Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Italy’s AI servers and GPU hardware market reached approximately USD ~ billion based on a recent historical assessment, driven by accelerating enterprise AI adoption and high-performance computing investments across cloud providers, research institutions, and industrial enterprises. Data from the European Commission Digital Economy indicators and Italy’s National Recovery and Resilience Plan digital infrastructure funding shows expanding deployment of AI training clusters and inference servers. Growth is supported by demand for generative AI workloads, computer vision, and simulation across manufacturing, finance, and telecom sectors.

Northern technology and research hubs including Lombardy, Piedmont, and Lazio dominate AI server and GPU hardware adoption due to concentration of data centers, hyperscale cloud regions, and national supercomputing facilities. Milan and Turin host enterprise AI clusters and industrial analytics deployments linked to automotive and manufacturing ecosystems, while Rome benefits from public research institutions and government digitalization programs.

Market Segmentation

By Product Type

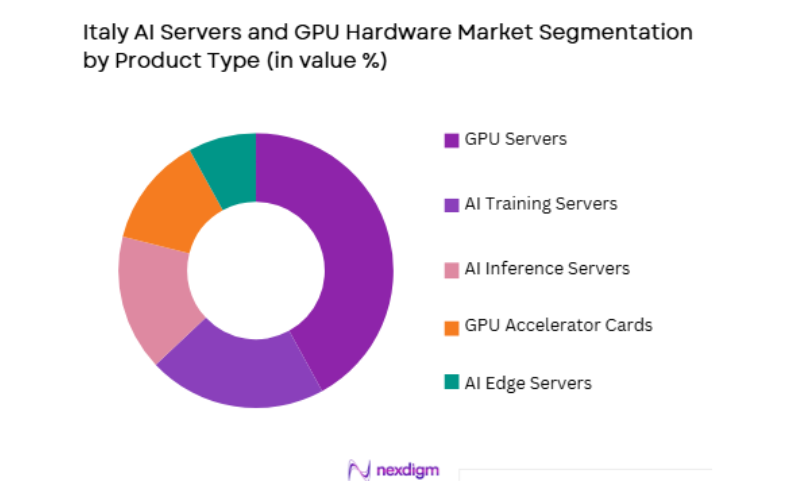

Italy AI Servers and GPU Hardware market is segmented by product type into GPU servers, AI training servers, AI inference servers, GPU accelerator cards, and AI edge servers. Recently, GPU servers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Enterprises and cloud providers deploy GPU-dense rack servers to support large-scale model training, simulation, and advanced analytics workloads that require parallel compute capacity and high-bandwidth memory architectures. National supercomputing initiatives and enterprise AI labs invest heavily in multi-GPU systems integrated with high-speed interconnects and storage fabrics.

By End-Use Sector

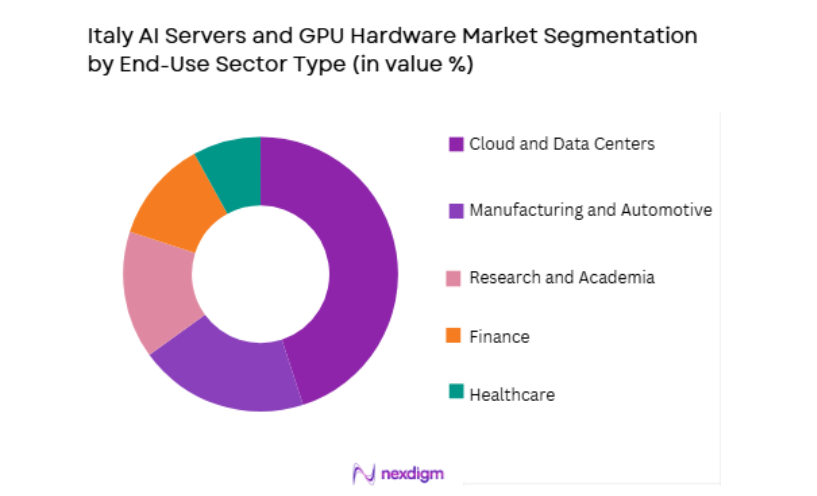

Italy AI Servers and GPU Hardware market is segmented by end-use sector into cloud and data centers, manufacturing and automotive, research and academia, finance, and healthcare. Recently, cloud and data centers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Hyperscale and colocation providers deploy large GPU clusters to host AI training platforms and generative AI services consumed by enterprises across industries. Rapid expansion of AI-enabled cloud offerings requires continuous hardware refresh cycles with higher-performance GPUs and dense server architectures. Italy’s role as a regional data hub in southern Europe encourages infrastructure investment from global cloud operators and interconnection providers.

