Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Israel Mergers and Acquisitions in Aerospace and Defense market is significantly shaped by ongoing mergers and acquisitions (M&A) activities, driven by strategic partnerships and acquisitions between local and international firms. In 2023, the market was valued at USD ~ billion, influenced by a growing need for advanced defense technologies and collaborations. The M&A activities are largely motivated by a desire to bolster capabilities in unmanned aerial systems, cybersecurity, and missile defense systems. This trend reflects Israel’s strategic position in the global defense landscape, especially with the increasing demands for innovation and competitive advantage in aerospace technology.

The dominant countries within this market include Israel, the United States, and several European nations, notably the United Kingdom and France. Israel, as a major player in aerospace and defense, is well-positioned due to its robust defense technology sector, international partnerships, and geopolitical strategies. The country’s leading aerospace companies like Israel Aerospace Industries (IAI) and Elbit Systems contribute significantly to the market. Additionally, collaborations with global defense giants and the nation’s security imperatives drive the market’s dynamics, establishing Israel as a key player in both M&A and product innovation.

Market Segmentation

By Product Type:

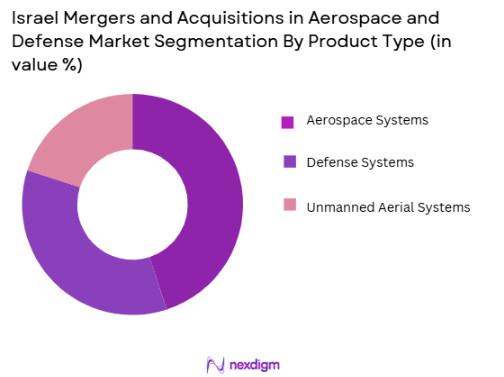

The Israel Mergers and Acquisitions in Aerospace and Defense market is segmented by product type into defense systems, aerospace systems, and unmanned aerial systems (UAS). The aerospace systems segment holds the dominant market share due to Israel’s extensive military and commercial aerospace capabilities. Israel’s aerospace industry is recognized for its high-end technology and expertise, contributing significantly to the development of advanced systems such as fighter jets, drones, and air defense systems. Additionally, continuous demand from both domestic and international defense markets further strengthens the dominance of aerospace systems in this market.

By Platform Type:

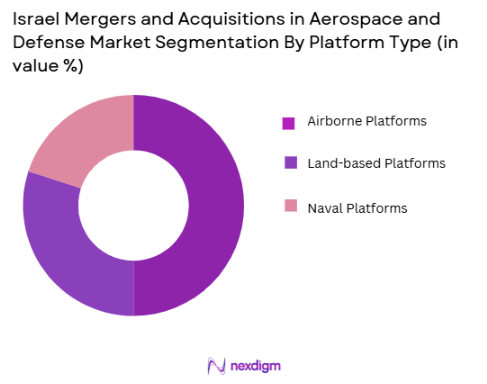

The market is also segmented by platform type into airborne platforms, land-based platforms, and naval platforms. The airborne platforms segment is expected to dominate the market, driven by Israel’s advanced aerial defense systems and unmanned aerial vehicles (UAVs). Israel’s strong focus on technological advancements in aerospace, such as the development of cutting-edge fighter jets, air defense systems, and drones, places airborne platforms at the forefront. The rising demand for military UAVs for surveillance and intelligence gathering also boosts the dominance of this segment in the market.

Competitive Landscape

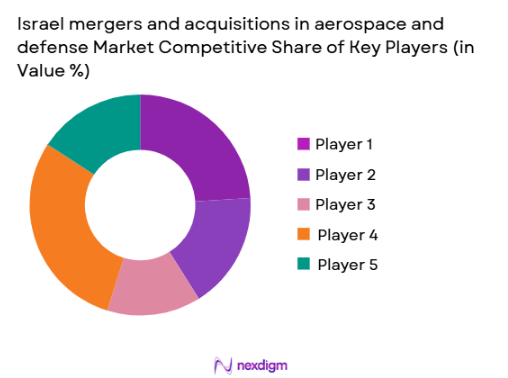

The Israel Mergers and Acquisitions in Aerospace and Defense market is highly competitive, with a few key players holding significant influence. Major companies such as Israel Aerospace Industries, Elbit Systems, and Rafael Advanced Defense Systems are leading the charge. These firms dominate the market due to their extensive experience in defense technologies, robust innovation pipelines, and significant market reach in both military and civilian aerospace applications. The market’s consolidation reflects the influence of these firms in shaping Israel’s aerospace and defense capabilities.

