Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Italy’s diagnostic laboratories market demonstrates substantial economic scale within the national healthcare system, supported by extensive public healthcare infrastructure and rising demand for diagnostic testing. Based on a recent historical assessment, the market size reached approximately USD ~ billion, supported by increasing diagnostic procedures, expansion of laboratory networks, and continuous demand for clinical pathology and molecular testing services. Data published by the Italian Ministry of Health and OECD health expenditure records indicate strong spending on diagnostic services, strengthening laboratory capabilities nationwide.

Diagnostic activity in Italy is strongly concentrated in major healthcare hubs where hospital networks, research institutions, and private laboratory chains operate extensive diagnostic facilities. Cities such as Milan, Rome, Bologna, and Turin dominate laboratory services due to advanced hospital ecosystems, strong biomedical research presence, and dense populations requiring continuous diagnostic monitoring. These urban healthcare clusters host large private laboratory groups and academic medical centers, enabling efficient diagnostic service delivery and facilitating continuous adoption of molecular diagnostics, pathology automation, and precision medicine testing.

Market Segmentation

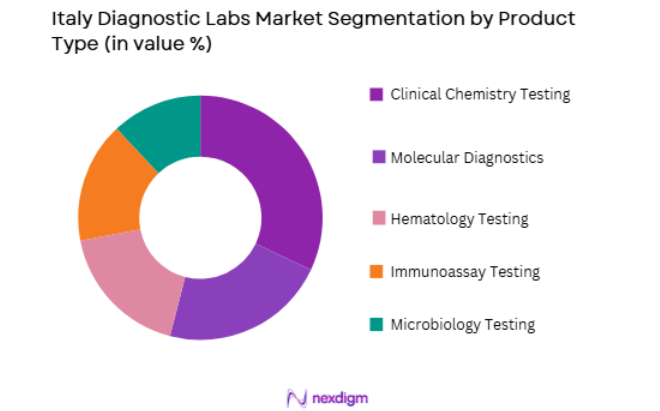

By Product Type

Italy Diagnostic Labs market is segmented by product type into Clinical Chemistry Testing, Molecular Diagnostics, Hematology Testing, Immunoassay Testing, and Microbiology Testing. Recently, Clinical Chemistry Testing has a dominant market share due to the high frequency of routine health examinations and chronic disease monitoring across Italian healthcare facilities. Clinical chemistry tests support large patient volumes in hospitals and diagnostic laboratories, enabling regular monitoring of metabolic conditions, cardiovascular risks, and endocrine disorders. Strong integration with automated laboratory analyzers, availability across hospital laboratories, and inclusion in routine health panels further strengthen the demand for clinical chemistry testing services throughout Italy’s diagnostic ecosystem.

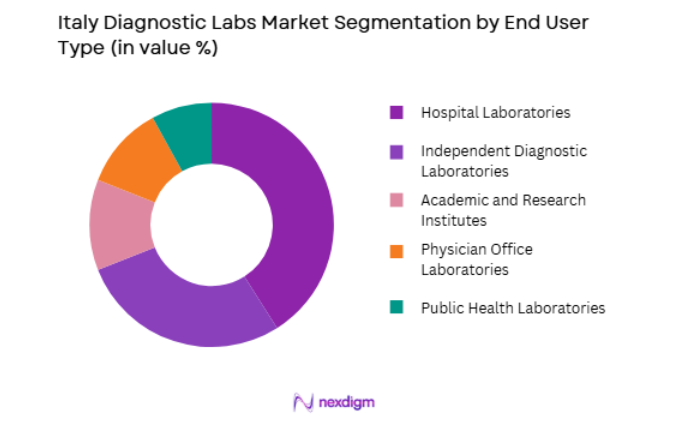

By End User

Italy Diagnostic Labs market is segmented by end user into Hospital Laboratories, Independent Diagnostic Laboratories, Academic and Research Institutes, Physician Office Laboratories, and Public Health Laboratories. Recently, Hospital Laboratories have a dominant market share due to their central role in Italy’s public healthcare system and strong integration with national health service hospitals. Large public hospitals conduct extensive diagnostic testing across pathology, microbiology, and molecular diagnostics to support inpatient and outpatient services. The availability of advanced diagnostic instruments, large testing volumes, and continuous clinical integration allows hospital laboratories to maintain operational dominance within the diagnostic testing infrastructure across Italy.

