Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Israel Military Aircraft market is valued at approximately USD ~, driven by ongoing defense modernization and significant investments in military technologies. With the Israeli Air Force’s focus on acquiring advanced fighter aircraft, drones, and specialized air platforms, the market experiences consistent growth. The expansion of Israel’s defense exports to countries such as India, Germany, and the United States further strengthens market dynamics. Additionally, the rising need for surveillance, intelligence, and combat capabilities supports the market’s trajectory. The demand for high-tech components, such as avionics, radar systems, and advanced mission systems, contributes substantially to the market’s value.

The market is primarily dominated by Israel, owing to its highly sophisticated defense capabilities and long-standing leadership in military aviation. Major players like Israel Aerospace Industries and Elbit Systems play a crucial role in both domestic and global aircraft production. Israel’s strategic alliances with countries such as the United States and its role as a defense exporter also contribute to its dominance. Furthermore, Tel Aviv and Herzliya are key hubs for the aerospace industry, housing major defense contractors and military research facilities, solidifying their importance in the global market.

Market Segmentation

By Aircraft Type

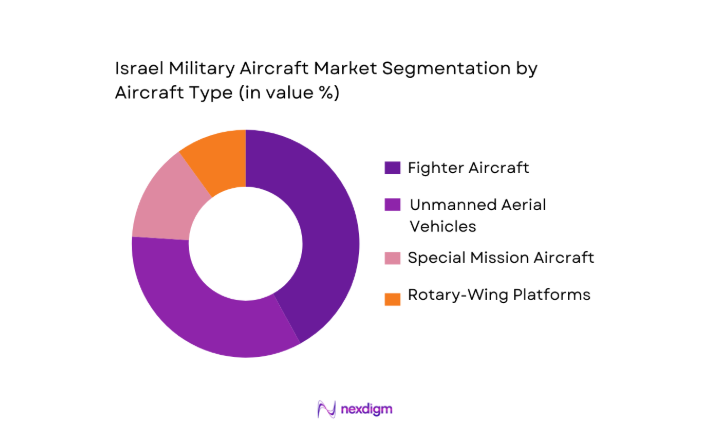

The Israel Military Aircraft market is segmented by aircraft type, including fighter aircraft, unmanned aerial vehicles, special mission aircraft, and rotary-wing platforms. Fighter Aircraft: This segment is dominated by advanced multi-role fighter jets such as the F-35I Adir, F-15IA, and indigenous designs like the Kfir C7. The superior air combat capabilities, stealth technology, and interoperability with allied air forces make fighter aircraft the dominant segment in Israel’s military aviation market. The continued modernization efforts and procurement programs significantly support this sector, with Israel’s military constantly enhancing its fleet to maintain air superiority.

By Technology Type

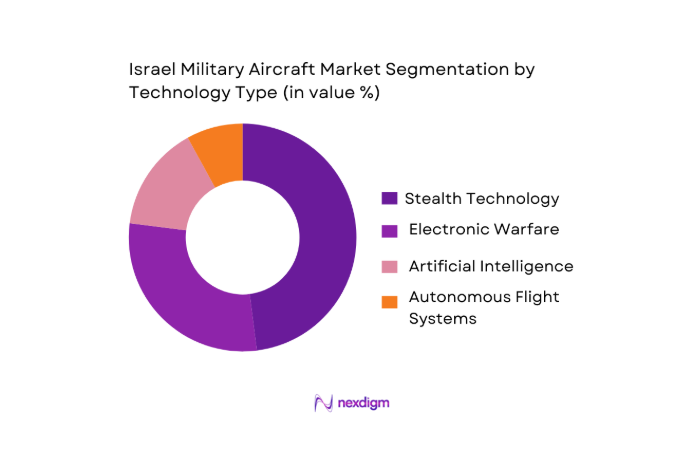

This segmentation covers advanced technologies used in military aircraft, including stealth, electronic warfare, artificial intelligence (AI), and autonomous flight systems.

