Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Israel remote sensing satellites market is driven by advancements in satellite technology, government investments, and an increasing demand for real-time data. Based on a recent historical assessment, the market size for remote sensing satellites is substantial, with a projected value of USD ~ billion in 2024. The growth of this market is underpinned by applications across defense, agriculture, and environmental monitoring sectors. Significant contributions from government initiatives, such as the Israel Space Agency’s investment in satellite infrastructure, fuel further expansion and development. These systems are deployed to address the need for high-resolution imaging, geospatial intelligence, and satellite-based data processing.

Israel is recognized as a key player in the remote sensing satellite market due to its advanced space technology and significant government support. Leading cities, such as Tel Aviv and Herzliya, are at the forefront of innovation in satellite systems, with Israel Aerospace Industries playing a critical role in satellite development and manufacturing. The country has gained international recognition for its expertise in defense applications, contributing to its dominance in the market. Additionally, Israel’s strategic location and partnerships with international organizations strengthen its position as a leader in remote sensing technology.

Market Segmentation

By System Type

The Israel remote sensing satellites market is segmented by product type into optical imaging, synthetic aperture radar (SAR), multispectral imaging, hyperspectral imaging, and thermal imaging systems. Among these, optical imaging systems dominate the market share due to their widespread adoption in earth observation, environmental monitoring, and defense sectors. These systems are preferred for their ability to capture high-resolution images, making them suitable for applications like land use monitoring, disaster management, and agricultural analysis. Their versatility in providing both visible and near-infrared data has also made them a popular choice across various industries, resulting in their dominant position within the market.

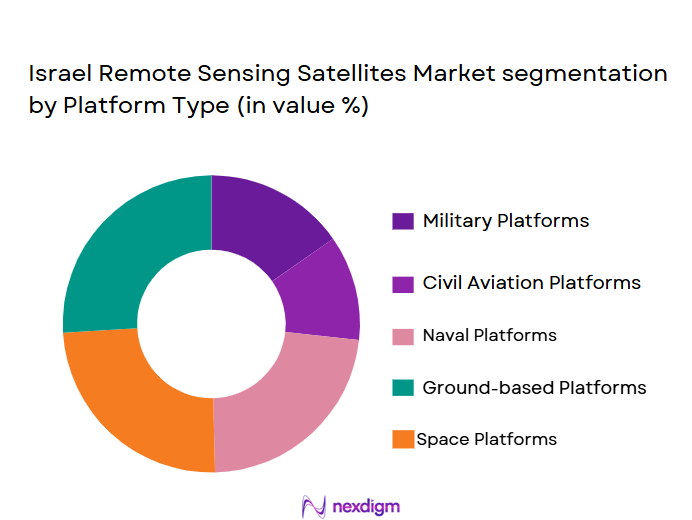

By Platform Type

The market for remote sensing satellites in Israel is segmented by platform type into Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Orbit (GEO), CubeSats, and High Altitude Pseudo Satellites (HAPS). The LEO satellites segment holds the dominant market share, owing to their ability to provide high-resolution imagery with shorter revisit times. LEO satellites are essential for applications requiring frequent data updates, such as weather forecasting, disaster management, and agricultural monitoring. Their cost-effectiveness, along with their low latency and smaller size, makes them the preferred choice for Israel’s space agencies and defense contractors, securing their lead in the market.

