Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Israel military sensors market is projected to reach a value of USD ~billion by the end of the year. This growth is driven primarily by the rising demand for advanced defense systems, including the deployment of ISR platforms, as well as cutting-edge sensor technologies like radar, infrared, and optical sensors. Furthermore, an increasing focus on national defense strategies and the push toward automation in military operations are fuelling the demand for high-performance sensors in Israel’s military sector. This has led to the development of more sophisticated sensor platforms for air, land, and naval operations, contributing to a robust market expansion.

The market is notably dominated by Israel, a country renowned for its cutting-edge defense capabilities and extensive military investments. Israel’s dominance in the sector is attributed to its advanced defense technology industry, particularly in military drones and unmanned systems, which leverage high-performance sensors for intelligence gathering and surveillance. The country also benefits from strong military collaborations with the United States and other allied nations, further boosting the demand for its sensor technologies. Additionally, the strategic importance of Israel in the Middle East, combined with its geopolitical challenges, drives significant investments in state-of-the-art military technologies, solidifying its market leadership.

Market Segmentation

By Product Type

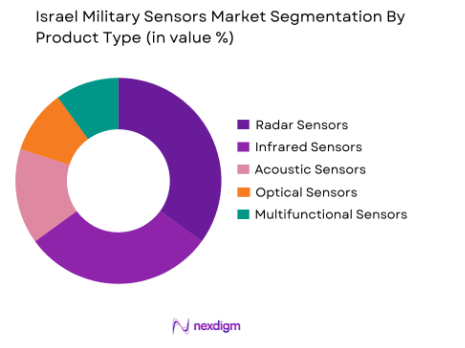

The Israel military sensors market is segmented by product type into radar sensors, infrared sensors, acoustic sensors, optical sensors, and multifunctional sensors. Recently, radar sensors have a dominant market share due to factors such as their ability to provide long-range detection capabilities and their increasing use in military surveillance and navigation systems. The growing need for enhanced border protection and surveillance, as well as advancements in radar technologies, have made these sensors integral to various defense operations. Additionally, radar sensors offer high adaptability to various environments, from land-based to airborne platforms, further cementing their dominance in the market.

By Platform Type

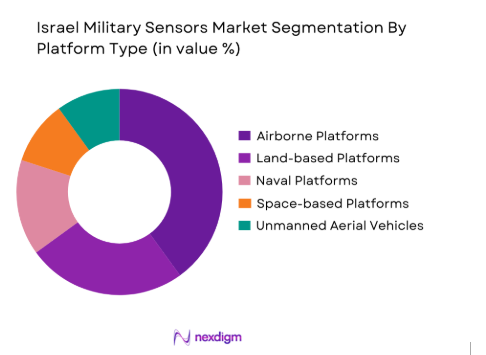

The market is also segmented by platform type into land-based platforms, airborne platforms, naval platforms, space-based platforms, and unmanned aerial vehicles (UAVs). Airborne platforms have the largest share, driven by the increased demand for aerial surveillance systems and advanced sensors for aircraft, drones, and helicopters. These platforms are crucial for intelligence gathering, reconnaissance, and security operations in defense. As UAVs become more widely used in military strategies, particularly for surveillance and tactical missions, the integration of airborne sensors continues to expand, maintaining their position as the leading platform type in the market.

Competitive Landscape

The Israel military sensors market is highly competitive, with several major players leading the charge in developing advanced sensor technologies. The market has witnessed a trend of consolidation, as larger defense firms acquire smaller, specialized sensor manufacturers to strengthen their portfolios and expand their technological capabilities. Major players also compete on the basis of innovation, price, and the ability to integrate sensors into various defense platforms. The presence of government contracts and international partnerships further intensifies the competitive dynamics, as companies work to secure long-term contracts with military agencies and allied nations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Market-Specific Parameter |

| Elbit Systems | 1966 | Haifa, Israel | Defense Electronics | ~ | ~ | ~ | ~ |

| Rafael Advanced Defense Systems | 1958 | Haifa, Israel | Integrated Defense Systems | ~ | ~ | ~ | ~ |

| Israel Aerospace Industries | 1953 | Lod, Israel | Aerospace & Defense | ~ | ~ | ~ | ~ |

| IAI (Israel Aerospace Industries) | 1953 | Lod, Israel | Aerospace and Defense | ~ | ~ | ~ | ~ |

| Magal Security Systems | 1969 | Yehud, Israel | Security Solutions | ~ | ~ | ~ | ~ |

