Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Japan Airport Information System market current size stands at around USD ~ million, supported by sustained modernization spending and rising digital adoption across major aviation hubs. Recent technology upgrades and platform integrations generated investments of USD ~ million, while active deployments surpassed ~ systems across terminals and airside operations. Operational digitization initiatives also drove recurring service revenues of USD ~ million, reflecting growing reliance on integrated information platforms for real-time coordination and performance monitoring across complex airport environments nationwide.

Tokyo and Osaka remain dominant deployment centers due to dense passenger flows, multi-terminal infrastructure, and mature digital ecosystems. These regions benefit from advanced ICT networks, high concentration of system integrators, and strong collaboration between airport authorities and technology providers. Policy-backed smart airport programs further accelerate adoption in these cities, while regional hubs in Chubu and Kyushu follow through phased modernization aligned with tourism growth, disaster resilience planning, and long-term capacity expansion strategies.

Market Segmentation

By Application

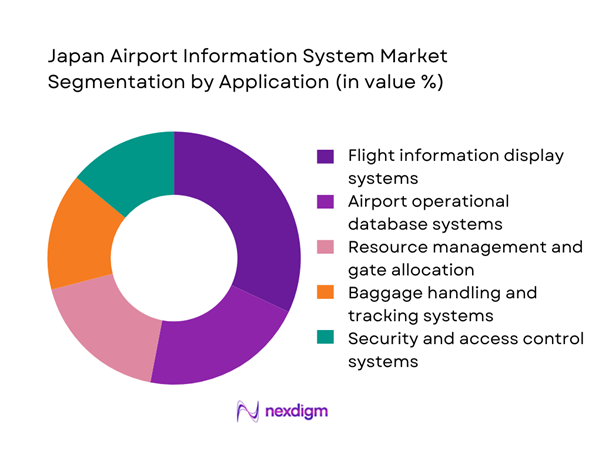

Passenger-facing systems dominate this segmentation as airports prioritize seamless travel experiences and operational efficiency. Flight information displays, self-service kiosks, and integrated wayfinding platforms attract the largest technology budgets, driven by the need to manage complex terminal flows and reduce manual intervention. Operational applications such as resource management and baggage tracking follow closely, reflecting airports’ focus on minimizing turnaround times and service disruptions. Security and access control solutions also gain prominence due to evolving safety requirements and digital identity adoption. Overall, application-led spending continues to shape procurement strategies, with airports favoring modular platforms that integrate passenger services and backend operations into unified information ecosystems.

By Technology Architecture

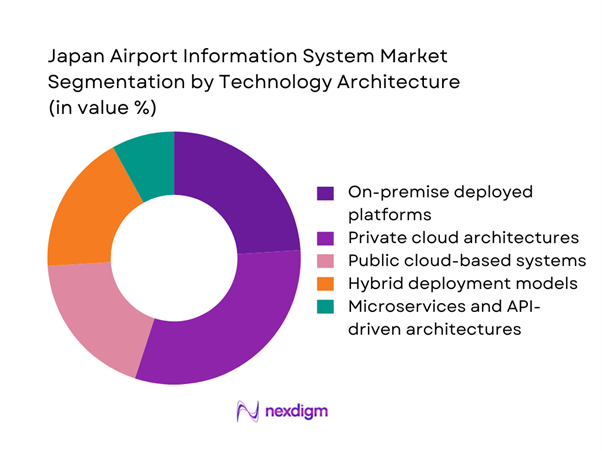

Hybrid and cloud-based architectures dominate as airports transition from rigid on-premise systems to more scalable and resilient platforms. Private cloud deployments lead in mission-critical operations where data sovereignty and latency control remain priorities, while public cloud adoption grows in analytics and passenger engagement layers. Hybrid models bridge legacy environments with modern microservices, enabling phased upgrades without disrupting live operations. API-driven architectures further strengthen interoperability across airlines, ground handlers, and airport authorities. This architectural shift reflects long-term strategies to reduce infrastructure complexity, enhance cybersecurity posture, and support rapid service innovation across increasingly connected airport ecosystems.

