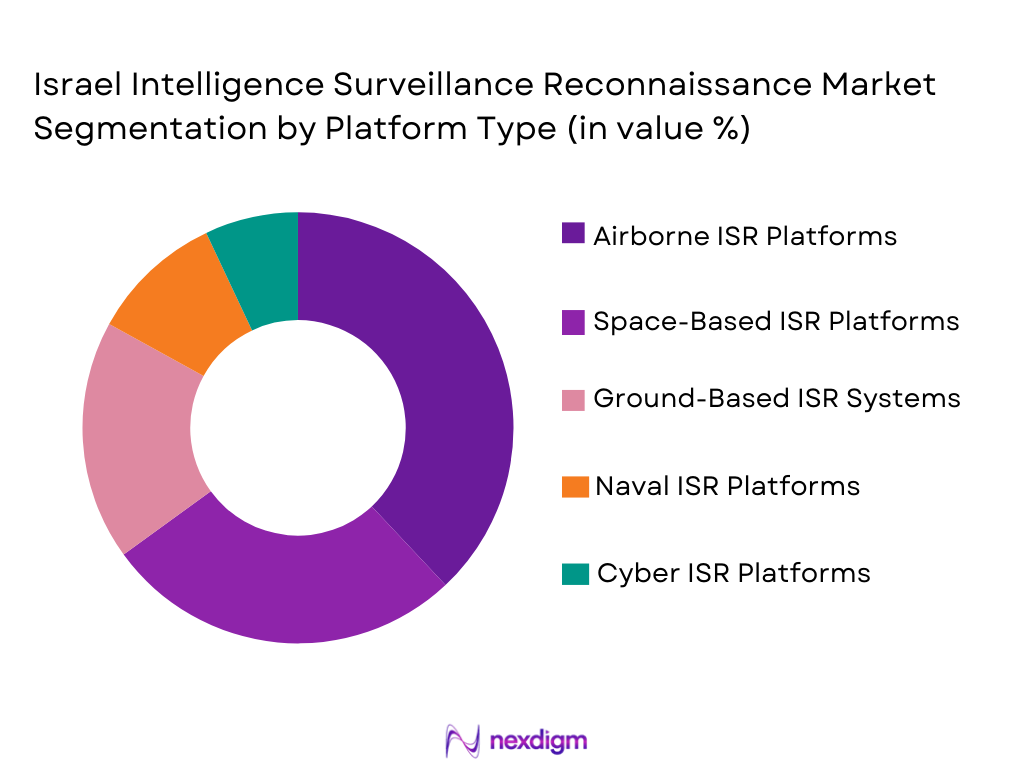

By Platform Type:

Israel Intelligence Surveillance Reconnaissance Market is segmented by platform type into airborne, space-based, ground-based, naval, and cyber ISR platforms. Recently, airborne platforms have a dominant market share due to their operational flexibility, rapid response capability, and extensive deployment across intelligence missions. Airborne ISR assets enable real-time intelligence collection, border surveillance, and tactical battlefield awareness, making them central to defense strategies. Strong emphasis on unmanned aerial systems enhances persistence while reducing operational risk. Faster acquisition cycles compared to space assets, combined with continuous payload upgrades, reinforce airborne platform dominance within the overall platform segmentation structure.

