Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Italy’s cloud infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by enterprise digital transformation, hyperscale data center expansion, and public sector cloud adoption under national digitalization programs. Demand growth is supported by migration from on-premises IT systems to scalable cloud platforms, expansion of colocation capacity, and investments by global cloud providers establishing regional availability zones. Financial services, manufacturing, and government digital services modernization programs have accelerated infrastructure deployment.

Milan dominates Italy’s cloud infrastructure landscape due to concentration of financial institutions, telecom interconnection hubs, and hyperscale data center campuses supported by dense fiber networks and reliable power infrastructure. Lombardy hosts most colocation and cloud availability zones, benefiting from proximity to European internet exchange corridors. Rome follows with strong government cloud demand and public administration digitalization programs.

Market Segmentation

By Product Type

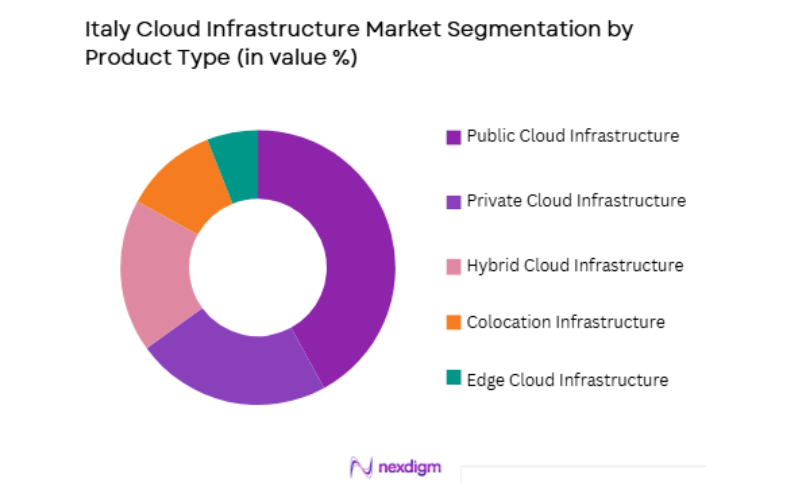

Italy Cloud Infrastructure market is segmented by product type into public cloud infrastructure, private cloud infrastructure, hybrid cloud infrastructure, colocation infrastructure, and edge cloud infrastructure. Recently, public cloud infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Enterprise IT modernization and scalability requirements have driven migration toward hyperscale public cloud platforms operated by global providers with Italian regions.

By End-Use Industry

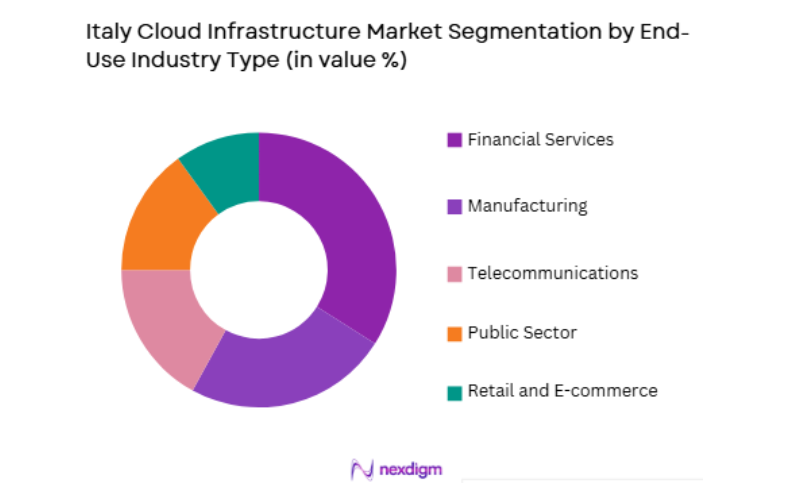

Italy Cloud Infrastructure market is segmented by end-use industry into financial services, manufacturing, telecommunications, public sector, and retail and e-commerce. Recently, financial services has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Italy’s banking and insurance sector requires secure, compliant, and highly available computing environments for digital banking platforms, payments, and analytics workloads.

