Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The home finance market in Italy has seen substantial growth, driven by factors such as an increasing demand for residential property, growing disposable income, and favorable financing conditions. The market is valued at approximately USD ~ billion in 2024, with mortgage loans, home equity, and refinancing options being the most sought-after products. The government’s continued focus on promoting homeownership and favorable interest rates have spurred consumer demand, while the overall positive economic sentiment has supported growth in the sector.

Key cities such as Rome, Milan, and Turin are prominent in the home finance market due to their economic development and high property values. These cities, along with the surrounding metropolitan areas, benefit from extensive infrastructure development, increased demand for real estate, and a robust presence of financial institutions. They have become key hubs in the home finance sector, with significant investments directed toward both urban and suburban housing developments.

Market Segmentation

By Product Type

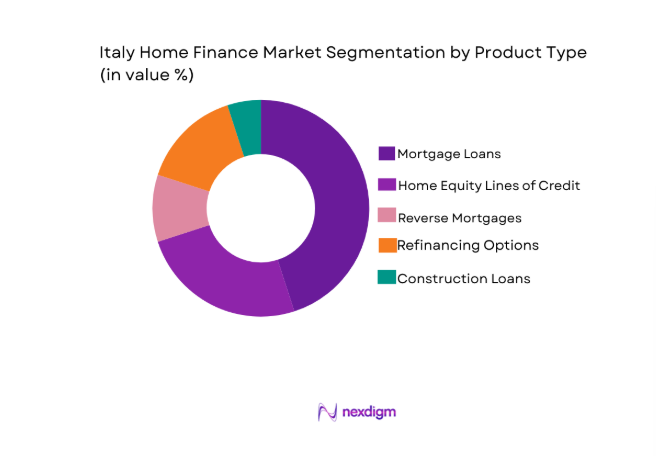

Italy’s home finance market is segmented by product type into mortgage loans, home equity lines of credit (HELOC), reverse mortgages, refinancing options, and construction loans. The dominant sub-segment is mortgage loans, as they cater to a large portion of homebuyers and are backed by favorable interest rates. Mortgage loans are highly sought after, with low-interest-rate offerings attracting first-time buyers and existing homeowners seeking to purchase or refinance homes. These products are bolstered by the widespread availability of digital lending platforms, which provide greater accessibility to consumers seeking home financing.

By Platform Type

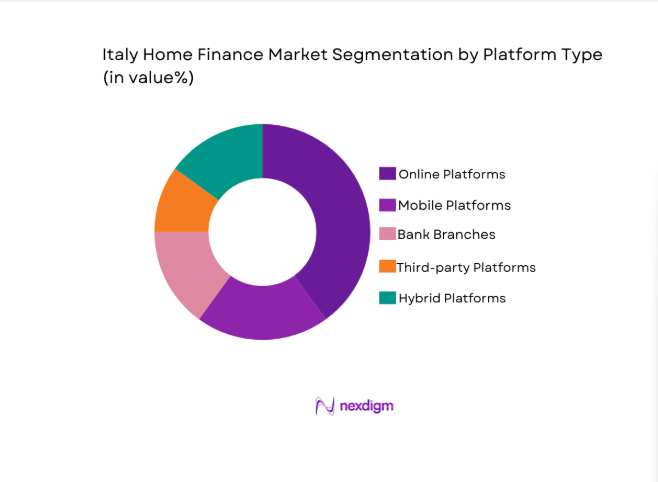

The home finance market is segmented by platform type into online platforms, mobile platforms, bank branches, third-party platforms, and hybrid platforms. Online platforms dominate this market segment due to their convenience, competitive pricing, and ease of access. Digitalization has been a key factor in making home financing more accessible, with many lenders focusing on providing seamless online loan application processes, reducing paperwork and time. Online platforms are leading the charge as the preferred mode for home finance due to the growing reliance on digital services among tech-savvy consumers.

Competitive Landscape

The home finance market in Italy is characterized by a competitive landscape with a mix of traditional banks, digital platforms, and fintech startups. Major players continue to consolidate their positions through mergers, acquisitions, and partnerships, leveraging technology to offer more personalized services. Larger institutions dominate, but digital lenders and challenger banks are gaining market share due to their agility and ability to cater to underserved segments of the population.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) |