Competitive Landscape

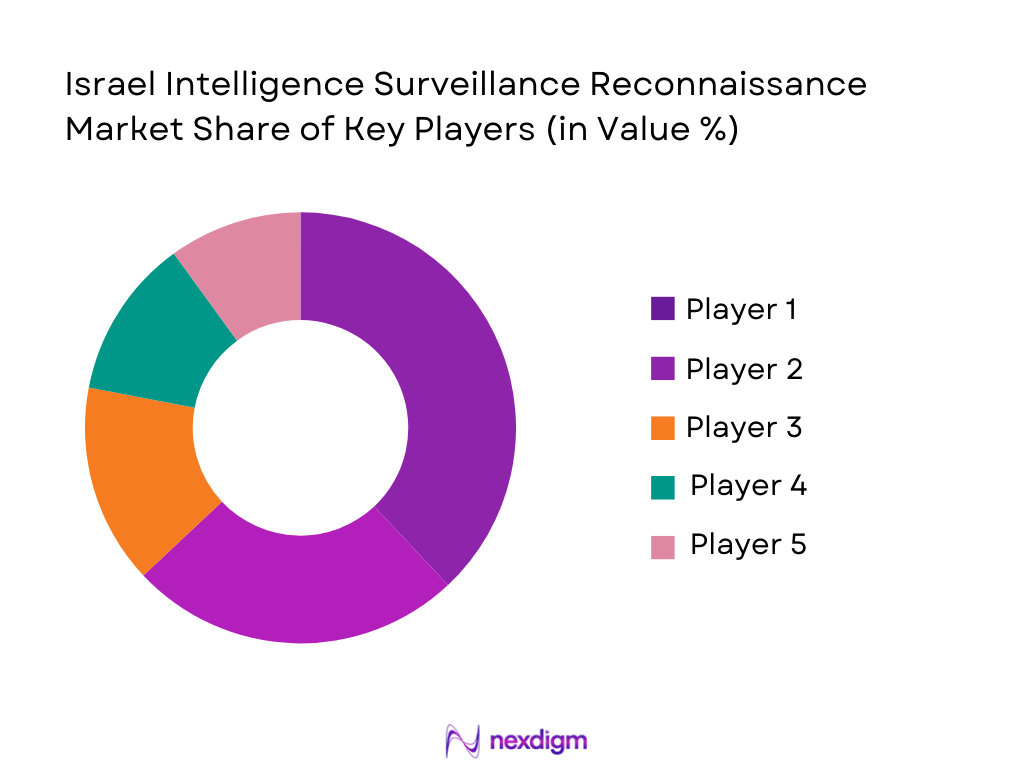

The competitive landscape of the Israel Intelligence Surveillance Reconnaissance Market is highly consolidated, dominated by established domestic defense companies with vertically integrated ISR capabilities and strong government alignment. Competition is driven primarily by technological sophistication, system integration depth, and long-term defense contracts rather than pricing. Indigenous firms benefit from close collaboration with intelligence agencies, enabling rapid customization and operational feedback-driven innovation. High entry barriers persist due to regulatory restrictions, security clearance requirements, and capital-intensive research and development needs. Strategic partnerships and export-oriented collaborations further reinforce the market position of leading players.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | R&D Intensity |

| Elbit Systems | 1966 | Israel | ~ | ~ | ~ | ~ | ~ |

| Israel Aerospace Industries | 1953 | Israel | ~

|

~

|

~

|

~

|

~

|

| Rafael Advanced Defense Systems | 1948 | Israel | ~

|

~

|

~

|

~

|

~

|

| Elta Systems | 1967 | Israel | ~

|

~

|

~

|

~

|

~

|

| Aeronautics Group | 1997 | Israel | ~

|

~

|

~

|

~

|

~

|

Israel Intelligence Surveillance Reconnaissance Market Analysis

Growth Drivers

Persistent Regional Security Threat Environment:

Persistent regional security threat environment continues to act as a core growth driver for the Israel Intelligence Surveillance Reconnaissance Market by compelling sustained investment in intelligence superiority and early-warning capabilities. Israel’s security doctrine prioritizes proactive threat detection, real-time intelligence, and continuous monitoring of hostile activities across land, air, sea, cyber, and space domains. This requirement drives continuous procurement of ISR platforms, advanced sensors, and analytics systems capable of operating in dense, contested environments. Intelligence agencies and defense forces require persistent surveillance to counter asymmetric threats, cross-border incursions, missile proliferation, and non-state actors. These operational realities increase demand for multi-layered ISR architectures integrating airborne, space-based, and ground systems. Continuous threat evolution also necessitates frequent system upgrades, software enhancements, and integration of new intelligence sources. As threats become more complex and technologically sophisticated, ISR systems must deliver higher resolution, faster processing, and secure dissemination of intelligence. This ongoing security pressure ensures long-term funding commitments, accelerates procurement cycles, and sustains high operational tempo, directly reinforcing market expansion across platforms, sensors, and intelligence processing solutions.

Rapid Advancement of Indigenous Defense Technology Ecosystem:

Rapid advancement of indigenous defense technology ecosystem significantly accelerates growth within the Israel Intelligence Surveillance Reconnaissance Market by enabling continuous innovation, faster deployment, and reduced reliance on external suppliers. Israel maintains a tightly integrated ecosystem linking defense forces, intelligence agencies, startups, and major defense manufacturers. This environment promotes rapid prototyping, operational testing, and iterative improvement of ISR technologies. Indigenous development capabilities allow tailored solutions addressing specific operational challenges, enhancing effectiveness and adoption. Government support through defense R&D funding, technology incubators, and procurement preferences strengthens domestic innovation pipelines. Integration of artificial intelligence, machine learning, and advanced data fusion into ISR systems is accelerated by strong local expertise. Close collaboration between end users and developers ensures rapid feedback loops, reducing development timelines and deployment risks. Indigenous manufacturing also supports lifecycle upgrades, sustainment, and scalability of ISR platforms. This ecosystem creates structural advantages, sustains competitive positioning, and drives continuous market demand for advanced intelligence, surveillance, and reconnaissance capabilities.