Competitive Landscape

The Italy diagnostic laboratories market is moderately consolidated, with a combination of multinational diagnostic companies and domestic laboratory networks shaping the competitive environment. Large healthcare service providers operate extensive laboratory networks supported by automation, molecular diagnostics technologies, and integrated pathology systems. Strategic partnerships with hospitals, acquisitions of independent laboratories, and expansion of specialized diagnostic testing capabilities have strengthened competitive positioning. Major companies focus on automation, digital pathology integration, and high-throughput diagnostic platforms to manage increasing testing volumes while maintaining operational efficiency and nationwide diagnostic service coverage.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Laboratory Network Scale |

| Synlab Group | 1998 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| Cerba HealthCare | 1967 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Eurofins Scientific | 1987 | Luxembourg | ~ | ~ | ~ | ~ | ~ |

| Laboratorio Analisi Synlab Italia | 2009 | Milan, Italy | ~ | ~ | ~ | ~ | ~ |

| Unilabs | 1987 | Geneva, Switzerland | ~ | ~ | ~ | ~ | ~ |

Italy Diagnostic Labs Market Analysis

Growth Drivers

Expansion of Preventive Healthcare and Chronic Disease Monitoring Programs

Italy’s healthcare system increasingly emphasizes preventive healthcare and early disease detection, which significantly drives demand for diagnostic laboratory services. Rising incidence of cardiovascular disease, diabetes, cancer, and metabolic disorders requires frequent laboratory testing to monitor disease progression and treatment outcomes. The national healthcare system encourages routine diagnostic screening programs for early detection, particularly in oncology and cardiovascular risk management. Aging demographics further increase laboratory utilization because older populations require continuous biochemical and hematological monitoring. Hospitals and outpatient diagnostic centers conduct extensive laboratory testing to support routine medical examinations and clinical decision making. Diagnostic laboratories play a critical role in preventive health strategies by providing accurate clinical data supporting disease management protocols. Increased awareness of preventive medicine among patients has also expanded demand for routine diagnostic services across both public hospitals and private diagnostic networks. Technological advancements in automated laboratory analyzers have improved efficiency and reduced turnaround time, enabling laboratories to manage higher test volumes effectively.

Adoption of Advanced Molecular and Precision Diagnostic Technologies

Continuous advancements in molecular diagnostics and genomic technologies are transforming laboratory testing capabilities across Italy’s healthcare ecosystem. Diagnostic laboratories increasingly deploy polymerase chain reaction technologies, next-generation sequencing platforms, and advanced biomarker testing to support precision medicine initiatives. These technologies enable clinicians to identify disease at earlier stages and personalize treatment strategies based on genetic and molecular markers. Hospitals and specialized laboratories invest heavily in automated diagnostic platforms capable of high throughput testing with enhanced accuracy. The integration of molecular diagnostics into infectious disease detection, oncology testing, and rare disease diagnostics has expanded laboratory service portfolios. Growing demand for personalized healthcare also encourages laboratories to expand genomic testing services supporting targeted therapy selection. Collaboration between research institutions, biotechnology firms, and clinical laboratories accelerates the translation of scientific discoveries into routine diagnostic applications. These developments enhance diagnostic efficiency while enabling more sophisticated disease detection capabilities within Italy’s laboratory testing infrastructure.