| Intesa Sanpaolo | 1998 | Turin, Italy | ~ | ~ | ~ | ~ |

| UniCredit | 1998 | Milan, Italy | ~ | ~ | ~ | ~ |

| Banca Mediolanum | 1982 | Milan, Italy | ~ | ~ | ~ | ~ |

| Poste Italiane | 1997 | Rome, Italy | ~ | ~ | ~ | ~ |

| Banco di Sardegna | 1953 | Cagliari, Italy | ~ | ~ | ~ | ~ |

Italy Home Finance Market Analysis

Growth Drivers

Government Initiatives

Government initiatives aimed at boosting homeownership and making housing affordable have significantly driven growth in Italy’s home finance market. Programs such as first-time homebuyer incentives, tax breaks, and subsidies on mortgage rates have played a key role in encouraging more consumers to invest in homes. These policies, combined with low-interest rates and government-backed loans, have been instrumental in pushing home finance growth by reducing the barriers to entry for potential homeowners. The government’s push to make homeownership more attainable, especially in urban areas, continues to stimulate demand for home finance products, particularly mortgages. Additionally, fiscal incentives aimed at energy-efficient homes and sustainable real estate development have contributed to market expansion by incentivizing more buyers to invest in housing projects that qualify for eco-friendly financing. The expansion of government programs has enabled a broader demographic to access financial products that were previously out of reach, ensuring a steady increase in market size.

Technological Advancements

Technological advancements, particularly in digital and mobile banking, have dramatically altered the home finance market in Italy. The rise of online mortgage platforms, mobile apps, and AI-driven loan processing systems has made it easier for consumers to access home financing. Digital platforms now allow customers to apply for loans and track their mortgage applications at the click of a button, reducing traditional barriers such as long wait times, paperwork, and lack of accessibility. The growing penetration of smartphones and the internet in Italy has further enabled consumers to utilize digital channels for home financing. Lenders are also using artificial intelligence to provide better credit assessments, ensuring faster approval times and reducing risks for both consumers and financial institutions. These technological innovations not only streamline the lending process but also reduce operational costs, providing more competitive rates for consumers. As the fintech sector continues to evolve, new opportunities for digital-first products will likely lead to even more market expansion.

Market Challenges

Economic Instability

Economic instability has been one of the biggest challenges facing the Italian home finance market. Uncertainty surrounding political decisions, the European economy, and consumer confidence has resulted in fluctuations in housing demand and mortgage rates. While Italy has seen stable growth in recent years, the broader macroeconomic environment can lead to periods of stagnation or downturns, affecting demand for home loans. The global financial crisis, though a past event, still casts a shadow over the sector, causing lingering hesitancy among consumers when it comes to borrowing large sums of money. Additionally, the Italian banking sector has faced issues related to non-performing loans, which could further complicate credit availability for consumers. Economic crises or political changes can affect the entire financing ecosystem, including the interest rates offered, loan approval processes, and overall consumer sentiment, which in turn creates challenges for both lenders and borrowers alike.

Regulatory Barriers

Regulatory barriers and challenges are another significant factor affecting the home finance market in Italy. The regulatory framework governing the home finance sector can be complex and often requires lenders to comply with various EU and national-level rules that may affect their ability to offer flexible products to consumers. Changes in regulations related to mortgage rates, lending limits, and consumer protection laws can also introduce uncertainties for financial institutions. Additionally, the process of securing a mortgage in Italy can involve significant bureaucracy, leading to long wait times for approval. Stringent lending criteria and documentation requirements, while protecting consumers, can also be a deterrent for many potential homebuyers. For lenders, navigating these regulatory hurdles can be costly and time-consuming, reducing their ability to be competitive. As the market continues to evolve, financial institutions must adapt to changing regulations while maintaining their competitive edge.

Opportunities

Sustainability and Green Financing

One of the key opportunities in Italy’s home finance market lies in the growing demand for sustainable and energy-efficient homes. With increasing awareness of environmental concerns, many homebuyers are now seeking properties that comply with green standards. The Italian government has provided significant incentives for energy-efficient housing, including subsidies for homebuyers who invest in sustainable properties. This trend is driving demand for green mortgages and eco-friendly financing options. Lenders are increasingly offering home finance products that cater to buyers seeking environmentally friendly housing solutions, often at competitive rates. The growing popularity of sustainable construction and retrofitting of existing homes also offers a lucrative opportunity for home finance providers. By offering financing for sustainable housing, lenders not only tap into a growing market but also align themselves with global trends focused on sustainability, reducing the carbon footprint of the housing sector. Financial products tailored to this niche will likely see higher demand as both consumers and developers prioritize sustainability.

