Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Israel small UAV market was valued at USD ~ billion, driven by sustained defense investment, continuous operational demand for tactical intelligence, surveillance, and reconnaissance, and strong export momentum for proven unmanned systems. Demand is reinforced by the need for rapid situational awareness, force protection, and precision targeting in complex operational environments. Ongoing innovation in miniaturized sensors, secure communications, and autonomous flight control systems further supports steady procurement across military, homeland security, and select government applications.

Based on a recent historical assessment, Tel Aviv, Haifa, and central Israel emerged as dominant centers within the Israel small UAV market due to the concentration of defense technology companies, research institutions, and operational command units. These locations host system design, software development, testing, and integration activities. Close collaboration between the Israeli Defense Forces, domestic UAV manufacturers, and electronics suppliers accelerates deployment and iterative upgrades. Strong export orientation and proximity to logistics infrastructure further reinforce national dominance in small UAV development and production.

Market Segmentation

By Product Type

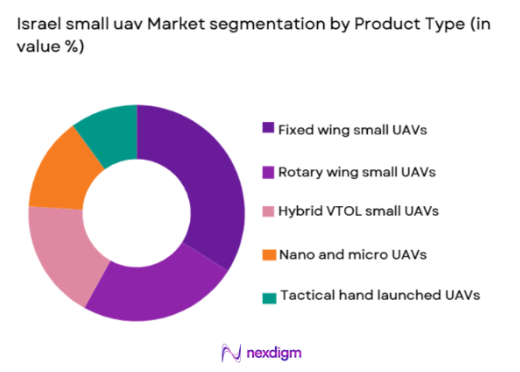

Israel small UAV market is segmented by product type into fixed wing small UAVs, rotary wing small UAVs, hybrid VTOL small UAVs, nano and micro UAVs, and tactical hand launched UAVs. Recently, fixed wing small UAVs have a dominant market share due to their extended endurance, longer operational range, and suitability for persistent ISR missions. These systems are widely used for border surveillance and tactical reconnaissance, benefiting from efficient aerodynamics and lower energy consumption. Strong domestic manufacturing expertise, proven operational performance, and compatibility with diverse payloads reinforce preference. Fixed wing platforms also support cost-effective fleet operations and rapid deployment, sustaining their dominance across defense and security users.

By End User

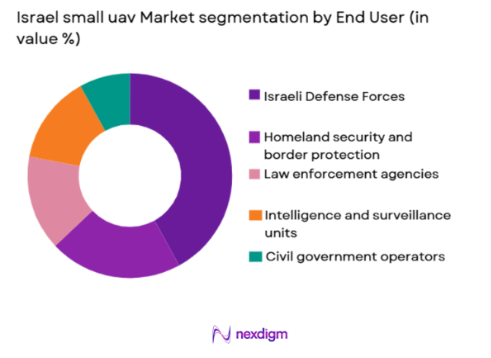

Israel small UAV market is segmented by end user segment into Israeli Defense Forces, homeland security and border protection agencies, law enforcement agencies, intelligence and surveillance units, and civil government operators. Recently, the Israeli Defense Forces have a dominant market share due to extensive operational reliance on small UAVs for tactical ISR, force protection, and mission planning. Continuous deployment across land and border operations drives recurring procurement and upgrades. Strong doctrinal integration, dedicated training infrastructure, and rapid feedback loops between operators and manufacturers accelerate adoption. High operational tempo and evolving threat environments further sustain dominant demand from defense forces.

Competitive Landscape

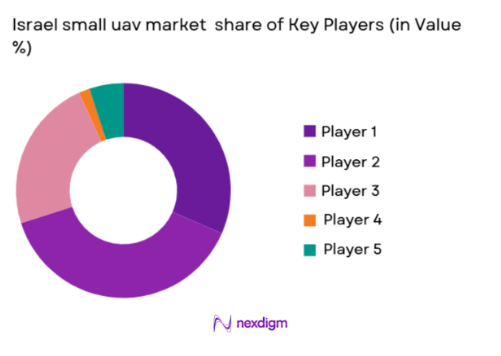

The Israel small UAV market is moderately consolidated, characterized by a mix of large defense primes and specialized UAV manufacturers with strong technology portfolios. Established players benefit from close collaboration with defense forces, export credibility, and vertically integrated capabilities, creating competitive advantages and high entry barriers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Primary UAV Segment |

| Israel Aerospace Industries | 1953 | Lod, Israel | ~ | ~ | ~ | ~ | ~ |

| Elbit Systems | 1966 | Haifa, Israel | ~ | ~ | ~ | ~ | ~ |

| Rafael Advanced Defense Systems | 1948 | Haifa, Israel | ~ | ~ | ~ | ~ | ~ |

| Aeronautics Group | 1997 | Yavne, Israel | ~ | ~ | ~ | ~ | ~ |

| BlueBird Aero Systems | 2002 | Herzliya, Israel | ~ | ~ | ~ | ~ | ~ |

Israel Small UAV Market Analysis

Growth Drivers

Operational Demand for Tactical ISR and Force Protection:

Operational demand for tactical ISR and force protection is a key growth driver for the Israel small UAV market as modern operations require real-time situational awareness. Small UAVs provide rapid intelligence collection in urban and border environments. Their deployment reduces risk to personnel while improving mission effectiveness. Persistent surveillance supports early threat detection. Integration with command systems enhances decision making. Continuous operational feedback drives iterative upgrades. Proven battlefield performance reinforces procurement confidence. Strong export demand further amplifies growth momentum.

