Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Japan aerospace and defense multi-functional display market is driven by increasing technological advancements and growing demand for enhanced situational awareness in military and defense applications. In 2023, the market was valued at approximately USD ~billion, driven by a shift towards advanced display technologies, such as OLED and LCD, for enhanced operational efficiency and clarity. In 2024, the market is expected to grow significantly as military forces demand displays that provide integrated information for better decision-making and performance. The growth in defense spending and strategic initiatives to modernize military systems is further propelling the market.

The market is dominated by countries such as Japan, the United States, and several European nations, owing to their technological advancements, substantial investments in defense infrastructure, and the demand for sophisticated, multi-functional display systems in both military and commercial aviation sectors. Japan remains a key player due to its strong defense and aerospace industry, coupled with its government’s increasing focus on military modernization. The United States, with its significant defense budget and emphasis on next-gen avionics, further strengthens its dominance in this sector.

Market Segmentation

By System Type

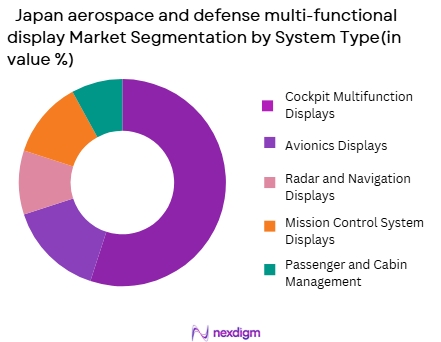

The Japan aerospace and defense multi-functional display market is segmented by system type into avionics displays, radar and navigation displays, cockpit multifunction displays, mission control system displays, and passenger and cabin management displays. Cockpit multifunction displays hold the dominant market share in 2024. These displays are pivotal in enhancing pilot situational awareness by integrating various information systems into a single interface. This market segment’s dominance is attributed to the consistent demand for integrated cockpit displays in both military and commercial aircraft, where real-time data access is crucial for mission success and flight safety. Moreover, the demand for multifunctional capabilities in a single display unit is further driving the growth of this segment.

By Platform Type

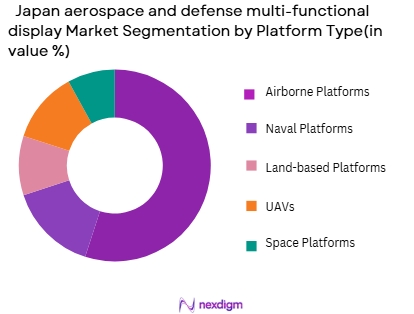

The platform type segmentation of the market includes airborne platforms, land-based platforms, naval platforms, unmanned aerial vehicles (UAVs), and space platforms. Airborne platforms dominate the market share in 2024, accounting for a significant percentage. This segment is driven by the high demand for multi-functional displays in military aircraft, which require advanced avionics and navigation systems for efficient operation. The constant upgrade of military aircraft fleets and the increasing adoption of advanced cockpit displays for better mission performance are pivotal in making airborne platforms the dominant category. Furthermore, commercial aviation’s increasing use of advanced cockpit displays for navigation and safety also contributes to the growth of this segment.

Competitive Landscape

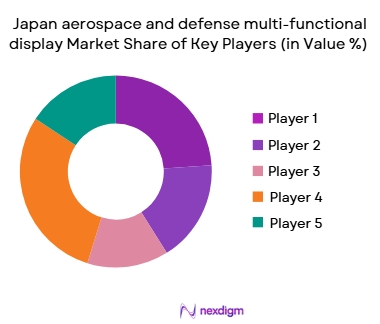

The Japan aerospace and defense multi-functional display market is highly competitive, with a few key players holding a significant share. Major players include companies such as Honeywell Aerospace, Thales Group, and Rockwell Collins, which dominate the market due to their advanced technological solutions and extensive product portfolios. These companies focus on providing high-quality, integrated display solutions that cater to both military and commercial aviation requirements. Additionally, newer entrants like Elbit Systems and Saab Group are emerging as important competitors, offering innovative products to meet evolving industry demands.

| Company | Year of Establishment | Headquarters | R&D Investment | Product Portfolio | Market Presence | Strategic Partnerships | Technological Innovations |

| Honeywell Aerospace | 1906 | United States | High | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | France | High | ~ | ~ | ~ | ~ |

| Rockwell Collins | 1973 | United States | Medium | ~ | ~ | ~ | ~ |

| Elbit Systems | 1966 | Israel | Medium | ~ | ~ | ~ | ~ |

| Saab Group | 1937 | Sweden | Medium | ~ | ~ | ~ | ~ |

Japan aerospace and defense multi-functional display Market Analysis

Growth Drivers:

Increased Defense Budgets and Modernization Programs:

Governments, particularly in Japan and other key aerospace nations, are investing heavily in defense budgets and military modernization programs. This focus on upgrading existing systems, including avionics and cockpit displays, drives the demand for advanced multi-functional displays. These investments are essential to improve operational efficiency, ensure enhanced situational awareness, and incorporate new technologies into military and aerospace platforms.

Technological Advancements in Display Systems:

The rapid development of cutting-edge display technologies, such as OLED, flexible displays, and augmented reality (AR), is significantly contributing to the growth of the market. These innovations enable the creation of more efficient, clear, and multifunctional display systems that improve pilot and operator decision-making. As aerospace and defense systems require increasingly sophisticated solutions, these technologies are becoming vital in enhancing performance and safety.

Market Challenges:

High Development and Integration Costs:

The development and integration of multi-functional displays into aerospace and defense systems can be expensive, involving high research and development costs, advanced manufacturing techniques, and rigorous testing and certification processes. These high costs can pose significant challenges, particularly for smaller companies or nations with limited defense budgets, affecting the affordability and scalability of these technologies.

