Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Italy Warehousing Market demonstrates strong expansion supported by rising logistics demand and supply chain modernization. Based on a recent historical assessment, the Italy Warehousing Market reached approximately USD ~ billion in value according to the Italian Contract Logistics Observatory and national logistics infrastructure studies. Market growth is driven by expanding e-commerce fulfillment networks, modernization of distribution infrastructure, increasing cross-border trade flows through European transport corridors, and growing demand for temperature-controlled storage supporting pharmaceuticals, food logistics, and advanced manufacturing supply chains.

Major logistics clusters dominate the Italy Warehousing Market due to strategic transportation infrastructure and proximity to manufacturing hubs. Milan, Verona, Bologna, and Piacenza serve as primary warehousing centers supported by rail freight terminals, highway connectivity, and industrial production networks. Northern Italy dominates logistics development because of strong export manufacturing ecosystems and integration with European supply routes. Port cities including Genoa and Trieste also support warehousing demand due to maritime trade flows and multimodal logistics infrastructure supporting continental freight movement.

Market Segmentation

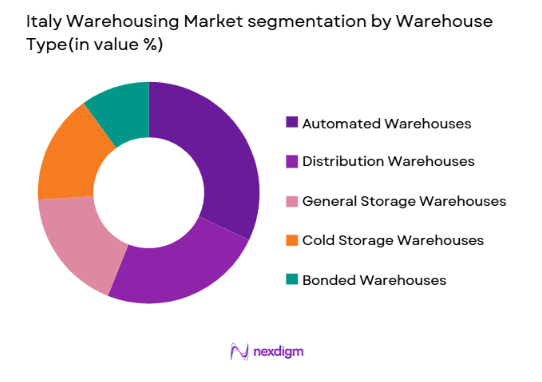

By Warehouse Type

Italy Warehousing Market is segmented by warehouse type into general storage warehouses, cold storage warehouses, automated warehouses, bonded warehouses, and distribution warehouses. Recently, automated warehouses have a dominant market share due to rising demand for high-efficiency logistics infrastructure across large fulfillment networks. Automation technologies such as robotic picking systems, automated storage and retrieval systems, and intelligent inventory management platforms improve operational productivity and reduce labor dependency in large logistics centers. Major logistics operators increasingly deploy automated facilities near industrial clusters and urban consumption centers to improve order processing speed and inventory accuracy. E-commerce fulfillment centers and retail distribution networks require rapid sorting, packaging, and dispatch operations that are difficult to achieve through conventional manual warehouse models. As logistics providers expand large distribution hubs across Northern Italy, automated warehouses enable faster throughput capacity, improved operational scalability, and greater supply chain reliability supporting national and international distribution operations.

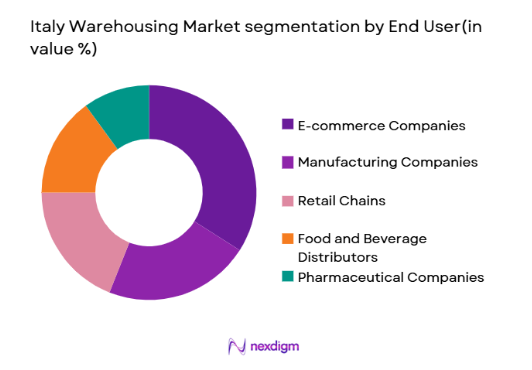

By End User

Italy Warehousing Market is segmented by end user into e-commerce companies, retail chains, manufacturing companies, pharmaceutical companies, and food and beverage distributors. Recently, e-commerce companies have a dominant market share due to rapid digital retail expansion and increasing consumer demand for fast delivery logistics. Large online marketplaces require extensive warehousing networks capable of supporting rapid order processing and last-mile delivery operations across urban population centers. Fulfillment centers designed for e-commerce operations incorporate advanced inventory management systems, automated sorting equipment, and high-capacity storage infrastructure to handle large product volumes. The rapid growth of online retail platforms operating across Italy has significantly increased demand for strategically located logistics facilities capable of supporting nationwide delivery networks. E-commerce operators continue expanding regional fulfillment hubs to improve delivery speed, optimize logistics costs, and support inventory distribution across multiple regional warehouses.