Expansion in Digital Platforms

The rapid expansion of digital platforms presents a significant opportunity for Italy’s home finance market. The digitalization of financial services has created more opportunities for online mortgage providers to cater to a tech-savvy generation of consumers who prioritize convenience. Digital platforms reduce operational costs, increase accessibility for consumers, and streamline the mortgage application process. As the Italian population becomes more digitally inclined, lenders have the opportunity to expand their reach through mobile apps, digital marketplaces, and peer-to-peer lending platforms. These platforms provide a level of flexibility and customer service that traditional banks cannot always match. Digital-first platforms allow customers to compare mortgage rates, access financial products, and apply for loans remotely, creating a more seamless experience for potential homebuyers. This transformation is poised to capture a large share of the home finance market, especially as younger generations, who are more familiar with digital technologies, increasingly enter the housing market.

Future Outlook

The future outlook for Italy’s home finance market appears positive, with continued growth driven by government support for housing initiatives and the increasing digitization of the sector. Technological developments such as AI-powered lending, blockchain for secure transactions, and mobile apps will transform the home finance landscape, making it more accessible to a broader demographic. Increased demand for sustainable homes and green financing products will likely drive further growth, while regulatory support for energy-efficient housing will help shape the market. Lenders will continue to innovate, with an increasing emphasis on digital platforms that provide faster, more efficient services. Additionally, as the economy stabilizes, consumer confidence in borrowing will likely increase, contributing to the overall expansion of the home finance market in Italy over the next five years.

Major Players

- Intesa Sanpaolo

- UniCredit

- Banca Mediolanum

- Poste Italiane

- Banco di Sardegna

- Credito Emiliano

- Banca Popolare di Sondrio

- Banca Nazionale del Lavoro

- Deutsche Bank

- Santander Consumer Bank

- ING Italia

- Banca Carige

- UBI Banca

- BP Sella

- FinecoBank

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Real estate developers

- Homebuyers and property investors

- Financial institutions

- Mortgage brokers

- Technology companies offering financial solutions

- Retail banks

Research Methodology

Step 1: Identification of Key Variables

Identification of critical market variables, including product types, platforms, and consumer preferences, to structure the research.

Step 2: Market Analysis and Construction

Analyzing market trends, consumer behavior, and key drivers to develop a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Validating research hypotheses through interviews with industry experts and primary data collection.

Step 4: Research Synthesis and Final Output

Synthesizing all collected data into a final report with actionable insights and market projections.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Property Prices and Demand for Homeownership

Increase in Housing Construction Projects

Government Incentives for Homebuyers

Technological Advancements in Mortgage Processing

Rising Affordability of Home Loan Products - Market Challenges

High Interest Rates and Borrowing Costs

Regulatory Constraints and Compliance Challenges

Economic Uncertainty Affecting Consumer Confidence

Rising Property Taxes

Fragmented Market Players and Lack of Unified Platforms - Market Opportunities

Growth in Green and Sustainable Housing Loans

Expansion of Digital and Mobile Platforms for Financing

Integration of Blockchain for Secure Transactions - Trends

Digitization of Mortgage and Financing Processes

Growth of Online and Mobile Lending Platforms

Increased Use of Artificial Intelligence in Credit Scoring

Rise of Sustainable and Green Mortgage Options

Focus on Cross-border Mortgage Solutions - Government Regulations & Defense Policy

Regulation of Mortgage Interest Rates

Government Tax Incentives for First-time Homebuyers

Regulatory Framework for Sustainable Housing Projects - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Mortgage Loans

Home Equity Lines of Credit (HELOC)

Reverse Mortgages

Refinancing Options

Construction Loans - By Platform Type (In Value%)

Online Platforms

Mobile Platforms

Bank Branches

Third-party Platforms

Hybrid Platforms - By Fitment Type (In Value%)

New Home Financing

Refinancing

Home Improvement Financing

Second Mortgages

Investment Property Financing - By End User Segment (In Value%)

Homebuyers

Real Estate Investors

Homeowners

Commercial Property Investors

Government Programs - By Procurement Channel (In Value%)

Direct Banks

Mortgage Brokers

Online Lenders

Peer-to-Peer Platforms

Government Programs

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intesa Sanpaolo

UniCredit

Banca Nazionale del Lavoro (BNL)

Banco di Sardegna

UBI Banca

Poste Italiane

Banca Mediolanum

Credito Emiliano

Banca Popolare di Sondrio

Santander Consumer Bank

Deutsche Bank

CheBanca!

Banca Carige

ING Italia

Sella Group

- Increasing Demand for Flexible Mortgage Products

- Homeowners’ Shift Toward Refinancing Options

- Real Estate Investors Seeking Financing Alternatives

- Government Programs Focused on Homeownership Accessibility

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now