Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Japan 3PL market was valued at approximately USD ~ billion according to logistics industry data compiled from the Ministry of Land, Infrastructure, Transport and Tourism and Statista supply chain reports. Demand is primarily driven by strong manufacturing exports, complex domestic distribution networks, and rising outsourcing of logistics operations by large retailers and industrial companies. Growth is also supported by expansion of e-commerce fulfillment services, warehouse automation investments, and the need for integrated transportation, inventory management, and supply chain optimization solutions across multiple industries.

Tokyo, Osaka, Nagoya, and Yokohama function as the most dominant logistics hubs supporting the Japan 3PL market due to dense industrial clusters, advanced port infrastructure, and strong consumption demand. Tokyo benefits from large retail distribution networks and major logistics headquarters, while Osaka and Nagoya support automotive and manufacturing supply chains requiring complex contract logistics services. Yokohama and Kobe ports facilitate international cargo movements and integrated freight forwarding activities, allowing logistics providers to manage high-volume import and export flows across the country.

Market Segmentation

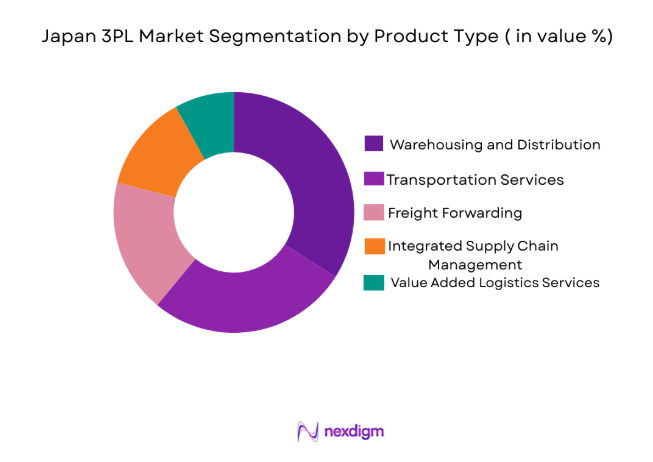

By Product Type

Japan 3PL market is segmented by product type into transportation services, warehousing and distribution, freight forwarding, value added logistics services, and integrated supply chain management. Recently, warehousing and distribution has a dominant market share due to factors such as rising e-commerce fulfillment demand, expansion of automated distribution centers, and strong domestic retail logistics requirements. Large retailers and manufacturers increasingly outsource storage, order processing, and inventory management operations to specialized logistics providers capable of handling large shipment volumes. Japan’s advanced warehouse automation, robotics adoption, and high urban consumption demand also strengthen this segment’s leadership within the market.

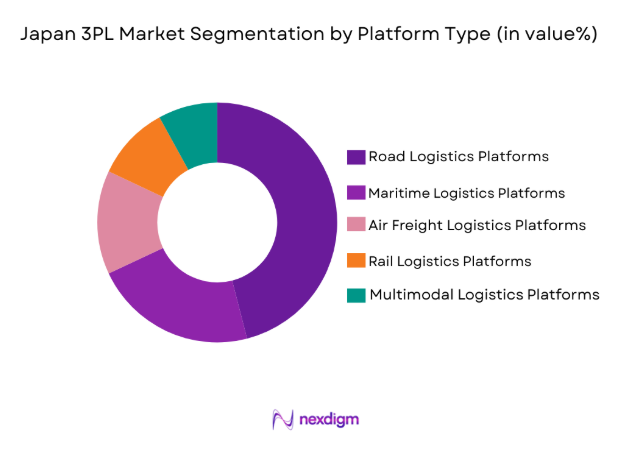

By Platform Type

Japan 3PL market is segmented by platform type into road logistics platforms, rail logistics platforms, air freight logistics platforms, maritime logistics platforms, and multimodal logistics platforms. Recently, road logistics platforms have a dominant market share due to the country’s highly developed highway infrastructure and strong domestic distribution demand across urban consumption centers. Retail deliveries, manufacturing shipments, and e-commerce parcel flows rely heavily on trucking networks connecting distribution hubs with regional markets. The flexibility, reliability, and nationwide connectivity of road transportation enable logistics companies to manage high shipment volumes efficiently across Japan.