Israel Military Sensors Market Analysis

Growth Drivers

Increase in Defense Budgets

The rising military expenditures globally, particularly in the Middle East, have fuelled the growth of the Israel military sensors market. Israel has significantly increased its defense spending to maintain a technological edge in the region, with a focus on advanced sensors for its military forces. This boost in defense budgets supports the adoption of state-of-the-art radar, infrared, and optical sensor technologies. Furthermore, the growing need for real-time surveillance and intelligence gathering for national security purposes, including border protection and counter-terrorism, has driven the demand for military-grade sensors. As Israel’s security concerns remain high due to geopolitical tensions, the Israeli defense sector continues to invest heavily in advanced military sensor systems, ensuring sustained market growth. The Israeli government’s initiatives to support local innovation and strengthen defense capabilities contribute to further expanding sensor demand across various defense platforms. Moreover, the global export of Israel’s defense technology, including military sensors, adds another layer of growth to the market, positioning the country as a dominant player in the defense technology sector. The integration of these systems into unmanned aerial vehicles (UAVs) and other autonomous systems also plays a key role in the growing demand for military sensors.

Technological Advancements in Sensor Systems

The continuous development of cutting-edge sensor technologies is a key driver for the market. Innovations in radar, infrared, and optical sensors have allowed for more accurate, long-range, and reliable military systems, which are crucial for modern warfare strategies. These technologies are particularly vital for ISR applications, where real-time data acquisition is essential for mission success. Israel’s extensive research and development (R&D) in sensor systems, along with its collaborations with global defense partners, have resulted in the production of highly specialized sensors capable of operating in various extreme conditions. Additionally, the miniaturization of sensor systems has enabled the integration of these technologies into smaller platforms, such as drones and other unmanned systems, broadening their usage in military operations. The increased demand for multi-functional, autonomous platforms further drives the need for sophisticated sensor systems that can provide comprehensive situational awareness across different domains of defense operations.

Market Challenges

Regulatory Constraints and Export Restrictions

A significant challenge for the Israel military sensors market is the stringent regulatory environment and export restrictions. Military sensor technologies often face export controls under international regulations such as the International Traffic in Arms Regulations (ITAR) and the Export Administration Regulations (EAR). These regulations limit the ability of Israeli companies to freely market and sell their sensors in certain regions, especially to countries with sensitive geopolitical concerns. As Israel’s defense technology is in high demand across the globe, these constraints pose a challenge for companies seeking to expand their market reach. Furthermore, the approval process for exporting defense technologies can be time-consuming and complex, delaying the deployment of sensor systems to international clients. This restriction not only limits the revenue potential for Israeli sensor manufacturers but also forces them to navigate a complicated landscape of legal and diplomatic challenges in the global defense market. The impact of these export regulations also extends to the development of new products, as manufacturers must ensure compliance with various regulatory frameworks, which can slow down innovation and market adoption.

High Development Costs

The development of advanced military sensors requires significant investment in research, development, and production facilities, which can result in high operational costs for manufacturers. The need for specialized materials, precision engineering, and high-level expertise further adds to the cost structure. For smaller manufacturers or emerging companies, the financial barrier to entering the market can be a significant hurdle. Even for established players, balancing the cost of innovation with competitive pricing remains a challenge. Additionally, the complexity of sensor systems, including integration with other defense platforms, increases the overall development costs. While the defense sector often justifies these costs due to the critical nature of military applications, the ongoing need for cost-efficient solutions remains a key challenge for companies. The rising costs of raw materials and supply chain disruptions also impact the cost structure of military sensors, making it difficult to maintain profitability while continuing to innovate and meet customer expectations. As defense budgets fluctuate, manufacturers must be able to adapt to these challenges and provide solutions that offer both high performance and affordability.

Opportunities

Advancements in Sensor Miniaturization

One of the most significant opportunities for the Israel military sensors market lies in the miniaturization of sensor systems. As demand grows for smaller, lighter, and more flexible military platforms, including unmanned aerial vehicles (UAVs), sensor manufacturers are presented with the opportunity to develop compact sensors that offer the same level of performance as larger counterparts. These smaller sensors can be integrated into various platforms, enabling advanced surveillance, reconnaissance, and intelligence gathering missions. Miniaturization also opens up new opportunities for military systems to operate in environments previously deemed unsuitable for larger, more traditional sensors. This trend is particularly important in the context of unmanned systems, where payload weight is a critical factor. The ability to integrate multiple sensors into smaller platforms will drive demand for these technologies, further expanding the market for military sensors in Israel. Additionally, as technology continues to evolve, these miniaturized sensors are expected to offer greater precision and functionality, making them highly valuable for modern defense operations.