Competitive Landscape

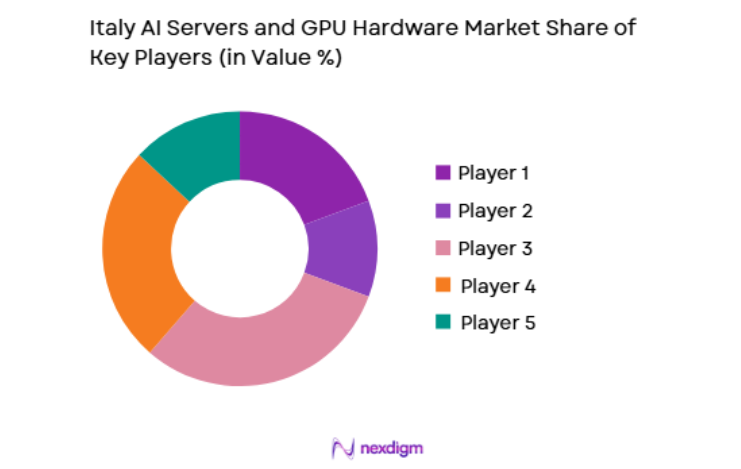

Italy’s AI servers and GPU hardware market is concentrated among global semiconductor and server manufacturers supplying hyperscale cloud operators, national supercomputing centers, and enterprise data-center deployments. Competition focuses on GPU performance leadership, system integration capability, and energy-efficient high-density server design. Partnerships with cloud providers and research institutions strongly influence procurement, while European digital sovereignty initiatives encourage local and regional supplier participation alongside dominant global vendors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI GPU Architecture Focus |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| AMD | 1969 | USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

Italy AI Servers and GPU Hardware Market Analysis

Growth Drivers

Enterprise and Cloud Generative AI Infrastructure Expansion

Italy’s rapid adoption of generative AI applications across finance, manufacturing design, customer analytics, and digital services is driving substantial demand for high-performance GPU servers capable of training and deploying large language and multimodal models within enterprise and cloud environments, encouraging hyperscale and regional cloud providers to expand AI data-center capacity and invest in next-generation accelerator hardware across Italian infrastructure hubs. Organizations increasingly require dedicated AI clusters to manage proprietary data and domain-specific models, shifting compute demand from shared CPU-centric environments toward GPU-dense architectures optimized for parallel processing and deep learning workloads. National digital transformation programs and enterprise innovation initiatives promote AI experimentation and production deployment, increasing procurement of training servers and high-memory GPUs. Telecom and financial service firms deploy AI platforms for fraud detection, network optimization, and automated customer interaction, requiring scalable GPU compute resources. Integration of AI into industrial design and simulation workflows also raises demand for accelerated computing in engineering environments.

National Supercomputing and Sovereign AI Infrastructure Investments

Italy’s strategic investment in high-performance computing and sovereign AI capabilities is significantly increasing demand for advanced GPU-accelerated servers and exascale-class compute infrastructure deployed in national research centers and public data facilities to support scientific simulation, climate modeling, pharmaceutical research, and national AI initiatives requiring massive parallel processing power and high-bandwidth interconnect architectures. Government-supported supercomputing programs procure large GPU clusters integrated with high-speed networking and storage systems, creating substantial domestic hardware deployment volumes. These infrastructures also provide shared AI training resources for academia and industry, expanding utilization and stimulating broader ecosystem demand for compatible GPU hardware. European digital sovereignty policies encourage localized AI compute capacity to reduce dependence on foreign cloud providers, reinforcing investment in national facilities. Collaboration between research institutions and industry accelerates adoption of GPU-accelerated modeling and analytics across sectors.

Market Challenges

High Capital Cost and Rapid Hardware Obsolescence Cycles

AI servers and GPU hardware involve extremely high upfront capital expenditure due to premium accelerator components, advanced interconnects, and specialized cooling infrastructure, posing financial challenges for Italian enterprises and data-center operators attempting to scale AI capabilities while managing uncertain return on investment and rapid technological evolution that shortens hardware lifecycle expectations and increases upgrade frequency requirements. GPU architectures evolve quickly with significant performance improvements across generations, making recently deployed clusters potentially less competitive within a few years and discouraging long-term investment commitments. Enterprises must balance procurement timing with technology roadmaps to avoid stranded assets, complicating budgeting and infrastructure planning. Power density and cooling requirements also increase operational costs and facility upgrade needs, particularly in legacy data centers. Limited secondary markets for high-end AI hardware reduce residual value recovery. Smaller enterprises face financing constraints and rely on cloud services instead of direct hardware ownership.

Energy Consumption and Data Center Infrastructure Constraints

AI servers and GPU clusters require substantial electrical power and advanced cooling systems due to high thermal output and compute density, creating infrastructure constraints in Italy where energy costs and grid capacity limitations affect large-scale data-center expansion and on-premise AI hardware deployment decisions across enterprises and cloud providers seeking to scale accelerated computing resources. GPU-dense racks significantly increase power demand compared with traditional servers, necessitating facility upgrades such as liquid cooling, high-capacity transformers, and redundant power supply systems. Italy’s energy pricing and sustainability regulations increase operational expenditure for compute-intensive infrastructure, influencing total cost of ownership calculations. Data-center site selection is constrained by grid availability and permitting requirements, limiting rapid expansion of AI clusters in some regions. Enterprises deploying on-premise GPU servers must invest in specialized cooling and electrical systems, raising barriers to adoption.

