Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Italy energy storage market is expected to experience significant growth, with an estimated market size of USD ~ billion, driven by the increasing demand for clean energy, the adoption of renewable sources, and the integration of energy storage systems into the national grid. The growth is primarily fueled by Italy’s strong regulatory push to meet renewable energy goals and technological advancements in energy storage systems. With continued investments in energy transition projects, the market is projected to expand rapidly over the coming years.

Italy, being a leader in renewable energy, has witnessed significant dominance in the energy storage market, driven by a favorable regulatory environment, government incentives, and high levels of investments in clean energy infrastructure. The country is one of the largest producers of renewable energy in Europe, with solar and wind energy contributing significantly to its power grid. Regional initiatives in areas such as Lombardy and Sicily have contributed to the acceleration of energy storage technologies.

Market Segmentation

By Product Type:

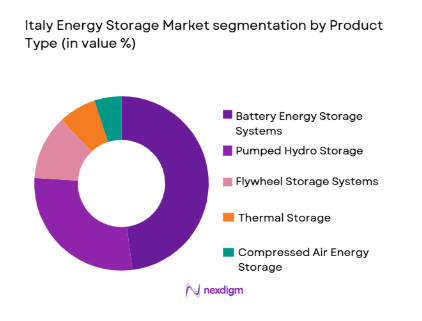

Italy energy storage market is segmented by product type into battery energy storage systems (BESS), pumped hydro storage, flywheel storage systems, thermal storage, and compressed air energy storage (CAES). Recently, BESS has gained significant market share due to factors such as technological advancements in lithium-ion batteries, declining costs, and the need for efficient, scalable storage solutions. The widespread adoption of battery energy storage systems in residential, commercial, and utility-scale applications has propelled this sub-segment’s dominance in the Italian market, driven by both government incentives and high demand for grid stability and energy independence.

By End-User:

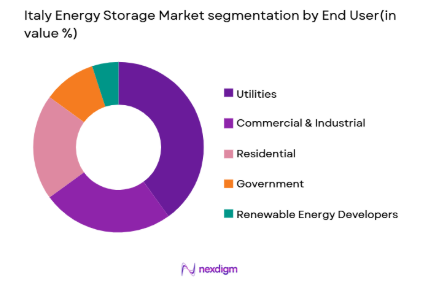

Italy energy storage market is segmented by end-user into utilities, commercial and industrial, residential, government, and renewable energy developers. Recently, utilities have dominated the market share due to the need for grid modernization, storage to balance supply-demand fluctuations, and enhance energy security. Utility companies are heavily investing in large-scale energy storage projects to support renewable integration, stabilize the grid, and meet regulatory requirements for energy storage capacity. The segment has been rapidly expanding as part of Italy’s green energy initiatives, which emphasize a clean and reliable energy mix.

Competitive Landscape

The Italy energy storage market is competitive, with a mix of international and local players driving technological innovation and project deployment. Major players are focusing on strategic partnerships, acquisitions, and investments to secure a foothold in the growing market. The consolidation trend has intensified as larger companies integrate storage solutions with their renewable energy portfolios. These companies are working on improving storage efficiency and cost-effectiveness, while also aiming to comply with Italy’s evolving renewable energy standards.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Market-Specific Parameter |

| Enel X | 2008 | Rome, Italy | ~ | ~ | ~ | ~ | ~ |

| E.ON | 2000 | Essen, Germany | ~ | ~ | ~ | ~ | ~ |

| A2A Energia | 2008 | Milan, Italy | ~ | ~ | ~ | ~ | ~ |

| Siemens Energy | 1847 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| BYD Company Limited | 1995 | Shenzhen, China | ~ | ~ | ~ | ~ | ~ |

Italy Energy Storage Market Analysis

Growth Drivers

Government Support for Renewable Integration:

The Italian government has placed significant emphasis on expanding renewable energy, which in turn is driving demand for energy storage systems. As part of its Green Deal strategy, Italy is pushing to meet ambitious renewable energy targets, and energy storage solutions are crucial for balancing intermittent renewable energy sources like solar and wind. Through various financial incentives, tax credits, and direct investments in renewable energy projects, the government has created a conducive environment for energy storage growth. The ongoing initiatives at both local and national levels, including smart grid infrastructure and storage facilities, have further spurred the adoption of storage technologies across industries and residential areas. Additionally, the European Union’s push for renewable integration also plays a pivotal role in shaping the future of Italy’s energy storage landscape.