Complexity in System Integration with Legacy Platforms:

Many military and aerospace systems use legacy technologies that are difficult to integrate with new multi-functional displays. The integration process often requires extensive modifications to existing infrastructure, leading to additional costs, delays, and operational challenges. These obstacles hinder the swift adoption of advanced display systems and reduce the efficiency of modernization programs.

Opportunities:

Expansion in Commercial Space Exploration:

With the growing interest in commercial space exploration and the increasing involvement of private companies like SpaceX, Blue Origin, and others, there is a significant opportunity for multi-functional displays in space systems. As space missions become more complex and require advanced data management, the demand for high-quality, multifunctional displays for navigation, communication, and monitoring is expected to rise, opening new markets for aerospace display manufacturers.

Rise in Unmanned Aerial Vehicles (UAVs):

The increasing use of UAVs for both military and civilian applications presents an opportunity for the aerospace and defense multi-functional display market. UAVs require highly integrated, compact, and advanced display systems for flight control, navigation, and surveillance. As the adoption of UAVs expands, there will be a growing demand for specialized multi-functional displays, presenting new growth avenues for industry players.

Future Outlook

Over the next ~ years, the Japan aerospace and defense multi-functional display market is expected to experience steady growth, driven by increased investments in advanced avionics systems, government defense budgets, and the rising demand for enhanced mission-critical display systems. The evolution of display technologies, such as flexible OLED displays and augmented reality (AR) integration, will play a pivotal role in shaping the future of the market. These technological advancements will enable military and aerospace platforms to enhance their operational capabilities and situational awareness.

Major Players

- Honeywell Aerospace

- Thales Group

- Rockwell Collins

- Elbit Systems

- Saab Group

- Garmin

- Curtiss-Wright

- BAE Systems

- Collins Aerospace

- Raytheon Technologies

- Northrop Grumman

- Leonardo

- Mitsubishi Electric

- L3 Technologies

- Panasonic Avionics Corporation

Key Target Audience

- Military Organizations (Japan Ministry of Defense)

- Aerospace and Aviation Manufacturers

- Defense Contractors

- Government Agencies

- Aerospace Technology Firms

- Investments and Venture Capitalist Firms

- Aviation and Defense Regulatory Bodies (FAA, EASA)

- OEMs and System Integrators

Research Methodology

Step 1: Identification of Key Variables

The initial step includes identifying the key drivers, challenges, and growth factors that influence the Japan aerospace and defense multi-functional display market. Through extensive desk research, secondary data sources, and proprietary databases, critical variables such as technological advancements, government policies, and demand for defense modernization are identified and mapped.

Step 2: Market Analysis and Construction

This phase involves collecting historical data related to the Japan aerospace and defense multi-functional display market. The analysis focuses on factors such as technological integration, the rate of adoption of advanced display systems, and evolving customer needs. Revenue generation data and trends are evaluated to understand market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

In this phase, market hypotheses developed through earlier steps are validated by conducting interviews with industry experts, such as military personnel, aerospace manufacturers, and display system developers. These interviews help verify the assumptions and provide in-depth insights into operational practices and technological trends.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing all research findings into actionable insights. This includes detailed analysis of market segments, technological trends, and future projections. Direct engagement with key manufacturers and stakeholders in the aerospace and defense industry provides valuable feedback, ensuring a well-rounded and accurate report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing defense spending

Technological advancements in display systems

Rise in demand for enhanced situational awareness - Market Challenges

High costs of development and production

Complex integration with legacy systems

Stringent regulations and certification requirements - Market Opportunities

Expansion of military modernization programs

Increasing use of multi-functional displays in UAVs

Growth in commercial space exploration - Trends

Adoption of high-definition displays

Integration of augmented reality features

Shift towards OLED and flexible display technologies - Government regulations

Military display system certifications

Aerospace industry environmental standards

Civil aviation display system regulations - SWOT analysis

- Porters 5 forces

- By Market Value,2020-2025

- By Installed Units,2020-2025

- By Average System Price,2020-2025

- By System Complexity Tier,2020-2025

- By System Type (In Value%)

Avionics displays

Radar and navigation displays

Cockpit multifunction displays

Mission control system displays

Passenger and cabin management displays - By Platform Type (In Value%)

Airborne platforms

Land-based platforms

Naval platforms

Unmanned aerial vehicles (UAVs)

Space platforms - By Fitment Type (In Value%)

OEM fitment

Retrofit fitment

Modular fitment

Custom fitment

Universal fitment - By EndUser Segment (In Value%)

Military

Commercial aviation

Government agencies

Private aerospace companies

Space exploration agencies - By Procurement Channel (In Value%)

Direct purchase

Third-party resellers

OEMs

Government procurement

Online distribution

- CrossComparison Parameters(Market value, Installed units, Price range, Technology integration, Regional adoption)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Panasonic Avionics Corporation

Honeywell Aerospace

Rockwell Collins

Thales Group

Curtiss-Wright Corporation

Boeing

Lockheed Martin

Raytheon Technologies

L3 Technologies

Northrop Grumman

Elbit Systems

Saab Group

Leonardo

Meggitt

Garmin

- Increased demand for displays in military aircraft

- Adoption of multi-functional displays in commercial aircraft

- Integration of advanced technologies in military vehicles

- Government initiatives to modernize aerospace systems

- Forecast Market Value,2026-2035

- Forecast Installed Units,2026-2035

- Price Forecast by System Tier,2026-2035

- Future Demand by Platform,2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now