Competitive Landscape

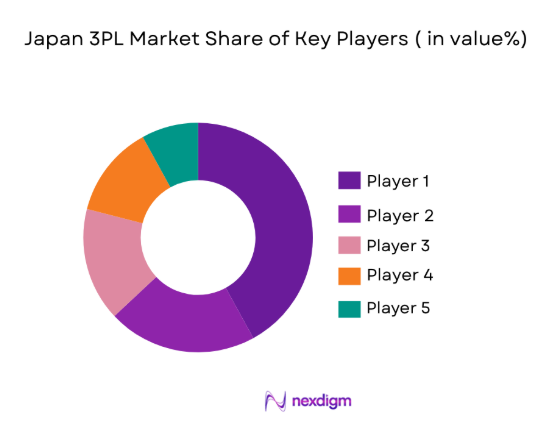

The Japan 3PL market is moderately consolidated with several large domestic logistics corporations controlling significant national distribution networks while global logistics providers compete in specialized segments such as freight forwarding and contract logistics. Major players maintain extensive warehousing infrastructure, integrated transportation networks, and advanced digital logistics technologies. Strategic partnerships with e-commerce companies and manufacturing firms strengthen their market presence while investments in automation, robotics, and data-driven supply chain platforms further enhance operational efficiency and competitive differentiation.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Logistics Infrastructure Capacity |

| Nippon Express Holdings | 1937 | Tokyo | ~ | ~ | ~ | ~ | ~ |

| Yamato Holdings | 1919 | Tokyo | ~ | ~ | ~ | ~ | ~ |

| Sagawa Express | 1957 | Kyoto | ~ | ~ | ~ | ~ | ~ |

| Kintetsu World Express | 1970 | Tokyo | ~ | ~ | ~ | ~ | ~ |

| Yusen Logistics | 1955 | Tokyo | ~ | ~ | ~ | ~ | ~ |

Japan 3PL Market Analysis

Growth Drivers

Expansion of E-commerce Fulfillment and Omnichannel Retail Logistics

Rapid growth of digital commerce platforms across Japan significantly increases demand for third party logistics services capable of managing high order volumes and complex distribution networks. Online retailers require integrated logistics solutions that include warehousing, inventory management, packaging, and last mile delivery coordination. Logistics providers therefore expand automated fulfillment centers equipped with robotics, advanced sorting systems, and real time inventory tracking technologies. Urban consumers increasingly expect faster delivery times and reliable shipment visibility through digital tracking platforms. Retail companies outsource logistics operations to specialized 3PL providers to improve operational efficiency and reduce infrastructure investment costs. The expansion of cross border e-commerce shipments also increases demand for freight forwarding and customs management services. Logistics companies invest in digital transportation management systems and route optimization technologies to manage high shipment volumes efficiently. As e-commerce penetration continues expanding within urban and regional markets, third party logistics providers become critical infrastructure supporting national retail distribution networks.

Manufacturing Supply Chain Outsourcing and Industrial Logistics Integration

Japan’s large manufacturing sector increasingly relies on specialized logistics providers to manage complex supply chains supporting automotive, electronics, machinery, and industrial equipment production. Manufacturing companies require efficient transportation, inventory management, and supplier coordination to maintain production continuity and reduce operational costs. Third party logistics providers offer integrated services including inbound material logistics, warehouse management, and outbound product distribution. Industrial companies also benefit from advanced logistics technologies such as real time shipment monitoring and predictive supply chain analytics. Outsourcing logistics operations allows manufacturers to focus on core production capabilities while reducing fixed infrastructure investments. Large logistics providers maintain nationwide transportation fleets and distribution facilities that connect factories with domestic and international markets. The growing complexity of global manufacturing supply chains therefore strengthens demand for professional logistics management services. As production networks expand and supply chain coordination becomes more sophisticated, third party logistics providers continue gaining strategic importance across Japan’s industrial ecosystem.