Technological Advancements in Energy Storage:

Technological progress in energy storage systems has been a key growth driver for the market in Italy. Innovations in lithium-ion batteries, flow batteries, and other advanced storage technologies have made energy storage solutions more efficient and cost-effective. With continuous reductions in battery costs, particularly for lithium-ion batteries, energy storage is becoming increasingly accessible to both large-scale utility applications and residential users. These advancements are enhancing the efficiency and durability of storage systems, making them a more attractive option for consumers and businesses alike. Moreover, the increasing ability to store energy for longer periods without significant losses has contributed to the scalability of these systems. These innovations continue to meet the growing demand for sustainable and reliable energy storage across sectors in Italy.

Market Challenges

High Initial Capital Investment:

One of the major challenges facing the Italy energy storage market is the high upfront cost associated with deploying energy storage systems. Although the cost of energy storage technologies has decreased in recent years, the initial investment for both residential and commercial storage solutions remains a significant barrier for many. Energy storage systems, especially large-scale solutions, require substantial capital expenditures, which can be a hurdle for widespread adoption. Although the cost reduction trend continues, consumers and businesses are still hesitant to make large investments without guaranteed returns, such as through cost savings on energy bills or government incentives. The high capital cost remains a crucial challenge to accelerating the deployment of energy storage systems in Italy.

Regulatory and Policy Barriers:

Despite the favorable outlook for energy storage, regulatory and policy barriers pose significant challenges to market growth in Italy. Inconsistent regulations across regions, slow implementation of supportive policies, and lack of standardization are among the key hurdles facing energy storage developers. Regulatory frameworks around energy storage systems, especially regarding grid access, certification processes, and integration with renewable energy projects, remain underdeveloped or fragmented. As the market grows, more cohesive and supportive regulatory policies are needed to ensure the seamless integration of energy storage technologies into Italy’s energy infrastructure. Delays in policy implementation and grid access restrictions also slow down the pace at which energy storage solutions can be deployed effectively across the country.

Opportunities

Growth of Electric Vehicle Adoption:

The growing adoption of electric vehicles (EVs) presents significant opportunities for energy storage solutions in Italy. As the government and private sector increase investments in EV infrastructure and incentives for electric vehicle purchases, the demand for energy storage systems has surged. With more EVs on the road, both charging infrastructure and grid stability require substantial energy storage solutions to manage peak demand, store excess energy, and stabilize the grid. Energy storage systems can play a crucial role in supporting the charging infrastructure by ensuring a stable power supply and increasing the efficiency of charging stations. The integration of energy storage with EV infrastructure is an opportunity for energy storage developers to tap into a rapidly expanding market.

Expansion of Renewable Energy Projects:

As Italy continues to expand its renewable energy sector, the demand for energy storage solutions is expected to grow significantly. The increasing capacity of solar and wind energy projects, combined with Italy’s ambitious energy goals, creates opportunities for energy storage systems to help manage renewable energy intermittency. In particular, the need for storage solutions to balance supply and demand during periods of high renewable generation will drive market growth. Energy storage systems enable renewable energy producers to store excess energy generated during peak periods for later use, ensuring a reliable power supply even when renewable energy production is low. This expansion is likely to create a vast array of opportunities for storage companies to cater to the needs of the rapidly growing renewable energy market in Italy.