Competitive Landscape

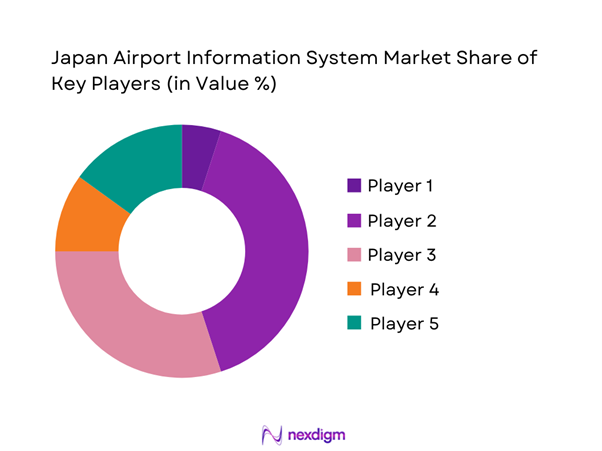

The market shows moderate concentration, with a core group of domestic technology leaders and a few global aviation IT specialists shaping large-scale deployments. Long-term framework contracts, high switching costs, and deep integration requirements favor established vendors, while niche providers compete in analytics, biometrics, and cloud orchestration layers.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| NEC Corporation | 1899 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Fujitsu Limited | 1935 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Hitachi Ltd. | 1910 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| SITA | 1949 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

| Amadeus IT Group | 1987 | Spain | ~ | ~ | ~ | ~ | ~ | ~ |

Japan Airport Information System Market Analysis

Growth Drivers

Rising passenger traffic at international hubs

Between 2022 and 2025, passenger throughput at major international gateways expanded to ~ million travelers annually, increasing pressure on legacy information systems. Airports responded with investments of USD ~ million in real-time data platforms to manage ~ flights per day and coordinate ~ operational processes across terminals. The surge in international connections also led to deployment of ~ new digital touchpoints for passengers, including self-service kiosks and mobile interfaces. These volumes reinforced the need for integrated airport information systems capable of handling ~ data transactions daily while maintaining service continuity and operational resilience.

Government-led smart airport modernization programs

Public-sector modernization initiatives from 2022 onward directed funding of USD ~ million into airport digitization programs covering ~ facilities nationwide. These programs supported the rollout of ~ smart systems focused on traffic flow optimization, emergency response coordination, and asset management. Policy-backed procurement cycles accelerated the replacement of ~ legacy platforms with integrated digital architectures, improving system uptime across ~ operational zones. As a result, airports achieved measurable gains in service reliability and infrastructure utilization, reinforcing the role of government programs as a structural growth catalyst for advanced information system deployments.

Challenges

High capital expenditure and long procurement cycles

Large-scale airport information system upgrades typically require upfront investments of USD ~ million per project, creating budget constraints for regional and secondary airports. From 2022 to 2025, average procurement timelines extended to ~ months due to multi-stage approvals, compliance checks, and integration planning across ~ stakeholder groups. These long cycles delay technology refresh rates and slow the adoption of innovative platforms. Financial pressures also limit the ability of smaller operators to deploy ~ advanced modules simultaneously, leading to phased implementations that reduce the immediate impact of modernization efforts.

Complex integration with legacy airport infrastructure

A significant portion of airport operations still relies on ~ legacy platforms installed over ~ years ago, making seamless integration with modern systems technically challenging. Between 2022 and 2025, airports reported spending USD ~ million annually on middleware and interface development to connect ~ disparate systems. The presence of ~ proprietary protocols and aging hardware increases project risk and extends deployment timelines. These complexities often require extended testing across ~ operational environments, raising costs and limiting the speed at which airports can fully transition to unified information ecosystems.

Opportunities

Greenfield airport developments and terminal expansions

New airport projects and terminal expansions between 2022 and 2025 unlocked investments of USD ~ million for integrated digital infrastructure. Each greenfield facility typically deploys ~ systems across passenger processing, operations control, and security management from the outset. This environment enables vendors to implement end-to-end information platforms without legacy constraints, accelerating time-to-value. With ~ new terminals planned or under construction, demand for scalable airport information systems continues to rise, offering long-term opportunities for solution providers to embed their platforms as core operational backbones.

Adoption of cloud-native airport management platforms

The shift toward cloud-native architectures drove spending of USD ~ million on platform migration and software modernization during 2022–2025. Airports transitioned ~ operational modules to cloud environments to improve scalability and disaster recovery capabilities. This resulted in deployment of ~ virtual systems supporting real-time analytics and remote operations management. Cloud-native adoption reduces dependency on on-site infrastructure and enables faster feature rollouts across ~ locations, positioning this trend as a key opportunity for technology providers offering secure, aviation-compliant digital platforms.

Future Outlook

The Japan Airport Information System market is set to evolve through deeper integration of cloud platforms, biometrics, and predictive analytics. Airports will increasingly prioritize resilience, cybersecurity, and interoperability as digital ecosystems expand. Regional hubs are expected to accelerate modernization in line with tourism growth and infrastructure renewal programs. Over the coming decade, collaboration between public authorities and technology providers will remain central to shaping a more connected and intelligent airport operations landscape.