Market Challenges

High System Complexity and Integration Burden:

High system complexity and integration burden represent a significant challenge for the Israel Intelligence Surveillance Reconnaissance Market by increasing costs, deployment timelines, and operational risk. Modern ISR solutions require seamless integration of sensors, platforms, communication networks, analytics software, and command systems across multiple domains. Achieving interoperability between legacy systems and next-generation technologies presents technical challenges that demand extensive testing and customization. Complex integration processes raise program costs and extend procurement cycles, affecting budget efficiency. As ISR architectures expand, managing data volumes, latency, and system resilience becomes increasingly difficult. Integration challenges also increase dependence on specialized engineering expertise, limiting flexibility and scalability. Cybersecurity considerations further complicate integration, requiring hardened architectures and continuous monitoring. These factors collectively raise lifecycle costs and complicate system upgrades. As a result, procurement decisions may be delayed, deployment schedules extended, and operational readiness impacted, constraining market momentum despite strong underlying demand.

Regulatory Constraints and Export Control Restrictions:

Regulatory constraints and export control restrictions pose a substantial challenge to market growth by limiting technology transfer, international collaboration, and export opportunities. ISR technologies are subject to stringent national security regulations governing development, deployment, and sale. Compliance with defense export controls restricts access to certain international markets and complicates joint development programs. Regulatory approval processes increase transaction timelines and administrative overhead. Restrictions on sensitive technologies such as advanced sensors, encryption, and analytics software limit scalability of commercial operations. Export limitations also affect economies of scale, increasing per-unit costs for domestic procurement. Additionally, evolving cybersecurity and data protection regulations impose additional compliance requirements on ISR systems. These regulatory pressures create uncertainty for long-term planning, discourage some international partnerships, and constrain revenue diversification, presenting structural challenges for market participants.

Opportunities

Expansion of Artificial Intelligence Driven Intelligence Processing:

Expansion of artificial intelligence driven intelligence processing presents a major opportunity for the Israel Intelligence Surveillance Reconnaissance Market by transforming raw data into actionable intelligence at unprecedented speed. AI enables automated target recognition, anomaly detection, and predictive analytics, reducing analyst workload and decision latency. Integration of machine learning algorithms enhances accuracy across imagery, signals, and multi-source intelligence. Demand for AI-enabled ISR solutions is growing as operational environments generate vast data volumes. AI capabilities also improve scalability and adaptability of ISR systems across missions. Indigenous expertise in AI research positions market participants to commercialize advanced analytics solutions. Adoption of AI-driven processing enhances system value, drives upgrade demand, and opens new revenue streams through software and service offerings, strengthening long-term market prospects.

Growth of Space Based Surveillance Capabilities:

Growth of space based surveillance capabilities offers significant opportunity by expanding persistent, wide-area monitoring and strategic intelligence collection. Investments in reconnaissance satellites enhance early warning, missile tracking, and regional situational awareness. Space assets complement airborne and ground systems, enabling layered intelligence architectures. Advances in miniaturization and launch technologies reduce deployment costs and increase constellation resilience. Demand for space-based ISR supports platform development, sensor innovation, and data processing solutions. Integration of space intelligence into national command networks increases system complexity and value. This expansion creates long-term procurement opportunities and reinforces market depth across multiple technology segments.

Future Outlook

The Israel Intelligence Surveillance Reconnaissance Market is expected to maintain steady growth over the next five years driven by persistent security requirements, continuous technological innovation, and strong government support. Advancements in artificial intelligence, autonomous systems, and data fusion are expected to reshape intelligence operations. Regulatory alignment and defense modernization initiatives will continue to support procurement. Demand for multi-domain intelligence solutions is expected to intensify as operational environments become increasingly complex.

