Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Italy Last-Mile Delivery Market generated approximately USD ~ billion in logistics revenue, supported by expanding e-commerce distribution networks and national courier infrastructure. Data reported by Eurostat and the Italian Ministry of Infrastructure and Transport highlights strong parcel delivery activity driven by online retail platforms and omnichannel fulfillment systems. Logistics providers continue investing in automated parcel sorting hubs, digital route optimization technologies, and electric delivery fleets that improve delivery efficiency and enable large-scale parcel distribution across metropolitan and regional logistics corridors.

Major logistics centers including Milan, Rome, Turin, and Bologna dominate last-mile delivery operations due to their concentration of retail fulfillment warehouses, parcel distribution hubs, and transportation infrastructure. Milan serves as the primary logistics gateway supporting nationwide parcel circulation, while Rome functions as a major consumption hub generating strong demand for courier services. Northern industrial regions such as Lombardy and Emilia-Romagna sustain dense logistics ecosystems supported by advanced highway connectivity, large warehouse clusters, and strong integration between freight forwarding operations and urban parcel delivery systems.

Market Segmentation

By Product Type

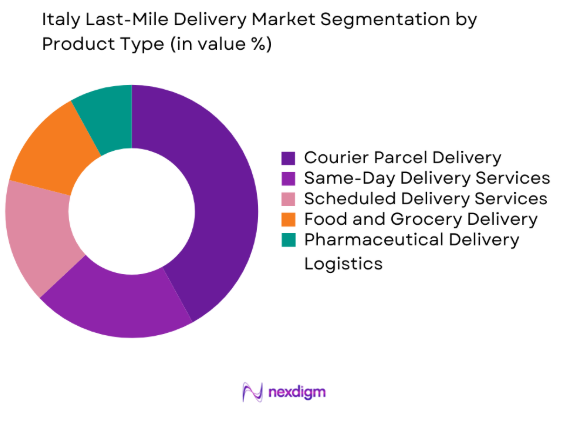

Italy Last-Mile Delivery Market market is segmented by product type into courier parcel delivery, same-day delivery services, scheduled delivery services, food and grocery delivery, and pharmaceutical delivery logistics. Recently, courier parcel delivery has a dominant market share due to factors such as widespread e-commerce fulfillment requirements, strong national courier infrastructure, and integration with automated parcel sorting systems. Large logistics operators handle extremely high parcel volumes through centralized distribution hubs that support rapid order fulfillment and efficient transportation to urban delivery networks. Retailers increasingly depend on parcel delivery partners to manage nationwide consumer shipments across fashion, electronics, home goods, and household products. Courier services also benefit from strong integration with cross-border logistics networks connecting Italy with major European distribution markets. Continuous expansion of omnichannel retail strategies strengthens demand for courier delivery systems capable of managing high parcel volumes across multiple distribution points.

By Platform Type

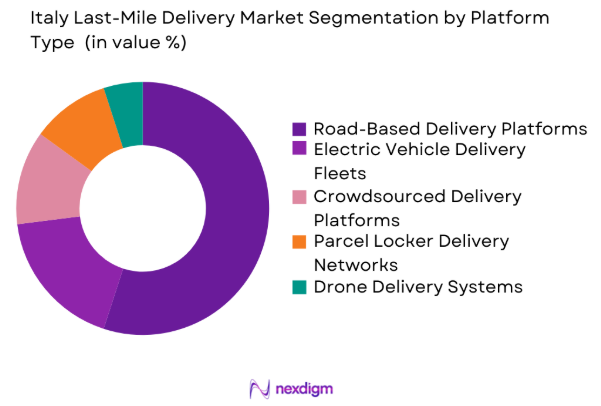

Italy Last-Mile Delivery Market market is segmented by platform type into road-based delivery platforms, electric vehicle delivery fleets, crowdsourced delivery platforms, parcel locker delivery networks, and drone-enabled delivery systems. Recently, road-based delivery platforms have a dominant market share due to factors such as established courier infrastructure, extensive road transportation networks, and compatibility with urban distribution requirements. Logistics companies rely heavily on vans and light commercial vehicles capable of transporting parcels between sorting hubs and final delivery destinations. Italy’s dense highway system and metropolitan logistics corridors support efficient vehicle-based parcel distribution. Courier operators also deploy advanced route optimization software that improves vehicle utilization and delivery performance. Road transport remains the most scalable logistics platform because it integrates seamlessly with existing parcel hubs and national distribution infrastructure.