Market Challenges

High Operational Costs Associated with Laboratory Infrastructure and Equipment

Diagnostic laboratories require significant capital investment to establish and maintain advanced laboratory infrastructure capable of delivering reliable clinical testing services. Automated analyzers, molecular diagnostic platforms, laboratory information systems, and specialized laboratory environments demand continuous financial investment. Laboratories must also invest in skilled personnel, quality control systems, and regulatory compliance procedures to maintain diagnostic accuracy and safety standards. High operational costs can limit expansion opportunities for smaller laboratories and independent diagnostic facilities operating within Italy’s healthcare market. Maintaining sophisticated laboratory equipment involves continuous maintenance, calibration, and replacement costs that add to financial pressure. Additionally, reimbursement policies within the national healthcare system often limit pricing flexibility for diagnostic testing services. Laboratories must therefore manage operational efficiency while maintaining high quality diagnostic services within regulated reimbursement structures. These financial constraints create barriers for new entrants attempting to establish competitive diagnostic laboratory operations.

Complex Regulatory and Accreditation Requirements for Clinical Diagnostics

Diagnostic laboratories operating in Italy must comply with rigorous regulatory frameworks governing clinical testing accuracy, laboratory safety standards, and quality assurance procedures. Accreditation requirements established by national health authorities mandate strict adherence to standardized testing protocols and laboratory quality management systems. Laboratories must regularly undergo inspections, validation processes, and certification renewals to maintain authorization to perform diagnostic testing. Compliance with European Union diagnostic regulations and in vitro diagnostic device standards further increases regulatory complexity. Laboratories must also implement extensive documentation and traceability procedures to ensure test reliability and patient safety. Meeting these requirements requires dedicated regulatory compliance teams and substantial administrative resources. Smaller laboratories often struggle to meet the financial and operational burden associated with regulatory adherence. As regulatory frameworks evolve to address emerging diagnostic technologies, laboratories must continuously update procedures and equipment to remain compliant within the healthcare system.

Opportunities

Expansion of Genomic Testing and Personalized Medicine Diagnostics

Personalized medicine is rapidly transforming healthcare delivery across Italy, creating new opportunities for diagnostic laboratories to expand specialized testing capabilities. Genomic testing enables clinicians to analyze patient genetic profiles to guide targeted treatment strategies in oncology and rare disease management. Diagnostic laboratories increasingly collaborate with pharmaceutical companies and biotechnology firms to develop companion diagnostic tests supporting personalized therapies. Expansion of genomic testing services also enables laboratories to offer advanced screening programs for hereditary diseases and genetic risk assessment. Hospitals and specialized diagnostic centers are investing in next generation sequencing technologies capable of performing large scale genomic analysis efficiently. These developments enable laboratories to diversify diagnostic service offerings while addressing growing clinical demand for personalized healthcare solutions. The integration of genomic data with clinical diagnostics enhances patient outcomes and strengthens laboratory roles within precision medicine ecosystems.

Digital Laboratory Integration and Artificial Intelligence Diagnostics

Digital transformation within healthcare systems is creating opportunities for diagnostic laboratories to implement advanced data analytics and artificial intelligence technologies. AI-based diagnostic algorithms assist laboratory professionals in interpreting complex diagnostic data, improving test accuracy and efficiency. Integration of laboratory information systems with hospital electronic health records enables seamless sharing of diagnostic results across healthcare networks. Automation technologies reduce manual processing and enhance workflow efficiency in high volume diagnostic laboratories. Digital pathology platforms also enable remote diagnostic interpretation by specialized pathologists, improving diagnostic accessibility across different regions. These technological innovations help laboratories manage increasing testing demand while maintaining high quality diagnostic performance. Investment in digital laboratory infrastructure is expected to enhance operational scalability and improve diagnostic turnaround times across Italy’s healthcare ecosystem.

Future Outlook

The Italy diagnostic laboratories market is expected to experience steady expansion driven by growing healthcare demand and technological innovation in laboratory diagnostics. Increasing adoption of molecular testing, automation technologies, and digital pathology systems will enhance laboratory efficiency and testing capabilities. Healthcare policy initiatives supporting preventive healthcare and early disease detection will continue to expand diagnostic testing demand. Integration of artificial intelligence in laboratory workflows and expansion of genomic diagnostics are also expected to strengthen future laboratory services. Continued investment in laboratory infrastructure and advanced diagnostic technologies will support sustainable market development.