Major Players

- NEC Corporation

- Fujitsu Limited

- Hitachi Ltd.

- Toshiba Corporation

- Panasonic Connect

- NTT Data Corporation

- SITA

- Amadeus IT Group

- Thales Group

- Indra Sistemas

- Collins Aerospace

- Honeywell International

- Siemens Mobility

- Atos SE

- IBM Corporation

Key Target Audience

- Airport authorities and terminal operators

- Airlines and ground handling service providers

- System integrators and aviation IT solution providers

- Investments and venture capital firms focused on smart infrastructure

- Ministry of Land, Infrastructure, Transport and Tourism Japan

- Civil Aviation Bureau of Japan

- Regional government airport development agencies

- Airport security and safety management organizations

Research Methodology

Step 1: Identification of Key Variables

Market scope definition, technology classification, and demand drivers were mapped across airport operations and passenger services. Key variables included deployment intensity, integration complexity, and regulatory alignment. Stakeholder roles across public and private entities were identified. This step established the analytical framework.

Step 2: Market Analysis and Construction

Data points on system adoption, investment flows, and modernization programs were consolidated. Operational models across large and regional airports were compared. Scenario mapping helped structure demand patterns. This stage shaped the core market narrative.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through expert interactions with airport IT managers and system architects. Assumptions on technology migration and procurement cycles were refined. Risk factors and adoption barriers were stress-tested. This ensured practical relevance of insights.

Step 4: Research Synthesis and Final Output

All inputs were synthesized into coherent market themes and strategic insights. Cross-segment linkages were evaluated. Final content was structured to support decision-making for investors and industry stakeholders. Quality checks ensured consistency and clarity.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, airport information system taxonomy across AODB FIDS and A CDM platforms, market sizing logic by airport count and system deployment scale, revenue attribution across software licenses integration and support services, primary interview program with airport operators IT teams and system integrators, data triangulation validation assumptions and limitations)

- Definition and Scope

- Market evolution

- Operational and passenger service pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising passenger traffic at international hubs

Government-led smart airport modernization programs

Growing need for real-time operational visibility

Expansion of contactless and digital passenger services

Increased focus on airport safety and security automation

Integration of AI and data analytics in airport operations - Challenges

High capital expenditure and long procurement cycles

Complex integration with legacy airport infrastructure

Cybersecurity risks in connected airport ecosystems

Shortage of skilled IT and systems integration talent

Regulatory compliance and certification delays

Resistance to change from traditional operational models - Opportunities

Greenfield airport developments and terminal expansions

Adoption of cloud-native airport management platforms

Growth of regional airports under tourism promotion policies

Partnerships between IT vendors and airport authorities

Demand for predictive maintenance and AI-driven operations

Export of Japanese airport system expertise to Asia-Pacific markets - Trends

Shift toward unified airport management platforms

Growing use of biometrics in passenger processing

Increased reliance on real-time data dashboards

Migration from on-premise to hybrid cloud models

Standardization of APIs for multi-vendor integration

Emphasis on resilience and disaster recovery systems - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

Commercial aviation fleets

Cargo and logistics aircraft fleets

Business and general aviation fleets

Military and government aviation fleets

Charter and regional carrier fleets - By Application (in Value %)

Flight information display systems

Airport operational database systems

Resource management and gate allocation

Baggage handling and tracking systems

Security and access control systems

Passenger processing and wayfinding platforms - By Technology Architecture (in Value %)

On-premise deployed platforms

Private cloud architectures

Public cloud-based systems

Hybrid deployment models

Microservices and API-driven architectures - By End-Use Industry (in Value %)

Large international airports

Regional and domestic airports

Airlines and airport operators

Ground handling and service providers

Air navigation service providers - By Connectivity Type (in Value %)

Wired Ethernet-based networks

Fiber optic communication systems

Private LTE and 5G networks

Public wireless networks

Satellite and backup communication links - By Region (in Value %)

Hokkaido

Tohoku

Kanto

Chubu

Kansai

Chugoku

Shikoku

Kyushu and Okinawa

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (deployment scale, regulatory compliance capability, cybersecurity maturity, system integration depth, service uptime SLAs, total cost of ownership, localization and language support, AI and analytics readiness)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

NEC Corporation

Fujitsu Limited

Hitachi Ltd.

Toshiba Corporation

SITA

Amadeus IT Group

Thales Group

Indra Sistemas

Collins Aerospace

Honeywell International

Siemens Mobility

Atos SE

NTT Data Corporation

IBM Corporation

Panasonic Connect

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now