Competitive Landscape

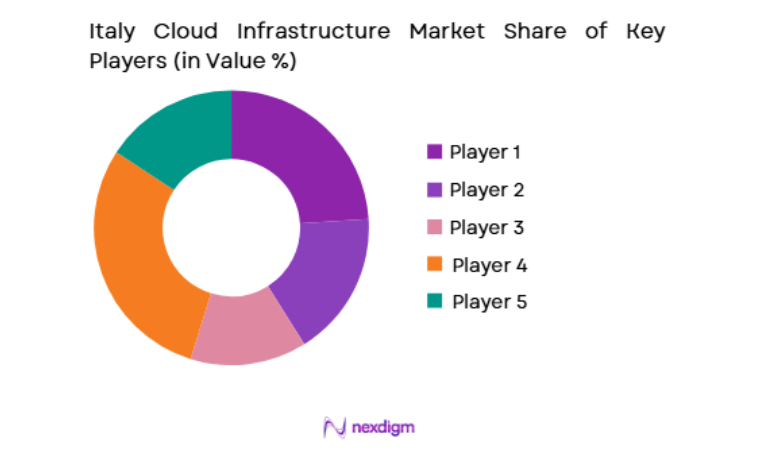

Italy’s cloud infrastructure market is moderately concentrated, led by global hyperscale providers and major European telecom-cloud operators with regional data center footprints. Hyperscalers drive capacity expansion through Italian cloud regions, while telecom and colocation firms provide interconnection and hybrid hosting services. Strategic partnerships between cloud providers, telecom carriers, and system integrators shape enterprise adoption.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Italy Cloud Region Presence |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ |

| OVHcloud | 1999 | Roubaix, France | ~ | ~ | ~ | ~ | ~ |

| Aruba Cloud | 2011 | Bergamo, Italy | ~ | ~ | ~ | ~ | ~ |

Italy Cloud Infrastructure Market Analysis

Growth Drivers

National Digital Transformation and Public Sector Cloud Adoption Programs

Italy’s cloud infrastructure expansion is strongly driven by coordinated national digitalization strategies that prioritize migration of public administration systems, healthcare platforms, and municipal services to secure domestic cloud environments to improve efficiency, resilience, and citizen service delivery. Government cloud initiatives mandate modernization of legacy IT infrastructure and consolidation into certified cloud platforms, creating sustained demand for domestic data center capacity, sovereign cloud environments, and compliant infrastructure operated within national borders. Public procurement frameworks favor cloud-first deployment models for new digital services, accelerating infrastructure utilization by ministries, regional governments, and public agencies across Italy. Investments in national strategic cloud platforms and public sector digital identity, payments, and administrative portals require scalable compute and storage capacity, reinforcing hyperscale and sovereign cloud infrastructure deployment.

Enterprise Cloud Migration and Industrial Digitalization Across Manufacturing Economy

Italy’s industrial base, characterized by manufacturing, logistics, and design-oriented enterprises, is undergoing accelerated digital transformation that relies on scalable cloud infrastructure to support automation, data analytics, and connected production systems across geographically distributed facilities. Industrial firms are migrating enterprise resource planning, product lifecycle management, and supply chain platforms from on-premise servers to cloud environments to improve operational agility and collaboration across supply networks. Adoption of industrial internet of things and predictive maintenance technologies generates continuous data streams requiring cloud-based storage, processing, and analytics infrastructure, expanding enterprise cloud consumption. Small and medium manufacturing enterprises, which dominate Italy’s industrial structure, increasingly adopt public and hybrid cloud platforms to access advanced computing capabilities without large capital investments in IT infrastructure. Cloud-hosted design, simulation, and digital twin tools are enabling Italian manufacturing firms to innovate products and processes, reinforcing infrastructure demand for high-performance computing and storage services. Integration of e-commerce, logistics tracking, and customer analytics systems across manufacturing supply chains further increases reliance on cloud platforms for data integration and real-time visibility.

Market Challenges

Data Sovereignty, Regulatory Compliance, and Localization Constraints

Italy’s cloud infrastructure market faces structural challenges related to stringent European and national data protection regulations that impose requirements on data residency, privacy, and security controls, complicating deployment and operation of cloud infrastructure across regulated sectors such as finance, healthcare, and public administration. Compliance with European data protection frameworks and national cybersecurity certification schemes requires cloud providers to establish localized infrastructure, governance controls, and audit capabilities, increasing operational complexity and cost relative to more flexible global cloud deployment models. Enterprises handling sensitive or strategic data often require sovereign or nationally controlled cloud environments, limiting the use of standard hyperscale public cloud architectures and necessitating customized infrastructure configurations within Italy. Regulatory approval processes for public sector cloud deployments can extend procurement timelines and delay infrastructure utilization, affecting market growth pace.

Energy Availability, Sustainability Requirements, and Data Center Power Constraints

Expansion of cloud infrastructure in Italy is constrained by energy availability, power grid capacity, and sustainability regulations affecting large-scale data center deployment, particularly in northern regions where demand for electricity is already concentrated across industrial and urban sectors. Hyperscale data centers require significant and stable power supply, and grid connection approvals, land availability, and environmental permitting processes can delay infrastructure construction and capacity expansion. Italy’s electricity costs are comparatively high within Europe, increasing operational expenses for data center operators and influencing location decisions relative to lower-cost energy regions. Sustainability requirements and carbon reduction targets encourage use of renewable energy and efficient cooling technologies, necessitating additional investment in green infrastructure and energy sourcing agreements.