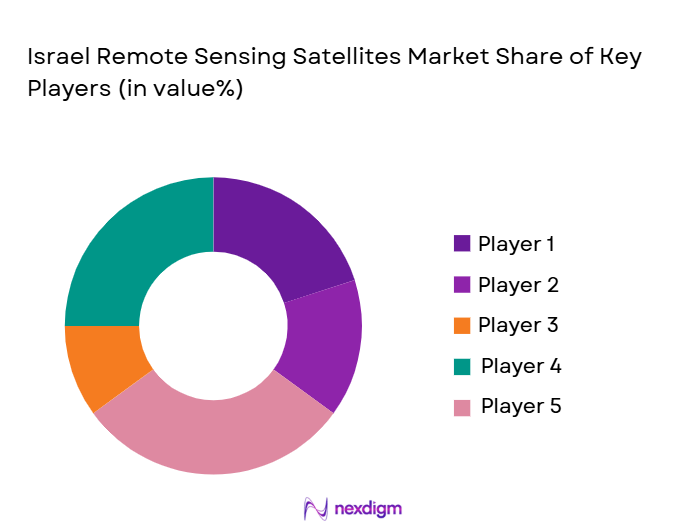

Competitive Landscape

The competitive landscape of the Israel remote sensing satellite market is characterized by significant consolidation, with key players such as Israel Aerospace Industries and Elbit Systems leading the market. These companies benefit from strategic partnerships, government contracts, and a robust technological infrastructure. Their continued dominance is supported by their ability to deliver advanced satellite solutions for both military and civilian applications. The market also sees the rise of startups focusing on cost-effective solutions, though the market remains primarily driven by established defense and aerospace companies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Market-Specific Parameter |

| Israel Aerospace Industries | 1953 | Tel Aviv | ~ | ~ | ~ | ~ | ~ |

| Elbit Systems | 1966 | Haifa | ~ | ~ | ~ | ~ | ~ |

| Rafael Advanced Defense Systems | 1948 | Haifa | ~ | ~ | ~ | ~ | ~ |

| MDA (MacDonald, Dettwiler and Associates) | 1969 | Haifa | ~ | ~ | ~ | ~ | ~ |

| SkyFi | 2015 | Tel Aviv | ~ | ~ | ~ | ~ | ~ |

Israel remote sensing satellite Market Analysis

Growth Drivers

Government Investment in Space Infrastructure

Government investment in space infrastructure is a significant driver for the Israel remote sensing satellites market. The Israel Space Agency has made substantial investments in satellite technologies and infrastructure, aiming to expand the country’s capabilities in satellite manufacturing, data collection, and analysis. The government’s involvement in space initiatives is not only focused on military applications but also on civilian sectors, including agriculture and environmental monitoring. Additionally, the Israeli government is fostering partnerships with private companies to develop cost-effective satellite solutions that address various industries’ needs. These investments have contributed to an increase in the country’s satellite launch capabilities and the overall demand for remote sensing technologies. As the government continues to allocate funds to research and development in space technologies, Israel’s leadership in the global satellite market is expected to solidify further. Moreover, government policies that support private sector innovation in space tech will likely result in advancements in satellite technology, boosting the market’s growth. With the government’s active participation and an established regulatory framework, Israel is poised to expand its presence in the global remote sensing satellite market.

Technological Advancements in Satellite Systems

Technological advancements in satellite systems are fueling the growth of the Israel remote sensing satellites market. Over the years, Israel has made significant strides in developing state-of-the-art satellite technology. These advancements, including improved imaging systems, miniaturization of satellite components, and enhanced data processing capabilities, are making satellite systems more efficient and cost-effective. Innovations in AI and machine learning are also improving satellite data analysis, enabling better insights for industries such as agriculture, defense, and urban planning. The development of high-resolution imaging systems and better power management for satellites has made them more reliable and capable of providing real-time data for various applications. The adoption of smaller, lighter satellites, including CubeSats, is allowing for quicker and more frequent launches, further driving the demand for remote sensing solutions. With continuous innovation, the Israeli satellite industry is well-positioned to maintain a competitive edge in the market, fostering further market expansion. These advancements in satellite technology are expected to contribute significantly to market growth, enabling the adoption of remote sensing solutions across multiple sectors.