Major Players

- SynlabGroup

- Cerba HealthCare

- Eurofins Scientific

- Unilabs

- Diagnostica Medica

- Lifebrain Group

- Humanitas Diagnostic Center

- Istituto Auxologico Italiano

- Bianalisi Group

- Gruppo San Donato Diagnostics

- Laboratorio Analisi Fleming

- Diagnostica De Mori

- CDI Centro Diagnostico Italiano

- Bios SpA Diagnostics

- Synlab Italia

Key Target Audience

- Pharmaceutical companies

- Biotechnology companies

- Healthcare providers and hospital networks

- Diagnostic equipment manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare insurance providers

Research Methodology

Step 1: Identification of Key Variables

Primary variables influencing the Italy diagnostic laboratories market were identified through healthcare infrastructure analysis, diagnostic testing demand patterns, regulatory frameworks, and laboratory technology adoption. These variables established the core structure for evaluating diagnostic laboratory market performance.

Step 2: Market Analysis and Construction

Market size evaluation involved integrating healthcare expenditure statistics, laboratory testing volumes, and diagnostic service utilization across hospital and independent laboratories. Public healthcare data and industry reports were used to construct an accurate representation of the market structure.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including clinical laboratory professionals, healthcare administrators, and diagnostic technology specialists were consulted to validate market assumptions. Their insights helped confirm demand drivers, operational challenges, and emerging technological trends influencing laboratory services.

Step 4: Research Synthesis and Final Output

Collected data was synthesized using qualitative and quantitative analytical methods to produce a structured market report. Cross validation ensured consistency across healthcare expenditure datasets, laboratory service statistics, and diagnostic technology adoption trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising Prevalence of Chronic Diseases and Preventive Screening Programs

Government Investments in Public Healthcare Diagnostics Infrastructure

Technological Advancements in Molecular and Genetic Testing - Market Challenges

High Cost of Advanced Diagnostic Equipment and Testing Technologies

Regulatory Compliance and Quality Accreditation Requirements

Shortage of Skilled Laboratory Technicians and Specialists - Market Opportunities

Expansion of Personalized Medicine and Genomic Testing

Growth of Preventive Health Screening Programs

Integration of AI and Automation in Laboratory Diagnostics - Trends

Increasing Adoption of Molecular and Genetic Diagnostics

Automation and Digitalization of Laboratory Workflows - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Testing

Molecular Diagnostics Testing

Immunoassay Testing

Hematology Testing

Microbiology Testing - By Platform Type (In Value%)

Hospital-Based Diagnostic Labs

Independent Diagnostic Laboratories

Point-of-Care Diagnostic Platforms

Mobile Diagnostic Units - By Fitment Type (In Value%)

Standalone Laboratory Facilities

Hospital-Integrated Laboratories

Diagnostic Laboratory Networks

Public Health Laboratory Centers - By End User Segment (In Value%)

Hospitals

Diagnostic Centers

Research and Academic Institutes

- Market Share Analysis

- Cross Comparison Parameters (Test Portfolio Breadth, Laboratory Network Coverage, Technology Adoption Level, Accreditation and Quality Standards, Turnaround Time Efficiency, Pricing Structure, Partnership with Hospitals)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Synlab Italia

Cerba HealthCare Italia

Unilabs Italia

Eurofins Scientific

Bio-Reference Laboratories

Laboratory Corporation of America Holdings

Quest Diagnostics

DiaSorin

Roche Diagnostics

Abbott Diagnostics

Siemens Healthineers Diagnostics

Randox Laboratories

Biogroup Laboratory

Artemisia Lab

Fujirebio Diagnostics

- Hospitals Expanding In-House Diagnostic Testing Capabilities

- Independent Diagnostic Chains Scaling Regional Laboratory Networks

- Research Institutes Increasing Use of Advanced Molecular Diagnostics

- Growing Demand for Preventive Screening Among Patients

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now