Emerging Markets for Unmanned Systems

Another opportunity lies in the increasing global demand for unmanned systems, including drones and autonomous vehicles, which rely heavily on advanced sensors. The integration of military sensors into these systems enables real-time data collection and decision-making capabilities, providing a significant advantage in modern warfare. The growing adoption of unmanned aerial vehicles (UAVs) for surveillance, reconnaissance, and combat missions presents a unique opportunity for sensor manufacturers to expand their product offerings. Moreover, as emerging markets invest in defense technologies and modernize their military capabilities, there is a growing demand for advanced sensor systems to equip unmanned platforms. Israel, with its advanced sensor technology and strong defense industry, is well-positioned to capitalize on this trend. As global defense strategies shift toward autonomous and unmanned systems, the demand for military sensors integrated into these platforms will continue to grow, offering substantial opportunities for innovation and market expansion.

Future Outlook

Over the next five years, the Israel military sensors market is expected to experience steady growth driven by advancements in sensor technologies, increasing defense budgets, and rising global demand for unmanned systems. The integration of advanced sensors into platforms such as UAVs, autonomous vehicles, and military aircraft will remain a key growth driver. Additionally, regulatory support from both the Israeli government and international defense organizations will facilitate market expansion. The continued focus on ISR capabilities and autonomous systems will further enhance the market’s potential, leading to innovations that cater to the evolving needs of modern warfare.

Major Players

- Elbit Systems

- Rafael Advanced Defense Systems

- Israel Aerospace Industries

- IAI (Israel Aerospace Industries)

- Magal Security Systems

- Aeronautics Defense Systems

- Opgal Optronic Industries

- Bluebird Aero Systems

- Carmanah Technologies

- Silentium Defense

- Camero Tech

- Mantis Tech

- Tactical Air Support

- UVision Air

- AeroVironment

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Military contractors

- Defense technology manufacturers

- Aerospace & defense agencies

- Border and perimeter security authorities

- International defense alliances

- Strategic defense initiatives

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying key factors such as technological advancements, market trends, and regulatory environments that influence the market.

Step 2: Market Analysis and Construction

Market analysis is conducted through a combination of primary and secondary research, utilizing data from industry reports, interviews, and surveys to build a comprehensive view.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses formed during the market analysis are validated through consultations with industry experts and key stakeholders to ensure accuracy and relevance.

Step 4: Research Synthesis and Final Output

The final output synthesizes all research findings and expert insights to create a detailed report, providing market forecasts, segmentation, and strategic recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in defense budgets in Israel and neighboring regions

Development of advanced sensor technologies for enhanced detection

Expansion of Israel’s military collaborations with global powers - Market Challenges

Regulatory constraints and export restrictions on sensor technology

High development costs of cutting-edge sensors

Cybersecurity concerns with interconnected sensor systems - Market Opportunities

Growing demand for ISR (Intelligence, Surveillance, Reconnaissance) capabilities

Advancements in sensor miniaturization for UAVs and autonomous systems

Expansion of sensor integration in military drones and unmanned systems - Trends

Shift towards hybrid and multifunctional sensor platforms

Adoption of AI and machine learning for sensor data analysis

Increased focus on non-traditional sensor types for advanced warfare

- By Market Value 2020-2025

- By Installed Units 2020-2025

- By Average System Price 2020-2025

- By System Complexity Tier 2020-2025

- By System Type (In Value%)

Radar Sensors

Infrared Sensors

Acoustic Sensors

Optical Sensors

Multifunctional Sensors - By Platform Type (In Value%)

Land-based Platforms

Airborne Platforms

Naval Platforms

Space-based Platforms

Unmanned Aerial Vehicles (UAVs) - By Fitment Type (In Value%)

Standalone Systems

Integrated Systems

Modular Fitments

Built-in Systems

Upgradable Systems - By EndUser Segment (In Value%)

Defense Contractors

Military Forces

Government Agencies

Private Sector Security Firms

International Defense Alliances - By Procurement Channel (In Value%)

Direct Purchases

Government Tenders

Private Sector Purchases

Through Intermediaries

International Collaborations

- Market Share Analysis

- Cross Comparison Parameters (Market share, technology adoption rate, pricing strategy, geographic reach, product offerings)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Elbit Systems

IAI (Israel Aerospace Industries)

Rafael Advanced Defense Systems

El-Op Electro-Optics Industries

AeroVironment

Tactical Air Support

Magal Security Systems

Opgal Optronic Industries

Bluebird Aero Systems

Carmanah Technologies

Silentium Defense

Camero Tech

UVision Air

Aeronautics Defense Systems

Mantis Tech

- Increasing defense budgets of Israeli military forces

- Growing demand for ISR and security applications in neighboring regions

- Rise of private sector players investing in defense technology

- Expansion of cross-border defense collaborations

- Forecast Market Value 2026-2035

- Forecast Installed Units 2026-2035

- Price Forecast by System Tier 2026-2035

- Future Demand by Platform 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now