| Company | Establishment Year | Headquarters | Product Specialization | Revenue (USD) | M&A Activities | Global Reach |

| Israel Aerospace Industries (IAI) | 1953 | Tel Aviv, Israel | ~ | ~ | ~ | ~ |

| Elbit Systems | 1966 | Haifa, Israel | ~ | ~ | ~ | ~ |

| Rafael Advanced Defense Systems | 1948 | Haifa, Israel | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, USA | ~ | ~ | ~ | ~ |

| Boeing | 1916 | Chicago, USA | ~ | ~ | ~ | ~ |

Israel Mergers and Acquisitions in Aerospace and Defense Market Analysis

Growth Drivers

Urbanization

Urbanization plays a crucial role in the growth of the Israel Mergers and Acquisitions in Aerospace and Defense market. In 2024, Israel’s urban population is expected to exceed ~% of the total population, according to the World Bank. This shift towards urban living drives demand for advanced defense and aerospace technologies as urban centers require enhanced surveillance, air defense, and technological infrastructure. Cities like Tel Aviv and Jerusalem lead the charge in technological innovation, fostering defense-related M&A activities. The expansion of metropolitan areas increases the need for security, resulting in rising investments in cutting-edge defense systems.

Industrialization

Industrialization is a key driver behind the Israel Mergers and Acquisitions in Aerospace and Defense market. As of 2024, Israel’s industrial output is projected to grow at an annual rate of ~%, with significant investments directed towards aerospace and defense manufacturing. This growth is propelled by Israel’s focus on high-tech industries, particularly in aerospace systems, drones, and air defense technologies. The industrial sector is expanding rapidly, which in turn increases the demand for robust defense technologies and strategic mergers. Industrial growth in sectors like manufacturing and defense fosters M&A, as firms seek to scale operations and technologies.

Restraints

High Initial Costs

High initial costs remain a key restraint in the Israel Mergers and Acquisitions in Aerospace and Defense market. As of 2024, the Israeli government allocated USD 1.5 billion for the procurement of advanced defense systems. However, the costs associated with R&D, prototyping, and high-tech manufacturing continue to present challenges for many companies seeking to enter or expand within the market. The complex nature of aerospace systems, such as fighter jets, drones, and defense communications, requires substantial investment, often deterring smaller companies from engaging in M&A activities. The high cost of innovation and production limits the ability of certain players to fully capitalize on emerging opportunities.

Technical Challenges

The technical challenges associated with the development and integration of aerospace and defense systems act as a restraint in the Israel Mergers and Acquisitions market. As of 2024, Israel’s Ministry of Defense is addressing the significant technological gap in military and aerospace system interoperability, particularly with systems from different manufacturers. The technical complexity of integrating diverse platforms, including land-based, airborne, and naval systems, creates substantial hurdles. Additionally, concerns over the long-term sustainability of defense systems pose challenges for acquisitions, with companies facing difficulties in scaling their operations across multiple defense sectors.

Opportunities

Technological Advancements

Technological advancements present considerable opportunities for growth in the Israel Mergers and Acquisitions in Aerospace and Defense market. As of 2024, Israel’s military and aerospace sectors are heavily focused on advancing technologies like autonomous systems, AI-powered defense systems, and space exploration. The Israeli government is investing USD ~billion in research and development of autonomous unmanned systems, offering tremendous opportunities for both domestic and international companies to collaborate through mergers and acquisitions. These advancements create a ripe environment for innovative technologies, opening the door for strategic partnerships to enhance capabilities and expand product portfolios. [Source: Israel Ministry of Defense

International Collaborations

International collaborations offer a key opportunity for growth in the Israel Mergers and Acquisitions in Aerospace and Defense market. Israel is a prominent player in global defense, with strategic partnerships with countries such as the United States, India, and European nations. In 2024, Israel’s defense exports are forecasted to reach USD ~billion, driven by collaborations on advanced technologies, including radar systems, drones, and missile defense. These international partnerships not only strengthen Israel’s position in the global market but also foster a climate of innovation and shared resources, promoting M&A activities and industry consolidation.

Future Outlook

Over the next 5-10 years, the Israel Mergers and Acquisitions in Aerospace and Defense market is projected to experience steady growth, driven by technological innovations and the increasing need for defense modernization. M&A activity will continue to shape the market as both domestic and international companies seek to enhance their capabilities in unmanned systems, cybersecurity, and missile defense. The expansion of Israel’s defense budget and its position as a strategic ally in global defense collaborations will further fuel the market’s expansion, with increasing investments from both public and private sectors.