Stealth Technology: Stealth aircraft, especially the F-35I Adir, dominate this segment. The need for low observability in combat and intelligence missions has accelerated the adoption of stealth technology. Israel’s integration of advanced radar-evading materials, advanced avionics, and low radar signatures has placed this technology at the forefront of military aircraft procurement.

Competitive Landscape

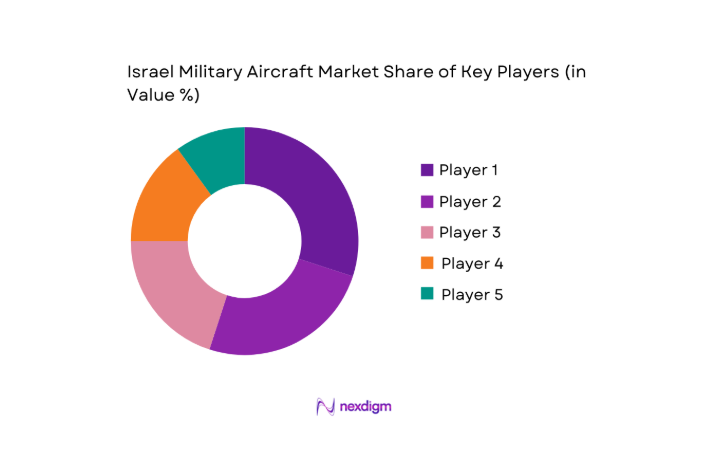

The Israel Military Aircraft market is dominated by both local and international defense players. Israel’s domestic aerospace sector, including companies like Israel Aerospace Industries (IAI), Elbit Systems, and Rafael Advanced Defense Systems, is supported by strategic collaborations with global defense giants such as Lockheed Martin, Boeing, and Northrop Grumman. These companies contribute to the production of fighter jets, UAVs, avionics, and mission systems.

| Company Name | Establishment Year | Headquarters | Market Focus | Technologies | Export Reach | Key Product |

| Israel Aerospace Industries | 1953 | Tel Aviv, Israel | ~ | ~ | ~ | ~ |

| Elbit Systems | 1966 | Haifa, Israel | ~ | ~ | ~ | ~ |

| Rafael Advanced Defense Systems | 1980 | Haifa, Israel | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, USA | ~ | ~ | ~ | ~ |

| Boeing Defense | 1916 | Chicago, USA | ~ | ~ | ~ | ~ |

Israel Military Aircraft Market Analysis

Growth Drivers

Export Demand Surge

Israel’s defense export ecosystem, which encompasses military aircraft components, UAVs, avionics, and support systems, experienced a record export performance in 2024, reaching over USD ~contracts, an increase from USD ~ in the prior year, and representing the fourth consecutive annual record according to the Israel Ministry of Defense. Over 54 percent of these export deals (by value) were with European countries, while another 23 percent went to the Asia‑Pacific region, and 9 percent to North America, reflecting strong global acceptance of Israeli military aviation technologies and air defense systems. This substantial export trajectory demonstrates how international demand, especially in regions seeking battle‑proven technologies, is a primary driver of market growth. European defense budgets have concurrently risen, influencing increased procurement of advanced aerospace equipment, including radar and mission systems that integrate with aircraft platforms.

Modernization Spend

Israel’s national military investment surged in 2024, with total expenditure reaching approximately USD ~, marking the largest year‑on‑year increase since 1967 according to SIPRI data. This sharp rise in military spending, which accounted for roughly ~ percent of GDP, underpins the domestic procurement of next‑generation military aircraft, advanced avionics suites, and support systems used across air force modernization programs. Such significant allocation of fiscal resources enables the sustained acquisition and upgrade of fighter fleets, ISR platforms, and integration of defense electronics. Concurrently, Israel’s GDP was reported at USD ~, with a GDP per capita of USD ~, illustrating macroeconomic stability that supports defense budget commitments without proportionate strain on overall economic output. The expanding modernization budget also helps fund indigenous R&D, bridging strategic capability gaps and supporting long‑term defense industrial base resilience.