Market Challenges

Severe Labor Shortages in the Logistics and Transportation Workforce

Japan faces significant labor shortages across the logistics and transportation sector due to an aging population and declining workforce participation. Truck drivers, warehouse operators, and logistics coordinators are increasingly difficult to recruit and retain across the country. The shortage of skilled logistics personnel limits operational capacity and increases labor costs for logistics service providers. Many logistics companies must invest heavily in automation technologies and digital management platforms to offset workforce limitations. Smaller logistics operators often struggle to compete with large firms capable of deploying advanced warehouse robotics and automated sorting systems. Rising labor costs also increase operational expenses for logistics providers managing large transportation fleets and distribution centers. Delivery delays and service disruptions may occur when workforce shortages affect shipment scheduling and transportation availability. Government initiatives promoting logistics automation and workforce training aim to reduce labor shortages over time. However the demographic structure of the population continues creating structural workforce challenges across the logistics sector.

Rising Logistics Infrastructure Costs and Urban Distribution Constraints

Operating logistics infrastructure within Japan’s major metropolitan areas requires substantial investment in warehousing facilities, transportation fleets, and digital logistics technologies. Land prices and industrial property costs remain high in major logistics hubs such as Tokyo, Osaka, and Nagoya. Logistics providers therefore face significant capital requirements when expanding warehouse capacity near urban consumption centers. Traffic congestion and strict urban transportation regulations also create operational challenges for delivery fleets managing last mile shipments. Logistics companies must adopt route optimization software and delivery scheduling technologies to reduce operational inefficiencies. Environmental regulations and emission standards further increase transportation costs as logistics providers transition toward low emission vehicles and sustainable logistics practices. Smaller logistics firms often face difficulty financing large infrastructure investments required to remain competitive. These structural cost pressures can reduce profit margins across the industry. As logistics demand continues expanding, infrastructure investment requirements remain a significant operational challenge.

Opportunities

Expansion of Logistics Automation and Smart Warehouse Technologies

Increasing adoption of robotics, automated storage systems, and artificial intelligence driven warehouse management platforms creates significant opportunities for logistics providers operating in Japan. Automation technologies enable logistics companies to process large shipment volumes efficiently while reducing reliance on manual labor. Advanced warehouse robotics systems improve order picking accuracy, inventory visibility, and operational productivity within distribution facilities. Logistics providers also integrate real time data analytics platforms capable of optimizing inventory levels and shipment scheduling. Large logistics companies increasingly invest in smart warehouses equipped with automated conveyor systems, robotic picking technologies, and digital inventory tracking tools. These technological advancements allow logistics operators to manage complex supply chains more efficiently while maintaining high service reliability. The continued expansion of e-commerce fulfillment networks also increases demand for technologically advanced distribution facilities. As automation technologies become more cost efficient and scalable, logistics companies gain new opportunities to improve operational performance and expand service capabilities.

Growth of Cross Border Trade and International Freight Logistics Services

Japan maintains strong international trade relationships with major economies including China, the United States, South Korea, and European countries which generates continuous cargo movement across global logistics networks. Export oriented manufacturing industries depend on efficient international freight forwarding services to deliver products to overseas markets. Third party logistics providers coordinate multimodal transportation, customs documentation, and cargo consolidation services supporting international trade operations. Logistics providers also benefit from increasing demand for integrated freight solutions that combine air, sea, and land transportation services. Expansion of global supply chains increases the need for logistics companies capable of managing complex cross border shipment flows. Digital freight platforms and shipment visibility technologies further improve cargo tracking and operational efficiency across international logistics networks. As international trade volumes continue expanding, third party logistics providers gain significant opportunities to strengthen their presence within global supply chain management services.