Major Players

- Elbit Systems

- Israel Aerospace Industries

- Rafael Advanced Defense Systems

- Elta Systems

- Aeronautics Group

- Orbit Communication Systems

- ContropPrecision Technologies

- Bird Aerosystems

- Steadicopter

- Camero-Tech

- SCD Semiconductor Devices

- UVisionAir

- Tera Group

- XTEND

- NSO Group Technologies

Key Target Audience

- Defense ministries

- Intelligence agencies

- Homeland security departments

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense procurement authorities

- Aerospace and defense OEMs

- Strategic infrastructure operators

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying critical variables influencing the Israel Intelligence Surveillance Reconnaissance Market. These include platform types, technology adoption, procurement patterns, and regulatory factors. Data sources are mapped to ensure coverage of demand and supply dynamics. Variables are validated for relevance and consistency.

Step 2: Market Analysis and Construction

Collected data is analyzed to construct market structures and segmentation frameworks. Quantitative and qualitative assessments are applied to evaluate trends and competitive dynamics. Cross-verification ensures accuracy and reliability. Market models are refined through iterative validation.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings are tested through expert consultation with industry and defense specialists. Assumptions are challenged and adjusted based on expert insights. Feedback loops improve analytical robustness. Final hypotheses reflect validated market realities.

Step 4: Research Synthesis and Final Output

Validated data and insights are synthesized into a coherent market narrative. Analytical outputs are aligned with research objectives. Findings are reviewed for consistency and clarity. The final report delivers structured, actionable intelligence.

- Executive Summary

- Israel Intelligence Surveillance Reconnaissance Market Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising regional security threats and intelligence requirements

Continuous modernization of national defense capabilities

Integration of artificial intelligence in ISR operations

Expansion of unmanned and autonomous surveillance platforms

Increased focus on real-time situational awareness - Market Challenges

High system integration and lifecycle costs

Complex regulatory and export control frameworks

Cybersecurity vulnerabilities in networked ISR systems

Dependence on advanced semiconductor supply chains

Operational complexity across multi-domain environments - Market Opportunities

Development of AI-driven predictive intelligence platforms

Expansion of space-based and high-altitude ISR assets

Growth in joint and allied intelligence-sharing frameworks - Trends

Multi-domain intelligence fusion architectures

Increased use of autonomous ISR systems

Real-time data analytics and edge computing

Enhanced interoperability across defense networks

Shift toward modular and scalable ISR solutions - Government Regulations & Defense Policy

Strengthening of national intelligence and cybersecurity laws

Defense procurement reforms supporting indigenous technology

Policies promoting secure data handling and intelligence sharing - SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Signals Intelligence Systems

Imagery Intelligence Systems

Measurement and Signature Intelligence Systems

Electronic Warfare Support Systems

Multi-Intelligence Fusion Platforms - By Platform Type (In Value%)

Airborne ISR Platforms

Ground-Based ISR Systems

Naval ISR Platforms

Space-Based ISR Assets

Cyber and Network-Based ISR Platforms - By Fitment Type (In Value%)

New Platform Integration

Retrofit and Upgrade Installations

Modular Payload Fitment

Mission-Specific Temporary Fitment

Integrated Command Network Fitment - By EndUser Segment (In Value%)

Defense Forces

Intelligence Agencies

Homeland Security Organizations

Border Security Authorities

Strategic Infrastructure Protection Units - By Procurement Channel (In Value%)

Direct Government Procurement

Defense OEM Contracts

System Integrator Partnerships

Intergovernmental Defense Programs

Emergency and Rapid Acquisition Channels - By Material / Technology (in Value %)

Advanced Sensor Materials

Artificial Intelligence Analytics

Secure Communication Technologies

Data Fusion and Processing Software

Miniaturized Electronics and Components

- Market structure and competitive positioning

- Market share snapshot of major players

CrossComparison Parameters (system integration capability, sensor range performance, data processing latency, interoperability standards, cybersecurity resilience, platform versatility, lifecycle support capability, technology innovation pace, procurement flexibility) - SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Elbit Systems

Israel Aerospace Industries

Rafael Advanced Defense Systems

Aeronautics Group

Elta Systems

NSO Group Technologies

Tera Group

Orbit Communication Systems

Controp Precision Technologies

Bird Aerosystems

XTEND

Steadicopter

Camero-Tech

UVision Air

SCD Semiconductor Devices

- Operational reliance on real-time intelligence for tactical decisions

- Demand for interoperable systems across military branches

- Focus on rapid deployment and adaptability of ISR assets

- Emphasis on secure and resilient communication networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now