Market Challenges

Export Restrictions

Despite the record defense export figures Israel achieved in 2024, export restrictions imposed by some governments pose significant challenges. For example, Germany drastically reduced export permits for defense equipment to Israel after the onset of conflict, with export approvals for military goods dropping from €~ in 2023 to only around €~ for weaponry, and €~ for other military goods in 2024. Such policy shifts restrict Israeli suppliers from accessing traditional export markets and complicate procurement cycles for military aircraft systems and related components. Other countries, including the U.K., suspended portions of defense export licences, further introducing regulatory unpredictability into arms trade channels. These fluctuations in export permissions can disrupt production planning, strain relations with global partners, and impose compliance overhead that can delay or cancel contracts critical to sustaining production lines and employment within Israel’s aerospace supply chain. Managing these export licensing dynamics becomes a strategic imperative for Israeli defense firms engaged in global aircraft market engagements.

Supply Chain Limits

Israel’s defense and military aircraft supply base competes on global platforms while operating within a relatively small domestic manufacturing footprint that accounts for roughly 11.13 percent of GDP as value added in manufacturing. This structural characteristic implies that critical components, such as specialized avionics parts, high‑precision composites, and electronic warfare modules, often require import of raw materials or subassemblies. Given global supply chain volatility — influenced by geopolitical tensions, logistics costs, and semiconductor shortages — defense manufacturers face risk of production delays and cost pressure. Israel’s export‑oriented aviation components are sensitive to disruptions in semiconductor and advanced materials supply chains, which indirectly constrains delivery schedules for complex aircraft systems and upgrades. Continuity of supply, particularly for high‑tech sensor and mission systems integral to military aircraft, requires stable partnerships with global suppliers and diversification strategies to mitigate localized chokepoints. Maintaining resilience in this ecosystem is essential to support both domestic air force modernization and fulfillment of export contracts worldwide.

Market Opportunities

UAS Expansion

Unmanned Aerial Systems represent a significant opportunity for the Israel military aircraft market, supported by Israel’s strong defense export performance of almost USD ~ in 2024 that included UAVs and related systems as part of broader defense deliveries. Although drones accounted for a smaller proportion of export value compared to other segments in 2024, Israel’s established leadership in UAS technologies — including intelligence, ISR, and autonomous platforms — positions it to capitalize on rising global demand for unmanned solutions. Many defense purchasers increasingly prioritize unmanned systems for cost‑effective surveillance, strike, and reconnaissance missions, especially in contested environments. The integration of UAS capabilities with broader air operation concepts enhances force scalability and reduces risk to personnel, stimulating procurement interest worldwide. Israel’s technology base, education system, and innovation ecosystem support advances in autonomy and mission systems for UAS, extending commercial and military application potential beyond traditional manned aircraft roles. Continued focus on UAS development can expand market participation, reinforce export networks, and build long‑term demand for interoperable unmanned systems.

Advanced Sensors

Advanced sensor technologies, including airborne radar, electronic surveillance, and integrated EW suites, contribute significantly to the competitive edge of Israeli military aviation systems. For example, ELTA Systems Ltd reported sales of USD ~ in 2024, with approximately ~ of revenue derived from export orders and an order backlog of USD ~. These figures highlight the strong international demand for state‑of‑the‑art sensor platforms integrated into military aircraft and ISR platforms. Advanced sensors enhance situational awareness, threat detection, and mission reliability for air operations, driving procurement decisions across armed forces seeking better survivability and operational effectiveness. The robust order backlog reflects confidence among global buyers in Israeli sensor technologies and their applicability in modern conflict environments. As demand for battlefield intelligence, precision targeting, and real‑time data fusion increases, advanced sensors embedded within aircraft ecosystems represent a durable growth vector for the Israeli defense aviation market.