Future Outlook

The Japan 3PL market is expected to experience steady expansion supported by rising logistics outsourcing across manufacturing and retail sectors. Continued growth of e-commerce fulfillment and last mile delivery networks will increase demand for advanced warehousing and transportation services. Logistics automation, robotics, and digital supply chain platforms will play an important role in improving operational efficiency. Government support for logistics modernization and infrastructure development is also expected to strengthen industry capabilities.

Major Players

- Nippon Express Holdings

- Yamato Holdings

- Sagawa Express

- Kintetsu World Express

- Yusen Logistics

- Nissin Corporation

- Sankyu Inc

- Seino Holdings

- Mitsui-Soko Holdings

- Fukuyama Transporting

- DHL Supply Chain Japan

- DB Schenker Japan

- CEVA Logistics Japan

- Kuehne + Nagel Japan

- Hitachi Transport System

Key Target Audience

- Logistics and supply chain companies

- Manufacturing and industrial companies

- Retail and e-commerce companies

- Automotive manufacturers

- Pharmaceutical and healthcare companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying critical variables influencing the Japan 3PL market including logistics infrastructure capacity, outsourcing demand, e-commerce shipment volumes, and supply chain integration technologies. Secondary industry sources and government logistics reports help determine the most relevant parameters for market evaluation.

Step 2: Market Analysis and Construction

Extensive secondary research is conducted using logistics industry databases, trade statistics, company financial reports, and transportation sector publications. Market structures, service segments, and supply chain networks are analyzed to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics executives, supply chain managers, and transportation analysts provide insights validating assumptions regarding market structure, service demand, and technology adoption across the sector.

Step 4: Research Synthesis and Final Output

All research findings are consolidated into structured market insights, combining quantitative logistics data with qualitative industry analysis to produce a comprehensive assessment of the Japan 3PL market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid expansion of e-commerce logistics networks

Increasing outsourcing of supply chain operations by manufacturers

Growth of automated warehousing and digital logistics technologies - Market Challenges

High labor costs and workforce shortages in logistics operations

Urban congestion affecting last mile delivery efficiency

Rising fuel and transportation infrastructure costs - Market Opportunities

Expansion of robotics driven smart warehouses

Growth of cross border e-commerce logistics services

Increasing demand for temperature-controlled logistics solutions - Trends

Adoption of AI driven logistics optimization platforms

Expansion of sustainable logistics and electric delivery fleets - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Transportation Management Services

Dedicated Contract Logistics

Integrated Supply Chain Solutions

Warehousing and Distribution Services

Value Added Logistics Services - By Platform Type (In Value%)

Road Freight Logistics Platforms

Rail Freight Logistics Platforms

Air Cargo Logistics Platforms

Maritime Logistics Platforms

Multimodal Logistics Platforms - By Fitment Type (In Value%)

Inhouse Contract Logistics Operations

Outsourced Third Party Logistics

Hybrid Logistics Management

Integrated Digital Logistics Platforms - By End User Segment (In Value%)

Retail and E-commerce Companies

Manufacturing and Industrial Enterprises

Automotive and Electronics Producers

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio, Warehousing Capacity, Transportation Network Coverage, Technology Integration, Fulfillment Speed, Industry Specialization, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Nippon Express Holdings

Yamato Holdings

SG Holdings

Hitachi Transport System

Kintetsu World Express

Mitsui-Soko Holdings

Sankyu Inc

Nissin Corporation

Sagawa Express

Fukuyama Transporting

DHL Supply Chain Japan

Kuehne + Nagel Japan

DB Schenker Japan

CEVA Logistics Japan

Yusen Logistics

- Retailers increasing reliance on outsourced fulfillment networks

- Automotive manufacturers requiring just in time logistics coordination

- Electronics producers demanding high precision distribution networks

- E-commerce marketplaces expanding nationwide delivery partnerships

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now