Competitive Landscape

The Italy Last-Mile Delivery Market is characterized by a moderately consolidated structure dominated by several global logistics corporations and established domestic courier operators. Leading companies compete through nationwide distribution infrastructure, advanced parcel sorting facilities, digital logistics platforms, and large vehicle fleets. Continuous investments in automated logistics hubs, real-time shipment tracking technologies, and electric delivery vehicles strengthen operational efficiency and customer service capabilities. Strategic partnerships between e-commerce platforms and courier operators also enhance distribution capacity and accelerate parcel delivery across urban and suburban markets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet |

| Poste Italiane | 1862 | Rome, Italy | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta, USA | ~ | ~ | ~ | ~ | ~ |

| FedEx | 1971 | Memphis, USA | ~ | ~ | ~ | ~ | ~ |

| BRT Corriere Espresso | 1928 | Milan, Italy | ~ | ~ | ~ | ~ | ~ |

Italy Last-Mile Delivery Market Analysis

Growth Drivers

Expansion of E-Commerce Distribution Networks Across Italy

The expansion of digital retail platforms across Italy significantly increases demand for efficient last-mile delivery services capable of managing large parcel volumes generated by online purchases across fashion, electronics, groceries, and consumer goods sectors. E-commerce companies depend on reliable logistics partners to transport orders from fulfillment centers to residential and commercial destinations across urban and suburban regions. Logistics operators therefore invest in automated parcel sorting hubs, advanced warehouse management systems, and high-capacity distribution centers that support large shipment volumes. Courier companies also expand delivery fleets including electric vans designed for urban logistics. Real-time tracking platforms, route optimization systems, and omnichannel retail distribution strategies further strengthen demand for advanced last-mile delivery infrastructure.

Urban Population Density and Concentrated Consumption Centers

Italy’s urban population concentration creates strong demand for last-mile delivery networks capable of managing high shipment volumes across major metropolitan regions including Milan, Rome, Turin, and Naples where consumer demand for retail goods, groceries, pharmaceuticals, and household products remains high. Urban residents increasingly rely on courier services as digital retail platforms provide convenient access to everyday purchases without visiting physical stores. Logistics companies therefore expand metropolitan delivery infrastructure including micro-fulfillment hubs, local distribution centers, and parcel pickup points that accelerate parcel processing and distribution. Route optimization software helps delivery fleets navigate congested urban transport corridors more efficiently. Growing urban consumption and dense populations continue strengthening demand for reliable last-mile logistics systems.

Market Challenges

Urban Traffic Congestion Affecting Delivery Efficiency

Traffic congestion in major Italian cities significantly disrupts last-mile delivery operations as courier vehicles navigate crowded streets, narrow roads, and unpredictable travel conditions while meeting strict delivery timelines required by e-commerce retailers and consumers. Cities including Rome, Milan, and Naples experience heavy traffic volumes that slow delivery fleets and increase logistics costs. Peak commuting hours further intensify congestion, making consistent transit scheduling difficult for courier operators. Logistics companies deploy route optimization systems, flexible delivery windows, and smaller vehicles to manage urban mobility challenges. Historic city centers with limited road capacity further complicate distribution efficiency. Growing parcel volumes from digital retail also increase delivery vehicle presence, worsening congestion pressures across dense metropolitan logistics networks.

Rising Operational Costs for Logistics Providers

Last-mile delivery companies in Italy face increasing operational costs driven by fuel prices, vehicle maintenance, labor wages, and continuous technology investments required to support competitive logistics services. Courier operators maintain large delivery fleets that require regular servicing and replacement, increasing capital expenditure. Labor expenses also rise as logistics firms employ extensive driver and warehouse workforces to manage parcel processing and delivery operations. Investments in automated parcel sorting systems, digital logistics platforms, and route optimization technologies further add to operational spending. Environmental regulations in many Italian cities also require logistics providers to adopt electric vehicles and compliance technologies. At the same time, intense price competition from e-commerce platforms limits the ability to increase delivery charges.

Opportunities

Adoption of Electric Delivery Vehicle Fleets for Urban Logistics

The transition toward electric vehicle delivery fleets presents a major opportunity for logistics companies operating in Italy’s last-mile delivery market as environmental regulations and sustainability initiatives increasingly promote low-emission transportation across urban regions. Municipal authorities enforce low-emission zones that restrict diesel vehicles in city centers, encouraging logistics providers to adopt electric delivery vans that comply with environmental policies while maintaining service efficiency. Electric vehicles offer lower long-term operating costs because electricity is typically cheaper than conventional fuel and maintenance requirements are reduced due to simpler vehicle systems. Logistics companies are therefore expanding electric fleets supported by government incentives, improving urban distribution efficiency while reducing carbon emissions and strengthening sustainable logistics infrastructure.