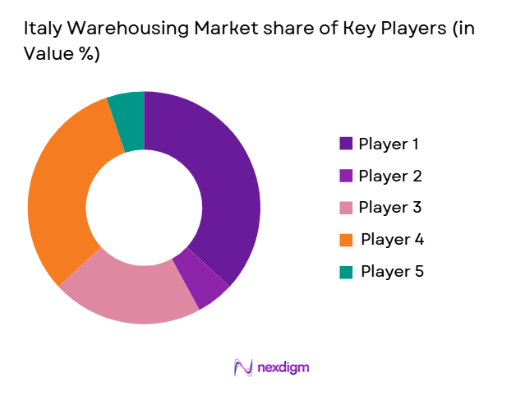

Competitive Landscape

The Italy Warehousing Market is moderately consolidated with several multinational logistics real estate developers and contract logistics providers controlling large logistics parks and automated distribution centers. Major companies expand through logistics park development, technology integration, and strategic partnerships with e-commerce and manufacturing firms. International investors increasingly acquire large logistics properties due to strong demand for modern distribution facilities across Northern Italy.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity |

| Prologis | 1983 | United States | ~ | ~ | ~ | ~ | ~ |

| Segro | 1920 | United Kingdom | ~ | ~ | ~ | ~ | ~ |

| GLP Europe | 2009 | Luxembourg | ~ | ~ | ~ | ~ | ~ |

| Panattoni Europe | 2005 | United Kingdom | ~ | ~ | ~ | ~ | ~ |

| Goodman Group | 1989 | Australia | ~ | ~ | ~ | ~ | ~ |

Italy Warehousing Market Analysis

Growth Drivers

E-commerce Expansion and Omnichannel Distribution Demand:

Rapid expansion of digital retail platforms significantly accelerates warehousing demand across the Italy Warehousing Market because e-commerce operations require large fulfillment centers capable of handling high-volume inventory storage and order processing across nationwide delivery networks. Large online retailers increasingly establish strategically located fulfillment hubs near major urban centers to improve delivery speed and reduce transportation costs associated with last-mile distribution. These logistics facilities integrate automated picking systems, warehouse management software, and robotic sorting equipment capable of processing thousands of daily orders with high operational efficiency. E-commerce companies must maintain extensive product inventories within regional warehouses to ensure product availability across multiple geographic markets. Increasing consumer expectations for same-day and next-day delivery further intensify demand for high-capacity warehousing infrastructure capable of supporting fast order processing cycles. Logistics providers also invest heavily in intelligent inventory tracking technologies and automated storage systems to improve warehouse throughput and minimize operational delays. As digital retail penetration expands across Italian consumer markets, fulfillment centers require increasingly sophisticated logistics infrastructure to manage growing product volumes and complex supply chain requirements. Retailers adopting omnichannel distribution strategies combine physical store networks with centralized warehouses to ensure seamless inventory management across multiple retail channels. Consequently, warehousing demand continues expanding as e-commerce platforms scale logistics operations across Italy.

Strategic Position of Italy in European Trade Corridors:

Italy’s geographic position within European trade corridors significantly strengthens the importance of warehousing infrastructure supporting international supply chains linking Mediterranean maritime routes with continental freight transportation networks. Major seaports including Genoa, Trieste, and La Spezia serve as gateways for containerized cargo entering Southern Europe, creating strong demand for nearby warehousing and distribution facilities supporting cargo consolidation and inland transportation. Rail freight corridors connecting Northern Italy with Germany, Switzerland, and Austria enable efficient movement of goods across major European industrial markets, which increases the strategic importance of logistics hubs located near rail terminals and intermodal transport facilities. Warehouses located near major highway networks such as the A4 and A1 corridors enable rapid distribution of imported goods to manufacturing clusters and urban consumer markets across Italy. Multinational logistics providers increasingly develop large logistics parks along these transportation corridors to support cross-border trade flows and supply chain integration with European manufacturing centers. Industrial production clusters in Lombardy, Veneto, and Emilia-Romagna require modern warehousing infrastructure capable of supporting export logistics operations and raw material storage for manufacturing processes. Logistics operators also integrate advanced supply chain technologies within warehouse facilities to manage complex international distribution networks efficiently. As international trade volumes continue expanding through Italy’s transport infrastructure, warehousing capacity remains essential for supporting efficient freight handling and distribution.

Market Challenges

High Industrial Land Costs Near Major Logistics Corridors:

One of the most significant challenges affecting the Italy Warehousing Market is the increasing cost of industrial land located near major logistics corridors and metropolitan consumption centers where demand for modern warehouse facilities remains extremely high. Logistics developers require large land parcels for constructing high-capacity distribution centers capable of supporting automated storage infrastructure and high-volume freight operations. However, limited availability of industrial land within strategic logistics locations significantly increases property acquisition costs for warehouse development projects. Developers must often compete with manufacturing facilities, infrastructure projects, and commercial real estate investors seeking land within the same transportation corridors. Zoning regulations and land-use restrictions further complicate industrial land development because many municipalities enforce strict environmental and urban planning regulations that limit large logistics facility construction. High property acquisition costs subsequently increase warehouse leasing prices, which raises operational costs for logistics providers and supply chain operators. Smaller logistics companies may struggle to secure warehouse space in premium logistics zones due to rising lease rates and property development costs. Infrastructure expansion projects and urban development pressures also reduce the availability of large industrial land parcels necessary for constructing modern logistics parks. As logistics demand continues expanding across Italy, land scarcity near major transportation hubs remains a significant structural constraint affecting warehouse development.