Opportunities

Sovereign and European Trusted Cloud Infrastructure Development

Italy has a significant opportunity to expand cloud infrastructure through development of sovereign and European-trusted cloud platforms aligned with regional digital sovereignty initiatives that prioritize data control, regulatory compliance, and technological autonomy across critical sectors such as government, finance, and defense. European enterprises and public institutions increasingly seek cloud environments operated under European jurisdiction with transparent governance and compliance assurance, creating demand for domestic and EU-based infrastructure providers. Italy’s participation in European trusted cloud frameworks and cross-border sovereign cloud initiatives positions domestic infrastructure operators to capture demand from regulated industries requiring certified hosting environments. Partnerships between Italian telecom operators, national cloud providers, and European technology firms can establish sovereign cloud regions combining hyperscale scalability with European governance standards.

Edge Computing and Industrial Cloud Integration in Smart Manufacturing Regions

Italy’s distributed manufacturing economy and industrial clusters create a strong opportunity for edge-integrated cloud infrastructure that combines centralized hyperscale capacity with localized edge data centers supporting low-latency industrial and logistics applications across production sites. Industrial automation, robotics, and real-time analytics systems require localized processing near factories and warehouses, driving deployment of regional edge cloud nodes interconnected with central cloud platforms. Northern Italy’s manufacturing districts in Lombardy, Veneto, and Emilia-Romagna provide dense demand centers for edge-cloud integration supporting connected machinery, quality control, and supply chain visibility systems. Telecom operators expanding 5G networks can integrate edge computing infrastructure with cloud platforms to enable industrial internet of things applications and autonomous logistics solutions.

Future Outlook

Italy’s cloud infrastructure market is expected to grow steadily over the next five years, supported by enterprise digitalization, sovereign cloud initiatives, and hyperscale data center expansion. Continued public sector cloud migration and industrial digital transformation will sustain demand. Edge computing and AI-enabled cloud services will drive infrastructure diversification.

Major Players

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- OVHcloud

- Aruba Cloud

- TIM Cloud

- Oracle Cloud

- IBM Cloud

- Equinix

- Digital Realty

- Interxion

- Fastweb

- Retelit

- Leonardo Cloud

- Seeweb

Key Target Audience

- Large enterprises and corporations

- Financial institutions

- Manufacturing companies

- Telecommunications operators

- Public sector agencies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Cloud service providers

Research Methodology

Step 1: Identification of Key Variables

Key variables including cloud deployment models, data center capacity, hyperscale presence, and enterprise demand sectors were identified. Regulatory, digitalization, and industrial digital adoption factors influencing Italy’s cloud infrastructure were mapped.

Step 2: Market Analysis and Construction

Primary and secondary data from cloud providers, telecom operators, policy programs, and infrastructure investments were synthesized. Market segmentation and competitive positioning were derived through capacity, deployment, and demand analysis.

Step 3: Hypothesis Validation and Expert Consultation

Growth assumptions and infrastructure trends were validated through consultations with cloud architects, data center engineers, and enterprise IT specialists. Findings were cross-verified with observed Italian cloud adoption patterns.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative insights were integrated into a structured framework covering segmentation, competition, drivers, challenges, and opportunities. Final outputs were reviewed for consistency with Italy’s digital economy and cloud infrastructure dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Enterprise digital transformation and AI workload expansion

National cloud adoption and data sovereignty initiatives

Hyperscale data center investments across Italy - Market Challenges

Data localization and compliance complexity

Energy cost pressures on data center operations

Skills shortage in cloud architecture and operations - Market Opportunities

Growth of sovereign and regulated industry clouds

Edge cloud deployment for Industry 4.0 and 5G

Public sector cloud migration programs - Trends

Shift toward hybrid and multicloud architectures

Acceleration of AI-ready cloud infrastructure - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compute Infrastructure (IaaS Servers & Virtual Machines)

Storage Infrastructure (Object & Block Storage Systems)

Network Infrastructure (SDN & Cloud Networking)

Hyperconverged Infrastructure (HCI Systems)

Cloud Security Infrastructure (Identity & Protection Platforms) - By Platform Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Multicloud Infrastructure

Edge Cloud Infrastructure - By Fitment Type (In Value%)

Greenfield Cloud Deployments

Brownfield Cloud Modernization

Colocation-based Cloud Integration

On-premise to Cloud Migration - By End User Segment (In Value%)

Large Enterprises

Small & Medium Enterprises

Government & Public Sector

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio Depth, Data Center Footprint, Sovereign Cloud Capability, Industry-specific Solutions, AI Infrastructure Readiness, Hybrid & Multicloud Integration, Security & Compliance Certifications, Pricing Flexibility, Managed Services Capability, Edge Cloud Presence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Telecom Italia (TIM)

Leonardo S.p.A.

Engineering Ingegneria Informatica

Aruba S.p.A.

OVHcloud

Amazon Web Services

Microsoft

Google Cloud

Oracle

IBM

Atos

NTT DATA Italia

Fastweb

Vodafone Italia

Telecom Italia Sparkle

- Enterprises scaling hybrid and AI cloud platforms

- SMEs adopting managed cloud and SaaS infrastructure

- Public sector prioritizing sovereign cloud environments

- Telecom operators integrating edge and core cloud

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now