Technological Advancements in Miniaturization and Autonomy:

Technological advancements in miniaturization and autonomy significantly drive the Israel small UAV market by expanding operational capability. Smaller sensors deliver higher resolution imagery. Improved batteries extend endurance. Autonomous navigation reduces operator workload. AI-enabled analytics accelerate target recognition. Secure data links improve resilience. Modular architectures support rapid payload changes. Domestic innovation ecosystems accelerate development cycles. These advancements sustain replacement and upgrade demand.

Market Challenges

Airspace Regulation and Operational Constraints:

Airspace regulation and operational constraints pose a significant challenge for the Israel small UAV market as UAV density increases. Coordination with civil aviation authorities is required. Restricted airspace limits training flexibility. Regulatory compliance increases operational complexity. Urban operations face safety concerns. Licensing and certification processes add administrative burden. Balancing security and safety requirements is challenging. These factors can slow deployment expansion.

Electronic Warfare and Counter-UAV Threats:

Electronic warfare and counter-UAV threats challenge market growth by reducing operational survivability. Adversaries deploy jamming and spoofing systems. Communication disruption affects mission success. Increased need for secure links raises costs. Countermeasures add system complexity. Rapid threat evolution shortens technology cycles. Continuous upgrades strain budgets. These challenges necessitate sustained R&D investment.

Opportunities

Expansion of AI Enabled Autonomous Small UAVs:

Expansion of AI enabled autonomous small UAVs presents strong opportunity within the Israel small UAV market as autonomy improves operational efficiency. AI supports automated navigation and target detection. Reduced operator burden increases scalability. Swarm coordination enhances coverage. Adaptive learning improves mission outcomes. Defense funding supports AI integration. Export interest in autonomous systems grows. This opportunity supports long-term growth.

Growing Export Demand for Proven Small UAV Systems:

Growing export demand for proven small UAV systems offers opportunity as international customers seek combat-tested platforms. Israeli UAVs benefit from operational credibility. Customization for diverse missions expands addressable markets. Government support facilitates exports. Training and sustainment services add value. Strategic partnerships extend reach. This opportunity strengthens global market presence.

Future Outlook

The Israel small UAV market is expected to experience steady growth over the next five years, supported by continuous defense modernization and strong export demand. Advances in autonomy, sensor integration, and endurance will shape product development. Regulatory frameworks are expected to adapt to increased UAV usage. Rising emphasis on multi-mission and swarm-capable systems will further drive demand.

Major Players

- Israel Aerospace Industries

- Elbit Systems

- Rafael Advanced Defense Systems

- Aeronautics Group

- BlueBird Aero Systems

- UVision Air

- Controp Precision Technologies

- NextVision Stabilized Systems

- Steadicopter

- Xtend

- Heven Drones

- Smart Shooter

- Orbit Communication Systems

- RT LTA Systems

- SightX

Key Target Audience

- Defense ministries

- Military procurement agencies

- Homeland security organizations

- Law enforcement agencies

- Border protection forces

- Defense system integrators

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including UAV fleet size, procurement budgets, operational requirements, technology trends, and regulatory frameworks were identified through structured secondary research.

Step 2: Market Analysis and Construction

Data were analyzed to construct market size, segmentation, and competitive dynamics using validated analytical models and triangulation.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with UAV operators, defense engineers, and industry experts to ensure accuracy.

Step 4: Research Synthesis and Final Output

All validated insights were synthesized into a comprehensive report with consistency and reliability checks

- Executive Summary

- Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for ISR and tactical surveillance

Operational shift toward unmanned and autonomous systems

Continuous innovation in sensors and miniaturization - Market Challenges

Airspace regulation and operational restrictions

Electronic warfare and counter UAV threats

Limited endurance and payload constraints - Market Opportunities

Expansion of AI enabled autonomous small UAVs

Growing use of UAV swarms and collaborative missions

Export growth driven by proven combat performance - Trends

Miniaturization of sensors and payloads

Increased endurance through energy optimization

Integration of AI based target recognition

Adoption of swarm and networked UAV operations

Growth in dual use military and civil applications - Government Regulations & Defense Policy

Support for indigenous UAV development programs

Strengthening of export control and licensing frameworks

Regulatory oversight on UAV airspace integration - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fixed wing small UAVs

Rotary wing small UAVs

Hybrid VTOL small UAVs

Nano and micro UAVs

Tactical hand launched UAVs - By Platform Type (In Value%)

Land based launch platforms

Naval deployed platforms

Vehicle mounted UAV systems

Backpack portable platforms

Catapult and rail launch platforms - By Fitment Type (In Value%)

New system procurement

Retrofit and upgrade installations

Modular payload integration fitment

Mission specific configuration fitment

Training and simulation fitment systems - By EndUser Segment (In Value%)

Israeli Defense Forces

Homeland security and border protection

Law enforcement agencies

Intelligence and surveillance units

Commercial and civil government operators - By Procurement Channel (In Value%)

Direct government procurement

Defense prime contractor sourcing

System integrator procurement programs

Export and international sales

R&D and prototype acquisition programs - By Material / Technology (in Value %)

Composite airframe materials

Electric propulsion systems

Electro optical and infrared payloads

Autonomous navigation and AI software

Secure data link and communication systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Endurance, Payload Capacity, Range, Launch Method, Autonomy Level, Sensor Integration, Communication Security, Lifecycle Cost, Export Readiness)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Israel Aerospace Industries

Elbit Systems

Rafael Advanced Defense Systems

Aeronautics Group

UVision Air

BlueBird Aero Systems

Controp Precision Technologies

NextVision Stabilized Systems

SightX

RT LTA Systems

Orbit Communication Systems

Steadicopter

Xtend

Heven Drones

Smart Shooter

- High reliance on small UAVs for tactical ISR missions

- Strong preference for rapid deployment and portability

- Emphasis on survivability in contested environments

- Growing demand for multi mission and modular UAV systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now