Labor Shortages and Logistics Workforce Constraints:

Labor shortages represent another major challenge affecting the operational efficiency of the Italy Warehousing Market because modern logistics operations require skilled personnel capable of managing complex warehouse technologies and high-volume distribution systems. Large distribution centers rely on workers responsible for inventory management, equipment operation, packaging, and transportation coordination throughout daily logistics operations. However, logistics companies increasingly report difficulty recruiting and retaining workers willing to perform physically demanding warehouse tasks within high-throughput fulfillment environments. Demographic trends including workforce aging and declining participation in manual labor occupations reduce the availability of logistics employees across major industrial regions. Additionally, warehouse operations require workers with technical expertise capable of operating automated systems, robotics equipment, and digital inventory platforms integrated into modern logistics facilities. Training new employees to manage these technologies requires additional investment and time for logistics operators. Labor shortages may reduce warehouse productivity and increase operational delays during peak distribution periods when order volumes increase significantly. Rising wage expectations also increase operating costs for logistics companies managing large warehouse networks across multiple regions. Consequently, labor availability remains a critical operational constraint for warehousing companies operating in Italy’s rapidly expanding logistics sector.

Opportunities

Development of Smart Automated Logistics Parks:

The growing adoption of warehouse automation technologies creates substantial opportunities within the Italy Warehousing Market because logistics operators increasingly prioritize intelligent logistics infrastructure capable of improving operational efficiency and reducing labor dependency. Smart logistics parks incorporate advanced technologies including robotic picking systems, automated storage and retrieval systems, artificial intelligence inventory management platforms, and Internet of Things sensors monitoring warehouse conditions and equipment performance. These integrated systems enable logistics companies to process large product volumes with greater speed, accuracy, and operational consistency compared with traditional warehouse models. Automated logistics parks also improve space utilization through vertical storage infrastructure and intelligent inventory placement algorithms that maximize warehouse capacity. Logistics developers increasingly construct large automated distribution centers capable of supporting high-throughput order processing for e-commerce platforms and multinational retail distribution networks. Smart warehousing technologies also enhance supply chain transparency by providing real-time visibility into inventory movement across distribution networks. Investors and logistics real estate developers continue expanding large logistics parks across Northern Italy where transportation infrastructure supports high-volume freight operations. As supply chains become more complex and digitalized, smart automated warehousing infrastructure will become a central component of logistics modernization.

Expansion of Temperature Controlled Supply Chain Infrastructure:

Growing demand for temperature controlled logistics infrastructure presents a major opportunity within the Italy Warehousing Market due to increasing distribution requirements for pharmaceuticals, biotechnology products, fresh food, and frozen food supply chains. Temperature sensitive products require specialized cold storage facilities capable of maintaining controlled environmental conditions throughout storage and transportation operations. Pharmaceutical manufacturers depend on temperature regulated warehouses for storing vaccines, medical supplies, and biotechnology products requiring precise thermal stability to maintain product integrity. Similarly, food distribution networks require refrigerated logistics infrastructure supporting storage and transportation of perishable goods across retail supply chains. Cold chain logistics operators invest heavily in advanced refrigeration systems, temperature monitoring technologies, and energy efficient storage facilities capable of maintaining strict regulatory compliance requirements. Expansion of pharmaceutical manufacturing and biotechnology research industries within Europe further increases demand for specialized cold storage warehouses supporting medical supply chains. Logistics providers also integrate digital temperature monitoring systems ensuring continuous product quality verification throughout distribution processes. As demand for temperature sensitive products continues expanding across healthcare and food industries, specialized cold chain warehousing infrastructure will become an increasingly important segment of the logistics market.

Future Outlook

The Italy Warehousing Market is expected to experience sustained expansion over the coming years driven by digital commerce growth, increasing supply chain complexity, and rising logistics infrastructure investments. Technological innovation including robotics, artificial intelligence, and smart warehouse management platforms will reshape operational efficiency within distribution centers. Government infrastructure initiatives supporting freight corridors and intermodal transportation networks will further strengthen logistics capacity. Growing demand for sustainable logistics facilities and energy-efficient warehouses will also influence future warehouse development strategies across Italy.