Future Outlook

The future of the Italy energy storage market is bright, with substantial growth expected over the next five years. The combination of technological advancements, continued governmental support for renewable energy, and increasing investments in grid modernization will fuel the demand for energy storage systems. As Italy works toward meeting its renewable energy targets, the adoption of energy storage will continue to rise across residential, commercial, and industrial sectors. The market will also benefit from the ongoing development of smart grid solutions and advancements in long-duration storage technologies, making energy storage an integral part of Italy’s clean energy future.

Major Players

- Enel X

- E.ON

- A2A Energia

- Siemens Energy

- BYD Company Limited

- Engie

- General Electric

- Schneider Electric

- ABB Group

- Tesla

- Wärtsilä

- Fluence Energy

- LG Chem

- Panasonic

- Vestas

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Utilities and power producers

- Commercial and industrial businesses

- Residential consumers

- Renewable energy developers

- Energy storage technology manufacturers

- Electric vehicle infrastructure providers

Research Methodology

Step 1: Identification of Key Variables

Understanding critical parameters, including technological trends, regulatory frameworks, and market dynamics.

Step 2: Market Analysis and Construction

Comprehensive market analysis based on historical data and trends.

Step 3: Hypothesis Validation and Expert Consultation

Engaging with industry experts and validating assumptions using empirical data.

Step 4: Research Synthesis and Final Output

Synthesizing data into actionable insights and compiling the final research report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Support for Renewable Integration

Technological Advancements in Energy Storage

Increasing Demand for Grid Stability

Rising Investment in Energy Transition Projects

Declining Battery Costs and Efficiency Gains - Market Challenges

High Initial Capital Investment

Regulatory and Policy Barriers

Energy Storage System Lifetime and Degradation

Limited Availability of Raw Materials

Lack of Sufficient Infrastructure - Market Opportunities

Growth of Electric Vehicle Adoption

Expansion of Renewable Energy Projects

Advancements in Long-Duration Storage Technologies - Trends

Rise in Hybrid and Integrated Storage Solutions

Focus on Energy Storage in Smart Grids

Technological Innovations in Solid-State Batteries

Increasing Use of AI and Machine Learning for Energy Storage

Government Incentives for Clean Energy Storage Systems - Government Regulations & Defense Policy

Renewable Energy Integration Standards

Battery Recycling and Disposal Regulations

Support for Energy Storage in National Energy Plans - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Energy Storage Systems

Thermal Energy Storage Systems

Flywheel Energy Storage Systems

Pumped Hydro Storage Systems

Compressed Air Energy Storage Systems - By Platform Type (In Value%)

Grid-Connected Systems

Off-Grid Systems

Hybrid Systems

Commercial Storage Systems

Residential Storage Systems - By Fitment Type (In Value%)

On-site Solutions

Off-site Solutions

Mobile Solutions

Distributed Systems

Centralized Systems - By EndUser Segment (In Value%)

Utility Companies

Commercial & Industrial Users

Residential Consumers

Government & Public Sector

Renewable Energy Projects - By Procurement Channel (In Value%)

Direct Procurement

Third-party Procurement

Distributors & Resellers

Online Platforms

Bidding Systems - By Material / Technology (In Value%)

Lithium-ion Batteries

Lead-acid Batteries

Sodium-sulfur Batteries

Flow Batteries

Thermal Storage Materials

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material/Technology, Government Support, Market Demand, Cost Efficiency, Technological Innovation)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Enel X

E.ON

A2A Energia

Siemens Energy

Toshiba Corporation

LG Chem

Sungrow Power Supply

BYD Company Limited

TotalEnergies

SAFT Batteries

VARTA AG

Eos Energy Enterprises

Fluence Energy

Nidec Corporation

Bloom Energy

- Growing Adoption of Residential Energy Storage

- Increasing Investments in Industrial Energy Storage Solutions

- Utilities’ Focus on Storage for Grid Optimization

- Renewable Energy Sector Driving Storage Demand

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now