Opportunities

AI-Enabled Industrial Design, Simulation, and Digital Twin Platforms

Italy’s strong automotive, machinery, aerospace, and industrial design sectors create significant opportunity for deployment of GPU-accelerated AI servers to support advanced simulation, generative engineering, and digital twin modeling workflows that require high-performance parallel computing to optimize product design, manufacturing processes, and operational performance across complex engineering environments within enterprise R&D centers and industrial innovation hubs. Engineering teams increasingly use AI-driven simulation and generative design tools that rely on GPU clusters for rapid iteration and optimization. Digital twin platforms for factories and products demand continuous high-resolution modeling and analytics capabilities. Integration of AI into CAD, robotics planning, and material science accelerates compute requirements. National innovation programs supporting advanced manufacturing encourage investment in accelerated computing infrastructure. Collaboration between industry and research institutions further drives adoption of HPC-class GPU servers.

Regional AI Cloud and Colocation GPU Infrastructure Expansion

Italy’s role as a southern European digital hub and gateway to Mediterranean connectivity positions the country for expansion of regional AI cloud and colocation facilities hosting GPU clusters to serve enterprises across Europe, the Middle East, and Africa, creating strong opportunity for large-scale deployment of AI servers and accelerators within carrier-neutral data-center campuses and interconnection-rich metropolitan regions such as Milan and Rome supporting cross-border AI service delivery and data-localization requirements. Global cloud providers seek regional GPU capacity to reduce latency and comply with European data regulations. Colocation operators invest in AI-ready facilities with high-density power and cooling. Enterprises increasingly adopt hybrid AI cloud models requiring local GPU resources.

Future Outlook

Italy’s AI servers and GPU hardware market is expected to expand strongly as enterprise AI adoption and sovereign compute investments accelerate nationwide. Generative AI and simulation workloads will drive deployment of high-density GPU clusters across cloud and industrial environments. Energy-efficient cooling and advanced interconnect technologies will shape next-generation AI infrastructure.

Major Players

- NVIDIA

- AMD

- Intel

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Supermicro

- Cisco

- Atos

- Fujitsu

- Inspur

- Huawei

- IBM

- NEC

- Gigabyte

Key Target Audience

- Cloud service providers

- Telecom operators

- Manufacturing enterprises

- Automotive OEMs

- Financial institutions

- Healthcare technology providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including AI workload intensity, GPU deployment density, data-center capacity, and enterprise AI adoption rates were mapped across Italian industries and regions. Supply-side variables such as vendor shipments, accelerator performance trends, and infrastructure investment were also identified to structure the market model.

Step 2: Market Analysis and Construction

Segment-level demand across product types and sectors was assessed using data-center expansion indicators and AI adoption metrics. Market size was constructed through bottom-up aggregation of GPU server, accelerator, and AI system revenues deployed within Italy’s enterprise and cloud infrastructure landscape.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding adoption drivers, constraints, and deployment patterns were validated through consultation with data-center architects, HPC specialists, and enterprise AI infrastructure engineers. Cross-verification with national digital infrastructure initiatives and procurement programs refined the market estimates.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were synthesized into segmentation, competitive, and strategic analyses describing Italy’s AI server and GPU hardware ecosystem. Final outputs emphasize structural demand drivers, technological shifts, and infrastructure constraints shaping market evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of European AI and HPC infrastructure programs

Enterprise adoption of AI and data analytics workloads

Growth of hyperscale and colocation AI data centers - Market Challenges

High cost and supply constraints of advanced GPUs

Power and cooling limitations for dense AI hardware

Dependence on imported semiconductor components - Market Opportunities

Sovereign AI and HPC infrastructure initiatives

AI deployment across manufacturing and public sector

Renewable powered AI data center expansion - Trends

Adoption of high density GPU clusters

Liquid cooling in AI server infrastructure - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

GPU Accelerated AI Servers

AI Training Servers

AI Inference Servers

Multi GPU High Density Servers

AI Optimized Rack Scale Systems - By Platform Type (In Value%)

Hyperscale Cloud AI Platforms

Enterprise AI Data Centers

Research and Academic AI Clusters

Telecom AI Infrastructure

Edge AI Server Deployments - By Fitment Type (In Value%)

New AI Server Deployments

Data Center AI Retrofits

Modular AI Server Racks

Integrated AI Infrastructure Systems - By End User Segment (In Value%)

Cloud Service Providers

Enterprises

Government and Research Institutions

Telecom Operators

- Market Share Analysis

- Cross Comparison Parameters (GPU Density, Compute Performance, Power Efficiency, Cooling Architecture, Interconnect Bandwidth, Memory Bandwidth, Scalability, Rack Power Density, AI Framework Optimization, Deployment Flexibility, Supply Chain Availability, Total Cost of Ownership))

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

AMD

Intel

Dell Technologies

Hewlett Packard Enterprise

Lenovo

Supermicro

Gigabyte

ASUS

IBM

Cisco

Oracle

Microsoft

Amazon Web Services

Google

- Cloud providers scaling GPU clusters in Italy

- Enterprises deploying private AI compute infrastructure

- Research institutions expanding AI and HPC labs

- Telecom operators enabling AI driven network optimization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now