Major Players

- Israel Aerospace Industries

- Elbit Systems

- Rafael Advanced Defense Systems

- Lockheed Martin

- Boeing

- Northrop Grumman

- BAE Systems

- General Dynamics

- Leonardo

- Thales Group

- Saab

- Airbus

- Raytheon Technologies

- Dassault Aviation

- Kratos Defense & Security Solutions

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace manufacturers

- Defense contractors

- Commercial aerospace companies

- Military agencies and defense ministries

- International defense contractors

- Private equity firms

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying key market drivers and variables, such as technological advancements, regulatory changes, and geopolitical influences that impact M&A activities in the aerospace and defense market. Desk research from secondary sources such as reports, databases, and news articles will help establish an ecosystem map for key stakeholders.

Step 2: Market Analysis and Construction

Data from historical market reports and industry analysis will be aggregated to assess the performance of the Israel Mergers and Acquisitions in Aerospace and Defense market. The analysis will focus on past M&A activity, financial outcomes, and the competitive landscape to provide a reliable overview of the market’s past and current state.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with industry experts, including executives from defense and aerospace firms, will be conducted to validate the hypotheses developed from market research. These consultations will include structured interviews and surveys with stakeholders from leading defense contractors, aerospace manufacturers, and government agencies.

Step 4: Research Synthesis and Final Output

The final step will involve synthesizing the gathered data into actionable insights. The research findings will be verified through interviews with key industry figures, ensuring the data is accurate and reflects the true dynamics of the Israel Mergers and Acquisitions in Aerospace and Defense market. This phase will also include analyzing the implications of M&A on future market trends and company strategies.

- Executive Summary

- Research Methodology([Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Strategic investments in defense technologies

Rising demand for military and aerospace systems

Technological innovations in aerospace manufacturing - Market Challenges

Regulatory complexities and compliance requirements

High cost of R&D and system integration

Geopolitical risks affecting cross-border mergers - Trends

Increased adoption of artificial intelligence in defense systems

Rise of cybersecurity-focused mergers in aerospace

Shift towards sustainable aerospace technology solutions

- Market Opportunities

Expanding defense budgets in the Middle East

Growth in unmanned systems and autonomous technologies

Collaborations with international aerospace and defense leaders - Government regulations

Tightened export controls on aerospace and defense technologies

Evolving certification standards for unmanned aerial systems

Increased scrutiny on foreign investments in defense sectors - SWOT analysis

Strength: Israel’s strong aerospace and defense technological base

Weakness: High reliance on international partnerships

Opportunity: Expansion of aerospace capabilities through strategic M&As

Threat: Volatility in the geopolitical landscape affecting market stability - Porters 5 forces

Threat of new entrants: Moderate due to high capital requirements

Bargaining power of suppliers: High due to specialized components

Bargaining power of buyers: Moderate due to limited alternatives

Threat of substitute products: Low for advanced aerospace systems

Industry rivalry: High due to competitive defense and aerospace markets

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Commercial Aerospace Systems

Military Aerospace Systems

Unmanned Aerial Systems (UAS)

Air Defense Systems

Aerospace Communications Systems - By Platform Type (In Value%)

Airborne Platforms

Land-based Platforms

Naval Platforms

Space Platforms

Hybrid Platforms - By Fitment Type (In Value%)

Original Equipment Manufacturer (OEM)

Aftermarket

Upgrade & Retrofit

Component & Subsystem Supply

Full-Scale System Supply - By EndUser Segment (In Value%)

Government and Military Agencies

Commercial Airlines

Aerospace Manufacturers

Defense Contractors

Space Agencies - By Procurement Channel (In Value%)

Direct Procurement

Through Contractors

Government Tendering

Private Sector Partnerships

Collaborations with Foreign Partners

- Market Share Analysis

- CrossComparison Parameters(Technology adoption rate, M&A activity, geographical expansion, innovation in defense, product portfolio diversification)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Israel Aerospace Industries

Elbit Systems

Rafael Advanced Defense Systems

IAI Aviation Group

Aeronautics Ltd.

Bluebird Aero Systems

Aviation Industry Corporation of China

Lockheed Martin

Northrop Grumman

Boeing

General Dynamics

Thales Group

Leonardo

Dassault Aviation

BAE Systems

- Government agencies driving the demand for military and defense acquisitions

- Aerospace manufacturers looking for enhanced

- technology capabilitiesCommercial airline partnerships focused on long-term equipment upgrades

- Defense contractors expanding through strategic acquisitions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now