Major Players

- Prologis

- Segro

- GLP Europe

- Panattoni Europe

- Goodman Group

- Logicor

- P3 Logistic Parks

- VGP Group

- Kryalos SGR

- Prelios SGR

- Hines

- CBRE Investment Management

- Savills Investment Management

- Fercam Logistics

- DHL Supply Chain

Key Target Audience

- Logistics and Warehousing Companies

- E-commerce Companies

- Retail Distribution Companies

- Manufacturing Companies

- Pharmaceutical Distribution Companies

- Food and Beverage Logistics Companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Primary variables influencing the Italy Warehousing Market including logistics demand, infrastructure investment, warehouse capacity, automation adoption, and industrial land availability were identified through sector analysis and logistics industry data evaluation.

Step 2: Market Analysis and Construction

Comprehensive analysis was conducted using logistics infrastructure studies, industrial property databases, and trade logistics indicators to construct a detailed model describing supply chain infrastructure development and warehousing capacity trends.

Step 3: Hypothesis Validation and Expert Consultation

Market findings were validated through consultation with logistics industry experts, supply chain managers, and infrastructure analysts to confirm operational trends and verify assumptions regarding warehouse capacity expansion.

Step 4: Research Synthesis and Final Output

All research insights were consolidated into a structured analytical framework integrating logistics infrastructure data, industrial real estate trends, and supply chain development indicators to generate the final market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Ecommerce Logistics and Last Mile Delivery Networks

Growth of International Trade Through Italian Seaports

Rising Demand for Cold Chain Warehousing for Food and Pharmaceuticals

Increasing Investment in Logistics Parks and Distribution Infrastructure

Adoption of Warehouse Automation Technologies - Market Challenges

High Land Acquisition Costs Near Major Logistics Corridors

Regulatory Complexity in Zoning and Industrial Land Development

Labor Shortages in Warehouse Operations and Logistics Services

Infrastructure Bottlenecks in Road and Rail Connectivity

High Capital Investment Requirements for Automated Warehousing - Market Opportunities

Expansion of Smart Logistics Parks Near Major Seaports

Growth of Pharmaceutical and Temperature Controlled Warehousing

Development of Sustainable and Energy Efficient Warehousing Facilities - Trends

Rapid Adoption of Automated Storage and Retrieval Systems

Integration of Artificial Intelligence in Warehouse Management

Growth of Multi Tenant Logistics Hubs Near Urban Centers

Expansion of Cross Docking Facilities Supporting Fast Delivery

Increasing Deployment of Robotics Based Picking Systems - Government Regulations & Defense Policy

National Logistics Strategy Supporting Supply Chain Infrastructure

European Union Logistics and Transport Regulations

Environmental Sustainability Standards for Industrial Warehousing - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

General Storage Warehouses

Cold Storage Warehouses

Automated Warehouses

Distribution Warehouses

Bonded Warehouses - By Platform Type (In Value%)

Ecommerce Fulfillment Centers

Retail Distribution Centers

Industrial Manufacturing Warehouses

Third Party Logistics Warehouses

Cross Docking Facilities - By Fitment Type (In Value%)

Greenfield Warehouse Facilities

Brownfield Warehouse Conversions

Built To Suit Warehouses

Multi Tenant Logistics Parks

Integrated Logistics Hubs - By EndUser Segment (In Value%)

Ecommerce Companies

Retail Chains

Manufacturing Companies

Pharmaceutical and Healthcare Companies

Food and Beverage Distributors - By Procurement Channel (In Value%)

Direct Corporate Leasing

Logistics Service Provider Contracts

Third Party Logistics Partnerships

Government Supported Logistics Projects

Real Estate Developer Leasing - By Material / Technology (in Value %)

Automated Storage and Retrieval Systems

Warehouse Management Software

Robotics and Picking Automation

Smart Conveyor and Sorting Systems

IoT Enabled Inventory Tracking Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Warehouse Capacity, Automation Level, Geographic Coverage, Cold Storage Capability, Fulfillment Speed, Technology Integration, Logistics Network Connectivity, Sustainability Compliance, Client Industry Coverage, Pricing Structure)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Prologis

GLP Europe

Logicor

Segro

P3 Logistic Parks

VGP Group

Panattoni Europe

Goodman Group

Kryalos SGR

Prelios SGR

Savills Investment Management

Hines

CBRE Investment Management

DFDS Logistics

Fercam Logistics

- Ecommerce companies expanding regional fulfillment networks to support rapid delivery expectations

- Retail chains increasing demand for centralized distribution centers to optimize inventory management

- Manufacturing firms integrating warehousing facilities with production and export logistics operations

- Pharmaceutical distributors expanding temperature controlled storage capacity to meet regulatory compliance

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now