Future Outlook

The Israel Military Aircraft market is expected to experience significant growth over the next decade. Continued defense modernization, the need for advanced aerial capabilities, and the increasing demand for unmanned systems will drive the market forward. Furthermore, international collaborations and an expanding export market, particularly with allied nations, will ensure sustained demand for advanced aircraft. Technological advancements in stealth capabilities, avionics, and artificial intelligence will further accelerate the adoption of cutting-edge systems.

Major Players

- Israel Aerospace Industries

- Elbit Systems

- Rafael Advanced Defense Systems

- Lockheed Martin

- Boeing Defense

- Northrop Grumman

- Saab AB

- Airbus Defence and Space

- Thales Group

- Leonardo S.p.A

- General Atomics

- Textron Aviation

- BAE Systems

- Honeywell Aerospace

- Pratt & Whitney

Key Target Audience

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- National Air Forces

- Global Defense Contractors

- Aerospace and Defense Manufacturers

- Aerospace Component Suppliers

- Aerospace Technology Developers

Research Methodology

Step 1: Identification of Key Variables

The first step in this research involves creating an ecosystem map that identifies all stakeholders in the Israel Military Aircraft market, including military agencies, defense contractors, and component suppliers. This is achieved by combining secondary research data with proprietary databases, ensuring that all critical variables such as technology adoption, procurement cycles, and export regulations are accurately identified.

Step 2: Market Analysis and Construction

This phase involves analyzing historical data on aircraft production, technological advancements, and defense budgets. An evaluation of the key players’ market share and their product portfolios will also be conducted to accurately determine the current and projected growth of the market.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be validated by conducting telephone interviews with industry experts, including representatives from defense ministries, military agencies, and key contractors. These consultations will allow for validation of market dynamics and refinement of the forecast models.

Step 4: Research Synthesis and Final Output

The final phase integrates feedback from key industry experts and stakeholders to ensure the accuracy of the market data. Interaction with defense contractors and agencies will also provide insights into procurement processes and market trends, validating the findings from a bottom-up approach.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach, Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition and Scope

- Market Dynamics

- Historical Market Performance and Evolution

- Strategic Timeline

- Growth Drivers

Export Demand Surge

Modernization Spend

Tech Leadership - Market Challenges

Export Restrictions

Supply Chain Limits

Competitor Entry - Market Opportunities

UAS Expansion

Advanced Sensors

Aftermarket MRO - Market Trends

AI/ML Integration

Autonomous Systems - Government Regulations and Export Control Regimes

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020‑2025

- By Unit Shipment Volume, 2020‑2025

- By Average System Pricing, 2020‑2025

- By Platform Type (In Value %)

Fighter/Combat Aircraft

Unmanned Systems

Special Mission Aircraft - By Technology Capability (In Value %)

Stealth & Low Observable

Sensor & EW Integration

Autonomous / AI‑Enabled Systems - By End‑Use Application (In Value %)

Air Superiority & Strike

ISR & Electronic Warfare

Border / Maritime Surveillance - By Deployment Type (In Value %)

Domestic Forces

Export Markets - By Procurement Channel (In Value %)

Government Contracts

Foreign Military Sales/ Direct Export

- Market Share of Major Players

- Cross Comparison Parameters (Platform Capability Index, Sensor & EW Performance Score, Export Reach & Partner Footprint, Lifecycle Cost Efficiency, Production & Delivery Lead Time, Technology Readiness Level)

- SWOT Analysis of Key Players

- Pricing Analysis

- Major Players: Detailed Profiles

Israel Aerospace Industries

Elbit Systems Ltd

Rafael Advanced Defense Systems

Lockheed Martin

Boeing Defense

Northrop Grumman

Airbus Defence & Space

Saab AB

Leonardo S.p.A

Thales Group

General Atomics

Textron Aviation

BAE Systems

Honeywell Aerospace

Pratt & Whitney

- Strategic Procurement Criteria

- End User Operational Drivers

- Defense Budget Allocation Patterns

- Impact of Geopolitical Pressures on Buyer Behavior

- By Market Value, 2026‑2035

- By Unit Shipment Volume, 2026‑2035

- By Average System Pricing, 2026‑2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now