Market Challenges

High Costs of Satellite Development and Launch

One of the significant challenges in the Israel remote sensing satellites market is the high costs associated with satellite development and launch. Developing advanced satellite systems involves substantial capital investment in research, manufacturing, testing, and launching. The costs of building high-resolution imaging systems and ensuring their durability in space contribute to the overall expenses, making it a barrier for smaller companies and startups. Additionally, the cost of launching satellites, including the need for specialized infrastructure, can make it difficult for players in the market to maintain cost-effective operations. Although the government has been actively investing in space infrastructure, the expense of satellite launches remains a significant challenge for the market. This high cost factor can limit the frequency of launches and the expansion of satellite constellations, potentially hindering market growth. Furthermore, the financial burden of satellite maintenance and the need for skilled personnel in satellite technology adds to the operational expenses of market players, making it challenging for them to stay competitive.

Regulatory Hurdles and Licensing Issues

Regulatory hurdles and licensing issues present a major challenge to the growth of the Israel remote sensing satellites market. Strict regulatory frameworks governing satellite launches, data collection, and space exploration create barriers for companies seeking to enter the market or expand their operations. The need for proper licensing and compliance with both domestic and international regulations can delay satellite launches and increase operational costs. Israel’s regulatory landscape for remote sensing satellites involves obtaining approvals for satellite deployments, ensuring compliance with international space treaties, and securing the necessary clearances for satellite data use. These regulations often require significant time and resources to navigate, adding complexity to the satellite market. As more countries and companies engage in space-based technologies, regulatory complexities are expected to increase, potentially causing delays in satellite projects and limiting the growth potential of the market.

Opportunities

Growing Demand for Earth Observation Data in Agriculture

The growing demand for earth observation data in agriculture presents a significant opportunity for the Israel remote sensing satellites market. As agriculture continues to modernize, the need for precise, real-time data on crop health, soil moisture, and land usage is becoming increasingly vital. Satellite-based remote sensing systems offer an efficient way to monitor large agricultural areas, providing farmers with insights that help optimize productivity and resource usage. Israel’s advanced remote sensing satellite capabilities can cater to the growing need for precision agriculture by offering high-resolution imagery, data analytics, and monitoring systems. This is especially crucial for regions dealing with changing climate conditions, where data-driven insights can help manage water usage, predict crop yields, and address food security concerns. By expanding satellite solutions in the agricultural sector, Israel can contribute to sustainable farming practices while capitalizing on this growing demand for earth observation data. This opportunity for growth will likely drive further investment in remote sensing satellite infrastructure and technology development, benefiting both the agricultural sector and the broader market.

Expanding Defense and Surveillance Applications

Expanding defense and surveillance applications provide a key opportunity for the Israel remote sensing satellites market. Israel has long been a leader in satellite technology for defense purposes, and the increasing global demand for satellite-based surveillance, reconnaissance, and security services is poised to benefit the market. Remote sensing satellites play a critical role in military intelligence, border monitoring, and national security operations. As geopolitical tensions increase and the need for more sophisticated surveillance systems grows, the demand for remote sensing satellites in defense applications will likely increase. Israel, with its expertise in defense technology and satellite systems, is well-positioned to lead the market in providing these services. This growth opportunity is further supported by the Israeli government’s ongoing investments in defense technologies and its commitment to space-related innovation. By capitalizing on the need for advanced defense solutions, Israel’s satellite manufacturers can expand their footprint in the global defense market, opening new avenues for growth and development in remote sensing satellites.

Future Outlook

The future outlook for the Israel remote sensing satellites market is promising, with continued growth expected over the next five years. Technological advancements in satellite systems, increased demand for real-time data, and continued government support will drive the market’s expansion. With a focus on improving satellite launch capabilities and developing cost-effective solutions, Israel is set to maintain its competitive edge in the global space industry. Growing applications in sectors such as agriculture, defense, and environmental monitoring will contribute to the market’s growth, supported by favorable regulations and investments in space infrastructure.