Expansion of Smart Parcel Locker Networks and Alternative Delivery Points

Smart parcel locker networks create a significant opportunity for last-mile logistics providers by enabling consumers to collect deliveries from secure automated lockers located in residential areas, transport hubs, and commercial centers instead of relying on home delivery. Parcel lockers reduce failed delivery attempts when recipients are unavailable, lowering additional transportation costs for courier operators. These systems also allow logistics companies to consolidate multiple parcel deliveries at single locations, improving operational efficiency and reducing fleet travel distances across cities. E-commerce companies increasingly collaborate with logistics firms to expand locker networks that provide convenient parcel collection points. Digital notifications and mobile tracking platforms further enhance transparency and customer convenience across Italy’s growing urban delivery ecosystem.

Future Outlook

Italy’s last-mile delivery sector is expected to experience sustained expansion driven by rapid growth in digital commerce, rising consumer expectations for faster delivery services, and increasing investment in logistics technology. Automation within parcel sorting hubs and the adoption of artificial intelligence route optimization systems will improve operational productivity. Government sustainability initiatives supporting low-emission transportation will accelerate adoption of electric delivery fleets. Urban logistics infrastructure such as micro-fulfillment centers and parcel locker networks will further enhance distribution efficiency across Italian cities.

Major Players

- Poste Italiane

- DHL Supply Chain

- UPS

- FedEx

- BRT Corriere Espresso

- GLS Group

- Amazon Logistics

- DPDgroup

- Nexive

- SDA Express Courier

- Geodis

- Aramex

- XPO Logistics

- InPost

- Hermes Europe

Key Target Audience

- Logistics and supply chain companies

- Courier and parcel delivery operators

- E-commerce platform companies

- Retail distribution companies

- Transportation infrastructure providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Electric vehicle logistics fleet manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key variables including parcel shipment volumes logistics infrastructure delivery fleet size technology adoption and e-commerce transaction activity were identified through secondary research using government transport databases Eurostat logistics statistics and national commerce data.

Step 2: Market Analysis and Construction

Market size and structural framework were constructed using logistics revenue data transportation statistics and parcel distribution indicators compiled from government publications industry associations and international logistics databases.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses regarding parcel growth patterns logistics technology adoption and urban distribution infrastructure were validated through consultations with supply chain specialists logistics executives and industry analysts.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into a structured analytical framework combining transportation statistics logistics infrastructure assessments and e-commerce distribution data to produce the final market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid Expansion of E-Commerce Parcel Volumes

Urban Logistics Demand in High Population Cities

Adoption of Technology-Enabled Delivery Optimization - Market Challenges

Urban Traffic Congestion and Delivery Delays

Rising Labor and Fuel Operating Costs

Regulatory Restrictions on Urban Delivery Vehicles - Market Opportunities

Expansion of Electric Vehicle Delivery Fleets

Development of Smart Parcel Locker Networks

Integration of AI-Based Route Optimization Platforms - Trends

Growth of Same-Day and Instant Delivery Services

Adoption of Micro Fulfillment Centers in Cities

Expansion of Contactless and Smart Delivery Technologies - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Courier and Parcel Delivery Systems

On-Demand Delivery Services

Same-Day Delivery Networks

Scheduled Delivery Logistics Systems

Automated Parcel Distribution Systems - By Platform Type (In Value%)

Road-Based Delivery Platforms

Electric Vehicle Delivery Platforms

Drone Delivery Platforms

Crowdsourced Delivery Platforms

Smart Locker Delivery Platforms - By Fitment Type (In Value%)

Company-Owned Delivery Fleets

Third-Party Logistics Integrated Delivery

Hybrid Fleet Delivery Systems

Contracted Courier Delivery Networks

Technology-Enabled Micro Fulfillment Delivery - By End User Segment (In Value%)

E-Commerce Retailers

Food and Grocery Platforms

Pharmaceutical and Healthcare Distributors

Consumer Electronics Retailers

Fashion and Apparel Retailers - By Procurement Channel (In Value%)

Direct Logistics Service Contracts

E-Commerce Platform Partnerships

Retailer Fulfillment Agreements

Digital Logistics Marketplace Platforms

Third-Party Logistics Outsourcing

- Market Share Analysis

- Cross Comparison Parameters (Fleet Size, Delivery Speed, Technology Integration, Geographic Coverage, Parcel Handling Capacity, Last-Mile Infrastructure Network, Electric Vehicle Adoption, Parcel Locker Network Integration, Real-Time Tracking Capability, Delivery Cost Efficiency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Poste Italiane

DHL Supply Chain

UPS

FedEx

Amazon Logistics

GLS Group

BRT Corriere Espresso

DPDgroup

InPost

Nexive

Hermes Europe

Geodis

XPO Logistics

SDA Express Courier

Aramex

- Rising Demand from National E-Commerce Retailers

- Food Delivery Platforms Expanding Urban Delivery Networks

- Pharmaceutical Distributors Requiring Temperature Controlled Deliveries

- Retail Chains Integrating Omnichannel Distribution Systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now