Major Players

• Elbit Systems

• Rafael Advanced Defense Systems

• MDA (MacDonald, Dettwiler and Associates)

• SkyFi

• IAI Space Systems

• Israel Space Agency

• SpacePharma

• Innovative Solutions In Space

• Telesat

• Inmarsat

• GeoIQ

• SpaceX

• Boeing

• Airbus

Key Target Audience

• Government and regulatory bodies

• Defense agencies

• Satellite manufacturing companies

• Agricultural and environmental organizations

• Space technology developers

• Aerospace and defense contractors

• Commercial space operators

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the key factors that affect the Israel remote sensing satellites market. This includes understanding the key market segments, technological advancements, and regulatory considerations that influence market dynamics.

Step 2: Market Analysis and Construction

This step involves analyzing the market data collected from primary and secondary sources. It includes building a comprehensive market model, identifying trends, and estimating future growth patterns.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through consultations with industry experts and stakeholders. Their input helps refine assumptions, improve market models, and ensure accurate forecasts.

Step 4: Research Synthesis and Final Output

The final step synthesizes the research findings and presents the complete report, including market trends, forecasts, and strategic insights. The output is validated for accuracy and relevance before publication.

- Executive Summary

- Israel Remote Sensing Satellites Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased demand for surveillance and reconnaissance capabilities

Rising investments in environmental monitoring programs

Technological advancements in miniaturization and satellite launch costs - Market Challenges

High costs associated with satellite manufacturing and maintenance

Regulatory hurdles and licensing requirements for satellite launches

Limited availability of skilled workforce in satellite technology sectors - Market Opportunities

Collaborations with private space companies for low-cost satellite solutions

Growing adoption of remote sensing in agriculture for precision farming

Expansion of satellite services in emerging markets and developing countries - Trends

Shift toward smaller, more cost-effective satellite solutions

Growing integration of AI and machine learning for data analysis

Rising demand for real-time data from remote sensing satellites - Government Regulations & Defense Policy

Increased defense budget allocations for satellite-based surveillance

Growing regulatory frameworks for space debris management

Emerging policies for international cooperation in satellite technology - SWOT Analysis (Capability Strengths, Cost Vulnerabilities, Competitive Pressures)

Porter’s Five Forces (Procurement Power, Supplier Concentration, Substitutes, Barriers to Entry)

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Optical Imaging Systems

Synthetic Aperture Radar (SAR) Systems

Multispectral Imaging Systems

Hyperspectral Imaging Systems

Thermal Imaging Systems - By Platform Type (In Value%)

Low Earth Orbit (LEO) Satellites

Medium Earth Orbit (MEO) Satellites

Geostationary Orbit (GEO) Satellites

CubeSats

High Altitude Pseudo Satellites (HAPS) - By Fitment Type (In Value%)

Standalone Satellites

Satellite Constellations

Integrated Satellite Systems

On-demand Satellite Services

Hybrid Systems - By EndUser Segment (In Value%)

Government & Defense

Environmental Monitoring Agencies

Agricultural Sector

Energy & Utilities

Commercial Enterprises - By Procurement Channel (In Value%)

Direct Sales

Online Platforms

Government Contracts

Third-party Distributors

OEM Partnerships

- Market Share Analysis

- Cross Comparison Parameters

(Market Value, Installed Units, Platform Type, System Type, Fitment Type, Procurement Channels, End-User Segments, Regional Dynamics, Regulatory Landscape) - SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Israel Space Agency

Elbit Systems Ltd.

Israel Aerospace Industries (IAI)

SpacePharma

Rafael Advanced Defense Systems

Aerospace Industries Ltd.

GeoIQ

SkyFi

MDA (MacDonald, Dettwiler and Associates)

Innovative Solutions In Space

Dawn Aerospace

Inmarsat

Intelsat

SES S.A.

Telesat

- Government agencies for surveillance and defense

- Environmental organizations for climate and weather monitoring

- Agricultural firms for precision farming technologies

- Private sector companies for geospatial data analytics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now